(This article is an excerpt from Richard Heinberg’s book Snake Oil: How Fracking’s False Promise of Plenty Imperils Our Future.)

Fracking will end America’s reliance on imported oil. The United States can look forward to a hundred years of cheap natural gas. The US will soon become energy independent and will surpass Saudi Arabia to become the world’s foremost petroleum producer.

Fracking will end America’s reliance on imported oil. The United States can look forward to a hundred years of cheap natural gas. The US will soon become energy independent and will surpass Saudi Arabia to become the world’s foremost petroleum producer.

These are extraordinary claims, but they are not entirely without basis. To quote a gas exploration company representative’s repeated assertion at a presentation I attended in 2009, “The proof is in the production.”1 Just a few years ago, US natural gas production was declining and apparently set to go off a cliff. Instead, today’s gas-in-storage is at or near record highs, the price of natural gas has recently retreated to historic lows, and there is serious talk of exporting liquefied natural gas to other nations by ocean tankers.

Similarly, US oil production—which had been generally declining since 1970—is now on the rise, primarily because of the application of hydraulic fracturing and horizontal drilling in tight reservoirs. In 2012, US oil production soared by 766,000 barrels per day, the biggest one-year boost ever; domestic production is at its highest level in 15 years.

Nevertheless, claims that have recently been made for the potential of fracking technology to produce spectacular amounts of shale gas and tight oil for decades to come have drawn skeptical responses from some geologists. The boom has been going on for a few years now—long enough to generate data and to permit reasonable observers to gain some perspective.

In this chapter, we will review the long history of the technology behind the shale gas and tight oil booms in the United States, and the short history of the booms themselves. Then, in Chapter 3, we’ll drill into data to see whether the facts really support the industry’s claims.

A BRIEF HISTORY OF FRACKING

The essential purpose of hydrofracturing is to create and maintain fractures in oil- or gas-bearing rock; these fractures enable oil or gas to migrate toward a well bore so it can be extracted from the ground.

The idea of fracturing rock to free up hydrocarbons goes back almost to the beginning of the oil industry. In 1866, US Patent No. 59,936 was issued to Civil War veteran Col. Edward Roberts, who developed an invention he titled simply, “Exploding Torpedo.” Roberts would lower an iron cylinder filled with 15 to 20 pounds of gunpowder into a drilled borehole until it reached oil-bearing strata. The torpedo was then exploded by means of a cap on top of the shell connected by wire to a detonator at the surface. Roberts also envisioned filling the well bore with water to provide “fluid tamping” to concentrate the concussion and more efficiently fracture the rock.

The invention worked. The Roberts Petroleum Torpedo Company went on to “shoot” thousands of Pennsylvania oil wells with explosives, and production from the wells increased as much as 1,200% within the first week after the procedure. Roberts’s contracts with well owners gave him a royalty of 15% of subsequent oil production; understandably, many drillers wanted the benefit of “shooting” but not the cost, so they built their own torpedoes, exploding them at night with no observers around—a practice that gave rise to the term “moonlighting.”

In the 1940s, Floyd Farris of Stanolind Oil and Gas studied the use of water as a fracturing agent, carrying out the first hydraulic fracturing experiment in 1947 at the Hugoton gas field in southwestern Kansas. His experiments led to the first commercial application of hydrofracturing in 1949, when a team of petroleum production experts applied it to an oil well near Duncan, Oklahoma. Later the same day, Halliburton and Stanolind successfully fractured another well near Holliday, Texas. Starting in the 1970s, the use of hydrofracturing became widespread within the petroleum industry, often in efforts aimed at “enhanced oil recovery” (EOR) in conventional oil and gas fields. However, oil- and gas-bearing shale rocks remained mostly out of bounds for drillers.

In the 1980s and 1990s, George P. Mitchell of Mitchell Energy & Development, now part of Devon Energy, discovered that shale has naturally occurring cracks. Some shales are more fractured than others; if hydrofracturing could be applied where cracks are already present, large amounts of gas might easily be released.

In 1991, Mitchell pioneered the use of horizontal drilling for natural gas, guiding wells down a kilometer or so, then bending the well bore to extend horizontally another kilometer. This accomplished two things: it provided more contact between the well bore and oil- or gas-bearing strata, and it allowed producers to drill horizontally beneath neighborhoods, schools, and airports—which would prove to be a great advantage in cases like the Barnett shale, where significant gas deposits lie beneath the City of Fort Worth.

A few years later, Mitchell developed “slick-water” fracturing, which involves adding friction-reducing gels to water to increase the fluid flow in fractured wells. Mitchell then combined horizontal drilling and slick-water hydraulic fracturing, and focused his efforts on producing gas from the Barnett formation in Texas.

Over the following years, the industry worked to develop more complex mixtures of fracturing fluids with ingredients including fine sand and a laundry list of chemicals, many of them toxic. Some of these materials (such as sand) act as “proppants,” which are injected after the rock is initially fracked in order to prop open the newly created rock fractures. Other ingredients perform a range of functions, from optimizing fluid flow, to scouring the inside of the well casing. The exact formulas for fracking fluids are typically proprietary and carefully guarded. Changes to the Clean Water Act in the Energy Policy Act of 2005 exempted natural gas drillers from having to disclose the chemicals used in hydraulic fracturing, thus averting costly regulatory oversight. This came at the urging of then-Vice-President Dick Cheney, and the relevant passage in the Act has come to be known as the “Halliburton loophole,” since Cheney had a long-standing business association with Halliburton, and that company stood to benefit substantially from the exemption.

The last key technological component of modern fracking consisted of multi-well pad or cluster drilling—the drilling of up to 16 wells from one industrial platform. This enables operators to concentrate machines and material in one place so as to reduce costs and accelerate well approvals. Cluster drilling from one pad was not introduced until 2007.

Figure 14. Schematic Diagram of a Horizontal Shale Gas Well. Multiple horizontal shale gas wells are often drilled from a common platform, with each well stimulated with multiple hydraulic fracture treatments.

