There are tides and seasons in the comments I field for posts here on my blog, certain questions that get asked at regular intervals, certain saliva-flecked tirades I can count on getting whenever certain things appear in my writings or happen in the world. One of the more frequent of the questions is how to preserve wealth in the face of a difficult future. This question pops up reliably when an economic crisis is on its way, as it happens, and I’ve started fielding it again in recent weeks; my readers may want to brace themselves.

Like so many of the common questions here, it’s an important question, and it has no simple answer. The combination of those features isn’t accidental. It’s an important question because it can’t be answered in any meaningful way without grappling with what wealth actually is, and it’s because wealth is not what most people think it is that the question has no simple answer.

We can start our exploration with a lump of stone and metal whizzing through the lethal radiation-soaked vacuum of interplanetary space between the orbits of Mars and Jupiter. Its name is Psyche, and it’s about the size of Greece. It’s been splashed over the news in recent years because it’s got more metal in it than most other asteroids, and scientists have speculated that the metallic portions of Psyche might include a great deal of gold. Of course the mass media jumped on that instantly and started insisting that if only it could be dragged into our part of the solar system it would make everyone on Earth a billionaire.

If we needed any more evidence that the mass media is full of people who literally don’t know enough about economics to be let out of doors alone without a note from their mommies, here it is. Let’s do the thought experiment, shall we? Suppose a solid gold asteroid were to be lassoed by astronauts, parked in low Earth orbit, chopped up into pieces small enough to go through reentry without annihilating a city or two when they hit, and brought down to earth. Would that actually make everyone on Earth a billionaire?

No, of course not. It would simply drop the price of gold to ten cents an ounce or so, put a lot of miners permanently out of work, and result in an extensive stock of solid gold cookware on the shelves of every cheap department store in the industrial world. (I have it on the authority of an old National Geographic article that cast gold cookware is excellent stuff, since food doesn’t stick to it and gold does an extremely good job of spreading heat evenly.) To be precise, it would have the same effect as trying to help a stranded castaway on a desert island by parachuting down a suitcase full of gold bars instead of food, water, and so on.

The lesson here, and it’s a crucial one, is that gold is not wealth. Gold is one of the many tokens our species uses to manage the distribution of wealth. It has certain advantages over other tokens—in particular, it’s very widely accepted and governments can’t print more of it any time they feel like, so it tends to maintain more of its value in hard times—but it’s simply a token that can be exchanged for wealth, provided that there’s wealth to be gotten in exchange.

Of course the same thing is even more true of the most popular kind of tokens in our society: money. If you have a stash of hundred dollar bills tucked under your mattress, or a set of arbitrary magnetic charges in a computer memory somewhere claiming that you have an equivalent amount in your bank account, do you have wealth? No, you have a collection of tokens that you can exchange for wealth under current conditions.

Those conditions can change. If the US government collapses next Tuesday, and the full faith and credit thereof no longer amount to a hill of beans, your collection of bills would be worth next to nothing and your collection of arbitrary magnetic charges would be worth even less than that. If shopkeepers decide that they don’t want to put too much trust on the full faith and credit of the US government any more, and ask customers to pay in a more stable currency, your tokens won’t be worth much more. Those of my readers who live south of the Mason-Dixon line, or in most countries outside the US, already know that this can happen. Those who live in other parts of the US might want to look up the origins of the phrase “not worth a Continental” someday.

So gold is not wealth, and money is not wealth. What is wealth? Etymologists will tell you that the word “wealth” comes from the old-fashioned word “weal” the way “health” comes from “heal,” and that “weal” shares an origin back in the mists of Indo-European prehistory with “well” (in the sense of “well-being”) and “will.” In Anglo-Saxon times wel meant “according to one’s wish” and wela meant both “well-being” and “riches.” To be wealthy is to have the things you need and want, the things that support your well-being and enable you to do what you like.

Back in the nineteenth century, John Ruskin pointed out that this concept needs to be balanced by another: illth. As wealth is to weal (and well and will), illth is to ill. To have illth is to be burdened by things you don’t need and don’t want, things that harm your well-being and prevent you from doing what you like. Every economy produces both wealth and illth: that is to say, every economy produces goods and services, but also harms and hindrances. The relative proportion of wealth and illth varies across time, for reasons we’ll discuss later. The distribution of wealth and illth is the great problem of economics. One essential reason modern economists make bad predictions and bad policy so reliably is that they ignore half of this problem, and pretend that the production and distribution of illth isn’t relevant to their discipline.

