This is a guest post by Matthieu Auzanneau, a freelance journalist in France, author of the Oil Man blog at Le Monde, where this post first appeared.

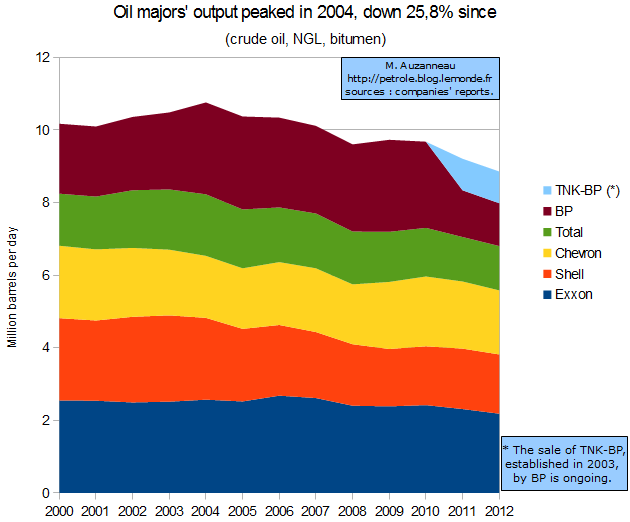

The combined crude oil production of the five main international oil companies (Exxon, BP, Shell, Chevron and Total) hit an historic high in 2004. Since then, it has fallen by 25.8%, despite large increases in investments.

Click to enlarge |

Total crude oil produced by the majors was 10.760 million barrels per day (MB/D) in 2004. In 2012, it reached only 7.981 MB/D. It has decreased by 2.779 MB/D in 8 years (-1/4), as I have been able to calculate from figures that appear in the twelve latest annual reports of those five companies.

Is this a clear early indication of an imminent decline in the worldwide production of black gold, a phenomenon predicted since 1998 by former oil company scientific executives, from the French Total group in particular?

The majors are all facing a decline in their crude oil production, which began in each case before 2007. This comes despite extremely large growth in their investments, allowed by the significant increase in crude oil prices experienced since the late 2000s. Total, for example, has seen its production fall by almost 20% since 2007, although the French giant now has at least 40% more extraction wells.

Since 2004, the total oil production by the majors has only increased once, between 2008 and 2009, and by just 0.13 MB/D, despite the unprecedented level of sales and purchases of oil assets experienced in recent years. So-called production sharing contracts, which allocate a larger share of production to the host country when the price per barrel rises, do not appear to explain the lowering of production by the majors, far from it. The production share of the five majors in worldwide production dropped from 13.39% in 2004 to 9.98% in 2011. It diminished further in 2012.

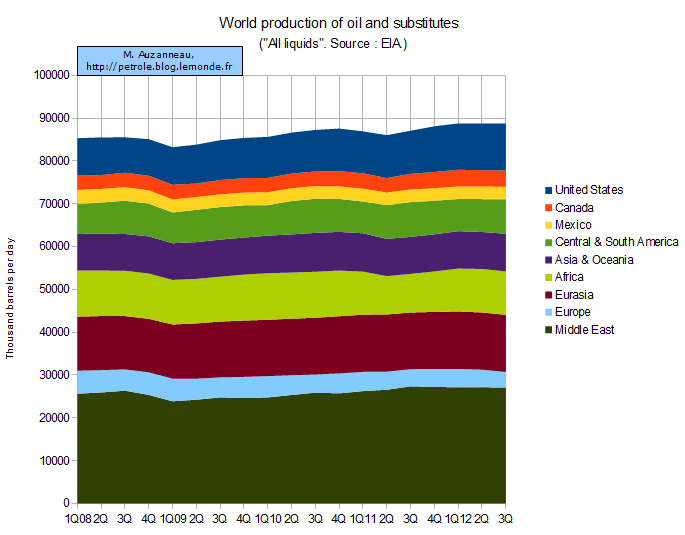

Worldwide crude oil production rose by 4% between 2004 and 2011. It has hardly increased at all since 2006, however: since then it has been on an undulating plateau, within a small margin of less than 1.25%.

The significant decline in extractions by the majors has been compensated for by the OPEC countries (+ 2.189 MB/D), primarily Iraq and Saudi Arabia, and also by the countries of the former Soviet Union (+ 2.131 MB/D). In the rest of the world, where the majors often occupy the key positions, oil production (excluding agrofuels) has fallen by 1.104 MB/D, once again between 2004 and 2011.

In 2012, worldwide production appears to have increased significantly, firstly thanks to the boom in shale oil in the United States; full detailed information is not yet available (to follow).

Click to enlarge |

The case of BP

Since 2011, the decline in the total production of the majors has been significantly amplified by the sale to the Russian national company Rosneft of parts of the BP group with TNK-BP, an important joint venture established in Russia in 2003. The sale of TNK-BP alone has eliminated around 40% of BP’s previous production. This production reached its record level in 2005. If this sale had not taken place, total production by the five majors would have still declined by 17.7% in 8 years, reaching 8.86 MB/D in 2012. And BP’s production would still have been in sharp decline.

Since 2011, BP has had to sell other major production assets in order to settle the account for the oil spill in the Gulf of Mexico in 2010. In this case, as in that of TNK-BP, it is the need to go in search of intact sources of oil in increasingly extreme conditions that has hindered BP’s development: the drill site responsible for the catastrophe in the Gulf of Mexico holds a drilling depth record; the conflict between the TNK-BP shareholders at the root of the sale of parts of BP was about the opportunity of a huge drilling campaign in the Arctic Ocean, where the oil majors, notably BP, have recently met with a number of failures.

The "seven sisters" have aged

Exxon, Shell, Chevron, BP and Total are still forces to be reckoned within the oil industry, as much for their still considerable outputs, for their investment capacities and technical expertise, as for their strategic role as the preferred providers of consumers in the old Western industrial powers. These Western majors, starting with the most powerful, Exxon, remain, now more than ever, at the top of the ranks of the largest private companies on the planet.

The majors came into existence between the late 19th century and the early 20th century. Long dubbed the "seven sisters", they are now only five in number as a result of the mega-mergers that have taken place over the last two decades.

Until the 1960s, the Anglo-Saxon majors, as well as the forerunners of the French company Total, largely dominated worldwide production. The OPEC cartel of oil producing countries was created in 1960 to stand up to the restricted and secretive cartel of the "seven sisters", which reigned supreme outside the United States for half a century.

Throughout the 1960s, and especially in the 1970s, as the OPEC member countries nationalised their oil fields in the wake of Algeria, Libya and Iraq, the control wielded over production by the Western majors was reduced.

The response at the end of the 1970s broadly stabilised the balance of the market share, thanks in particular to the launch of the North Sea and Alaska, two extraction areas that have been in significant decline for more than a decade because of the exhaustion of their crude oil reserves.

OPEC is now content with a little over 40% of worldwide production. But it controls more than 70% of the planet’s proven reserves.

Consequently, as the known oil fields are getting depleted, production should become more and more concentrated in the major OPEC countries, starting (or finishing) with Saudi Arabia, as well as, to a lesser extent, in the former Soviet Union.

It seems unlikely for the moment that the development of non-conventional and extreme sources of oil, in particular shale hydrocarbons, will be able to change that fact. We will come back to this again.

For this translation, a very big thank to Laura Bennett: culturetranslation.com