From Gail the Actuary at the Oil Drum:

This is a paper that was published back in 2000 in the Journal of Geoscience Education. What is unusual about it is that it forecast a peak in oil production in 2008. The author was a young woman named Marie Plummer Minniear, who was studying for her master’s degree at the University of Toledo. Her advisor was geologist Craig Bond Hatfield. This piece was written before many current writers (such as Matt Simmons and Richard Heinberg) started writing about the issue. Many thanks to Chris Kuykendall for bringing this paper to our attention.

Abstract

In recent years, several published reports have assured the public that all is well with the global petroleum supply, citing new oil-production technologies and a record-high oil-reserve figure. Oil production has exceeded demand since late 1997, driving oil prices downward. Global oil consumption, however, is continuing to increase while new oil discoveries decrease. Petroleum is a finite resource, and the production rate will peak and then permanently decline when approximately half of the producible resource has been consumed. The United States has already experienced this; petroleum production in the United States has been in decline since 1970 despite new production technologies and energetic exploration. At recent rates of increase in oil production, the peak in global petroleum production will arrive in about 2008. All is not well with the global petroleum supply, and our society must begin to prepare for the changes that a declining petroleum supply will bring.

Forecasting the Permanent Decline in Global Petroleum Production

In recent years, geologists who warn of the impending oil crisis have come under increasing criticism, often from economists. An example appeared in Business Week magazine in 1997. The authors reported that geologists have a long history of underestimating oil reserves, citing an example from 1874 when the Pennsylvania state geologist “direly warned that ‘the U.S. [has] enough petroleum to keep its kerosene lamps burning for only four years'” (Coy, McWilliams, and Rossant, 1997). Coy, McWilliams, and Rossant also note that oil reserves are at an all-time high and emphasize ever improving technologies, unconventional petroleum resources, and the law of supply and demand. They concede that “nature only gave us so much oil,” yet perpetuate the mistaken idea that our economy is in no danger from reduced oil production and rising oil prices. In fact, Massachusetts Institute of Technology energy researcher Michael C. Lynch is quoted as saying, “Oil-price forecasters make sheep seem like independent thinkers…[t]here’s no evidence that mineral prices rise over time. Technology always overwhelms depletion” (Coy, McWilliams, and Rossant, 1997). Similar arguments are provided by Adelman and Lynch (1997) and Linden (1998). Such arguments commonly point out failed predictions of oil crises that go back a century or so. Everyone, however, agrees that oil is a finite resource. This means that the permanent decline in global production of conventional petroleum unquestionably is approaching. The important question is: When will it arrive?

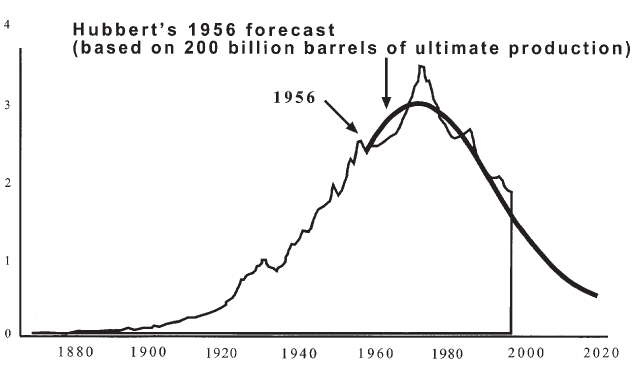

Petroleum geology has benefited greatly from advances in technology and increased knowledge. So much more is now known than 100 years ago that it logically follows that recent assessments are more reliable than the older ones. Some early forecasts, however, have proved to be remarkably accurate. In 1956, for example, M. King Hubbert published an estimate of the peak and subsequent permanent decline in crude-oil production for the contiguous 48 United States. Central to this prediction was the concept that for any petroleum-producing region characterized by unrestricted production, the permanent decline in production would begin when approximately half of the total producible resource had been consumed.