Source: Image Copyright (c) The Analysis Group, 2011. Used with permission.

In many respects, the industry’s newfound ability to access shale gas and tight oil pivots on these technological developments. But there is more to the story. Mitchell Energy’s focus on unconventional gas was partly motivated by the federal government’s removal of natural gas price controls and by new federal tax credits designed to promote the development of unconventional natural gas resources. In the late 1980s and early ’90s, limits to US conventional natural gas supplies were becoming apparent—limits that would lead to steeply rising gas prices in the early 2000s. The US federal government and some states began offering tax credits or severance tax abatements to companies developing tight gas, coalbed methane, or shale gas. Soaring oil prices were similarly instrumental to the development of the Bakken tight oil play. In retrospect, it’s clear that it was the bringing together of several technological innovations in the context of high oil and gas prices and changes in government regulations that made large-scale commercial exploitation of shale gas and tight oil reservoirs possible.

HOW TO FRACK A SHALE GAS (OR TIGHT OIL) WELL

Suppose you want to get in on the fracking game. Here’s a short instruction manual to get you going.

Start with a geological survey. You need to know where the gas or oil is, and you will probably wish to operate within one of the “plays” already identified by the industry (such as the Marcellus, Eagle Ford, or Bakken). But you need more than the general information that you can glean from the US Department of Energy and US Geological Survey websites—you need to know the location of “sweet spots” within these plays where production will be highest. You will be able to obtain that knowledge only by purchasing proprietary drilling data from other companies, and by drilling your own test wells. Recent technological innovations in 3-D seismic imaging will help immensely in enabling you to visualize exactly where the most prospective rock layers are.

Sooner or later you will need drilling leases—rights, purchased from landowners, to exploit subsurface mineral resources. Start with a search of land ownership records at county offices. Actual lease negotiations and signings may take place on doorsteps or kitchen tables in rural homes (as in the film Promised Land). You may want to load your boilerplate agreement with language that allows you to build roads, buildings, gates, drilling pads, and pipelines anywhere on the owner’s land; to interfere with farming, hunting, timber rights, conservation programs, and other land uses; to take millions of gallons of water from wells on the land; to leave the landowner liable for any damages caused to neighbors by your drilling practices; and to store wastewater and chemicals on the land. You’ll offer the property owner an up-front bonus payment per acre (from five hundred to several thousand dollars, depending on a variety of factors), plus royalties that promise a percentage of the value of oil or gas that’s produced. The lease will give you a three- to five-year deadline to drill. If a well is drilled, the lease stays in effect for as long as the well produces.

Once you know where you want to drill and you have a leasing agreement in hand, you’re ready to get to work. Plan the drilling site—and, if you’re drilling for gas, the pipeline route by which to move your product to market. Send some workers with earth-moving equipment to clear an area for the drilling operations: you’ll need an earthen berm enclosing a football-field-sized site. The drilling rig itself—a 120-foot-high steel structure of platforms surrounding a huge rotary drill—can be rented and assembled from about 60 tractor-trailer-loads of equipment.

Drilling will probably take two or three weeks, with steel pipe being lowered into the hole as the drill bit chews its way straight down a mile or two, then turns laterally to drill outward another few thousand feet. You’ll cement special steel pipe, called casing, into place in the uppermost parts of the well. This will protect groundwater and stabilize the well for the next stages of the process.

You’re now ready to slide a device known as a “perforating gun” down to the deepest portion of the well; this sets off small explosive charges that punch holes in the horizontal steel production casing. Once that’s accomplished, it’s necessary to flush the system with diluted acid to unclog the holes.

Now comes the hydrofracturing stage. Bring in huge pumps on semitrucks, along with four to six hundred tanker loads of water and fracking fluids. With the pumps, first drive a few million gallons of water mixed with “slickening” agents down into the horizontal leg of the casing, forcing the water through the holes to make hairline cracks in the shale. Then add microscopic grains of sand to the water to prop the cracks open.

After the well is fracked, you will “pump back” water and fracking fluid for several days to open up the well bore so that oil or gas can flow out. You may recapture the fracking fluid for reuse in the next job, or you might decide to put it in an evaporation pond, or send it off to a municipal treatment facility (which is probably poorly equipped to deal with it).

If you’ve been drilling for gas, you will now cap the well until you’ve constructed a pipeline to connect it with larger transmission pipes. If it’s an oil well, you may be able to start production right away and move the product by truck and rail tanker.

Now it’s time to drill the next well on your pad; its horizontal leg will point in a different direction from the first well. Once several wells have been drilled and you’ve finished with the pad, simply break down the rented drilling rig so its owner can truck it away to the next site. Most of your work is done.

As soon as you’ve opened the tap and started production from your new oil or gas well, you will also rehabilitate, as best you can, most of the land around the drilling site, leaving (if it’s a gas well) a fenced area the size of a large living room with several pipes protruding about three feet from the ground, along with a couple of small tanks.

Figure 15. US Lower 48 States Shale Plays.

Source: Energy Information Administration, September 2011.

Along the way, you will have had to move a lot of equipment, water, and chemicals. Altogether, each well will have generated 1,800 to 2,600 18-wheel-truck trips.

Hiring personnel, renting the drilling rig, paying for the lease, hiring trucks—all of this is expensive. By the time you turn on the tap, you probably will have invested $10 to $20 million in your well pad—which, if you’ve been drilling for gas, may produce only $6 to $15 million worth of product over its lifetime at today’s prices. If it’s an oil well, you are more likely to show a profit, though there’s no guarantee.

So why does anyone bother? That’s another story—one we’ll explore in Chapter 5.

THE SHALE GAS BOOM, PLAY BY PLAY

Meanwhile, let’s continue with our history of the recent and ongoing fracking boom. That history is dotted with the names of the “plays,” or geologic formations, where fracking is common. It takes only a few moments to grasp the essential information about each one.

