Editors: Steve Andrews, Tom Whipple

Quote of the Week

“For shale gas to be commercially produced [in the U.K.], extensive work must be carried out to better understand the potential resource base, the social…will for which remains sour. We remain highly skeptical over the longer-term viability of shale gas in the UK.” BMI Research oil and gas analysts (2/17)

Oil and the Global Economy

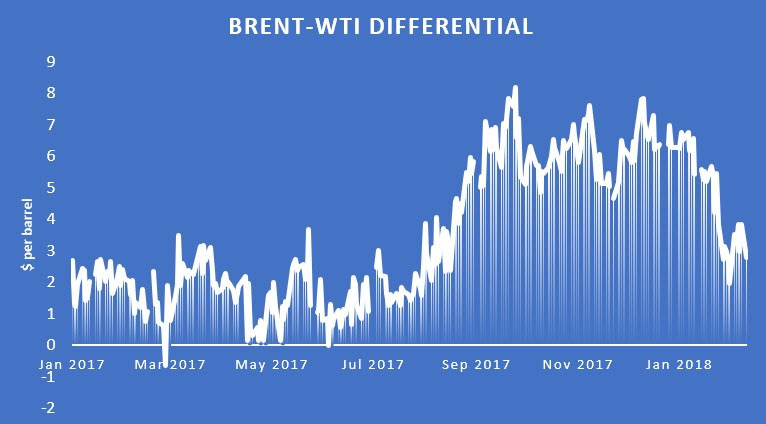

After a $7 a barrel fall between late January and mid-February, oil prices have rebounded by about $4.50 a barrel and are now in the $63-67 range. Both major oil price benchmarks, WTI and Brent, saw the second straight week of gains. There seem to be several factors behind the rebound. These range from strong demand particularly in Asia to reports that the oil glut that has obtained for the last few years is shrinking. US crude stocks fell by 1.6 million barrels last week and by 2.7 million at the Cushing hub which is receiving much of the US shale oil production. Last week’s EIA data showed US crude exports above 2 million b/d, very close to the record of 2.1 million set in October. Of note was the first export of US crude on board a 2 million barrel capacity supertanker that was loaded at the Louisianan Offshore Oil Port that has been reconfigured to handle exports as well as imports.

It has been well established for many years that higher oil prices have a negative effect on economic growth. Everything, most notably gasoline, becomes more expensive so that people of necessity slow their buying and economic slowdowns of varying proportions ensue. A recent Wall Street Journal story attempts to argue that due to the US shale oil boom which they think is likely to continue for decades, this is no longer the case. The WSJ case rests on the assertion the US has “plentiful reserves of tight oil” and that exploitation of these reserves will trigger so much economic activity it will offset whatever oil prices increases may occur. Indeed the EIA is forecasting that world oil prices will remain below $100 a barrel until the mid-2030’s. Given that global demand for oil at current prices has been increasing at an annual rate of over 1 million b/d in recent years, it is difficult to see how US shale oil production can meet this demand. There is a major disconnect in the understanding of where oil production and prices are going in the next decade or so.

The OPEC Production Cut: The latest discussions between OPEC and its oil-exporter allies concluded that the supply glut is dissipating at a faster pace than previously anticipated. After about four years of surplus, the global oil market will rebalance in the second or third quarter, earlier than previously estimated. This conclusion is based on signals of tighter supply, including Brent crude briefly surging above $70 a barrel and oil stockpiles in developed nations falling by the most in six years. OECD inventories are now just 74 million barrels above the five-year average recorded in January 2017, according to a report by Reuters. When the output reduction deal went into effect at the beginning of last year, inventories were 340 million barrels above the benchmark.

Compliance with the effort to balance the market with production cuts was supported by “several over-performing countries” mainly the Saudis, their small Gulf allies and Russia. The collapse of Venezuelan production helped OPEC while increasing production in Nigeria and Libya slowed the effort.

There are reports that OPEC and Russia, along with some other oil exporters, are looking to create a “supergroup of oil-producing countries.” The “supergroup” led by Saudi Arabia and Russia would provide a framework to manage the oil market post-2018. There is fear that the end of the current agreement later this year would result in all-out pumping that would crash oil prices once again.

