In 2023, the U.S. set an annual oil (crude oil + condensate) production rate record of 12.927 million barrels/day (mb/d) according to the U.S. Department of Energy/Energy Information Administration (U.S. DOE/EIA or EIA). I’ve heard numerous media commentators ebulliently commenting about that fact without considering the implications for future U.S. oil production. Those implications are serious and not that far away.

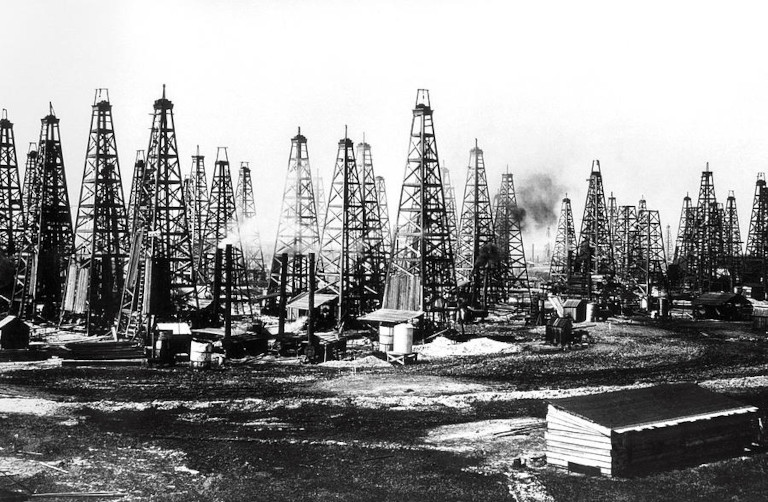

The fact that U.S. oil production reached a very high level in 2023 and that so much of the production came from Texas made me think of the first major Texas oil bonanza, Spindletop (Figure I).

Figure I-Spindletop oil field

Spindletop was discovered in 1901. The first well, the Lucas Geyser, had a flow rate of 100,000 b/d upon discovery, more than all the world’s oil wells combined at the time. A feeding frenzy ensued at Spindletop after the Lucas Geyser discovery which led to intense development of the field as Figure I illustrates.

In the early days of Spindletop, oilmen thought that the high production rate for the field would last forever but production fell off rapidly after 1902 and Patillo Higgins, the individual who discovered the field, said something to the effect, “It was milked hard and furthermore, not too intelligently”. The 2023 U.S. oil production situation has similarities to Spindletop in terms of oil plays being milked hard and I would say, not too intelligently.

Oil production in the U.S. is now dominated by five shale plays: Permian Basin, Eagle Ford, Bakken, Niobrara and Anadarko. The Permian Basin, Eagle Ford and Bakken combined produce approximately 90% of all U.S. tight oil production. The five tight oil plays have been milked hard since the start of modern fracking in ~2008, and particularly hard in 2023.

Oil obtained from shale plays is identified as tight oil and it’s obtained through the techniques of horizontal drilling combined with fracking.

Oil production data in this report are from the EIA unless otherwise specified. For this report, I’m only considering crude oil + condensate, what is typically referred to as oil. Some data for 2024 has been included to illustrate how production is going this year through April, the most recent data from the EIA.

The Importance of Shale Plays for U.S. Oil Production

To highlight where the tight oil plays are located in the U.S., Figure II is a map showing the prominent tight oil and gas plays:

Shale Oil and Gas Plays in the U.S.

Figure II

The five prominent shale oil plays provided approximately 9 mb/d of production out of a total U.S. production of approximately 13 mb/d in 2023, ~70% of total U.S. oil production. The Permian Basin alone produced approximately 6 mb/d (~45%) of total U.S. oil production and about two-thirds of tight oil production.

Deep water (>1000 feet) Gulf of Mexico (GOM) oil production added another ~1.9 mb/d of U.S. production in 2023. That leaves approximately 2 mb/d of oil production beyond tight oil and deep water GOM production and I’m including Alaskan oil production in that figure. Two mb/d is a long way from the 9.637 mb/d figure of U.S. oil production in 1970, which didn’t include production from northern Alaskan oil fields such as Prudhoe Bay and Kuparak.

Cumulative U.S. oil production, excluding 2008-2023 tight oil and deep water GOM production, was approximately 200 billion barrels for the period 1930 through 2023. For the period 2008-2023, cumulative U.S. oil production from tight oil was approximately 25 billion barrels and that from the deep water GOM was approximately 8 billion barrels.