According to Hubbert (1956), the peak in U.S. crudeoil production would occur between 1966 and 1971, based on estimates of ultimately recoverable oil (all oil that will have been produced by the time of exhaustion of the producible resource) of 150 billion to 200 billion barrels. The peak arrived in 1970, and crude-oil production in the United States has been in decline ever since. Figure 1 illustrates the accuracy of Dr. Hubbert’s 1956 forecast. Figure 2 shows the history of global petroleum production, which, of course, is still increasing, as was U.S. oil production prior to 1970. Previous estimates, like the 1874 prediction referred to by Coy, McWilliams, and Rossant (1997), were the product of limited information. But even then, geologists recognized the finite nature of fossil fuels. Their numbers were in error, but the concept was not.

It is also true that improvements in technology and resulting lower production costs have made previously inaccessible or unprofitable deposits now viable. However, the newly profitable fields are too small to make a significant contribution to the global reserves or supply. For example, Business Week proclaims, “The British-Borneo platform can profitably drain fields with as little as 30 million barrels, ‘and we’ll probably push it lower’…” (Coy, McWilliams, and Rossant, 1997). While this is good news for the oil companies, 30 million barrels represents one-half of one day of global production at the 1997 level and even less today (American Petroleum Institute, 1998). If it is possible for new production technology to allow the production rate to continue to grow beyond the mid-point of ultimate production, then the subsequent decline in production rate will be accelerated.

The supply-and-demand cycle is familiar to all but does not apply indefinitely to petroleum or any other finite resource. It assures us that any shortage will create higher prices as demand exceeds supply; the higher prices then cause an increase in the supply, thereby meeting the demand and eliminating the shortage. These relationships are valid for renewable resources and have proven true for conventional petroleum in the past; however, after conventional petroleum production enters permanent decline, supply will continue to dwindle despite the escalating cost. No amount of money can supply a product that no longer exists, no matter how great the demand. This is not to suggest that our global oil supply will abruptly dry up and disappear but to illustrate the fallacy of blindly applying economic law to a finite resource like petroleum.

As stated by Coy, McWilliams and Rossant (1997), officially reported global reserves are higher than ever, but these reserve figures are unreliable. One tactic used to inflate reserves is to include unconventional petroleum sources in the estimate. Venezuela doubled its reserves in 1988 by including 20 billion barrels of heavy oil, which had been known for many years (Campbell, 1997). Unconventional sources, such as heavy oil, tar sands, and oil shale, do represent an enormous amount of potential petroleum, and people often incorrectly assume that these resources will easily make up the differences when conventional sources falter. A common view expressed by Dr. Peter Odell, and many others, is that large-scale exploitation of non-conventional petroleum resources is currently limited only by lack of demand and corresponding absence of profit, and that as soon as it is profitable to produce, non-conventional resources will be ready to seamlessly fill the gap left by a shrinking conventional petroleum supply (Odell, 1997).

On the contrary, at this time petroleum cannot be produced from unconventional sources at rates approaching more than a small fraction of production from conventional sources as required by global demand. Canada, for example, is currently producing petroleum from oil sands, a nonconventional resource. Syncrude Canada Ltd expected to ship 76 million barrels of synthetic crude in 1997 – one year of production equaling approximately 1.17 days of conventional global production at the 1997 rates (Oil and Gas Journal, 1997; Basic Petroleum Data Book, 1998). The comparison is not meant to belittle Canada’s oilsand endeavors; on the contrary, they should be applauded for their farsightedness and imitated. Nevertheless, unconventional petroleum resources are no substitute for conventional sources at this time and will require significant development, considerable time, huge capital investments, and innovative new technology in order to fill that role when needed.

Unfortunately, the development of unconventional resources is not being aggressively pursued at this time. The oil shortages of the 1970s spurred activity in the research and development of alternative energy sources, but many of the efforts were abandoned as soon as the price of oil dropped. In order to someday produce any alternative energy source in an economically feasible manner and in sufficiently large quantities to be a viable substitute for conventional petroleum, an enormous investment of time and money is necessary immediately, as is a commitment to continue that investment regardless of fluctuations in oil prices. What should have been a wake-up call in the 1970s has largely been forgotten (Hatfield, 1997b).