As already noted, the boom got its start with the Barnett formation in the 14 counties in and around Dallas and Fort Worth, Texas. In the early 20th century, geologists had identified thick, black, organic-rich shale in an outcrop close to the Barnett Stream, which gave the play its name. But shale is hard and impermeable, so efforts to produce gas in commercial quantities from the formation came to little until the late 1990s. Mitchell Energy began development of the Barnett in 1999; subsequent operators have included Chesapeake, EOG Resources, Gulftex Operating, Devon Energy (which bought out Mitchell), XTO, Range Energy Resources, ConocoPhillips, Quicksilver, and Denbury. The Barnett is now dotted with nearly 15,000 gas wells, which are mostly concentrated in a “core” area of production in and close to Fort Worth, where the shale is thicker and yields more gas per well. Current production is 5.85 billion cubic feet per day, but production rates have hit a plateau since late 2011, despite an ongoing increase in the number of operating wells. (All well and production numbers cited in this chapter are accurate to June 2012.)

Development of the Fayetteville formation (near Fayetteville, Arkansas) began in 2002 by Southwestern Energy. A surface outcrop of organic-rich shale had been identified before 1930, but once again natural gas extraction efforts were delayed until the arrival of high prices and new technology. After confirming commercial levels of gas in the formation in 2002, Southwestern embarked on a huge and successful concealed leasing operation, securing 455,000 acres in the prime development area prior to drilling its first publicly announced “discovery” well. By late 2004, up to 25 other companies had joined the land-rush, including SEECO, Chesapeake, Petrohawk, XTO, David H. Arrington, and One-Tec (Chesapeake eventually sold its interests in the Fayetteville shale to BHP Billiton Petroleum). The area of production is spread over 25,000 square miles in parts of Cleburne, Conway, Faulkner, Jackson, Johnson, Pope, Van Buren, and White Counties and includes 3,873 wells yielding a total of 2.8 billion cubic feet per day. The recent production trend has been flat despite continued drilling, which suggests that this play is in its late-middle-age phase.

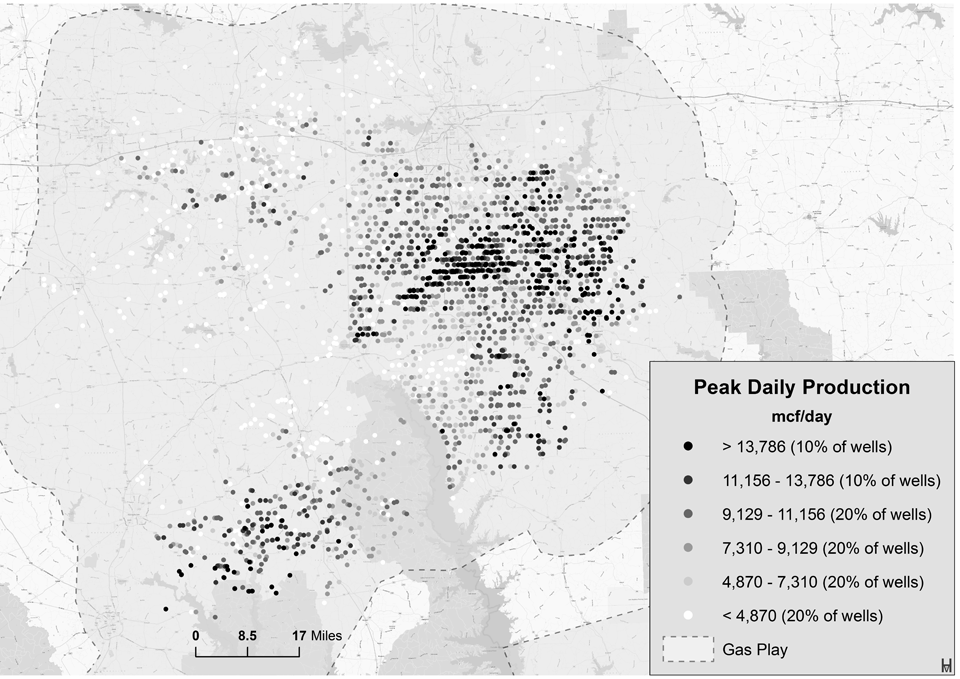

Figure 16. Distribution and Peak Daily Production of Wells in the Haynesville Shale Gas Play.

Source: Data from DI Desktop/HPDI, compiled by J. David Hughes, September 2012.

The Haynesville play, which straddles the Louisiana-Texas border, is named after the town of Haynesville in Claiborne Parish, Louisiana. Chesapeake was first on the scene here in early 2008, followed by Anadarko, Petrohawk, XTO, Exco, EnCana, J-W, EOG, and SWEPI. The leasing rush and subsequent production boom have minted more than a few new millionaires in the Shreveport, Louisiana region. The Haynesville play extends under the core Texas counties of Harrison, Panola, Shelby, and San Augustine, as well as De Soto, Red River, and Caddo Parishes in Louisiana. It has an estimated 250 trillion cubic feet of recoverable gas. In 2010 another rich natural gas reservoir, the Bossier shale, was discovered overlying the Haynesville by six to eight hundred feet. There are currently over 2,800 wells operating in the formations, producing just under 7 billion cubic feet of gas per day, roughly a quarter of all US shale gas being brought to market. While production from the Haynesville formation is the highest of any US shale gas play, it is now declining: this is a fully mature play, though it is only about five years old.

The Marcellus play underlies a large area of the Appalachian region of the northeastern United States, including the Southern Tier and Finger Lakes regions of New York, northern and western Pennsylvania, eastern Ohio, western Maryland, most of West Virginia, and extreme western Virginia. Altogether, it covers several times more area than the Barnett. It was named for a distinctive organic shale outcrop near the village of Marcellus, New York. Though a few gas wells were drilled a half century ago in Tioga and Broome Counties, New York, these produced only slowly, with a long capital recovery period. Range Resources drilled the first modern hydrofractured, horizontal Marcellus gas well in 2004, setting off a leasing and drilling boom that is still under way. Over 85 companies are currently operating in the Marcellus, including Chesapeake, XTO, Marathon, Phillips, Chevron, Anadarko, Longfellow, and True Oil. The play currently hosts 3,850 operating wells with current total production of about 5 billion cubic feet per day—a number that could increase substantially as further drilling occurs, and especially if New York State’s fracking moratorium is lifted. The Marcellus is still a youthful play.