The Permian Basin is Where the Action is

The Permian Basin is by far the highest oil producing shale play in the U.S. The other four prominent shale oil plays in the U.S. achieved maximum production prior to 2020 but the Permian Basin hasn’t thus far started to decline.

In recent months, monthly new oil production from the Permian Basin has been quite impressive with over 400,000 b/d of new production coming on-line based upon Drilling Productivity Reports from the EIA. Unfortunately declining production from older wells has been over 400,000 b/d so Permian Basin oil production has at best crept up only slowly in recent months.

A big problem with tight oil wells is that they decline rapidly soon after production starts. The vast majority of the oil production from a new tight oil well occurs in the first two years of production. In order to maintain or increase production in a shale play, new wells have to be brought on-line at a high rate to replace declining production from older wells.

Figure III is a graph of the number of active horizontal oil wells in the Permian Basin:

Figure III *Graph from Novi Labs

In the first seven months of 2023, 3,232 horizontal oil and gas wells came on-line in the Permian Basin1, roughly 460 new wells per month or approximately 5,500 per year. As of the end of 2023, the Permian Basin had over 45,000 producing oil and gas wells.1

A second problem for shale plays is that most of the production occurs in “sweet spots” that can be considerably smaller than the total shale play and those “sweet spots” don’t magically grow over time.

As an example, in the North Dakota portion of the Bakken play, over 90% of all production comes from four counties in a play that covers 16 counties within North Dakota. Over time, the “sweet spots” get saturated with wells ultimately leading to declining production. Initial production rates and ultimate recoveries per well are substantially greater on average for wells within the “sweet spot” counties of North Dakota compared to counties outside of the “sweet spot” but within the play.

Another problem for the Permian Basin was presented by petroleum geologist Art Berman recently in the video below when he stated that new wells drilled in 2023 may ultimately produce roughly half of what new wells from 2019 will ultimately produce:

https://www.youtube.com/watch?v=qqTh2nBEcCs

His speculation is that wells are now being drilled too close together and scavenging between wells is occurring.

Also in the video he states that new wells are coming in at higher initial flow rates than in the past but that they are declining at a faster rate. In recent years, the industry has concentrated their drilling on the most fruitful acreage available within shale plays and as Berman states, they are effectively using wider straws to extract the oil leading higher initial flow rates. It won’t be long before the most fruitful areas are played out in the Permian Basin. What the industry is doing is sacrificing future production to maximize short term production.

Numerous petroleum geologists and oil analysts have recognized that there are future problems with the Permian Basin and U.S. tight oil production in general. Here is a recent statement from an oil industry insider concerning future U.S. tight oil production:

“Shale will likely tip over in five years, and US production will be down 20 to 30% quickly. When it does—this feels like watching the steam roller scene in Austin Powers. Oil prices in the late 2020s will be something to behold.”

An industry executive responding to a poll by the Dallas Fed;

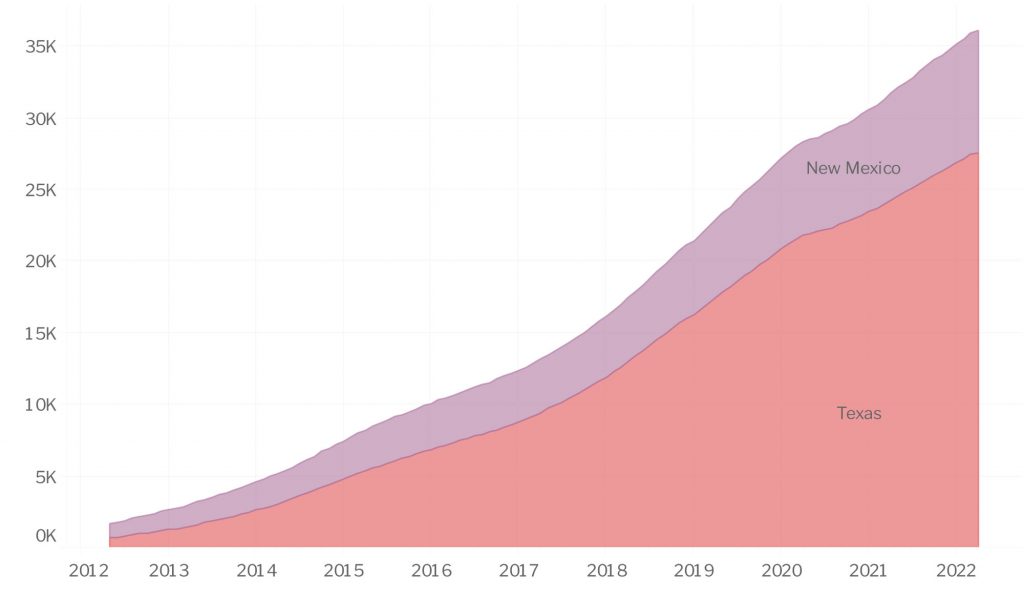

Figure IV is a graph of historical oil (crude oil + condensate) production from the Texas Permian Basin for 2008 through 2023:

Figure IV *Data are from the Railroad Commission of Texas **The numerical values in Figure IV represent oil production

Oil production from the Texas Permian Basin increased approximately 53,000 b/d from 2022 to 2023. While 53,000 b/d is not insignificant, the really large production increases for the Texas Permian Basin are becoming a distant memory.

Figure V is a graph of Texas oil production from 2010 through 2023:

Figure V

The Texas oil production rate reached its highest level in 2023 at 5.519 mb/d, an increase of 512,000 b/d over 2022. The lower production rates in 2020 and 2021 were due to the Covid pandemic and in the case of 2021, the extremely cold weather in February 2021 that reduced oil production for that month by approximately 20%, or about 1.0 mb/d.

It appears that there was some revival of conventional oil production in Texas in 2023 which may be comparable to giving an oldster Geritol, meaning a short-term revival.

Can Texas oil production increase beyond the production level of 2023? Time will tell.

Update: The April 2024 oil production rate for Texas was 22,000 b/d lower than the maximum monthly production rate in November 2023.

New Mexico’s oil production rate has risen dramatically in recent years, essentially all of it from the New Mexico portion of the Permian Basin. Figure VI is a graph of New Mexico’s oil production rate from 2010 through 2023:

Figure VI

New Mexico’s oil production rate increased 253,000 b/d in 2023, relative to 2022, to reach a rate of 1.826 mb/d. How long can production continue to increase in New Mexico? I expect that New Mexico’s oil production will reach a maximum within the next few years.

Update: New Mexico’s oil production was up 87,000 b/d in April 2024 relative to November 2023, when U.S. oil production reached a monthly peak in 2023.

What Goes Up Can Also Go Down

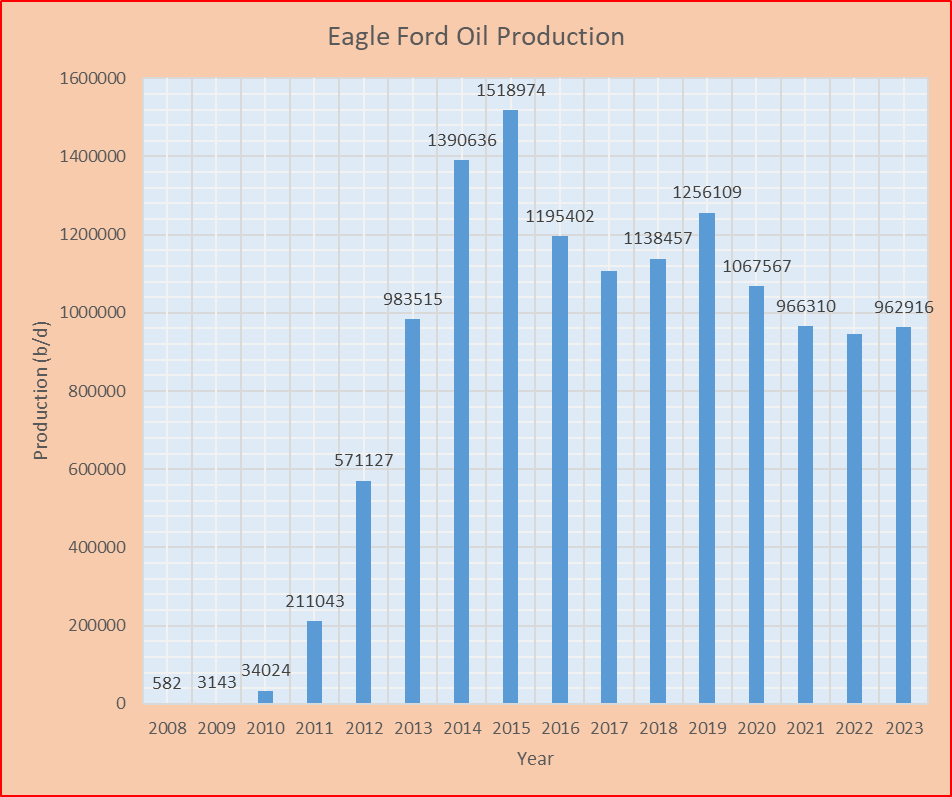

Figure VII is a graph of historical oil (crude + condensate) production from the Eagle Ford play for the period 2008 through 2023:

Figure VII *Data are from the Railroad Commission of Texas **The numerical values in Figure VI represent oil production

In 2023, the Eagle Ford oil production rate was 962,916 b/d, an increase of approximately 18,000 b/d over 2022. I expect the 2023 increase will be a temporary increase like what occurred in 2018/2019 for Eagle Ford. The Eagle Ford oil production rate reached its highest value in 2015 at 1,518,974 b/d. The 2023 production rate was off by 556,058 b/d relative to 2015, 36.6%.

Figure VIII is a graph of historical oil production from the Bakken region of North Dakota for the period of 2008 through 2023:

Figure VIII *Data are from the state of North Dakota

North Dakota Bakken oil production increased by approximately 121,500 b/d in 2023 relative to 2022. I view that as a temporary increase like what was observed for Eagle Ford in 2018/2019 (See Figure VII). The 2023 oil production rate was down 285,958 b/d relative to 2019, 19.9%.

Update: Production from the Bakkan portion of North Dakota was down 39,494 b/d in April 2024 relative to September 2023 (The maximum production month in 2023).

The production increase in 2023 was accompanied by a large increase in the number of producing oil wells, 1,484, from December 2022 to December 2023. There hadn’t been an increase in the number of wells of that magnitude since 2014. The number of producing wells as of December 2023 was nearly 3,000 more than in December of 2019 when North Dakota Bakken oil production was at its maximum.

The North Dakota Bakken oil production increase in 2023 was almost exclusively in the four “sweet spot” counties of Williams, Dunn, Mountrail and McKenzie. The majority of the increase in those counties (70.7%) was in the counties of Dunn and Williams. The areas exploited in the four “sweet spot” counties during 2023 won’t be available for exploitation in the future.

Petroleum geologist Art Berman makes the case that like the Permian Basin and Eagle Ford, estimated ultimate recovery (EUR) values per well for the Bakken play dropped approximately 50% from 2020 to 2023 even as production increased from 2022 to 2023.2 He argues that the production increase was due to the significant increase in the number of producing wells and delayed production increases from restored wells shut-in during the Covid pandemic.

Here is a statement from Art Berman’s recent report concerning the Bakken shale play:

The implications of this Bakken study and recent evaluations of the Permian and Eagle Ford plays are clear—this is the beginning of the end for the tight oil plays.2

A small portion of the Bakken shale play is located in Montana but Montana’s oil production rate is only about 5% of the North Dakota Bakken production rate.

Figure IX is a graph of the historical oil production rate for the Niobrara oil shale play from 2014 into 2024:

Figure IX3

The Niobrara oil shale play is mostly in Colorado and Wyoming but not all oil production in those two states necessarily comes from the Niobrara play. Figure X is a graph of the summed oil production from Colorado + Wyoming:

Figure X

Oil production from those two states increased 32,000 b/d in 2023 relative to 2022.

Update: The summed production from Colorado + Wyoming was down approximately 32,000 b/d in April 2024 relative to December 2023 (The maximum production month in 2023).

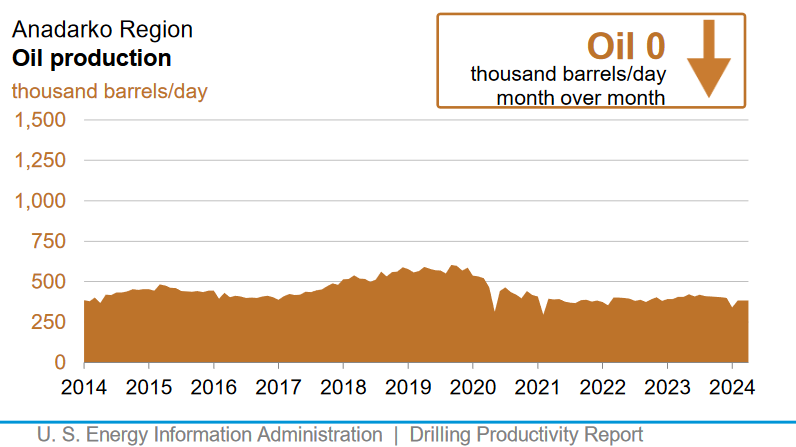

Figure XI is a graph of the historical oil production rate from the Anadarko shale play from 2014 into 2024:

Figure XI4

In my report “The Status of U.S. Oil Production” from 2022, I stated:

In both cases [Niobrara and Anadarko] it appears likely that production will not again reach the levels they had once attained.