Odell (1997) also says that market prices will “bid up sufficiently to generate new non-conventional oil supplies.” As he points out, there will most likely be an increase in the cost of petroleum and the multitude of petroleum products we all use every day. Companies are not in business to lose money. Unconventional petroleum is more costly to produce than conventional partly because of research and development expenses and also because it cannot be produced in great quantity per year. Oil companies will not begin serious exploitation of unconventional petroleum resources until they can make a profit doing so, and there is little profit in synthetic crude when oil prices are low. According to the economists’ law of supply and demand, oil prices will begin to rise as production falters in the near future. At the higher prices, it will then be profitable (as well as necessary) to exploit unconventional petroleum resources. Any increased costs will be passed on to the consumer, of course. The world will not run out of oil altogether, just out of cheap oil.

Coy, McWilliams, and Rossant (1997) also proclaim that, due to new technologies and abundant capital, we have “the recipe for a potential explosion in oil production.” New oil-production technology, such as that employed in recent years in the North Sea, could delay the beginning of global oil-production decline for a few years beyond the mid-point of ultimate production. But, in that case, the subsequent decline will be accelerated. Considering both conventional and unconventional petroleum sources, production and prices may fluctuate for years with production increasing at times and prices decreasing. But in the end, production of conventional petroleum will permanently and irrevocably decline, and unless demand has been reduced or cheap unconventional sources (or other non-petroleum substitutes) are sufficiently developed, prices will rise as supply becomes inadequate. With existing technology, unconventional energy sources will be considerably more expensive than conventional oil.

As Coy, McWilliams, and Rossant (1997) stated, reserve estimates are at an all-time high. However, determining the amount of conventional petroleum reserves with any reasonable precision is nearly impossible. A total reserve of 1,000 billion barrels is widely used (American Petroleum Institute, 1998) but is widely regarded as suspicious by geologists for several reasons. In 1988, 1989, and 1990, many OPEC nations reported fantastic increases in their reserve figures, as is illustrated in Figure 3. The OPEC nations’ production quotas were based on the sizes of their reserves; the countries reporting the largest reserve figures earned the greater shares of the total OPEC production. Venezuela’s reported reserves increased by 125%, the United Arab Emirate’s by 197%, Iraq’s by 112%, and Iran’s by 90%. Kuwait’s 50% increase is modest by comparison (American Petroleum Institute, 1998). This created an apparent increase in global reserves of 27%, or about 300 billion barrels. These wild increases are considered unsubstantiated and unreliable (Cambell, 1997; Hatfield, 1997a; MacKenzie, 1996).

In addition, many countries, including several of the top oil producers, have reported no changes in their reserve estimates for several years. China and the former Soviet Union are among those that report no differences from year to year. Iraq and Kuwait report no changes in their reserves after the gigantic increases of the late 1980s. Yet, annual production in those countries has been vast and has greatly exceeded new oil discovery (American Petroleum Institute, 1998). Actual reserves are decreasing rather than remaining static. Some countries are believed to be understating their reserves. C.J. Campbell (1997) believes that the former Soviet Union, the United States, China, and the United Kingdom, all major oil producers, have underestimated their oil reserves. Any additional reserves these countries may possess, however, will not have a significant impact on the global production peak because their unreported reserves are only a fraction of the unsubstantiated reserves reported by the OPEC nations. Given the unreliable information used to calculate the global reserve, it should be viewed with healthy skepticism.

One reasonable suggestion is that a figure for global reserves of approximately 730 billion barrels be used. This revised estimate attempts to correct for the gross reserves inflation of the late 1980s by OPEC but does not claim to factor in all suspected overestimating and underreporting. The figure of 730 billion barrels is derived in the following manner. During the ten years prior to the wild increases of 1988 – 1990, global reserves were increasing at an average rate of 0.65% annually (American Petroleum Institute, 1998). Disregarding the unsubstantiated increases starting in 1988, the 0.65% growth rate was then applied annually for each year through 1997. This interpolation yields a suggested global reserve of 730 billion barrels rather than the reported 1,000 billion barrels. It is worth noting that the average annual increase in the reported global petroleum reserves from 1988-1996, excluding the enormous leaps in 1988, 1989, and 1990, was only 0.37% – less than the 0.65% of the previous decade. In reality, any estimate, including this one, given the inherent problems with the available data, is more likely a product of manipulation and educated guesswork than solid data.