The recent surge in US shale oil production complicates their plans but also makes cooperation beyond the current agreement all the more important . A world in which the US might be adding upwards of 1 million b/d of new supply in a single year is one in which OPEC’s control over output levels would be crucial to avoid another price collapse.

US Shale Oil Production: The EIA says that U.S. oil production also remained flat recently slowing the surge in oil production. Winter weather usually slows shale oil production especially in North Dakota so we can expect production increases will continue in the spring. The Energy Information Administration is saying US production could top 11 million b/d by the end of 2018, a year earlier than it had expected just a month ago.

Despite the fact that US oil production has topped 10 million b/d, approaching a record set in 1970, many investors in the companies driving the shale oil revolution are still waiting for their payday. Despite promises of focusing on shareholder returns this year, there is a divergence of strategies among the top shale companies. Reuters reports that an analysis of the top 15 largest independent shale companies finds that only five have started paying or raising quarterly dividends. Six of them have never paid a dividend or have not restored the cuts made since 2014. The remainder have kept their payouts steady.

EIA’s recently released Annual Energy Outlook 2018 Reference case projects that US shale oil production will increase through the early 2040s, when it will surpass 8.2 million b/d and account for nearly 70 percent of total US production. Tight oil production made up 54 percent of the US total in 2017. Many outside observers continue to express skepticism that the US can continue growing shale oil production for the next 25 years from the Permian Basin which is the only place the country that could potentially contain enough shale oil to support such levels of production.

Halliburton said last week that its earnings could be negatively impacted because of bottlenecks related to the supply of fracking sand used in shale drilling. Fracking sand is integral to growing shale production, as more and more sand is pumped down into newly drilled wells. Shale drillers have credited the heavy doses of sand with squeezing out more oil and gas from the average well. This claim is challenged by outside observers who say the additional sand may increase production for the first few weeks, but does not affect the amount of oil that will ultimately be recovered from a well.

Demand for fracking sand surged from 34 million tons in 2012 to 61.5 million tons in 2014, but fell in the ensuing years as drilling dried up when oil prices collapsed. Now fracking sand consumption is surpassing previous highs as drilling increases and more sand is being used in new wells. In 2018, fracking sand demand is expected to top 100 million tons, according to Rystad Energy. Much of the sand has come from places like Wisconsin, which produces “northern white sand” that is hard and round, helping to create porous fractures in shale wells. It is expensive, particularly because it has to be shipped by rail to Texas shale fields. The Financial Times reported that fracking sand could cost $120 per ton on at Texas well heads, triple what it costs at the mine in the northern U.S.

2. The Middle East & North Africa

Iran: Washington extended sanctions relief under the 2015 Iran nuclear agreement, keeping the deal intact for at least another several months. However, the Administration said it would issue no more such waivers as it negotiates a modified deal with European allies. The US Treasury Department, however, imposed new punitive actions not directly related to the nuclear deal. These new measures are meant to pressure Tehran over ongoing missile tests and a recent crackdown on Iranian protesters. In response to the new US sanctions, Tehran said it would retaliate against the new sanctions. Russian Foreign Minister Sergei Lavrov said Moscow would not support attempts by Washington to modify the Iran nuclear deal.

A review of the 14 days of the demonstrations that began on December 28th shows that there were at least 213 anti-government protests and 34 pro-regime rallies across 90 cities. The protests were caused by working-class grievances, and they swept through provincial cities and towns. The demonstrations were smaller than the massive marches that took place during the 2009 Green Movement.

Iran is being subjected to serious water shortages, much to the concern of officials who fear protests and civil strife if conditions do not improve. There is talk of rationing water in the capital, Tehran, one of the largest cities in the Middle East, because the usual autumn rains did not come. “God is always testing people with various kinds of disasters,” Ayatollah Ostadi, a member of the Supreme Council of Seminaries, said in a sermon in the holy city of Qom. “We ask God’s forgiveness for our sins through rain.”

