KSA pledges SR 30bn Egypt aid

17/12/2015

“JEDDAH: Custodian of the Two Holy Mosques King Salman has ordered that Saudi Arabia’s aid and investment package to Egypt should be increased to SR30 billion (US$ 8 bn) in the next five years.

The announcement was made by Deputy Crown Prince Mohammed bin Salman at a meeting with Egyptian Prime Minister Sherif Ismail in Cairo on Tuesday, said SPA (Saudi Press Agency)

Prince Mohammed said at the start of the meeting that King Salman ordered the increase in the package — to contribute to Egypt’s oil needs for five years and for an increase in traffic for Saudi ships in the Suez Canal.

According to a report in Bloomberg quoting Egyptian Investment Minister Ashraf Salman on Wednesday, the investment of SR30 billion would be through Saudi Arabia’s public and sovereign funds, with inflows beginning immediately. Egypt is also set to renew a deal to import Saudi oil products for five years on favorable terms, Ismail said.”

http://www.arabnews.com/featured/news/851651

This follows pledges of US$ 12.5 bn aid by Saudi Arabia, Kuwait, the UAE and Oman in March 2015, at an economic conference (EEDC) in Sharm el-Sheikh.

Will that be enough to rescue Egypt?

Let’s have a look at Egypt’s budget. In the previous post we found that Egypt’s oil production peaked in 1993. Declining and now stagnating oil production against an ever-growing oil demand of a ballooning population meant that Egypt is a net-oil importer since 2010. How did that impact on the budget? We use IMF data available from this website: http://www.imf.org/external/country/egy/index.htm

In the last years Egypt experienced turbulent times:

Feb 2011 Arab Spring, Mubarak resigns, New head of State Field Marshal Tantawi

June 2012 Morsi comes to power after winning presidential elections with 51.7% of votes

July 2013 Morsi deposed in military coup, Acting President is Head of Constitutional Court Mansour

June 2014 General Sisi comes to power

The last Article IV consultation of the IMF was in February 2015. The report sums up:

“Amidst political turmoil, chronic economic problems were left unaddressed and new problems became acute. Fiscal revenue and foreign exchange earnings collapsed while expenditure rose sharply, causing persistent inflation, large budget deficits, sizable external imbalances, and reserve loss.” (p 4)

http://www.imf.org/external/pubs/cat/longres.aspx?sk=42692.0

Let’s put the revenue and expenditure into stacked graphs, adding data from the previous April 2010 report, going back to 2005

http://www.imf.org/external/pubs/cat/longres.aspx?sk=23796.0

Revenue

Fig 1: Revenue by sector

We can see that the largest contributions are from GST and non-tax revenues. Although the IMF reports above do not define non-tax revenue, their working paper 15/98 “Tax policy in MENA countries” refers to them as non-resource revenues which comprise fees, stamp duties, transaction taxes, registration of real estate and vehicles and 100s of other taxes on specific activities.

Note that oil-related revenue does not play a big role. The gap between revenue and expenditure has been growing over the years 2005-2014. Grants from Kuwait, Saudi Arabia and the UAE improved this situation only temporarily. If low oil prices continue it will be difficult for Egypt to get additional grants in future as budgets of these 3 countries are also in deficit.

The projection period in Fig 1 shows current trends without budgetary reform. In this case the difference between expenditure and revenue will continue to grow

Expenditure

Fig 2: Expenditure by sector

The main expenditure items are interest payments on debt, wages and fuel subsidies. Interest payments are unavoidable, wages are hard to reduce and fuel subsidies are a hot political potato.

Again, projections in Fig 2 show trends without measures to reduce the budget deficit.

Structural budget reforms

Fig 3: Budget sector reforms

In order to limit the growth of the budget deficit, the IMF proposes following measures:

(a) Increasing taxes

(b) Reducing fuel subsidies

and, in order to dampen the impact on low income earners and improve the economy

(c) Lifting minimum wages

(d) Increased spending on education, health and R&D

(e) Increasing social transfers

Increasing taxes and reducing fuel subsidies will certainly not be popular. Misjudgments of public sentiment and/or wrong decisions can quickly result in street riots and political unrest.

Fuel subsidies

A huge directional change is required in order to implement fuel subsidy reforms

Fig 4 Comparison various subsidies projections IMF vs MoF

http://www.mof.gov.eg/English/Papers_and_Studies/Pages/The-State-Budget.aspx

We see that actual fuel subsidies have grown more or less in line with petroleum product imports. For the period 2005-2014 they accumulated to around 680 billion Egyptian Pounds (EGP) or US$ 90 bn. This of course has increased debt, in particular external debt.