The Utica shale is located a few thousand feet below the Marcellus shale and may have the potential to become a commercial natural gas resource on its own. It is thicker than the Marcellus and more geographically extensive, reaching much of Kentucky, Maryland, New York, Ohio, Pennsylvania, Tennessee, West Virginia, and Virginia, as well as parts of Lake Ontario, Lake Erie, and Ontario, Canada. So far, the only areas of the Utica that have been subject to leasing and drilling are in eastern Ohio and Ontario, Canada, where the formation is closer to the surface and the Marcellus is not present. Wherever the Marcellus formation is present, it is the preferred production target because it is closer to the surface and thus less expensive to drill. Current production from the Utica, from a mere 13 wells, is negligible.

The Eagle Ford play starts at the Texas-Mexico border in Webb and Maverick Counties and extends 400 miles toward East Texas; it takes its name from the town of Eagle Ford, where the shale outcrops at the surface. The play is 50 miles wide at a depth between 4,000 and 12,000 feet, with an average thickness of 250 feet, and contains both oil and gas. Petrohawk drilled the first Eagle Ford gas well with a horizontal leg and hydraulic fracturing in 2008 in La Salle County, Texas, but dozens of operators are currently active in the play, including Chesapeake, Devon Energy, Lewis, EOG, XTO, Statoil, and Talisman. Current gas production from the Eagle Ford consists of 2.14 billion cubic feet per day from 3,129 wells.

The Woodford play in Oklahoma saw minor gas production as early as 1939; by late 2004 there were 24 gas wells operating, and by early 2008 that number had grown to more than 750. The largest gas producer from the Woodford is Newfield Exploration; other operators include Devon Energy, Chesapeake, Cimarex, Antero, St. Mary, XTO, Pablo, Petroquest, Continental, and Range Resources. Production from the Woodford shale has peaked and is now in decline, with 1,827 wells currently producing a total of a little over a billion cubic feet of gas per day.

There are several plays currently producing at a lower rate, such as the Antrim shale in Michigan (9,409 wells yielding 290 million cubic feet per day with a declining trend), as well as formations that may have some future potential but are currently yielding negligible production—including the Caney shale in Oklahoma, the Conesauga and Floyd shales in Alabama, and the Gothic shale in Colorado.

Outside the United States, shale gas resources in China exceed even those of the United States; potential exists also in South America, Europe, extreme northern and southern Africa, and Australia. However, none of these regions is currently a significant producer. (In Australia, hydrofracturing is used to produce coalbed methane; a major controversy over environmental impacts is erupting there in response.)

Altogether, in just the last decade the US shale gas industry has drilled over 60,000 wells, with a total current rate of production of about 28 billion cubic feet per day. US shale gas production appears to have peaked or leveled off in late 2011 for reasons we will explore in Chapter 3. The drilling boom has produced roughly 20 trillion cubic feet of gas—over a hundred billion dollars’ worth of product—and has led to the creation of hundreds of thousands of jobs (however temporary) for drillers, truckers, and miscellaneous service personnel. Thousands of households have benefitted financially from lease and royalty payments. Utilities are now burning less coal and more natural gas due to the drilling boom. And makers of US energy policy envision more of the same—cheap, abundant natural gas for as far as the eye can see.

TIGHT OIL BY THE NUMBERS

Sometimes the shale rocks that yield natural gas to hydraulic fracturing also (or instead) contain oil. But calling this resource “shale oil” creates confusion because the term is so similar to “oil shale”—a phrase customarily applied to an entirely different resource in the western part of the United States. (We’ll discuss the potential of oil shale in Chapter 6.) In order to avoid this confusion, geologists usually call crude oil that’s present in shale (or similar rock) “tight oil.” Conventional, commercially accessible oil is typically found in porous rock that is topped by an impermeable “cap rock” that keeps the oil from migrating to the surface and oxidizing. But that’s typically not where the oil formed; it migrated there from “source rock,” usually shale, which formed slowly from sediments on ancient seabeds. Tight oil is petroleum that remained in this shale source rock, kept there by unusually tight pore spaces and a lack of pathways between pores. As with shale gas, tight oil presents a challenge for drillers—one that has been partially overcome by the use of new technology.

Most production of tight oil (sometimes called “light tight oil,” or LTE) in the United States is occurring in two formations—the Bakken play in Montana and North Dakota (also in Saskatchewan, Canada), and the Eagle Ford play in south Texas.