Oil minister Zanganeh said in an interview that oil production for the West Karoun oilfields for the Iranian month of Dey, 161,000 b/d last year, was up to 305,000 b/d for the same period this January. He also said OPEC members are likely to stick to production limits through the end of 2018 and that Iran’s daily gas production at South Pars, the world’s largest gas field, has increased by 83 million cubic meters in the past year.

Iraq: Iraq’s oil production remained strong in January, averaging about 4.54 million b/d, roughly in line with the trend that rounded out 2017. Fields under control of the federal government produced 4.18 million b/d and those controlled by the autonomous Kurdistan Regional Government produced 368,000 b/d. Iraq has boosted refining activity in the past year by at least 60,000 b/d, thanks to a patchwork of Oil Ministry projects. The ministry also has undertaken a series of new refinery projects that would create over 1 million b/d of new capacity, including a tender for a refinery south of Mosul. International companies, however, have shown reluctance to invest due to the financial uncertainty associated with the country’s subsidized fuel market.

Iraqi oil minister Jabbar al-Luiebi visited Turkey last week to discuss the future of the Ceyhan-Kirkuk oil pipeline. Turkey and Iraq are warming to each other as the two nations seek to undermine the ability of factions within their Kurdish minorities to further claims for an independent state. Baghdad wants all Iraqi oil shipments to be sold via the state marketer SOMO. Government requests to Kurdish authorities to restart exports through the pipeline connecting Ceyhan directly have been ignored.

Saudi Arabia: Aramco has considered the possibility of shipping US crude via its Motiva unit to Asia, decided that for the time being the option is economically unviable, but could reconsider in the future. Such a sale would be unprecedented, and a potential strategy by the Middle East nation in the face of rising US production.

A key facet of Saudi governance has been the allocation of oil revenues to the population in exchange for loyalty to the ruling Saud clan. However, a key weakness of the Vision 2030 renewal plan is its lack of focus on the potential political consequences of economic reforms. The plan seems to assume that its ramifications will be easily borne by the Saudi population. The IMF, however, says that the failure of the reforms to produce economic growth and private sector jobs for Saudis may lead either to rising unemployment and social pressures or increased public employment. If the government becomes unable to sustain its current level of payouts to the population, this will almost certainly result in rising dissent. So far the government has been able to keep the lid on through tough security measures, but the country is entering a stage of major economic reforms that will produce new stresses.

Speculation continues about who will be the ultimate buyer of the five percent share of Saudi Aramco. As political and economic uncertainties mount in Saudi Arabia, and oil prices continue to remain relatively low, there is the question as to whether the Saudi Aramco IPO would be viable. While courted by Western stock exchanges because of the unprecedented size of a possible IPO, it is possible that a direct sale to a Chinese consortium would serve the objectives of both the PRC and Saudi Arabia. The Saudis would not have to disclose as much about the operation of the company, and it would increase Beijing’s ability to push for oil to be priced in the renminbi. It even could have broader strategic implications including giving the Chinese some sort of preferred access to Saudi crude.

The Trump administration is looking at selling nuclear reactors to Saudi Arabia despite the kingdom’s refusal to accept the most stringent restrictions against the proliferation of nuclear weapons. US officials say a deal with the Saudis could open a new market worth tens of billions of dollars. Russia, South Korea, and China are also competing for the business. The Saudi Arabian resistance to the toughest proliferation controls—a ban on enriching uranium or reprocessing spent fuel—already is stirring concern among US lawmakers. Saudi Arabia has hired an international law firm specializing in energy regulation in its efforts to extract a favorable agreement on civil nuclear cooperation from the United States.

Libya: Libya’s National Oil Corporation has evacuated its workers from the 90,000 b/d El Feel oil field amid threats from the field’s guards who are locked in a pay dispute with the company. The guards are from the Petroleum Facilities Guards group that held all of Libya’s oil export terminals under a blockade for more than a year until September 2016. There has also been talk about a wider disruption to oil production which might affect Libya’s largest oilfield—Sharara—which can produce 300,000 bpd of crude.