I stand by that statement. Higher oil prices may lead to some short term production increases but I don’t see Niobrara production getting back to the ~800,000 b/d level or Anadarko getting back to the ~600,000 b/d level.

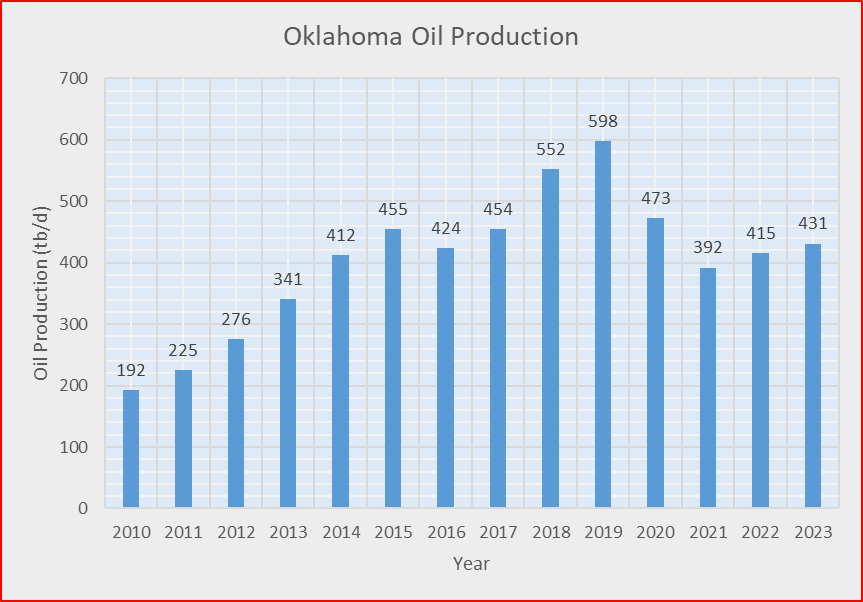

Anadarko is mostly located in Oklahoma. Figure XII is a graph of Oklahoma’s historical oil production from 2010 through 2023:

Figure XII

There was a 16,000 b/d increase in Oklahoma’s oil production in 2023 relative to 2022. Oklahoma’s oil production in 2023 was down 167,000 b/d relative to 2019, 27.9%.

Update: Oil production from Oklahoma was down 35,000 b/d in April 2024 relative to May 2023 (The maximum production month in 2023).

What’s happening in the Gulf of Mexico?

Figure XIII is a graph of historical oil production in the Gulf of Mexico (GOM) from 1985 through 2023. Displayed are shallow water and total GOM oil production:

Figure XIII

Total GOM oil production averaged 1.868 mb/d in 2023 versus 1.898 mb/d in 2019, the maximum production year for the GOM. The Bureau of Ocean Energy Management (BOEM) hasn’t been providing shallow and deep water oil production data for the last few years but almost all of the production is now from the deep water region (>1000 feet).

Table I contains an oil production forecast for the Gulf of Mexico from the BOEM through 2031:

Bureau of Ocean Energy Management Annual Production Forecast of 2022

| Year | Projected Oil Production (mb/d) | Actual Oil Production (mb/d) | Difference between Actual and Projected Production (b/d) |

| 2022 | 1.892 | 1.746 | -146,000 |

| 2023 | 2.000 | 1.868 | -132,000 |

| 2024 | 2.013 | ||

| 2025 | 2.052 | ||

| 2026 | 2.050 | ||

| 2027 | 2.062 | ||

| 2028 | 1.996 | ||

| 2029 | 1.943 | ||

| 2030 | 1.922 | ||

| 2031 | 1.850 |

Table I

I tend to be skeptical of oil production projections from U.S. government agencies such as the BOEM and EIA. Both agencies have a tendency to over estimate future oil production in their forecasts. That has been the case for the BOEM as illustrated in Table I and for the EIA as illustrated in Table II.

