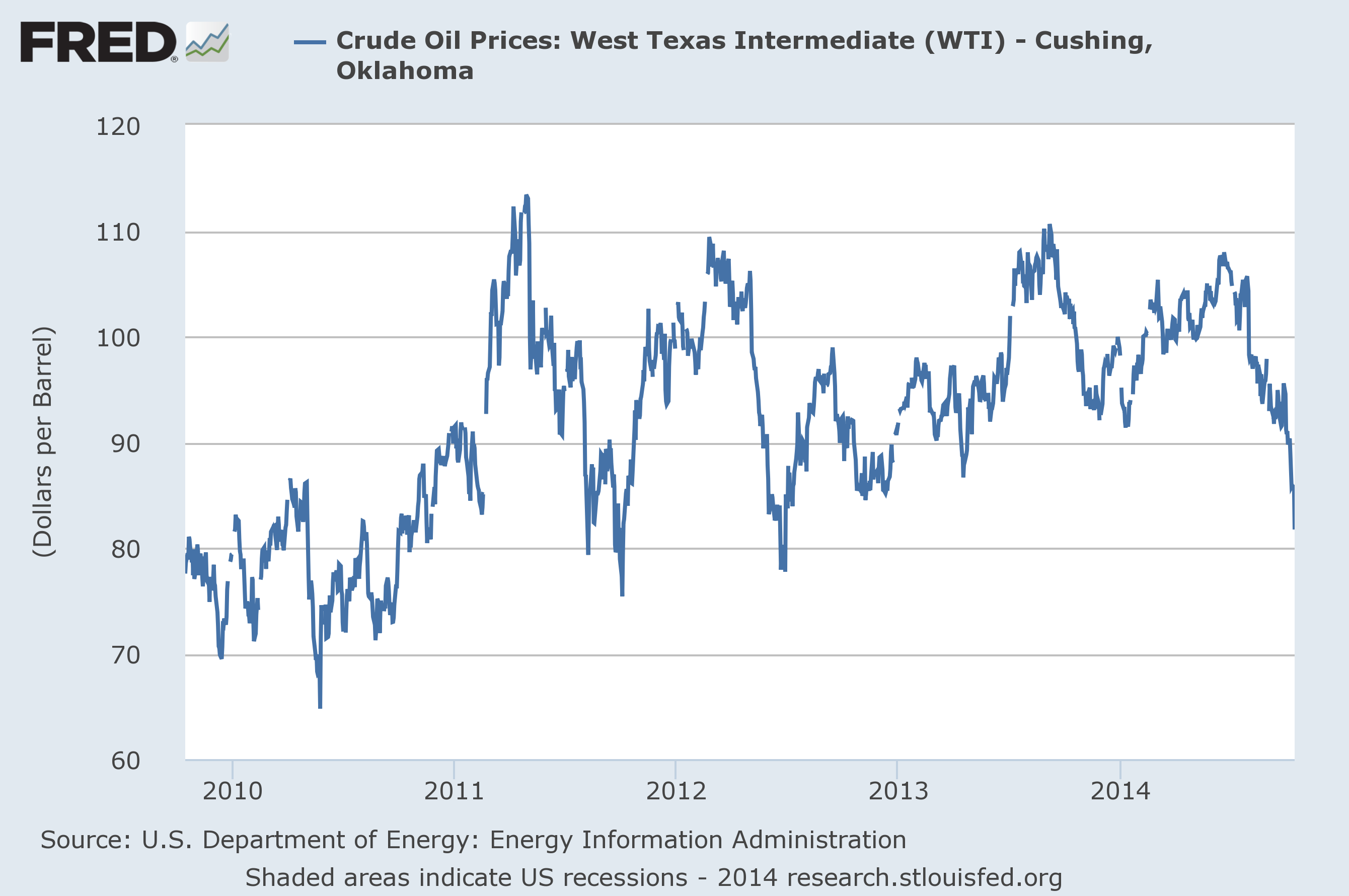

Oil prices (along with prices of many other commodities) have fallen dramatically since last summer. Some observers are waiting to see if Saudi Arabia responds with significant cutbacks in production. I say, don’t hold your breath.

Source: FRED.

