One of the current mysteries of British political economy is that our privatised water companies have promised to spend £10 billion to improve our sewage infrastructure, but that we’re all going to pay for it—while they are still paying billions of pounds to their shareholders.

Another mystery is the plight of Thames Water, Britain’s largest water company, at risk of financial collapse while sitting on £4.4 billion of cash, whose Chief Executive, Sarah Bentley resigned “with immediate effect” earlier this week. (This may be less of a mystery: Thames has £13.4 billion of debt, leakage rates are at a five-year high, and it is being repeatedly fined for discharging raw sewage.)

Rentier capitalism

As Mathew Lawrence noted in a piece in The Guardian:

Who, then, benefits from this model, if neither people nor planet? International investors, for one… It’s a self-defeating arrangement in which England and Wales are global outliers: indeed, they are globally exceptional in having wholly privatised water systems.

While trying to understand these mysteries, I came across a shortish review of Brett Christophers’ recent book Our Lives in Their Portfolios: Why Asset Managers Rule the World, by the economist Diane Coyle, that seemed to have much of the answer in it.

Over the course of a series of books, Christophers has researched the nature of different forms of rentier capitalism—in Britain and elsewhere. His latest book focuses on the way the infrastructure sector is financed in the post-privatisation era, in Britain and elsewhere.

(Image: Verso Books)

Long-term investments

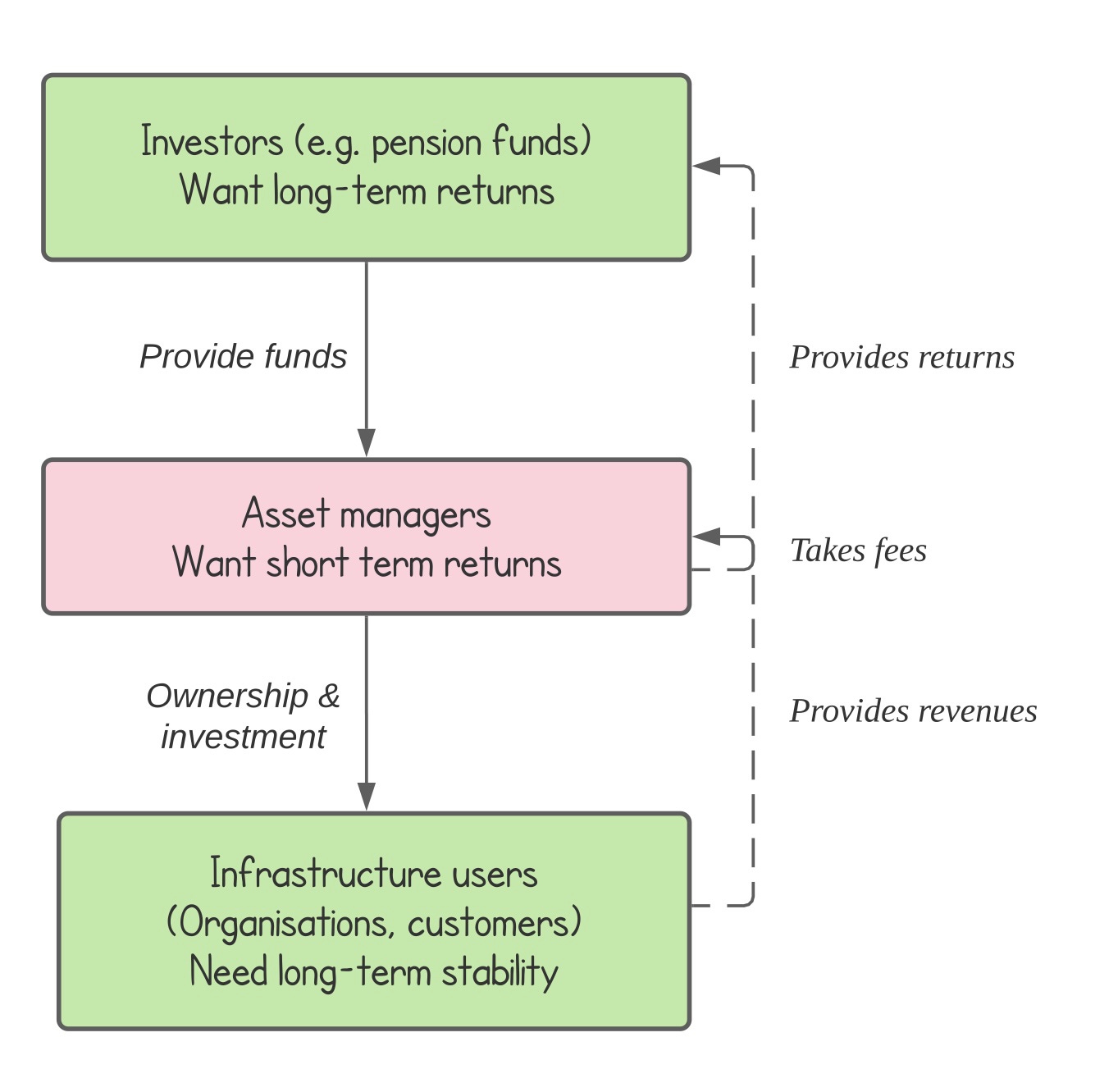

Britain’s physical infrastructure — water, energy, etc — is largely owned, and opaquely, by asset managers such as Macquarie and Blackstone. There are several features of infrastructure. Typically, it is a “natural monopoly”—there’s no point in having multiple sets of water and sewage pipes connected to a household, for example.