3. China

China and other countries in Southeast Asia are helping erase the LNG glut, which was thought to last well into the next decade. Beijing is making an aggressive push to scrap coal burning, particularly in smoggy cities, replacing home coal furnaces with natural gas. The effort has been so successful, arguably too successful, that there have been natural gas shortages this winter. At the start of 2017, there was an estimated 340 million tons of annual LNG export capacity around the world, up by more than a quarter since 2012. But all of the new capacity helped crash prices. At the start of 2014, for instance, spot LNG prices in Asia were about $20/MMBtu. A year later, spot cargoes were down by two thirds.

The surge in demand since China began switching from coal to natural gas in many eastern cities has been spectacular. In 2017, there was a 46 percent increase in LNG imports into China as it became apparent that domestic production could not keep up with demand. Analysts are saying that there is little likelihood of another 46-percent jump in imports in 2018. The critical factor for another large increase would be the speed at which China can build LNG storage facilities. China has plans in place to expand its underground gas storage capacity to 15 billion cubic meters by 2020 and raise this further to more than 30 billion by 2030. Right now however, China lacks sufficient capacity to buy and store LNG during the summer, when demand is the weakest and prices the lowest, and use the LNG in the winter during peak demand as the fuel is mainly used for heating and industrial activity.

China will exceed US nuclear power production “soon” due to recent initiatives by Beijing to accelerate adoption of nuclear power as a substitute or addition to coal powered generation stations. Beijing’s total capacity may also surpass that of the European Union, “Today there are about 60 nuclear power plants under construction around the world, and more than one-third of them are in China. As a result, we’ll soon see China overtaking the United States as the number 1 nuclear power in the world.”

4. Russia

Moscow’s economy may come to feel a negative impact from the OPEC-led oil production cut deal, the Russian central bank warned last week. The bank added that it expected GDP growth during the first quarter of the year to stand at 0.4 percent on a quarterly basis and rise to 0.5 percent quarter-on-quarter in April-June. Russia agreed to cut 300,000 b/d from its post-Soviet record-high oil production of over 11.2 million b/d in November 2016, to aid efforts by OPEC and other exporters to relieve a global glut that sank prices to less than $40 a barrel.

Russia’s much-hyped Yamal LNG in the Arctic Circle opened in December 2017. Despite difficult permafrost conditions and financial limitations imposed by US sanctions, Yamal LNG was finished on time and on budget. The project’s website praises the plant’s unique location as an opportunity for flexible and competitive logistics which will enable year-round energy supplies to the Asia-Pacific and European markets. Yamal LNG’s delivery flexibility, however, is constrained by conditions in the Arctic. Between December and April, the Northern Sea Route connecting the Yamal Peninsula and the Asia-Pacific is closed, forcing shipments toward Europe.

Turkey has yet to issue a permit for Russia’s Gazprom to start building the land-based part of the TurkStream gas pipeline, stoking fears the strategically important project will be delayed. If completed, the $8.6 billion pipeline would allow Russia to reduce its reliance on Ukraine as a transit route for its gas supplies to Europe. Ankara has authorized Gazprom, which has a de facto monopoly on Russian gas exports by pipeline, to start building two undersea sections of the project. However, it has still not given Gazprom permission for the land-based segment to ship Russian gas onward to southern Europe.

5. Nigeria

There is no end in sight for the Nigerian fuel crisis, which began in November 2017. Most filling stations are out of fuel despite claims by the Nigerian National Petroleum Corporation, NNPC, that it increased its allocations to meet growing demands. Nigeria requires 625,000 b/d of gasoline imports daily. The state-run company says it is taking action to “increase supply and replenish strategic reserves,” by offering more favorable terms for existing fuel swap arrangements. The NNPC is the nation’s only gasoline importer, and its Direct Sale-Direct Purchase program is failing to bring in adequate fuel supplies. The program, which trades about 800,000 b/d of crude in return for refined products, is due to be renewed in April.