In their Annual Energy Outlook 2010 (AEO2010), the EIA projected future U.S. 48 States offshore oil production as listed in Table II. Also in Table II are actual production values and the difference between actual production values and the projected AEO2010 values.

U.S. 48 States Offshore Oil Production Projections

|

Year |

AEO2010 Projected Production (mb/d) | Actual Annual Production (mb/d)* | Difference Between Actual Production and AEO2010 Projected Production (b/d) |

| 2009 | 1.62 | ||

| 2010 | 1.67 | 1.61 | -60,000 |

| 2011 | 1.77 | 1.37 | -400,000 |

| 2012 | 1.82 | 1.31 | -510,000 |

| 2013 | 1.97 | 1.31 | -660,000 |

| 2014 | 1.95 | 1.45 | -500,000 |

| 2015 | 1.94 | 1.55 | -390,000 |

| 2020 | 2.08 | 1.68 | -400,000 |

| 2025 | 2.14 | ||

| 2030 | 2.19 | ||

| 2035 | 2.36 |

Table II * Production data are from the US DOE/EIA

The EIA has a consistent pattern of over estimating in their oil production forecasts as Table II illustrates.

Here is a statement I made in my report “The Status of U.S. Oil Production” from May 2022 concerning GOM oil fields:

To maximize profitability of deep water fields, the industry cranks up production rapidly to a high production level, say 100,000 b/d or more, but peak production is reached within a year or two and generally followed by rapid decline.

Decline rates of older deep water fields are at least 5%/year and generally considerably higher. That means the oil industry has to bring on new production of at least 100,000 b/d, and probably more like 200,000 b/d, each year just to maintain production at a constant rate.

Table III contains information on projected new developments in the GOM for the period of 2023 through 2025:

Projected New Deep Water GOM Developments for 2023 Through 2025

| Field | Projected On-Line Date | Projected Maximum Production (b/d) |

| Winterfell | Late 2023/Early 2024 | 100,000 |

| Anchor | 2024 | 5,000 |

| Whale | 2024 | 100,000 |

| Ballymore | 2025 | 75,000 |

| Leon/Castile | 2025 | 60,000 |

Table III

An article in the Journal of Petroleum Technology from April 2021 stated the following:

The US Energy Information Administration’s (EIA) latest short-term energy outlook is predicting a raft of new projects will increase crude oil production from the US Gulf of Mexico by 200,000 B/D by the end of next year. The forecast sees 13 new projects coming on stream over the next year-and-a-half accounting for about 12% of total Gulf of Mexico oil production.

Four of the new projects will likely begin production in 2021 and nine more in 2022, according to Rystad Energy.

The oil production increase for the GOM in 2023 was due to new start-ups during 2022 and 2023. At this point in time, the deep water GOM is quite mature, meaning the region has been extensively explored and developed. I expect that deep water GOM oil production will start consistently declining in the next few years and in a larger way than the BOEM sees it as illustrated in Table I.

Update: For 2023, GOM oil production reached its highest rate in September at 1.997 mb/d. Production was down 166,000 b/d in April 2024 relative to September 2023.

Alaskan Oil Production

Figure XIV is a graph of Alaska’s historical oil production from 1970 through 2023:

Figure XIV

In 2023, the Alaskan oil production rate averaged 0.426 mb/d. Alaskan oil production reached its highest rate in 1988 at 2.017 mb/d so production has dropped 78.9% since 1988. No amount of dreaming, rhetorical exaggeration about how much oil exists in Alaska, or drilling will take the production rate back to those heady days.

There has been considerable news coverage in the last few years about the Willow Project which is located in the National Petroleum Reserve-Alaska (NPR-A) of northern Alaska. In my report of 2022 I wrote:

A few discoveries in the NPR-A have been made in recent years such as Willow, Willow West and Peregrine which explains the U.S. DOE/EIA projection in Table III for future Alaskan oil production [Table III contained projections of future U.S. oil production including Alaska which can also be found in Table V of this report]. The Willow field is projected to start production in 2024/2025. Production from new fields will be superimposed on declining production from old fields which will limit any production rate increases for the state of Alaska.

The Willow Project is projected to have a maximum oil production rate of 180,000 b/d during a projected lifetime of 30 years. I have heard commentators state that production from the Willow Project will lower oil prices in the future. The problem with that idea is that production declines in U.S. tight oil plays, the Gulf of Mexico and other U.S. oil producing areas will be substantially larger than the increase in production from the Willow Project.