Starting with the budget year 2014/15 there are 3 paths subsidies can go:

(i) IMF projection excluding subsidy reforms (red columns)

(ii) Ministry of Finance budget projection (brown columns)

(iii) IMF projection including subsidy reforms (yellow columns)

The IMF assumed that Egypt continues to be a net oil importer:

Fig 5: Egypt oil exports and imports

Oil price assumptions are not mentioned in the IMF report (Feb 2015) but are based on the IMF WEO Jan 2015:

Fig 6: IMF oil price assumptions

As an example, the next graph shows the difference between local and international Diesel prices for the period 1991-2015, based on data from the German Agency for International Cooperation:

Fig 7: Egypt Diesel prices vs international market prices

Data: https://www.giz.de/expertise/html/4317.html

Diesel prices are fixed in Egyptian pounds (see Fig 9) and changed by government decree from time to time. The above graph shows these domestic prices converted into US cents (brown columns), compared to international diesel spot prices on the US Gulf coast (blue columns). For all imported Diesel the Egyptian government has to pay the difference as subsidy. As international prices have come down so have the subsidies.

The reduction of fuel subsidies assumed by the IMF will bring the oil balance from -2.6% of GDP in 2013/14 to +1.3% over 5 years (IMF table 5). The oil balance is defined as (oil revenue minus fuel subsidies whereby oil revenue includes corporate income tax receipts from the Egyptian General Petroleum Corporation (EGPC) and foreign partners, royalties, extraordinary payments, excise taxes on petrol products, and dividends collected from EGPC.

Egypt Diesel prices in international comparison

Fig 8: Diesel prices

The German Agency for International Cooperation regularly monitors international fuel prices. It puts Egypt’s Diesel prices into Country Category 1 with high subsidies and the retail price of diesel below the price for crude oil on the world market.

https://www.giz.de/expertise/html/4317.html

https://www.giz.de/expertise/downloads/giz-2015-en-ifp2014.pdf

In July 2014, the Egyptian government increased fuel prices dramatically, from between 41% to 175%.

Fig 9: Egypt fuel price increases July 2014

Now the government isn’t taking any risks.

No petrol price increase in FY 2015/2016: Petroleum minister

8/3/2015

Petroleum Minister Sherif Ismail told Daily News Egypt the government will not raise domestic fuel prices in FY 2015/2016, as it is not suitable for the situation in Egypt.

http://www.dailynewsegypt.com/2015/03/08/no-petrol-price-increase-in-fy-20152016-petroleum-minister

Budget Sector Balance

Fig 10: Egypt’s budget deficit in % of GDP

Grants have come from Saudi Arabia and United Arab Emirates:

Fig 11: Financial assistance by GCC countries

Public debt

Fig 12: Egypt’s gross public debt

The debt in EGP has been calculated by multiplying the GDP ratios in table 6 with the nominal GDP. Public debt was growing at a whopping 20% pa between 2011 and 2014 while GDP grew at 14% pa, increasing debt to 90% of GDP.

In 2012/13 external debt rose by 26% as a result of financial assistance by Libya and Qatar. The UAE will provide loans in 2014/15, thereby increasing the external debt stock.

The IMF assumes that budgetary reform will bring debt growth rates down to 11% pa by the end of the decade while GDP should grow 2.8% faster than debt, resulting in a lower debt ratio of 80% of GDP. External debt will double in the next 4 years.

Financing needs

..

Fig 13: Egypt’s gross financing needs

The deficit is from Fig 3 (with budget reforms). We see that more than 80 % of the gross financing needs come from maturing debt (with an average of just 2 years).

For comparison, the following graph shows gross financing needs of other emerging market economies which are all much lower than Egypt’s.

Fig 14: Gross financing needs in emerging market economies

Data are from here:

April 2014 Fiscal Monitor “Public Expenditure Reform—Making Difficult Choices”

https://www.imf.org/external/pubs/ft/fm/2014/01/data/fmdata.xlsx

Current account

Fig 15: Egypt’s exports of goods and services vs imports and payments

The IMF did its tourism receipt projection under the assumption that there would be a rebound of 28% pa over 5 years. That was before the downing of the Russian Metrojet flight over Sinai on 31/10/2015 by a planted bomb. Whether tourism will ever recover is a big question.