The endless corruption probes roll on. An ad-hoc committee of the House of Representatives began yet another probe into the alleged loss of crude oil in Nigeria worth $21 billion. The House had directed the committee to investigate the debts owed to indigenous companies by International Oil Companies which many claim are not being paid. Several years ago, the government brought in a US accounting firm to trace the allegedly missing money. The firm reported that lack of cooperation by government officials and bad record keeping made it impossible to trace all the oil revenues the country has received.

Tension is brewing again in Ogoni ethnic nationality of Rivers State following the insistence by Movement for the Survival of Ogoni People that the people of Ogoni have not yet allowed any oil company to resume exploration on their land. This came as some royal fathers in Ogoni endorsed RoboMichael Nigeria Limited to explore for oil. Twenty-five years ago Shell Petroleum Development Company abandoned Ogoni after a face-off with the host communities over environment degradations caused by oil exploration.

6. Venezuela

While some expect that Venezuela’s oil production could fall by another 700,000 b/d this year to the vicinity of 1 million b/d, a leading expert on the Venezuelan oil industry points out that much of the country’s current oil production is coming from joint ventures with international oil companies. These organizations do not have the same problems as PDVSA, in that the IOC’s are well run, do not face political pressures, have the money for necessary maintenance, and to feed and pay their workers. Given the presence of foreign oil companies, there may be a floor below which Venezuelan oil production will not sink unless there is a complete societal breakdown.

PDVSA has told its employees that they are not allowed to follow users on social media except for those officially authorized by the company. The ban came a few days after it emerged that PDVSA is losing workers by the thousands, with as many as 10,000 leaving the company in just one week of January. As of August 2016, there were 143,000 people working for PDVSA, but the number has dwindled significantly since then.

Venezuela’s government on Tuesday launched the world’s first sovereign cryptocurrency, the “petro”, to help its collapsing economy. The government is trying to sell $2.3 billion worth of the new form of money. Theoretically, the petro is backed by Venezuela’s reserves of precious metals like gold and crude oil; however, the petro does not give investors any ownership stake in Venezuelan oil. Most economists say the petro won’t solve Venezuela’s many problems, including food shortages, plummeting oil production, and a mass exodus.

The Aruba government said on Thursday it started talks with the US after Citgo Petroleum slowed work on an overhaul of the Caribbean island’s 235,000-barrel-per-day refinery due to a lack of credit. The lack of financing had delayed work to restart the idled refinery this year and to convert it into an oil upgrader, Citgo said earlier this week. Some 600 local workers who had been hired to work on the overhaul have lost their jobs.

7. The Briefs (selections from the press – date of article in Peak Oil News is in parentheses – see more here: news.peak-oil.org)

Norway’s $1 trillion sovereign wealth fund, the world’s largest, will avoid investments in energy sources such as coal that are unlikely to be needed in a future low-carbon society. (2/24)

Offshore Norway, production from the Johan Sverdrup oil field in the North Sea is due to begin in 2019 and could peak at around 440,000 b/d. Phase 2 production, which is expected by 2022, could push total capacity to 660,000 b/d. (2/21)

Brent basket: On the back of its ever-evolving importance in global crude trading and pricing, Dated Brent itself is facing a period of evolution. The Brent basket is likely to see further additions beyond Troll in the coming years as production in the region continues to evolve. The largest projects in the North Sea particularly Norway’s huge Johan Sverdrup field, set to begin the first phase of production in late 2019 – are of a significantly different quality to the existing basket. Meanwhile, production at the light, sweet fields that currently make up the BFOE basket is continuing to fade.

BP on peak oil: Global demand for crude oil could peak in the next two decades, as renewables like solar power surge faster than expected to meet a greater share of the world’s energy needs, BP said Tuesday. The world’s appetite for oil and other liquid fuels could continue to grow until around 2035, hitting 110.3 million barrels a day—compared with 95 million barrels a day in 2015—before plateauing and falling off in the run-up to 2040, the British oil-and-gas giant said Tuesday in the main future scenario. (2/21)

BP on EVs: The emergence of self-driving electric cars and travel sharing are set to dent oil consumption by 2040, oil and gas giant BP said, forecasting a peak in demand for the first time. (2/21)