It’s important to remember the distinction between money and wealth, because—as already noted—the equation between the two depends on conditions that can change, and have changed very suddenly at various points in the past. The most obvious way that conditions can change is when nations cease to exist. When the Confederacy and the Russian Empire collapsed, for example, their money could no longer be used to get wealth or avoid illth. When France after the Second World War issued a new currency and required holders of the old currency to account for the origin of their wealth as a condition of trading old for new, people who’d gotten money by dubious means were seen burning old banknotes by the wheelbarrowful. In these and other cases of the same kind, a change in political conditions broke the link between money and wealth.In economic terms, we can define wealth and illth succinctly. Wealth is a share of the current production of goods and services, and illth is a share of the current production of harms and hindrances. While our culture’s customary tokens still function, the more money you have, whether that consists of gold coins or magnetic charges in a bank’s computer, the more wealth you can claim and the more illth you can avoid. Money, again, is one set of tokens our species currently uses to handle the distribution of wealth (and, without anyone ever quite admitting it, the avoidance of illth), and so it’s understandable that people confuse money with wealth.

Yet there’s a subtler way the link can be broken, and that’s by way of a mismatch between the amounts of money and wealth in circulation. When there’s more money than there is wealth to buy or illth to avoid, the law of supply and demand drives prices and wages up, and you have inflation. When there’s more wealth and illth available than there is money to get one and avoid the other, the same law drives prices and wages down, and you have deflation. Both damage the economy and hurt people, though the pain isn’t shared equally: inflation hurts borrowers and people with fixed incomes, deflation hurts investors and people with fixed expenses.

Both of them are often caused by government policies. When governments and put too much money in the economy, you get inflation—that’s why prices are rising now, since so many countries are printing money to try to cope with the impact of their coronavirus policies. When governments restrict the money supply using precious metal backing or some similar gimmick, you get deflation—that’s why the second half of the nineteenth century and the first third of the twentieth saw one disastrous economic depression after another, because most of the world’s nations were on the gold standard and the economy grew faster than the money supply.

What a great many people forget these days, however, is that government policy isn’t the only thing that can cause these problems. If for some reason the amount of wealth available to purchase takes a nosedive, for example, you can get inflation even if the government hasn’t spun the presses. That was what happened in most of the industrial world in the 1970s. US oil production peaked and began to decline, shortages rippled through the economy, and suddenly there was too much money chasing too little wealth. The resulting mess got a name of its own—stagflation—because economic growth stagnated while prices spiked. The same thing can happen if the amount of illth in circulation increases for reasons unrelated to the money supply.

The lesson to take from both these latter points is that the wealth and illth of a society can vary for reasons that have nothing to do with economics. If that happens, all the tokens in the world won’t bring you wealth or enable you to avoid taking a larger share of illth than you want.

With this in mind, let’s go a little deeper into the system of tokens we call “money.” At the heart of money as it currently exists is the notion that money should make money. If you put it in a bank account, you should get interest; if you invest it in stocks, you should get dividends and capital gains; if you buy bonds, you should get a return on your investment, and so on. That was not true of money until recently, historically speaking, but it’s been true for several centuries, and almost everyone these days treats it as though it’s as inevitable as tomorrow’s sunrise.

In point of fact, it’s anything but inevitable. It’s a specific gimmick that evolved over the last few centuries. It was invented to deal with the unprecedented era of global economic expansion that began with the systematic exploitation of coal as an energy resource in the eighteenth century, and went into overdrive once petroleum was added to the fossil fuel mix beginning in the 1850s. Before that era, economic growth was normally something that happened only when one society conquered another and got a sudden burst of new resources to exploit. Outside of that special case, the increased weath yielded by technological improvements was neatly balanced by the increased demand for wealth driven by expanding populations and resource depletion.

Fossil fuels broke that pattern by enabling, at least at first, the production of much more wealth than illth. Dealing with that bonanza required expansion of the money supply—a modest expansion during the era of coal, and a much greater expansion during the era of petroleum, which is why the gold standard got shoved aside once the latter era arrived. It became an item of faith during the petroleum era that economic growth was natural and inevitable. That faith remains fixed in place today, even though the conditions that made sustained economic growth possible are fading out of sight in the rearview mirror right now.

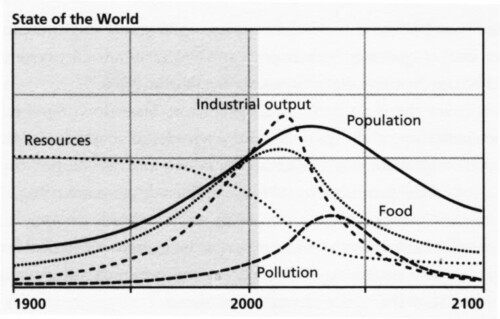

That’s one of the essential messages of the Limits to Growth model I discussed two weeks ago. The lesson taught by the World3 model can be summed up very crisply in terms of the language we’ve been using: over time, economic growth affects the relative production of wealth and illth by any economy. In the early days of economic expansion, it’s easy for an economy to produce more wealth than illth, but the further the expansion runs, the more the balance tips the other way, until eventually the economy produces more illth than wealth. Prolong economic growth too far, and the production of illth overwhelms the production of wealth and forces growth itself to its knees: that’s the lesson our political classes have been trying to ignore for fifty years.