An optimistic estimate for yet to-be-discovered oil is 650 billion barrels; this figure is well above most estimates of conventional oil yet-to-be discovered (MacKenzie, 1996). Six hundred and fifty billion barrels may indeed be a generous estimate. The global rate of discovery of new oil peaked in the early 1960s and, despite our increased knowledge and understanding, our improved technology, and our record-high rates of exploration in the 1980s, has continued to decline (MacKenzie, 1996). Ninety percent of all production comes from fields more than 20 years old. (Campbell, 1997). In fact, most additions to the global reserve estimate are the result of revisions rather than actual new oil discoveries. The previously mentioned OPEC nations are a prime example. In reality, actual discovery of new reserves is now less than 6 billion barrels per year and falling, whereas production exceeds 24 billion barrels per year and is rising. (Campbell, 1997). Figure 4 shows the steady decline of new discoveries.

The discovery of new major oil fields is highly unlikely. The requisite geologic factors are well understood, and the sedimentary basins well known and explored. This is not to say that no additional oil fields will be found but that the new discoveries will consist largely of smaller fields (MacKenzie, 1996; Campbell, 1997). This is a normal phase in the life cycle of a finite resource. Large fields are the easiest to find and of course are discovered early; in the declining phase of finite-resource exploration, intensive searching locates the smaller fields previously overlooked (MacKenzie 1996).

But it is the gigantic oil fields that supply the bulk of the world’s energy. As of 1996, 94% of all discovered oil has been in the 1,331 largest oil fields, while the almost 40,000 smaller fields contain only 6% of the world’s discovered oil – 94% of all discovered oil occurs in 3% of the fields (MacKenzie, 1996). The giant fields are critical to the global oil supply, but discovery of larger oil fields is highly unlikely, and discovery of smaller fields, while probable, will not significantly affect the global reserves.

Giant oil fields are those that contain between 500 million and 5 billion barrels of recoverable petroleum, and supergiants contain between 5 billion and 50 billion barrels. In order to add to the proven reserves the 650 billion barrels that are optimistically assumed to exist, 130 new giant fields each containing 5 billion barrels would have to be discovered or 1,300 new giant fields each containing 500 million barrels. The former is impossible and the latter ridiculous. Mankind’s history of petroleum exploration has yielded over 40,000 oil fields, of which 328 are giant fields (Ivanhoe and Leckie, 1983; MacKenzie, 1996). Thirteen new supergiant fields (assuming the maximum of 50 billion barrels each) would provide the expected 650 billion barrels, but as there are only 40 known to date (averaging only a fraction of 50 billion barrels each) (Ivanhoe and Leckie, 1983; MacKenzie, 1996), this is equally improbable. Because of the extent of global exploration since 1970, enormous oil fields in the numbers necessary would have been discovered already if they existed. There may be a few giant fields yet undiscovered and possibly a supergiant will surprise us all, but clearly this does not add up to 650 billion barrels. The small oil fields (6% of all oil discovered to date) yet to be discovered will not make up the difference. Even if the full 650 billion barrels of yet-to-be-discovered oil really did exist, assuming that the current rate of discovery (6 billion barrels per year) remains constant rather than continuing to decline, it would take over 108 years to find it all and longer still to produce that oil. The peak in global production would not be postponed even under these idealized hypothetical conditions.

A more reliable figure than those for the reserve estimate or the amount yet to be discovered is the amount of oil produced so far, and that is widely accepted as approximately 830 billion barrels (American Petroleum Institute, 1998). Using all these figures, an estimate of the ultimately recoverable oil can be calculated. Assuming reserves of 730 billion barrels and 650 billion barrels yet to be found, and bearing in mind the problems associated with those figures, these quantities, in addition to the 830 billion barrels already produced, yield 2,210 billion barrels of ultimately recoverable oil. This is just above the average of the most widely accepted range of estimates. MacKenzie (1996) reports that of the 40 estimates of ultimate oil production made between 1973 and 1993, 70% fall within the range of 2,000-2,400 billion barrels.