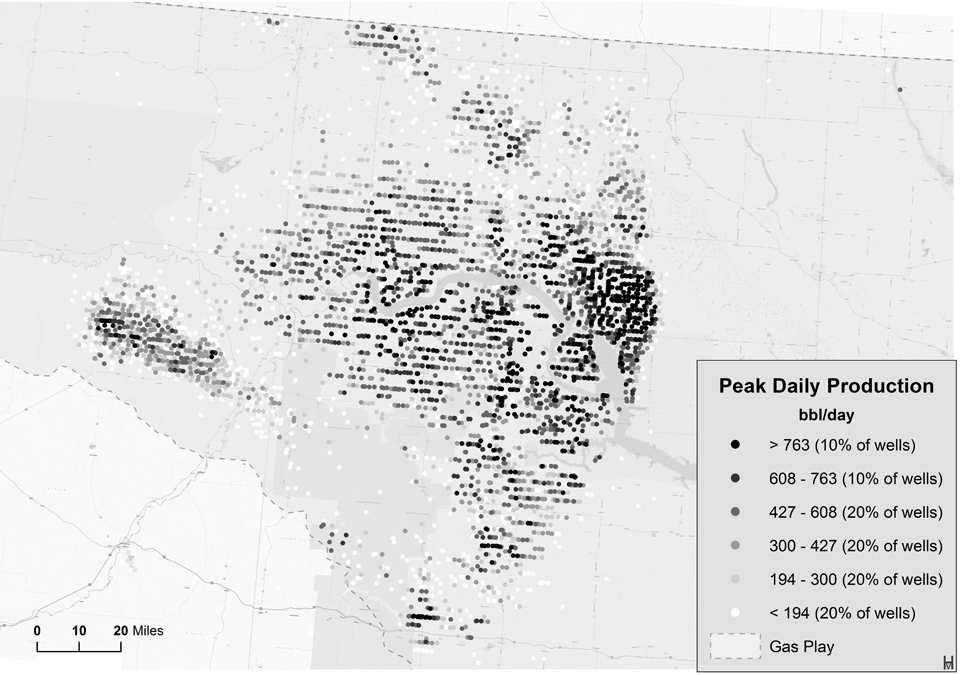

Figure 17. Distribution and Peak Daily Production of Wells in the Bakken Tight Oil Play.

Source: Data from DI Desktop/HPDI, compiled by J. David Hughes, September 2012.

Geologist J. W. Nordquist first described the Bakken formation in the Williston Basin in 1953, following an initial oil discovery at the Clarence Iverson farm in North Dakota in 1951. In 2000, Lyco Energy drilled the first horizontal pilot well into the Bakken; five years later EOG Resources demonstrated that horizontal drilling combined with hydraulic fracturing could recover significant oil from the play. Commercial production using modern fracking technology began in 2008, and by the end of 2010, oil production rates had reached 458,000 barrels per day, outstripping the industry’s capacity to ship oil out of the region.

Repeatedly throughout the past several decades, geologists have sought to estimate the total oil endowment of the Bakken formation. A 2008 report issued by the North Dakota Department of Mineral Resources suggested that the North Dakota portion of the Bakken contains 167 billion barrels of oil—which, if it represented oil reserves, would put North Dakota ahead of Iraq in terms of oil endowment. However, the percentage of this oil that can practically be extracted is highly debatable, with estimates as low as 1%. Companies operating in the Bakken include Anglo Canadian, Concho, Abraxas, EOG Resources, Continental, Whiting, Marathon, QEP, Brigham, Hess, Samson, and Statoil. As of mid-2012 there were about 4,600 wells producing a total of 570,000 barrels per day. While overall production from the Bakken has grown rapidly in recent years, the Montana portion of the play is already in decline. We will explore the overall potential for this play in the next chapter.

A New York Times Magazine article (“North Dakota Went Boom” by Chip Brown, January 31, 2013) chronicled the economic and social impact on life in North Dakota as a result of the leasing and drilling frenzy in the Bakken:

It has minted millionaires, paid off mortgages, created businesses; it has raised rents, stressed roads, vexed planners and overwhelmed schools; it has polluted streams, spoiled fields and boosted crime. It has confounded kids running lemonade stands: 50 cents a cup but your customer has only hundreds in his payday wallet. Oil has financed multimillion-dollar recreation centers and new hospital wings. It has fitted highways with passing lanes and rumble strips. It has forced McDonald’s to offer bonuses and brought job seekers from all over the country—truck drivers, frack hands, pipe fitters, teachers, manicurists, strippers.

Meanwhile, back in south Texas, the Eagle Ford play has seen substantial production of tight oil as well as shale gas (wells in the southeastern, deeper side of the play yield mainly natural gas while wells on the northwestern, shallower side yield mostly oil). Oil reserves are estimated at 3 billion barrels. Mid-2012 production was 424,000 barrels per day from 3,129 producing wells, with an increasing production trend.

While the Bakken and Eagle Ford together account for over 80% of current US tight oil production, there are other plays that offer varying degrees of promise. The Granite Wash formation, straddling the northern Texas-Oklahoma border, produces roughly 41,000 barrels per day from 3,090 active wells with a rising trend. The Cline shale, located east of Midland, Texas, in the Permian Basin, produces about 30,000 barrels per day from 1,541 wells; here again, production is increasing. Tight oil is also being produced from the Barnett shale in Texas, where 14,871 wells yield only 27,000 barrels per day. In this play the production trend is flat.

The Niobrara formation in Colorado and Wyoming presents problems with complex geology and access to water, especially given the severe drought that has gripped much of the United States, and Colorado’s recent catastrophic wildfires. Early comparisons with the Bakken have not borne out, and disappointing well results have led Chesapeake to sell off its Colorado leases. Noble, Anadarko, EOG, Quicksilver, and roughly a dozen other mostly small companies are competing in the play, with about 40 active drilling rigs. However, 10,811 operating wells currently yield a mere 51,000 barrels per day of production, and the production trend is flat.

The Austin Chalk play (which reaches across Texas and into Louisiana) and the Spraberry play (near Midland, Texas) each produce over 17,000 barrels per day.

The Monterey shale in Kern, Orange, Ventura, Monterey, and Santa Barbara Counties in southern California boasts tight oil resources of up to 15 billion barrels—four times the size of Bakken reserves. But resources are not the same as reserves, and so far production amounts to only 8,580 barrels per day from 675 operating wells, with a flat production trend. This could change if drilling picks up, in view of the Monterey’s very high resource endowment.

Elsewhere in the world, geology appropriate for the production of tight oil using fracking technology exists in R’Mah formation in Syria, Sargelu formation in the northern Persian Gulf region, Athel formation in Oman, Bazhenov formation and Achimov formation of west Siberia in Russia, Coober Pedy in Australia, and Chicontepec formation in Mexico. Little is yet being done to exploit these resources.

