Soon after we posted the piece on April 18 regarding the report from the Saudi Oil Minister, Ali al-Naimi, we discovered an article we’d clipped from the Oil & Gas Journal, sourced from the Oil & Gas Journal Online, dated March 28 (two days before the President’s energy speech). So, this March 28 article actually contained the news of the “output cut”, which Mr. Naimi re-delivered on April 18. The article quotes Barclays Capital managing director Paul Horsnell, and he paints a far different picture of the worldwide supply, demand and capacity issues than did Mr. Naimi:

“Saudi Arabia’s production is estimated at 8.2 million b/d. [which is what Mr. Naimi said they had indeed produced in March, some four weeks later] However, Horsnell said, recent data are pointing to Saudi output close to 9 million b/d in December and “and at that level in January and February.” [Mr. Naimi confirmed the 9 million b/d, as to February]

“He said, “This has two main implications. First, it is the source of another downward revision of start-of-year spare capacity levels, since Saudi Arabia’s output has been higher than was originally reported. The second implication is in what it suggests to us about how much Saudi Arabia needs to produce to balance the market.”

In other words, Mr. Horsnell is saying that since the world previously thought that the Saudi’s were producing less in December than they actually were, then the estimated worldwide “buffer” production capacity was significantly less than believed, as well. Also, his observation that the Saudi’s evidently needed to produce at 9 million b/d in order to balance the market is the exact opposite of what Mr. Naimi said, four weeks later.

Mr. Horsnell went on to say:

“Even producing 9 million b/d, Saudi Arabia still has left “a significant deficit at the margin of the market with inventories falling faster than normal, even before Libyan exports came off the market. Allowing for a normal second quarter global inventory build and replacing lost volumes from elsewhere seems likely to require Saudi Arabia to move up to 10 million b/d, in connection with higher volumes from the other holders of spare capacity …”

This doesn’t sound much like a market which is oversupplied …

Earlier in the same article, with respect to demand, Mr. Horsnell said:

“Oil demand growth in 2010 earlier was estimated at 2.57 million b/d, with 2011 growth previously forecast at 1.56 million b/d. Now 2010 demand growth is put at 2.83 million b/d-making it “the strongest year for global oil demand growth over the past 30 years.”

This doesn’t seem to jive with the drop in demand/oversupplied market to which Mr. Naimi referred …

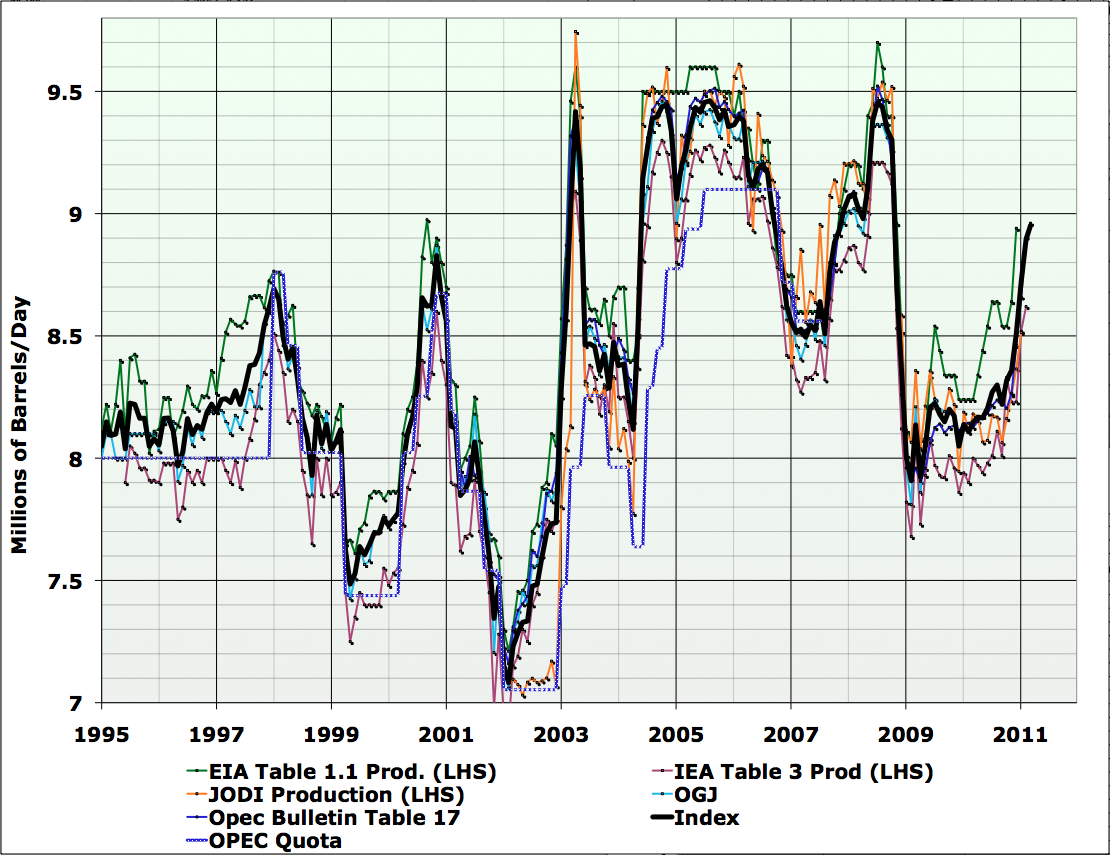

Tom Whipple, a former government analyst and current Peak Oil news aggregator came out soon after the Naimi announcement, outlining the oversupply scenario. However, on April 25, Mr. Whipple supplied some alternate explanations for the Saudi cutback. One of his explanation’s revolved around the fact that Saudi oil production has finally reached the practical limits to its growth, and that the Saudi’s could not sustain the 9+ million b/d rate comfortably. Stuart Staniford, a PhD physicist and analyst of Saudi production, provided some interesting graphs on April 13. Looking at one of those graphs in particular, what stands out is the substantial rate variation in the 2003-2011 period. Of course, Saudi is the ultimate swing producer. But with the exception of a period in 2005, it appears that rates never stay above 9 million b/d for very long; that is, even in face of high prices and a tight market the rates come down substantially, after a brief peak. One might worry that the “maximum reservoir contact” (MRC) wells in Ghawar and elsewhere are tending to cone water after a short run at high rates, and that some wells might be threatening to water out if these high rates are sustained. If this is the case, this would mean that the often touted “worldwide spare capacity” of 3 million b/d or so … is just not there (as it derives primarily from the Saudi’s). In turn, if the Saudi’s can’t really sustain even 9 million b/d, then this would have serious implications for the world in that the next, more intense manifestations of Peak Oil may be nearer than we think.

(Mr. Whipple also offered an alternate explanation in terms of “the Saudi’s making a political statement” in their cutting of production. This theory would suggest that the Saudi’s were upset with the flip-flops in US support for some of the other Arab regimes, and cut production as a result. This might be, but in light of the prior, substantial fluctuations shown by Staniford, it seems that some production capacity-related explanation is a better fit.)

{kind=link}