Russia’s oil production in the Arctic will reach peak levels in the 2020s, head of the state commission on natural resources Igor Shpurov said. Over 2017, he said, Russia produced in the Arctic about 76 million tons of oil, and the production would be growing to 2026 hitting a record of 122 million tons a year. (2/16)

Italy’s energy company Eni said Friday its production in December reached an all-time high of 1.92 million barrels of oil equivalent per day, attributing much of its gain to offshore Egypt. Full-year production averaged 1.82 million barrels of oil equivalent per day, up 3.2 percent from 2016. (2/17)

Offshore Cyprus: Italy’s Eni has put on hold the activities of a drillship that had been preparing to explore for gas after a standoff with Turkish military vessels in the area. A diplomatic solution to the dispute is being sought. The confrontation comes after Eni and its partner Total made a major gas find offshore Cyprus with the Calypso well, which reignited tensions with Turkey that believes its citizens in northern Cyprus have an equal right to the island’s offshore resources. (2/23)

Cyprus update: five vessels from the Turkish Navy have stopped a drillship commissioned by an Italian company to drill in the waters offshore Cyprus. The Cyprus News Agency reported the Saipem 12000 drillship commissioned by Eni was stopped Friday morning as it tried to reach its drilling location in the Mediterranean Sea. (2/24)

Turkey has yet to issue a permit for Russia’s Gazprom to start building the land-based part of the TurkStream gas pipeline, three sources familiar with the matter said, stoking fears the strategically important project will be delayed. If completed, the $8.6 billion pipeline would allow Russia to reduce its reliance on Ukraine as a transit route for its gas supplies to Europe. (2/21)

S&P Global Platts released a blockchain-based product that will allow market participants to submit weekly inventory oil storage data to the United Arab Emirates’ Fujairah Oil Industry Zone (FOIZ) and the relevant regulator, FEDcom. The system provides a fully auditable trail of the reported data. (2/23)

Kazakhstan’s giant Kashagan oil field is achieving new production highs every month and has done better than 300,000 b/d, but development beyond the current phase is likely to be in small steps. Shell said there were still reliability issues with the first phase, which started producing in 2016 after more than $50 billion of investment and multiple delays and has a target of 370,000 b/d. (2/23)

Kazakhstan aims to increase crude and gas condensate production by nearly 25% to 2.15 million b/d by 2025, according to the country’s development strategy released Tuesday. The mid-term increase in the output will be underpinned by the development of the giant Kashagan oil field in the Caspian Sea and the future expansion of the Tengiz project, The output forecast is based on the assumption of a Brent oil price of $55. The country’s production amounted to 1.73 million b/d in 2017. (2/21)

In India, high refinery runs and expanding refining capacity amid a strong recovery in demand pushed India’s crude oil imports to a record 4.93 million b/d in January 2018, up by double digits compared to both December 2017 (+12.5%) and January 2017 (+13.6%), according to data compiled by Thomson Reuters Oil Research & Forecasts. (2/17)

India is expected to account for 30-40 percent of overall demand growth for energy in the next two decades. India’s oil demand alone is expected to increase from about 4.4 million b/d in 2016 to about 9.7 million by 2040. One of the key drivers of this demand is the projected five-fold increase in the number of cars in India. Saudi Arabia can bet on India not only to postpone the date for ‘peak demand’ but also to underwrite robust growth in demand for oil. (2/23)

Singapore will introduce a tax on emissions of S$5.00 per ton of carbon dioxide equivalent ($3.80/tCO2e) from 2019. The move was announced in the country’s budget on Monday and will apply to all facilities producing more than 25,000 tons of greenhouse gas emissions per year. (2/21)

Panamanian Canal: As the market embarks on a second year of record LNG exports from the Atlantic Basin and strong competition from Asia for those volumes, a potential choke point is emerging: the Panama Canal. The canal can handle just one LNG vessel a day, laden or ballast, and only during daylight hours. The vessel transit restriction will be in place until October 2018 when capacity is expected to double to two vessels a day. (2/17)

