It’s hard to ignore the protests on the streets of the world’s cities of late. Those protests are coming from a populace who knows that the system they live under long ago stopped benefiting them. While the focus has been the senseless killing by police of an African-American man—all of which was caught on video—there are many other grievances: legalized financial theft by the one percent from the rest of us comes to mind, something that has resulted in growing and egregious inequality across the world.

It’s also hard to overestimate the hardship visited on the world’s people as many have been deprived of income and daily life by up to three months of pandemic-inspired stay-at-home orders and retail shutdowns. As I mentioned in my previous piece, the U.S. Federal Reserve Bank of Atlanta does a frequently updated estimate of U.S. GDP which as of this writing is minus 53.8 percent for the second quarter. (That’s annualized and seasonally adjusted.) The estimate for the current quarter started at minus 12.1 percent and has been dropping like a stone with each new piece of information. For comparison, U.S. GDP during the 2008-2009 financial crises shrank by only 4.2 percent.

And yet, the world’s stock markets are behaving as if the protests and the deprivation are inconsequential. After crashing in March in the wake of the spread of the coronavirus pandemic, major stock market indices are at or near all-time highs. For example, the S&P 500 Index was last around its Friday closing price on February 24, before the coronavirus pandemic market panic. How can this be explained?

I can remember as a boy that financial news was rarely on the front page of the newspaper. The financial section of any bookstore was tiny in comparison to history and literature. Now it takes up entire rows in the larger stores.

Five years before I entered college, the department with the highest enrollment at my school was English. The year that I arrived it was economics. A sea-change had occurred.

Between then and now, the world’s elites have worked overtime to financialize every aspect of the global economy by distorting government policy and business practice. All commercial endeavors are now preferentially organized not to serve the needs of customers in pursuit of a reasonable return, but to serve the needs of shareholders. Startup companies are formed not with an eye toward building something of lasting value for the founders, the employees, the vendors, the customers, and the community, but with an eye toward the exits when the founders sell out to a bigger company—a company whose primary focus is to rework the startup to maximize its payout to shareholders and managers.

This is sometimes accomplished by laying off a large number of employees, dumping the extra work on the remaining ones, loading the company up with large amounts of debt and then declaring a huge dividend for the new owners. The result is often a spectacular bankruptcy many years later that destroys the company when the owners are away on vacation at their beach houses in the Virgin Islands.

This arrangement has worked out very well for those at the top of the economic scale. And, it is lauded as the way to success and wealth. It’s just the way things are done, and we are supposed to accept it. But many people now on the streets are no longer accepting it, and they have probably not accepted it for a long time.

And yet, at least in America, the desire to live like those at the top—and the belief that it just might be possible despite one’s own humble current circumstances—is a perennial feature of the American mind. And, so we tend to see at the end of bull markets in financial assets, people who’ve never invested before or who’ve only done so indirectly through, say, a pension fund or a mutual fund, decide that they, too, should have the right to make easy money like the upper classes.

Hundreds of thousands of individual brokerage accounts have been opened since the beginning of the year, presumably by those trying to get in on that easy money. The economic shutdown only seemed to embolden them as stories of a quick economic recovery led them to dump their plumped up unemployment checks into the stock market. All this has been aided and abetted by the brokerages through zero commission trading.

Perhaps the best illustration of the insanity is trading in the shares of a now fallen icon of American commerce, rental car giant Hertz. Hertz filed for bankruptcy in May. Every expectation is that shareholders will be wiped out completely, and all the equity will be given to creditors as part of a financial restructuring of the company. And yet new small investors took the price of a now bankrupt Hertz from 40 cents to $3.78. As of Friday, the shares, which are almost certainly worthless, closed at $2.57 up 71 percent for the day.

For the moment those small investors are laughing at billionaire Carl Icahn who sold his 39 percent stake in the company for 70 cents per share losing about $1.8 billion on a long-term investment made back in 2014.

But I think Icahn will have the last laugh. The current buying panic in the U.S. and world stock markets looks very much like that which occurred in the technology bubble of the late 1990s. In 1999, the U.S. Federal Reserve, fearing that the so-called Y2K problem with computers might result in economic chaos, pumped huge amounts of liquidity into the financial system. When the new year rolled around and few problems arose, it was too late. The gargantuan central bank response had money already flowing uncontrollably into stock markets and into technology stocks in particular. The technology-laden NASDAQ index which had been up 85 percent in 1999, rose another 20 percent in early 2000 before crashing.

Likewise, today we have a huge central bank intervention—far more than in 1999—in response to an actual shock rather than an anticipated one. The previously truncated market blowoff that was already taking place earlier this year seems now to be resuming. Will these investors stampede many others including the professionals in the stock market and take the market averages 20 percent above their previous highs as we saw with the tech bubble?

I wouldn’t bet against it—even in the face of economic numbers worse than the Great Depression. That is how strong a force investor psychology can be, especially when it becomes completely unhinged from reality.

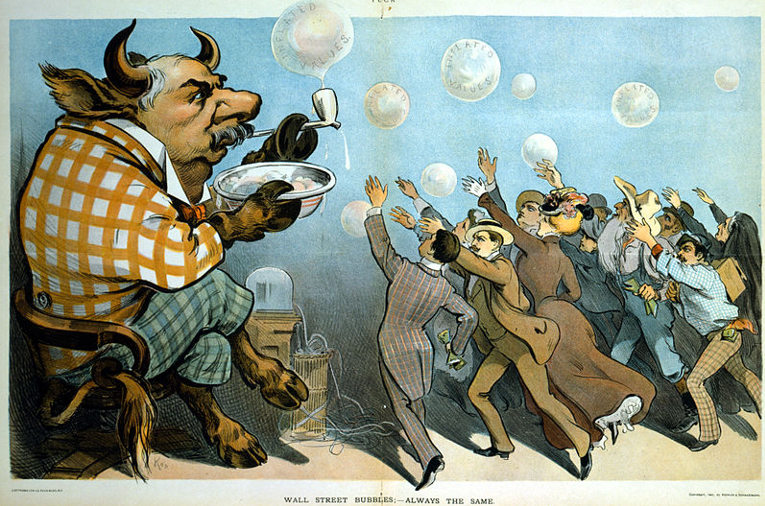

Cartoon: “Wall Street bubbles – Always the same”. American financier J. P. Morgan is depicted as a bull, blowing soap bubbles for eager investors. Puck (1901) Via Wikimedia Commons

{kind=link}