The bottom line of the debate between many economists and geologists is how long the conventional supply will continue to be available in increasing quantity and at low cost. The global production rate will begin to decline when the world has produced approximately half of the ultimately recoverable oil; the question is: When will this threshold be crossed? That estimate depends on the amount of ultimately recoverable oil, for which estimates vary, and on the rate of increase in the annual production rate, which also varies from year to year and is not precisely predictable. The average annual rate of increase in production for 1994 and 1995 was 1.74% (American Petroleum Institute, 1998). Assuming the ultimately recoverable oil (Q) is 2,210 billion barrels and that growth in the production rate continues to average 1.74% annually, the midpoint will arrive in 2009. However, after 1995, the production rate grew faster than 1.74% annually. Global petroleum production increased by 2.59% during 1997 (American Petroleum Institute, 1998). Assuming that Q equals 2,210 billion barrels and also assuming a steady 2.59% annual increase in the production rate, the midpoint arrives in 2008. These estimates are calculated using a low, but reasonable, value for the ultimately recoverable oil. For comparison, calculations based on higher totals for Q have also been completed. Because future production rates are difficult to predict, a widely used average rate of 2% annual growth has been used. Assuming that Q is 2,400 billion barrels, the high end of the most widely accepted range for Q at 2% annual growth in production, the threshold will occur in 2012.

Suppose that geologists, as they are often accused of doing, have somehow grossly underestimated the amount of petroleum yet to be discovered. Richard Miller, with the British Petroleum Research Center, believes that geologists have indeed made this error and that the ultimately recoverable oil figure is 4,000 billion barrels – not 2,000 to 2,400 billion barrels (Miller, 1992). Assuming that Q is 4,000 billion barrels – nearly double the average accepted estimates, at an average increase in the production rate of 2% per year, the midpoint and beginning of the permanent decline in global conventional petroleum production will arrive in 2032. Doubling the amount of oil, adding 2 trillion barrels, only increases the period of growth in oil production by 20 years.

It is important to remember that the suggested peak in production is dependent on continued growth in the production rate. If the production rate were to stop growing or even be reduced by a drop in demand or by political disruption, the beginning of the permanent decline in global production would be delayed several years beyond the midpoint of ultimate production.

From 1979 to 1983, global production declined 16%. L.F. Ivanhoe (1996) states that, were it not for the 1973 and 1979 oil shocks and the succeeding restrictions in the production rates of the OPEC nations, global oil production would have peaked in the mid-1990s. Figure 5 shows production for several OPEC nations from 1975 to 1995. Overall production was restricted from 1979 to the mid 1980s as the increase in demand for OPEC oil dropped due to temporary fuel conservation as well as increasing production from non-OPEC nations. This restriction on OPEC production will delay the peak in production for the OPEC nations. Clearly, such fluctuations can affect the timing of the peak in global production. However, the global oil-production rate has grown more than 20% since 1982. The greater the increase in the production rate, the sooner the peak in production and inevitable decline comes. More today means less tomorrow.

This also illustrates the misleading nature of many reports, including the following from The Economist (1995), “Proven reserves of oil are now enough to supply the world for 43 years at current rates of production….” The offending phrase is “at current rates of production” – meaning zero growth in the oil-production rate – a situation that has never existed for very long, and considering the explosion in demand from newly developing countries and from prosperous economies like the United States, is not likely to exist in the near future. A four-decade supply at the current consumption rate is a three-decade supply with 2% annual growth in the consumption rate. Furthermore, the view expressed in The Economist implicitly – assumes that high production rates can be maintained until exhaustion of the resource and then suddenly drop to zero. Jean Laherrere points out that one cannot simply divide the reserve amount by the annual production and assume the global oil supply will last that many years. Maintaining production at a steady annual rate requires continual additions to reserves. All oil fields decline during the second half of their life; current production rates can only be maintained if new discovery matches production (MacKenzie, 1996). But, as has been discussed, discovery has been declining for more than three decades and has not kept pace with production, which has been increasing.

Conclusion

Many of the numbers presented here are uncertain but are accurate enough for the warning to be heeded. Petroleum is a finite resource, and the production of conventional petroleum will probably peak within the next 15 years and then begin its permanent decline. It may not decrease at a steady rate, but it will decrease. The era of inexpensive, abundant oil is drawing to a close. Even if we chose to believe the improbable 4,000 billion-barrel estimate for the ultimately recoverable conventional oil, there still would be only roughly 35 years until the decline begins, assuming growth in the oil-consumption rate does not exceed 2% annually and also assuming that the discovery rate reverses its 35-year decline. That improbability would see many of us comfortably into retirement and beyond, but what of our children and grandchildren? In recent history, a woeful lack of foresight and responsibility on behalf of the coming generations has been demonstrated; will we also leave them to inherit this problem?

