Does Thursday’s announcement that the EU is considering to ban oil imports from Iran epitomise the draining of power from west to east? The big winners here will be China and India, who do not fear rising Iranian influence and who will gladly soak up any additional oil exports they may have to offer. However, ending this small dependency upon Iranian oil imports in Europe (Figure 2) does clear the way for military action without the need to ponder the immediate consequences on oil imports.

Figure 1 Iran displays export land traits where growing domestic consumption is eating into the oil available for export that has been declining slowly since 2003. Data from BP. Y-axis is barrels per day (1000s). Balance = production less consumption which is a proxy for net exports. Production = crude+condensate+NGL whilst consumption may include refinery “gains” and bio-fuel. In many countries there is also an active two-way trade in crude and refined products.

In a week where the UK embassy in Iran was overrun and the two countries are breaking off diplomatic ties, on the back of heightened concern about Iran’s nuclear weapons program and an unexplained explosion at an Iranian missile launching site, the EU has decided to flex its muscles and to ban Iranian oil imports. The big winners here are the other countries importing oil from Iran – Japan, China, India and South Korea. Does the EU really believe that in today’s extremely tight oil market that oil sanctions against Iran will worry them in the least?

Figure 2 Table from a worthy article on Iranian oil and demographics posted on Crude Oil Peak details the countries importing oil from Iran in 2008. The four EU countries to be affected by any embargo will be Italy, Spain, Greece and France. Given that Greece and Spain are already in recession and that Italy and France are heading in that direction, it seems likely that their oil consumption will already be on the wane and that losing these relatively small amounts of Iranian imports will have little consequence.

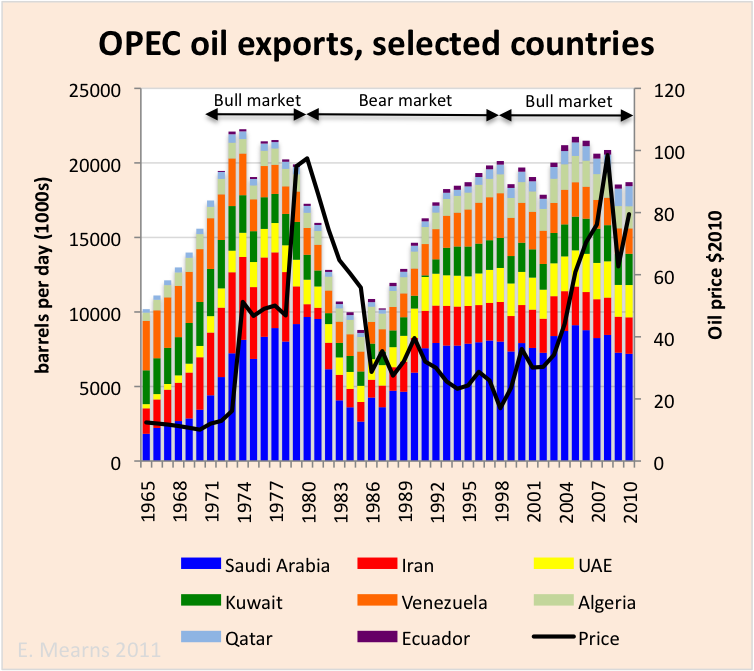

Figure 3 OPEC net exports (production consumption balance from BP) showing the importance of The Gulf states.

With the risks of armed conflict against Iran increasing with every week that passes it is important to grasp what this may mean for global oil markets. Two end points seem to exist. The first is where “the West”, i.e. NATO or some other looser alliance ± Israel launches a cruise missile attack (conventional) against Iran’s nuclear facilities. destroying them. In that eventuality Iran, with current leadership, would be unlikely to ever again export oil to “the West”, but since at that point The West will not be importing any oil from Iran this would not matter.

Figure 4 Iranian oil infrastructure, setting in the Arabian or Persian Gulf and the linch pin location of The Straights of Hormuz. Map from Wikipedia.

The second more extreme scenario is that armed conflict spreads, compromising oil exports through the Straights of Hormuz. Oil exports from Saudi Arabia, Kuwait, The United Arab Emirates (UAE), Qatar, Iraq and Iran all pass through Hormuz. Data is not available for Iraq, but exports from Saudi, Kuwait, UAE and Qatar stood at around 12,805,000 bpd in 2010. The global net export market stood at around 35,173,000 and so these 4 countries alone account for around 36.4% of the global export market (excluding Iraq and Iran). Should these exports cease, albeit temporarily, the oil price will go through the roof, causing severe trauma to the global economy, including China.

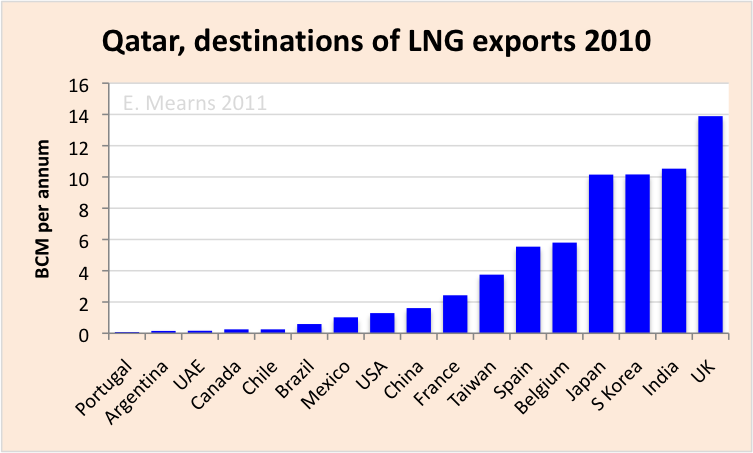

In addition, there are significant liquefied natural gas exports from Qatar that pass through Hormuz on a daily basis. According to BP, Qatar exported around 96 BCM of gas in 2010 (Figure 5) to the countries shown in Figure 6. In Europe, the UK, Spain, and Belgium would be most affected by disruption to LNG supplies from the Gulf whilst in Asia, India, S Korea, and Japan would be most affected. This highlights the increasingly exposed nature of OECD energy supplies where electricity supplies may be threatened by armed conflicts on the other side of the world.

Figure 5 Production / consumption balance for natural gas in Qatar.

Figure 6 Destinations of LNG exports from Qatar in 2010.

Euan Mearns has B.Sc. and Ph.D. degrees in geology from The University of Aberdeen. He worked as a researcher at The University of Oslo and then The Norwegian Institute for Energy Technology for a total of 8 years. In 1991 he set up a company in Aberdeen, Scotland providing isotope analyses to the international oil industry. His company worked for over 60 exploration and production companies world wide but eventually ran out of reservoirs to characterise and the company was sold in 2001. Since 2009, Euan has been an Honorary Research Fellow at the University of Aberdeen. His main interests lie in understanding energy systems, forecasting, and energy policy.

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

{kind=link}