Note in Fig 15 that exports of goods peaked in 2007/08 which caused current account deficits in the following years. Let’s have a look at the details:

Fig 16: Egypt export of goods

Egypt has a long-term structural trade deficit which worsened after 2007/08 when exports to the US peaked and started to decline. In that year the US went into recession due to high oil prices after crude oil production had started to peak in 2005. We see the footprint of this event everywhere. After the crisis year 2009, imports continued to increase while exports stagnated.

Data are from here: http://www.cbe.org.eg/english/economic+research/time+series/

External reserves

Fig 17: Egypt’s external reserves

Egypt’s external reserves halved after the Arab Spring early 2011. In 2014/15 they were the equivalent of 3.1 months of next year’s imports of goods and services, a minimum cash cushion. The latest update is shown in Fig 18.

EGYPT

Last Updated: December 9, 2015

International Reserves and Foreign Currency Liquidity

Fig 18: Composition of Egypt’s external reserves

https://www.imf.org/external/np/sta/ir/IRProcessWeb/data/egy/eng/curegy.htm

Update external financing needs

In September 2015 the IMF issued a preliminary up-beat assessment of the next Article IV consultation process.

- Completion of Suez Canal widening

- Major gas find in Egyptian waters

- Successful issuance of a $ 1.5 bn Eurobond

- GDP growth 4.2 % in 2014/15

- Decline of inflation

- Progress in energy subsidy reforms

- Containing wage bill

- Increasing tax revenue

https://www.imf.org/external/np/sec/pr/2015/pr15422.htm

However, the above statement does not reveal the true magnitude of the external financing needs which the IMF published just a month later in this report:

Arab Countries in Transition: Economic Outlook and Key Challenges

October 2015

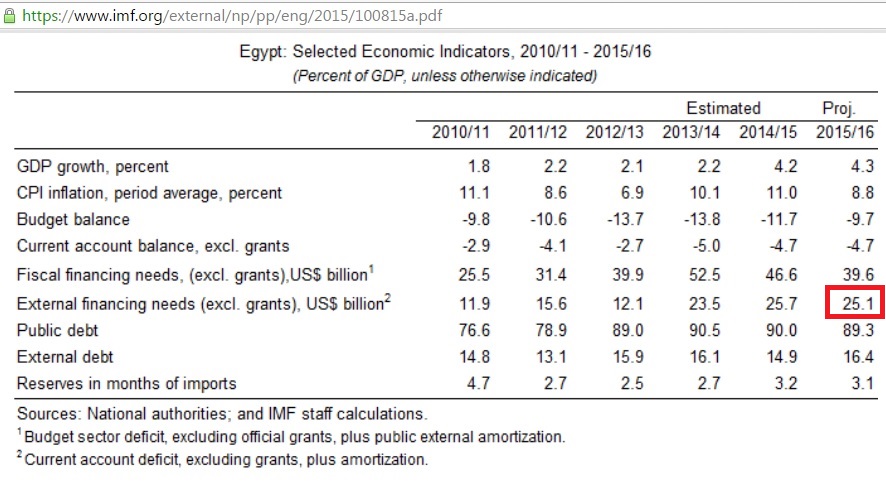

Fig 19: Egypt selected economic indicators

https://www.imf.org/external/np/pp/eng/2015/100815a.pdf

The external financing needs for 2015/16 are US$ 25.1 bn. Compare that to the Saudi aid pledge of US$8 bn over 5 years!

Population growth and distribution

Fig 20: Egypt population growth

Data: http://esa.un.org/unpd/wpp/DVD/

Conclusion:

Egypt faces many long-term fiscal and external accounting challenges which have been exacerbated by stagnating oil production. Fuel subsidies have accumulated over the years and contributed to an increase in debt which in turn results in a surge of interest payments. Net oil imports add to a structural current account deficit. Currently low oil prices are of an immediate advantage as both oil import bills and subsidies are lower. However, domestic oil production may drop if continuing low oil prices result in lower oil industry investments to offset decline in maturing fields. Financial assistance from GCC countries will be essential for the foreseeable future. But GCC countries are also under pressure from their own budget problems caused by low oil prices. So there will be a permanent struggle to keep Egypt financially alive, which is in the interest not only of GCC countries but the whole world as this country sits on an important strategic location. This is especially true as population continues to grow on a limited habitable area bounded by deserts and endangered by global warming.