THE CLAIMS RUSH

It may be helpful to pause at this point and recall again where we were at the start of the fracking boom. US oil production had generally been in decline for nearly four decades, oil and gas prices were high and rising, and mainstream media outlets were beginning occasionally to mention the possibility that world petroleum output was near its inevitable peak. In this context, rising gas production from north-central Texas, Arkansas, Louisiana, and Pennsylvania, and soaring oil yields in North Dakota and south Texas seemed like answers to a prayer. Here was an opportunity for the industry to beat back its critics—and make a lot of money in the process.

The situation recalls events in the 1970s. Oil price shocks during that decade, along with declining US oil production, provoked discussion about ultimate limits to petroleum supplies. America experienced a natural gas crisis as well: wellhead prices jumped more than 400% between 1971 and 1978, while production declined more than 11%. The oil dilemma was resolved by new discoveries in Alaska and the North Sea: petroleum prices declined in the 1980s and stayed low for over a decade. The US natural gas market was eventually rebalanced by demand destruction, with reduced consumption leading to stable and affordable prices that would last, again, until the early 2000s. Throughout the late 1980s and the 1990s, cheap oil and stable, affordable gas prices enabled Americans to forget about the need for energy conservation and the development of renewable energy sources, and to concentrate on their favorite pastimes—driving and consuming. Might the fracking boom offer similar relief to the oil and gas price spikes of the 2000s? The industry obviously thought so, and it was determined to make the most of the opportunity.

But there was a more immediate, practical motive for oil and gas companies to ballyhoo fracking’s significance: their need for investment capital. Small operators willing to assume substantial risk by developing marginal resource plays using expensive technology have led the fracking boom from its inception. These companies need investors to believe that fracking is the Next Big Thing. As in every resource boom since the dawn of time, hyperbole has become a tool of survival.

The hurricane of hype began in the shale gas fields of Texas, stirred by the charismatic Aubrey McClendon, then-CEO of Chesapeake Energy. McClendon hammered home the same message on every possible occasion—at investment conferences, in government hearings, and in prominent media interviews. For example, in testimony before the US House Select Committee on Energy Independence and Global Warming on July 30, 2008, McClendon had this to say:

America is at the beginning of a great natural gas boom. This boom can largely solve our present energy crisis. The domestic gas industry through new technology has found enough natural gas right here in America to heat homes, generate electricity, make chemicals, plastics and fertilizers, and most importantly, potentially fuel millions of cars and trucks for decades to come.

Another highly visible shale gas booster was Daniel Yergin, chairman of Cambridge Energy Research Associates, an oil and gas industry consultancy. In an April 2, 2011, article in the Wall Street Journal titled “Stepping on the Gas,” Yergin wrote: “Estimates of the entire natural-gas resource base, taking shale gas into account, are now as high as 2,500 trillion cubic feet, with a further 500 trillion cubic feet in Canada. That amounts to a more than 100-year supply of natural gas.”

A century of natural gas! It was a nice round figure, and big enough to banish any fears of looming scarcity. The number came to be repeated so frequently that even President Barack Obama parroted it unquestioningly, as in this public statement on January 25, 2012: “We have a supply of natural gas that can last America nearly 100 years, and my administration will take every possible action to safely develop this energy.”

But was one hundred years really enough?

Oil billionaire T. Boone Pickens, whose hedge fund had adopted significant positions in the natural gas sector starting in 1997, began running a series of television and print advertisements in 2008 to promote his “Pickens Plan” to “break the stranglehold of imported oil” using domestic natural gas for transportation. In an interview on CNBC in April 2011, he estimated America’s natural gas endowment: “If I announced that we have more oil equivalent than the Saudis do, I would be telling you the truth. . . . I say you’re going to recover 4,000 trillion [cubic feet]. Which is 700 billion barrels.” It turns out that 4,000 trillion cubic feet (tcf) is roughly the equivalent of 160 years of US natural gas production at current rates.2

A hundred years? 160 years? Why not more? So far, Aubrey McClendon appears to have topped all rivals with his claim, in an article on Chesapeake Energy’s website, that America has two hundred years of natural gas.3 In his most widely heard prediction about the importance of shale gas, in a CBS News 60 Minutes interview that aired on November 14, 2010, McClendon told Leslie Stahl: “In the last few years we have discovered the equivalent of two Saudi Arabias of oil in the form of natural gas in the United States. Not one, but two.” As if betting in a poker game, McClendon seemed to be saying, “I’ll see your Saudi Arabia and raise you one! And I’ll double down on that ‘hundred years,’ too!”

As we will see in more detail in the next chapter, even Daniel Yergin’s seemingly conservative hundred-year estimate is unsupportable and overstates supplies by several hundred percent. How could McClendon, Yergin, and Pickens possibly have come up with these super-optimistic shale gas supply forecasts? Simply by taking the highest imaginable resource estimate for each play, then taking the best imaginable recovery rate (based on extrapolating data from the very best-producing wells in the small “sweet spots” in each play), then adding up the numbers. Always the assumption was that the gas could be produced profitably at current prices. Only the most knowledgeable experts would know that the resulting figures were entirely unrealistic.

Fast-moving developments in the shale gas sector came as a surprise to official agencies like the US Department of Energy’s Energy Information Administration (EIA), the United States Geological Survey (USGS), and the International Energy Agency (IEA). None of these agencies had foreseen that high gas prices would lead small producers to apply fracking technology to known shale plays, and with such spectacular results. The EIA quickly sought to catch up to the industry’s achievements—in both production and public relations—by issuing new forecasts for future shale gas production. Borrowing uncritically from the gas producers’ own estimates, the EIA assigned a reserves figure of 410 trillion cubic feet to the Marcellus play alone. Soon the USGS weighed in, suggesting the real figure should be closer to 84 tcf; the EIA quickly backtracked and deferred to the USGS, cutting its own estimate for the Marcellus by 80%.4 The episode simply served to illustrate that ostensibly authoritative reserves and future production forecast numbers were in fact highly speculative, with enormous error bars.