Petroleum production and demand are continuing to increase, and discovery has been declining for 35 years. Unconventional sources such as tar sands and heavy oil are slow and expensive to produce. Immediate conservation and improved efficiency of petroleum use, as explained by Hatfield (1994), are necessary to extend the conventional supply long enough for alternatives to be developed. In fact, Hatfield maintains that with a permanent 2.4% annual decrease in global petroleum production, our conventional reserves would last indefinitely. Such a permanent decrease would, of course, hamper economic growth globally and be disastrous for developing nations. It would be prudent then, to develop large-volume, economically feasible, environmentally benign alternatives to petroleum before such a decrease is naturally and irreversibly imposed.

Our global community must begin to lessen its dependence on petroleum; not only is it a limited resource, but it is also an environmental disaster. Unconventional petroleum sources can be developed for irreplaceable petroleum products and non-petroleum substitutes for others. Earnest endeavors and commitment now may provide an easier transition for us and for our children, but, easy or difficult, the transition is coming. The public and, indeed, many of our government and business leaders are apparently unaware of this problem or have chosen to ignore it. At the December 1997 conference on global climate change in Kyoto, Japan, the finite nature of the petroleum supply was not a topic. The main discussion concerned reducing greenhouse-gas emissions voluntarily. What our leaders apparently fail to realize is that greenhouse gas emissions unavoidably will be reduced in the near future as petroleum production peaks and then declines. Nature has imposed a limit for us.

Acknowledgments

Deepest thanks to Dr. Craig B. Hatfield for introducing me to this area of geology, for the benefit of his expertise regarding this subject, for overall guidance and encouragement, and for the critical review of this manuscript.

References Cited

Adelman, M.A., and Lynch, M.C., 1997, Fixed view of resource limits created undue pessimism: Oil and Gas Journal, v. 95, n. 14 (April 7, 1997), p. 56-60.

American Petroleum Institute, 1998, Basic petroleum data book: v. XVIII, n. 2: American Petroleum Institute, Washington DC.

Campbell, C.J., 1997, Better understanding urged for rapidly depleting reserves: Oil and Gas Journal, 1997, OGJ Special, (April 7, 1997), p. 51-55.

Coy, P., McWilliams, G., and Rossant, J., 1997, The new economics of oil: Business Week, (November 3), p. 140-144.

Hatfield, Craig B.,1994, A permanent solution to the fuel supply problem: Journal of Geologic Education, v. 42, p. 432-436.

Hatfield, Craig B., 1997a, Oil back on the global agenda: Nature, v. 387 (May 8, 1997), p. 121.

Hatfield, Craig B., 1997b, A permanent decline in oil production?: Nature, v. 388 (August 14), p. 618.

Hubbert, M. King, 1956, Drilling and production practice, American Petroleum Institute, Washington DC, p. 7-25.

Ivanhoe, L.F., and Leckie, G.G., 1993, Global oil, gas fields, sizes tallied, analyzed: Oil and Gas Journal, v. 91 (February 15, 1993), p. 87-91.

Ivanhoe, L.F., 1996, Updated Hubbert curves analyze world oil supply: World Oil, v. 217, p.91-94.

Linden, Henry R., 1998, Flaws seen in resource models behind crisis forecasts for oil supply price: Oil and Gas Journal, v. 96, n. 52 (December 28, 1998), p. 33-37.

MacKenzie, James J., 1996, Oil as a finite resource: When is global production likely to peak?: World Resources Institute, Washington DC, (March), p. 1-22.

Miller, Richard G., 1992, The global oil system: The relationship between oil generation, loss, half-life, and the world crude oil resource: The American Association of Petroleum Geologists Bulletin, v. 76, n. 4, p. 489-500.

Odell, Peter R., 1997, Oil shock: A rejoiner: Energy World, n. 247 (March 1997), p. 11-14.

Anonymous, 1997, Investment incentives driving Canadian oil sands activity: Oil and Gas Journal, v. 95 (June 9), p. 25.

Anonymous, 1995, The Future of energy: The Economist, October 7, p. 23-26.