In Mexico, the front-runner in its presidential race would hit the brakes on the rapid pace of private investment in the country’s newly opened oil-and-gas sector if he wins the July election, a key adviser to Andrés Manuel López Obrador says. An administration led by Obrador, a leftist nationalist, would freeze the oil auction process at least until some “successful” results are seen from the first exploration and production blocks tendered in 2015. (2/24)

Mexico is the newest, and first Latin American, country to join the IEA. (2/20)

Mexican first: Six months after bursting on to the Mexican stock market with the third-biggest initial public offering since 2015 and the promise to become a Latin American energy champion, Vista Oil & Gas has sealed its first acquisition and is planning an aggressive 400-well drilling program in Argentina’s Vaca Muerta shale formation. A recent purchase give Vista production of 27,500 barrels of oil equivalent per day and a swath of Vaca Muerta acreage which Vista aims to bring into production next year. (2/20)

Canada’s National Energy Board has given Kinder Morgan the go-ahead to start construction work on a tunnel entrance in British Columbia’s Burnaby Mountain that will be part of the Trans Mountain oil pipeline expansion. Though this is a rare piece of good news for Kinder Morgan in the Trans Mountain saga, it does not mean that the pipeline construction will soon begin. (2/17)

U.S.’s SPR sales: Even with planned sales from its Strategic Petroleum Reserves, the US can still meet its obligations to cover an import shortage, the government said. A section of the spending bill signed by US President Donald Trump this month called for the sale of barrels from the SPR. (2/23)

US gasoline consumption has leveled off as the stimulus provided by low and falling oil prices between 2014 and 2016 has faded, so refiners are increasingly turning to diesel and customers in emerging markets. US gasoline consumption is forecast to rise by just 40,000 b/d in 2018, after remaining essentially unchanged last year, according to the US Energy Information Administration. (2/21)

Louisiana Offshore Oil Port (LOOP) loaded the first supertanker with US crude oil and it set sail from the Gulf Coast on route to Asia. The LOOP is the only US port capable of fully loading a very large crude carrier — a supertanker capable of carrying around 2 million barrels of oil — and the first outbound super-vessel from that port now steps up the United States’ competitiveness in crude oil sales overseas. The port is expected to reduce shipping costs, thus making US exports more attractive, especially on long-haul routes to the markets in Asia. (2/21)

Pipeline permit nixed: A federal judge in Louisiana revoked a permit for Energy Transfer Partners’ Bayou Bridge crude oil pipeline, halting work on a portion of the project following protests by local and environmental groups. The decision by US District Judge Shelly Dick in Baton Rouge underscores the growing clashes between energy pipeline operators expanding operations to accommodate new oil and gas flows from US shale fields and environmentalists concerned about spills and other hazards. (2/24)

ExxonMobil is close to issuing a final approval of a major expansion of its Beaumont refinery complex in Texas that could make it the largest crude oil processing plant in the US. The Beaumont Refinery currently has the capacity to process 365,000 b/d. Exxon has estimated the total post-expansion capacity for the Beaumont refinery to be between 700,000 and 850,000 b/d. The current largest refinery in the U.S., Motiva’s Port Arthur refinery in Texas, has a crude processing capacity of more than 600,000 b/d. (2/23)

Biofuels showdown? US President Donald Trump has called a meeting early this week with key senators and Cabinet officials to discuss potential changes to biofuels policy. This move was occasioned by a Pennsylvania refiner blaming the biofuels regulation for its bankruptcy. The meeting comes as the oil industry and corn lobby clash over the future of the Renewable Fuel Standard, a decades-old regulation that requires refiners to cover the cost of mixing biofuels such as corn-based ethanol into their fuel. (2/23)

Trump vs. court: A US court temporarily blocked the Trump administration from delaying or ending an Obama-era rule aimed at preventing oil and gas leaks during production, according to court documents, marking the fourth time either Congress or the courts have upheld the rule’s implementation. (2/24)

Methane madness? The evidence is now overwhelming that natural gas is not part of the climate solution, it is part of the problem. A new study finds that the methane escaping from Pennsylvania’s oil and gas industry “causes the same near-term climate pollution as 11 coal-fired power plants.” And that is “five times higher than what oil and gas companies report” to the state, according to analysis from the Environmental Defense Fund (EDF) based on 16 peer-reviewed studies. (2/22)