Meanwhile, public perceptions about the prospects for tight oil followed a similar trajectory. Early resource claims for the Bakken play were all over the map. A research paper by USGS geochemist Leigh Price in 1999 had estimated the total amount of oil contained in the Bakken shale at somewhere between 271 and 503 billion barrels.5 Later estimates by Meissner and Banks (2000) and by Flannery and Kraus (2006) ranged all the way from 32 to 300 billion barrels.6

If the amount of oil in place was a matter for dispute, the question of how much of this was recoverable constituted an even more decisive unknown variable. Here the estimates ranged from as little as 1% to as much as 50%. The USGS currently estimates the Bakken to have 3.65 billion barrels of technically recoverable oil in place (the more crucial economically recoverable amount is likely substantially lower).7 That’s still a big number, but it represents only six weeks of current world oil consumption.

Again, the industry, in its public statements, focused only on the largest numbers for both resources-in-place and recovery potential. The Bakken and Eagle Ford were heralded as the biggest developments in the oil world since the invention of the drill bit. Everyone involved would get rich, the boom would last decades, and it would lead America’s energy sector into a new Golden Age of plenty.

The industry’s PR efforts received an enormous boost from Leonardo Maugeri, senior manager for the Italian oil company Eni and senior fellow at Harvard University, who published a seemingly authoritative paper in June 2012 titled, “Oil: The Next Revolution.”8 In it, Maugeri claimed that “The shale/tight oil boom in the United States is not a temporary bubble, but the most important revolution in the oil sector in decades.” Published under the imprint of Harvard’s Kennedy School, Belfer Center for Science and International Affairs, the Maugeri report painted a euphoric picture of world oil abundance: “Oil is not in short supply. From a purely physical point of view, there are huge volumes of conventional and unconventional oils still to be developed, with no ‘peak-oil’ in sight.”

At the center of this portrait of abundance was US tight oil. While Maugeri managed to identify a few other promising places such as Iraq—where production, he figured, could go from the current rate of 3.35 million barrels per day to over 5 mb/d by 2020 (a highly optimistic notion, given the political realities there)—he saved his biggest hopes for the Bakken, Eagle Ford, and other North American tight oil plays. One phrase from the report leapt out: “. . . the total production capacity of the US could even exceed that of Saudi Arabia.” According to Maugeri, the United States could get an additional 4.17 million barrels per day from tight oil plays by the end of the decade. To put that number in perspective, total US production of crude oil in 2011 was 5.68 million barrels per day. Adding 4.17 mb/d to that number would yield a total almost equal to America’s peak level of production achieved in 1970 and also close to Saudi Arabia’s current production of about 10 mb/d. Energy reporters, taking their cue from Maugeri, began adopting the shorthand term, “Saudi America.”

Maugeri’s report received uncritical notice in major media outlets, including the New York Times, the Wall Street Journal, NPR, and most broadcast and cable news television networks, and his assertions became common wisdom. This happened despite the presence of several pivotal and fairly obvious errors in the report, including Maugeri’s consistent confusion of “depletion rate” with “decline rate,” a serious underestimation of decline rates from existing oil fields, and a simple but decisive math mistake in compounding declines.9 It turned out that the report had not been peer-reviewed or even competently fact-checked. “Oil: The Next Revolution” was thoroughly debunked by experts, but none of the criticisms surfaced in publications that had turned the report into headline news. It wasn’t hard to see why: Maugeri’s twisted tune was music to the ears of the oil industry.

Official agencies began revising their oil reserves numbers and production forecasts. The EIA, in its “Annual Energy Outlook 2013,” noted that US oil import dependency had fallen from 60% of total oil consumed in 2005 to 45% in 2011; assuming further growth in tight oil output, the agency projected oil imports to fall to only 37% of consumption in 2035. The United States would not achieve oil independence, but it would make substantial progress in that direction.

The IEA likewise adopted a more optimistic attitude about future petroleum supplies. The organization’s chief economist, Fatih Birol, even called the surge in US oil and gas production “the biggest change in the energy world since World War II.”10

As with shale gas, Daniel Yergin played a key role in pumping up expectations about the potential of tight oil. “[T]echnology has opened doors people didn’t know were there or didn’t think could be opened,” he told the Wall Street Journal. “We expect to see tight-oil production grow dramatically over the rest of this decade.”11

* * *

Altogether, these were amazing developments. Prior to the fracking boom, the United States had been assumed to be a fully mature oil and gas province. Since the start of the hydrocarbon era, more oil wells had been drilled in the continental US than in all other countries combined. The nation’s peaks in oil and gas production were apparently four decades in the rearview mirror. Yet, led by technology and enabled by the treatment of mineral rights under US property law, a host of small oil and gas companies had unleashed a genie of new production potential.

Nevertheless, there was another way of framing the situation. Soaring fuel prices, resulting from the depletion of giant conventional fields, had led drilling companies to go after some of the last, least inviting oil and gas plays in North America. These operators had invented superior barrel-scrapers, but they were still in essence scraping the bottom of the barrel by producing oil and gas from source rocks.