The standard run from The Limits to Growth shows how that ends. Industrial output and food—the main forms of wealth—begin to decline, food gradually, industrial output much more rapidly. Meanwhile pollution—an important form of illth—climbs further before it, too, tips over and starts to decline. Population peaks and declines as well, and resources finish their descent to sustainable levels. What this means in economic terms, of course, is that the sustained economic growth of the last few centuries gives way to a few centuries of sustained economic contraction.

With all this, let’s cycle back to the question we discussed at the beginning of this post: how to preserve wealth and avoid illth in the face of a difficult future. Most people who ask this want me to tell them what set of tokens they can hoard so that they will be able to exchange those tokens for wealth, at something like the same rate of exchange those tokens bring today. Most of them, though they’ve never heard of John Ruskin and don’t know the word “illth,” also want to use their tokens to avoid illth at something like the same rate they can today. Neither of these are possible, because wealth and illth are both functions of economic production. When the amount of wealth being produced is steadily dropping, and the amount of illth being produced is steadily increasing, any set of tokens—no matter what they happen to be—will command a smaller amount of wealth and avoid a smaller amount of illth.

That said, some tokens will lose value faster than others. Economists, like generals, reliably try to fight the next war using the weapons and tactics of the last one, and that has been a massive source of trouble over the last few decades. The last major era of economic crisis reached a peak in the 1930s, when the mismatch between an expanding economy and a gold-backed currency that couldn’t expand fast enough resulting in an epic depression. That was finally solved by abandoning the gold standard and flooding the economy with debt-based money.

When the global economy began to run into trouble in the 1970s, economists were still fixated on the experiences of the 1930s and tried to do the same thing all over again. That was a critical mistake, since the crisis of the 1970s was not caused by too much growth—it was caused by too little. Economists and policymakers have doubled down on the same mistake ever since, flooding the economy with money under the serene delusion that you can fix a shortage of wealth by increasing the number of tokens used to distribute it. That risked inflation, and the history of the last fifty years has been dominated by the struggle to find gimmicks to keep inflation under control while expanding the currency supply. (The culture of elite kleptocracy that has generated so many absurdly overinflated fortunes in recent years is one of these gimmicks.)

At this point, as a result, the single most pressing need the global economy faces is the need to clear away a spectacular oversupply of tokens. When the United States defaults on its unpayable debt or hyperinflates it out of existence—sooner or later it inevitably must do one or the other—that will take care of a lot of it, but by no means all. As the production of wealth declines and the production of illth increases, the mismatch between the supply of tokens and the supply of wealth will increase. To the extent that entire classes of tokens (such as US dollars) lose all their value, that will allow other classes to retain more of theirs, but every kind of token—yes, including gold—will have to shed a good share of its capacity to claim wealth and avoid illth.

All this can be summed up quite simply. During the long era of expansion made possible by the exploitation of fossil fuels, the world’s industrial nations had positive-sum economies: that is to say, the total amount of wealth in those nations increased on average from year to year, and it increased faster than the total amount of illth. Since the arrival of the first energy crisis in 1973, the world’s industrial nations have effectively had zero-sum economies: that is, the total amount of wealth—not of money, but of nonfinancial goods and services—remained largely static on average, while the total amount of illth rose to equal it. We are now moving into an age of negative-sum economies, in which the total amount of wealth decreases on average from year to year, while the total amount of illth rises steadily for a while.

In a negative-sum environment, trying to preserve wealth by stockpiling tokens is a fool’s errand, and no, it doesn’t matter what tokens you stockpile. Are there strategies that can deal effectively with such times? Yes, though they’re highly counterintuitive to minds raised to believe in limitless growth. We’ll discuss them in the first October post on this blog.

*******

In not wholly unrelated news, I’m delighted to announce that my widely acclaimed book on ecological economics, The Wealth of Nature: Economics As If Survival Mattered, is being reissued in a new and updated edition. It can be preordered at this time from the new publisher. If that’s of interest, you can get the details here.

In not wholly unrelated news, I’m delighted to announce that my widely acclaimed book on ecological economics, The Wealth of Nature: Economics As If Survival Mattered, is being reissued in a new and updated edition. It can be preordered at this time from the new publisher. If that’s of interest, you can get the details here.

Teaser photo credit: A fifty-five dollar Continental issued in 1779. By Beyond My Ken – Own work, CC BY-SA 3.0, https://commons.wikimedia.org/w/index.php?curid=9947666