With luck, the NPR-A may ultimately produce 1 billion barrels of oil. Over the years, there has been keen interest by people in the oil industry and others to open the Arctic National Wildlife Refuge-Alaska (ANWR-A) to oil development. ANWR-A is on the east side of the presently developed oil region of northern Alaska while the NPR-A is on the west side.

With the high rate of oil production from tight oil plays and with a Democratic president, there hasn’t been much talk about opening ANWR-A to oil development in recent years but when oil supplies get tight in the U.S., I expect that will change. I expect that in a best case scenario, ANWR-A could ultimately produce 3-4 billion barrels of oil. To put that in perspective, the U.S. presently uses approximately 5.5 billion barrels of crude oil + condensate a year. The NPR-A and ANWR-A are not going to be the salvation of the U.S. oil consumer in the future.

U.S. Oil Production

Figure XV is a graph of historical U.S. oil production from 1930 through 2023:

Figure XV

In 2023, the U.S. oil production rate averaged 12.927 mb/d which was 1.044 mb/d more than in 2022 and 616,000 b/d more than the previous annual production rate record of 12.311 mb/d in 2019.

The increase in U.S. oil production for 2023 was almost exclusively (97.2%) from four locations: Texas (+512,000 b/d), New Mexico (+253,000 b/d), North Dakota (+128,000 b/d) and the Gulf of Mexico (+122,000 b/d).

U.S. oil production in 2023 increased rapidly from 12.568 mb/d in January to 13.295 mb/d in November. Since November 2023, U.S. oil production has not increased beyond the November value, at least not through April, the most recent monthly EIA data. Considering the fine weather during April, not too hot and not too cold, there was no reason why producers didn’t go all out producing oil in April.

The one region which has continued to experience production increases is New Mexico where production was up 87,000 b/d in April 2024 relative to November 2023. We’ll have to wait and see how long production can continue to rise in New Mexico but it is likely that it will start declining within the next few years.

On the other side of the ledger, Table IV has data for major oil producing regions in the U.S. where production was down in April 2024 relative to the peak production month of 2023:

| Region | Maximum Oil Producing Month in 2023 | Production Rate in April 2024 Relative to the Peak Month of 2023 (b/d) |

| Gulf of Mexico | September | -166,000 |

| Texas | November | -22,000 |

| Bakken Portion of North Dakota | September | -39,494* |

| Oklahoma | May | -35,000 |

| Colorado/Wyoming | December | -32,000 |

Table IV *Data from the state of North Dakota

Table V is a summary of the EIA’s oil production projections from their Annual Energy Outlook 2023:

U.S. DOE/EIA Annual Energy Outlook 2023 Oil Production Projections

| Year | Tight Oil (mb/d) | Lower 48 States (mb/d) | Alaska Onshore (mb/d) | United States (mb/d) |

| 2022 | 8.01 | 9.59 | 0.44 | 11.83 |

| 2025 | 9.09 | 10.40 | 0.45 | 12.86 |

| 2030 | 9.08 | 10.46 | 0.60 | 13.31 |

| 2035 | 9.15 | 10.67 | 0.56 | 13.23 |

| 2040 | 9.18 | 10.80 | 0.65 | 12.96 |

| 2045 | 9.37 | 10.99 | 0.70 | 13.10 |

| 2050 | 9.62 | 11.17 | 0.73 | 13.24 |

Table V

The EIA appears to believe that the future U.S. oil supply situation is unbelieveably bullish, much more so than numerous petroleum geologists and independent oil analysts.

Just looking at the tight oil production projections, the EIA is projecting production in 2050 at 9.62 mb/d, even higher than projected values from 2025 through 2045. Based upon the EIA numbers, cumulative tight oil production would be over 100 billion barrels (Gb) from 2008 through 2050 and production would still be increasing.

Considering the problems being encountered now in the five shale plays that produce essentially all of the tight oil in the U.S., do the analysts at the EIA actually believe the tight oil production numbers in Table V or for that matter, the other numbers in the table?

Petroleum geologist David Hughes, who has specialized in petroleum resource assessements for decades, has been critical of what he considers highly inflated projections of future tight oil production by the EIA and has detailed his criticisms in numerous reports such as:

https://www.desmog.com/2021/12/08/david-hughes-shale-optimistic-fracking-forecasts-eia/

Hughes describes 3 problems with the EIA projections of future U.S. tight oil production:

- They overstate drillable acreage and assume lower quality acreage will be as productive as high quality acreage

- They believe that wells can be drilled closer together than is practical

- They believe that new technology can overcome exhaustion of wells

To the extent that the mainstream media covers the issue of future U.S. oil supply at all, it would present the optimistic projections of the EIA rather than what I consider the realistic assessments of experts like David Hughes and Art Berman. Of course optimism that isn’t supported by reality has consequences.