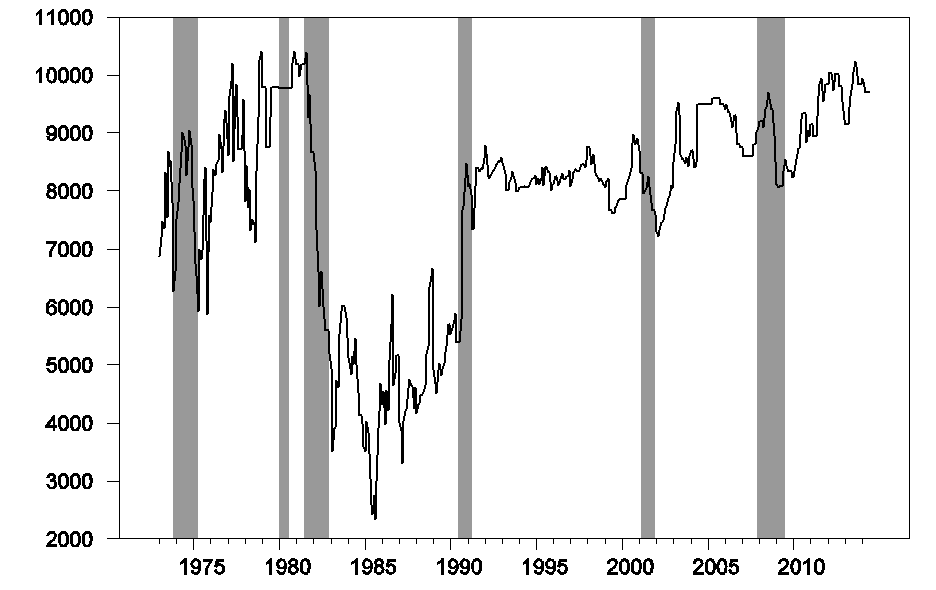

When oil demand fell in the 1981-82 recession, the Saudis cut production by 6 million barrels a day in an effort to soften the decline in oil prices. They also cut production in response to lower demand in the 2001 recession and the most recent recession. On the other hand, the kingdom boosted production quickly beginning in August 1990 and January 2003 in anticipation of lost production from Iraq in the two Gulf Wars. This historical behavior led many observers to believe that Saudi Arabia would always play the role of a swing producer to stabilize the price of oil.

Monthly crude oil production from Saudi Arabia, January 1973 to June 2014, in thousands of barrels per day. Data source: EIA. Shaded regions correspond to U.S. economic recessions.

But that’s hardly an accurate characterization of what happened during 2005-2007, when Saudi production declined even as prices skyrocketed. If that production decline was intentional, it was a dramatic departure from previous patterns. I think a better interpretation is that the market moves after 2005 became too big for the Saudis to control, and they gave up trying. I remain skeptical of the claim that Saudi Arabia is ever going to produce much in excess of 10 mb/d, regardless of what’s going on in the market.

Last week I discussed the three main factors in the recent fall in oil prices: (1) signs of a return of Libyan production to historical levels, (2) surging production from the U.S., and (3) growing indications of weakness in the world economy.

As far as Libya is concerned, the politics on the ground remain quite unsettled. It makes sense to wait and see if anticipated production gains are really going to hold before anybody makes major adjustments.

In terms of surging U.S. production, the key question is how low the price can get before significant numbers of U.S. producers decide to pull out. If world economic growth indeed slows, and if most of the frackers are willing to keep going strong even if the price falls to $80 a barrel, trying to maintain the price at $90 could be a losing bet for the Saudis. They’d be giving up their own revenue just in order to keep the money flowing into ever-growing operations in Texas and North Dakota.

And if some of the U.S. producers do move into the red at current prices, it’s in the Saudis’ longer-term interests to let that pain take its toll until some of the newcomers decide to pack up and go home. If U.S. production does decline, prices would quickly move back up. But if that happens after a shake-out, the next time there would be less enthusiasm for everybody to jump into the game if they always have to keep an eye on whether they might be undercut again. This may be less of an issue for the U.S. tight oil producers, who can move in or out much more easily than operations like deepwater or arctic, where there are huge fixed costs, long lead times, and a much bigger unavoidable loss if you gamble on prices always staying high.

And as for worries of another global economic downturn, so far they are only that– worries. If and when we see a downturn materialize, then I would expect to see the Saudis cut back production.

But until then it’s primarily a question of responding to surging output of U.S. tight oil. My guess is that Saudi Arabia would lower prices rather than cut production as long as that’s the name of the game.

And if it comes down to a game of chicken, I know who’s going to win.