The natural gas industry may be one of its own worst enemies. Most energy executives underestimate how much they can cut emissions as they extract and transport natural gas, according to a survey by the Energy Institute. Producers can reduce greenhouse gas flows by 75 percent simply by improving practices in the supply chain of the fuel, which consists mainly of methane. About half of that can be cut at no net cost. (2/21)

“No” in New England: Massachusetts officials thought they were close to securing future supplies of green energy by piping in hydroelectric power from Canada. But a week after Massachusetts said yes to the $1.6 billion project, neighboring New Hampshire said no, jeopardizing the 192-mile transmission line that would bring in the electricity through the Granite State. The rejection earlier this month marked the latest example of how hard it is to build large energy infrastructure in New England. (2/24)

RE and the grid: In a new paper, which appears in Renewable Energy, the researchers outline several solutions to making clean power reliable enough for all energy sectors—transportation; heating and cooling; industry; and agriculture, forestry, and fishing—in 20 world regions after all sectors have converted to 100 percent clean, renewable energy. The present study examines ways to keep the grid stable while meeting that goal. (2/19)

Solar strong? Government mandates should keep US solar power growing, despite new Trump administration tariffs on imported solar panels that are poised to raise prices. While the tariffs may slow the rate of solar expansion, local and state policies requiring utilities to procure renewable energy will continue to help create a baseline market for solar power, particularly for large, utility-scale projects. The Trump administration tariffs —30 percent in the first year, declining to 15 percent by the fourth—will raise the price of foreign-made solar panels and cells. But technological improvements and cost savings in other areas are expected to help the industry at least partially offset the increases, utility executives and analysts say. (2/21)

Floating wind farm: Norway’s Statoil said a floating wind farm in Scottish waters shows promise for deepwater installations. During its first three months in service, the company’s Hywind Scotland floating wind farm, the first of its kind, was put to the test and performed better than expected. Hurricane Ophelia in October pummeled the wind farm with 80 mile-per-hour winds and 100 mph winds with 26-foot waves were recorded two months later during Storm Caroline. Hywind closes down during the worst weather and automatically comes back on stream when conditions improve. (2/17)

Fitch on EVs: Greater product awareness and technological changes could fast-track the adoption of electric vehicles (EVs) that could plausibly lead to a peak oil demand before 2030, Fitch Ratings said on Tuesday. Although this is not the rating agency’s core scenario for EVs growth and market penetration, Fitch warned that EVs adoption is nevertheless “an increasing threat to oil demand.” (2/21)

Self-driving vehicles: If you’re wondering why it’s taking so long for car makers to offer full autonomy, as in eye-free driving, one clue is in the amount of data required to make driverless vehicles work safely. The amounts of digital information that need to be produced and then shared in real time are absolutely staggering. Vehicles will generate and consume, and in some cases transmit roughly 40 terabytes of data for every eight hours of driving. Cameras alone will generate 20 to 40 Mbps, and the radar will generate between 10 and 100 Kbps, Intel says. Each car driving on the road will generate about as much data as 3,000 people currently do. (2/24) [Question: how much electricity will this consume?]

AZ’s breakthrough: Waymo, a unit of Alphabet, is set to launch a ride-sharing service similar to Uber, but with no human driver behind the wheel. Officials in Arizona granted Waymo a permit to operate as a transportation network company across the state on January 24th. The imminent release of a robotic fleet of fully autonomous Chrysler Pacifica minivans could be flooding the highways of Arizona, causing major headaches for Uber. (2/21)

Climate quandary: Climate change doesn’t care about politics. Or economics. Or public sentiment about science. In December, an analysis showed the most accurate climate-science models to date predicted dire effects in future years. Now, two more grim assessments have arrived. A draft report prepared by a United Nations panel says the planet has a very high risk of passing the 1.5-degree C temperature increase by 2040 that scientists say is the limit before dire effects are seen. (2/24)