The EIA doesn’t have a particularly good record when it comes to assessing oil resources. In 2011 they commissioned INTEK, Inc. to make an assessment of the recoverable oil resources of the Monterey shale region in California and promoted that assessment. The assessment concluded that there were 15.4 billion barrels of recoverable reserves in the region. The assessment was highly criticized by David Hughes in this report:

https://www.resilience.org/resources/drilling-california-a-reality-check-on-the-monterey-shale/

In 2013, the EIA reduced the assessed recoverable volume of oil to 13.7 billion barrels. In 2015 the United States Geological Survey (USGS) reduced the recoverable volume estimate of oil to 21 million barrels, a reduction of 99.9% from the originally assessed volume.

The future of U.S. oil production will largely be tied to Permian Basin oil production in-as-much as the Permian Basin produces approximately 45% of all U.S. oil at present. Production from the Permian Basin will at some point in the not-too-distant future start to decline and that will create a sticky wicket for future U.S. oil production.

I expect the ultimate oil recovery from U.S. tight oil plays will be roughly 50 billion barrels. That is a lot of oil but it’s a long way from an infinite supply and considerably less than what has been produced so far from conventional U.S. sources.

I would not be surprised if U.S. oil production drops 5 mb/d or more by 2033 relative to 2023, 40% or more. That would only require an average decline rate of approximately 5.5%/year for U.S. oil production.

Conclusion

Since the start of tight oil production in the U.S., the objective of the oil industry has apparently been to get the oil out of the ground as quickly as possible. The down side of maximizing the production rate is that it leads to the peak production year arriving sooner and to a higher decline rate after the peak.

The U.S. has built an infrastructure tailored to maximize the use of oil. The U.S. consumer has grown accustomed to expecting cheap and easily available oil distillates. It will be interesting to see how U.S. consumers respond when that supply is not so cheap and available in the future.

When U.S. oil production declined after the 1970 peak as well as after the secondary peak due to Alaskan oil production (1985), U.S. oil imports rose. Importing more oil from global sources will not be so easy in the future for several reasons.

First, most of the global oil production increase during the period 2008-2018 came from the U.S., mainly due to U.S. tight oil production. In the last few decades, the rest of the world has been struggling to prevent production declines let alone increase production. Global oil production actually reached a maximum in 2018. There won’t be a lot of easily available oil on the global market for the U.S. to buy in the future like there was in the past due to resource constraints.

Second, there will be more global competition for the oil that is on the market from developing countries such as China and India.

Global oil supplies were cut off in the 1970s due to several OPEC oil supply interruptions. In response to those interruptions, the oil industry intensively developed northern Alaska, the U.S. portion of the Gulf of Mexico, the Mexican portion of the Gulf of Mexico, the North Sea and other offshore areas including deep water areas (>1000 feet). Those areas have now largely been tapped out.

The high price of oil in 2008 (WTI rose to $140/barrel in the summer of 2008) led to the rapid development of tight oil in the U.S. That is now being tapped out rapidly. It’s not clear where the industry can go from here based upon geology other than a few fruitful shale plays outside of the U.S.

It’s common to hear that electric vehicles will soon be taking over the transportation sector of the U.S. and displace the use of oil distillates. If the last 10 years are any indication of the future, it appears that oil distillate demand will remain strong in the U.S. for the foreseeable future.

To the extent that Americans think about U.S. and global oil supplies, my impression is that they believe those supplies are infinite, or nearly infinite, and that oil will always be available to them. Based upon the likely future of U.S. oil production presented in this report, as well as the likely future of global oil production, that may not be the case. Numerous prominent petroleum geologists have been warning for years about the resources limitations of oil both in the U.S. and globally. It’s now looking like the wolf is nearing the door.

1 https://novilabs.com/blog/permian-update-through-july-2023/

2 https://www.artberman.com/blog/bakken-break-even-prices-threaten-profits/

3 https://www.eia.gov/petroleum/drilling/pdf/niobrara.pdf

4 https://www.eia.gov/petroleum/drilling/pdf/anadarko.pdf