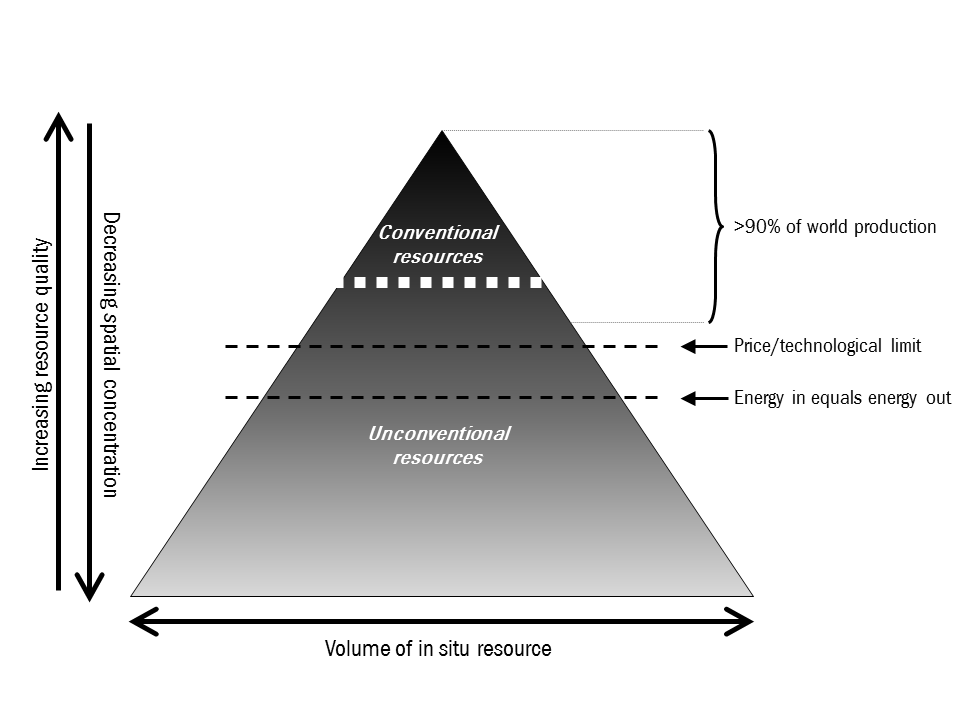

Figure 18. Oil and Gas Resource Volume Versus Resource Quality. This graphic illustrates the relationship of in situ resource volumes to the distribution of conventional and unconventional accumulations, and the generally declining net energy and increasing difficulty of extraction as volumes increase lower in the pyramid.

Source: J. David Hughes, “Drill, Baby, Drill,” Figure 37.

Every geologist understands the principle of the resource pyramid: the entire pyramid represents the total mineral resource in place. The top portion of the pyramid consists of the concentrated, easy-to-produce portion of that resource base, while lower levels correspond to more abundant but lower-quality resources that have higher production costs and whose extraction implies higher environmental risks. This mental model holds true for copper and iron mines, oil and gas fields, and even commercial fisheries. Shale gas and tight oil plays were far from the top of America’s gas and oil resource pyramids. In addition, each shale gas or tight oil play could be thought of as its own smaller resource pyramid: the best resources within each play would inevitably be targeted for production first, and, as time went on and as producers made their way down the stair steps of the pyramid, well productivity would decline and per-well decline rates would rise. Operating costs would soar. Production potentials that were forecast on the basis of extrapolating the best results from the first wells drilled into “sweet spots” in each play would inevitably prove highly misleading.

But not many analysts wanted to adopt this more realistic view. There was no money in it.

Leonardo Maugeri’s statement that “the shale/tight oil boom in the United States is not a temporary bubble” carries a whiff of resemblance to Nixon’s “I am not a crook” or Clinton’s “I did not have sexual relations with that woman”: the gentleman doth protest too much, methinks. But where lies the truth? Are shale gas and tight oil booms the “new normal” for American energy? Or do they more closely resemble a short-term Ponzi scheme?

Let’s take a closer look.

—

This article is an excerpt from Snake Oil: How Fracking’s False Promise of Plenty Imperils Our Future by Richard Heinberg.

See also:

Introduction. A Front-Row Seat At the Peak Oil Games

Chapter 1. This is What Peak Oil Looks Like

—

References

1.Peter A. Dea, President & CEO of Cirque Resources, (speaking at the ASPO-USA annual conference, Denver, CO, October 10, 2009).

2.“Interview with Boone Pickens,” JobVetka (website), last modified March 12, 2012, http://jobvetka.blogspot.com/2012/03/interview-with-boone-pickens.html.

3.“Natural Gas: Fueling America’s Future,” Chesapeake Energy (website), accessed May 10, 2013, http://www.chk.com/naturalgas/pages/fueling-americas-future.aspx.

4.Stephen Lacey, “After USGS Analysis, EIA Cuts Estimates of Marcellus Shale Gas Reserves by 80%,” ThinkProgress (blog), August 26, 2011, http://thinkprogress.org/climate/2011/08/26/305467/usgs-marcellus-shale-gas-estimates-overestimated-by-80/?mobile=nc.

5.Leigh Price, “Origins and Characteristics of the Basin-Centered Continuous-Reservoir Unconventional Oil-Resource Base of the Bakken Source System, Williston Basin” (paper presented to the Energy and Environmental Research Center (EERC)), http://www.undeerc.org/News-Publications/Leigh-Price-Paper/pdf/TextVersion.pdf.

6.Fred F. Meissner and Richard B. Banks, “Computer Simulation of Hydrocarbon Generation, Migration, and Accumulation Under Hydrodynamic Conditions—Examples from the Williston and San Juan Basins, USA” (oral presentation, AAPG International Conference and Exhibition, Bali, Indonesia, October 15–18, 2000), http://www.searchanddiscovery.com/documents/2005/banks/. Jack Flannery and Jeff Kraus, “Integrated Analysis of the Bakken Petroleum System, U.S. Williston Basin” (poster presentation, AAPG Annual Convention, Houston, TX, April 10–12, 2006), http://www.searchanddiscovery.com/documents/2006/06035flannery/.

7.“USGS Releases New Oil and Gas Assessment for Bakken and Three Forks Formations,” US Department of the Interior, April 30, 2013, http://www.doi.gov/news/pressreleases/usgs-releases-new-oil-and-gas-assessment-for-bakken-and-three-forks-formations.cfm.

8.Leonardo Maugeri, “Oil: The Next Revolution,” Geopolitics of Energy Project, Belfer Center for Science and International Affairs, John F. Kennedy School of Government, Harvard University, June 2012, http://belfercenter.ksg.harvard.edu/files/Oil-%20The%20Next%20Revolution.pdf.

9.David Strahan, “Oil Glut Forecaster Maugeri Admits Duff Maths,” David Strahan: Energy Writer (blog), July 30, 2012, http://www.davidstrahan.com/blog/?p=1570.

Image credit: 3 rigs diagram – Kurzgesagt