Apples image via vickyb/flickr. Creative Commons 2.0 license.

The present debate about the Greek financial situation tends often to pit Greece against the rest of the Eurozone. As an example, Oerstrom Moeller writes that:

Since 2010 the Eurozone economy has turned around from contraction to growth – the growth forecast for 2015 is 1.5 percent, work to set up a banking union is well under way, and measures constituting bulwarks have been put in place. The little stroke can fell great oakes was a proverb that ominously sounded in the corridors 4-5 year ago; not any longer.

and

Unless Greece is willing to restructure its economy implementing policy objectives and instruments used by the majority of the EU member countries why should the Eurozone bail it out? What is the virtue of having a member that consistently and continually refuse to bring its economy into a shape similar to the one that the rest of the club is running. Ireland, Portugal, Spain, and Italy have all gone through painful reforms and been rewarded with a much improved economic situation and a promising outlook for the future. What are the arguments for not asking Greece to do the same?

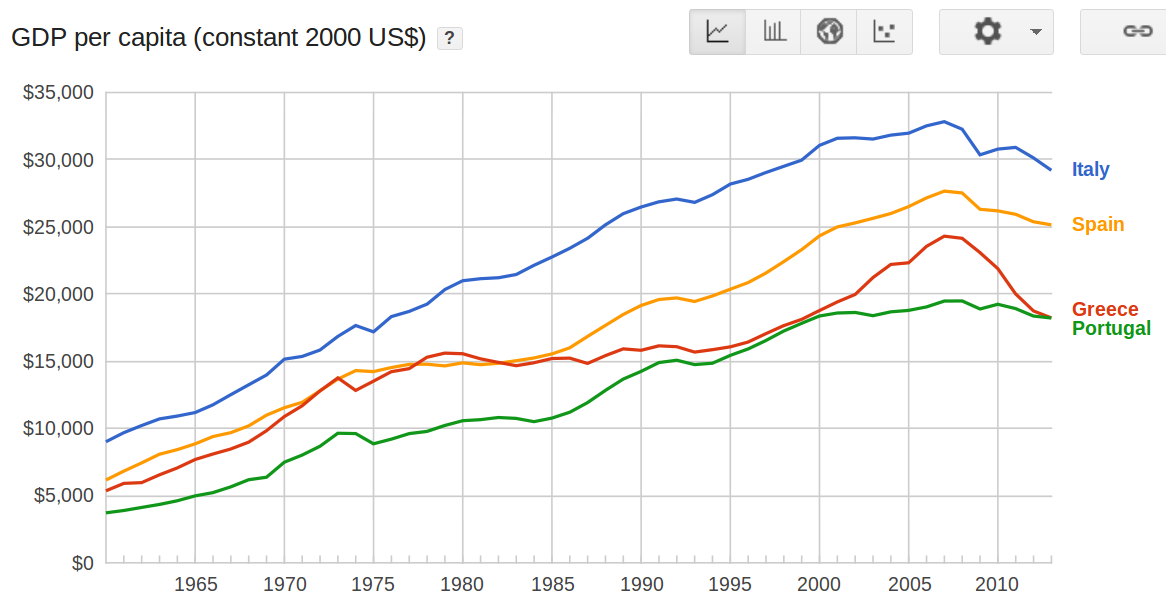

Unfortunately, the data tell a different story. Greece is not alone in having economic problems and all the Southern European countries tend to show similar trends. For instance in terms of GdP per capita, the Greek decline is sharper than that of the others, but not qualitatively different. (image from Google public data)

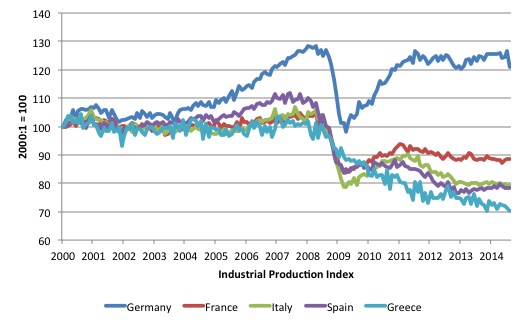

If this were not enough, take a look at the industrial production data (from Bilbo Economic Outlook). Greece is sinking, yes, but so are Italy and Spain, and France is hardly doing better.

There are other data showing similar trends: in short, Greece is not the bad apple of the bunch, but simply the weakest member of a group of countries that could never recover after the 2008 crisis.

As I wrote in an earlier post about Greece, financial factors may be simply a reflection of a much deeper trouble. And this trouble was already identified long ago in the study titled "The Limits to Growth", published in its first version in 1972. Note how the results of the "Limits" model (below taken from the 2004 version of the study) are similar to the decline observed in the GdP and the industrial production index of the southern European countries.

If the "Limits" model describes the present situation, then the Greek decline is not a direct consequence of problems with the Euro or with wrong policies of the Greek government. Rather, the causes at the root of the decline can be identified as the gradual increase of the costs of production of natural resources – and of energy in particular – coupled with the increasing costs of fighting pollution.

These factors affect the weaker economies first, and there is no doubt that Greece is one. Weaker than others, but not different in its structure. So, the problem cannot be solved by purely financial measures: we need to go to the root of it. We have to free the world’s economy from its dependency on fossil fuels and transform it into a "circular" economy, not any more dependent on badly depleted mineral resources. It can be done (it is described, for instance, in this recent report by the Ellen McArthur foundation). But we should have started much earlier; now it may be too late for Greece to avoid major damage (and, most likely, also for the rest of the world).