It also is a long-term investment—I was once told by Transport for London that a typical London station might be refurbished every 60 years. Most infrastructure, outside of the road network, comes with steady revenue streams attached. And this means that the investors who like to have infrastructure investments in their portfolio are often investors such as pension funds, which have long-term liabilities. So, when asset managers—which have shorter term horizons—insert themselves here there is a mismatch:

However, while the investors have long term horizons and look for steady returns (such as rents or fee income), and the infrastructure itself is long-lived, the funds set up by the asset managers coming in between are short term – a few years at most.

Middlemen

I thought it might be worth drawing a diagram to spell this out.

(Source: Andrew Curry)

It’s also worth noting a couple of other features here. The asset managers typically commit only a fraction of their own money (e.g. typically 1-5%) to the funds that they manage that actually own the infrastructure assets but the rewards they get for their role here are on a scale somewhere between “disproportionate” and “eye-watering”.

Brett Christophers appeared on the podcast A Long Time in Finance, hosted by Jonathan Ford and Neil Collins to talk about the book (30 minutes), and mentioned that Blacktone’s average salary was $2 million, funded by management fees of 12%. (I had to replay this bit of the recording to check I’d heard it right). It’s also not clear what they’re really doing for their money, as Coyle notes:

As all the operational aspects are contracted out to service companies, the asset managers are neither energy or water companies, nor investors in such companies: they are pure rentiers. The risks are borne entirely by others – and particularly the people experiencing crumbling homes or essential services.

Moral hazard

So—if you were drawing this model up from scratch, on a blank piece of paper—you’d say either that this misalignment problem is so severe that you should look for a different model (e.g. public interest companies, as in the case of the Welsh water company Dŵr Cymru), or ensure that regulation is broad enough to remove the obvious moral hazard that is involved (which is the sewage problem in a nutshell).

In fact, certainly in the UK, regulation has been captured by narrow definitions of market competition and consumer harm. On the Long Time in Finance podcast, one of the interviewers reminded me that the water regulator Ofwat had had a decision that reduced returns to investors overturned by the Competition and Markets Authority.

Similarly, they noted the ratchet effect that seemed to apply to the companies’ dealings with regulators—effectively a kind of bluff whereby the owners suggest that if the regulators tighten regulation, the investors will walk away, but so far a bluff that hasn’t been called. This may be naivety or it might because there’s a significant degree of regulatory capture in the way that the regulators behave.

Ransacked for rent

On the podcast, Christophers suggested that the reason we see our infrastructure companies

being ransacked for rent, with maximum income being extracted from them, and minimum cost being undertaken, is because the nature of the asset management model requires that to be the case. So investment funds raise money from funds by promising them higher returns than they are able to get through … investment in other asset classes, and the way they recruit their investment professionals is by offering them higher salaries and higher bonuses than they will get from McKinsey.

The gap here is that after the asset owners have extracted their share, the returns to the pension funds—and therefore to pensioners—are no higher than they would have been had they invested in other things. The share taken by the asset owners is almost pure extraction.

As Diane Coyle says:

While I don’t have a problem with the idea of private money coming into infrastructure investment, there is a clear incentive issue: as Avner Offer’s excellent recent (2022) book Understanding the Private-Public Divide set out, private money will always require pay-back faster than a major piece of infrastructure can deliver, so there are challenges in structuring the investment and governance. And the lack of transparency and failures of governance over the maintenance and operation of infrastructure and housing, resulting from the financialized structure of the investment through asset managers, are shocking.

One of the frustrating things about both the review and the podcast is that both seemed a bit blank on what to do about this. (This was a bit depressing, since Diane Coyle is one of the best public policy economists in the UK: she hopes that “the first step is clearly the disinfectant of light”, which is about half way down Donella Meadows’ list of places to intervene in the system.}

Calling the bluff

Certainly in the UK, it’s a consequence of the way that privatisation of public utilities was structured—one of those second-order effects that those brainboxes at the Treasury didn’t figure out might happen. (Some soft simulation work to understand how actors might actually behave might have helped).

But the reason that the pension funds go through the asset managers is because they have to: the asset managers are the owners. And the asset managers are the owners because they can squeeze out the type of generous returns that support $2 million average salaries. It’s another example of businesses extracting value to get high returns in an increasingly low return world.

Utility businesses should be dull businesses with steady but unspectacular returns that generate enough money to maintain themselves over time and pay for upgrades when necessary. What we’ve actually got is a sector where returns are set without apparent regard for long-run costs or investment requirements, or social or public need. In the short term, there are ways to both tighten and redesign regulation to bring these back into line. Change the rules, change the goals: push it higher up Donella Meadows’ list. Call the bluff, in other words.

Other models

But frankly, that would be patching over a system that was an error in the first place. When you are an outlier, it should provoke questions as to why. But being an outlier does mean that there are plenty of other models to borrow from that would work better, both in Europe and even closer to home. And there’s nothing like a bankruptcy to provide an opportunity, even if Britain’s Conservative government always turns these opportunities down (they used to happen regularly in the rail sector, where the publicly managed version of the service always performed better than a failed commercial franchise.)

Mathew Lawrence, for example, pointed to the example of Scotland:

(W)e have a readymade comparison in Scotland, which effectively resisted the privatisation of Scottish Water. The contrast between the two is stark: users in the rest of the UK spent an estimated 10% more on water bills than those in Scotland, and the publicly owned company invested 35% more per household per year than private firms in England.

There’s a short ‘trailer’ interview with Brett Christophers about the book on the Verso Books site (1’11”).