hIt is easy to become befuddled by the current discourse on peak oil. Peak oil is defined generally as the point at which the flow rate of oil to society has reached a maximum. But this simple definition has issues too, such as what should be considered “oil.” Take, for example, the following sentences from the executive summary of the International Energy Agency’s recent publication of the World Energy Outlook (WEO) 2010[1]:

…[In 2035] Global oil production reaches 96 mb/d, the balance of 3 mb/d coming from processing gains. Crude oil output reaches an undulating plateau of around 68-69 mb/d by 2020, but never regains its all-time peak of 70 mb/d reached in 2006, while production of natural gas liquids (NGLs) and unconventional oil grows strongly.

According to this data, a peak in the production of conventional crude oil occurred in 2006, but a peak in total “oil” production (including unconventional resources such as tar sands, natural gas liquids, etc.) may not occur for some time. So, should we consider this a confirmation of peak oil or not?

Radetzki, the author of a recent paper condemning the prophets of peak oil as “chimeras without substance,” would argue no.[2] He asked in his paper: “…but are there any technical or economic reasons to distinguish between conventional and non-conventional resources in an analysis of what is ultimately recoverable?” Radetzki notes in his article that the production of conventional crude may begin to decline soon but total oil production could increase (given proper economic investments, etc.) as unconventional resources are brought on-line, and the WEO seems to confirm this.

Radetzki’s argument is based on the conventional economic idea of resource depletion, put forth by numerous authors but maybe most famously by Barnett and Morse in 1963.[3] They wrote: “as resources become scarce and relative costs change, substitutions will occur to ameliorate effects of diminishing returns.” With respect to oil, this statement is understood to mean that technology will offset depletion by either helping to discover new resources, by bringing other known resources into production that were previously too expensive, or by developing a suitable substitute.

And indeed the evolution of oil production seems to verify these sentiments, as technology now exists to exploit oil from tar sand resources or to convert coal and gas to various oil derivatives. Considering that all of these resources can produce oil, and that there are decades (according to the WEO) of these resources remaining, does peak conventional oil even matter?

In short, yes.

Peak oil is important because it marks the peak of production of “cheap” oil, generally considered to be conventional crude oil. Do not be confused; transitioning from conventional crude oil to NGLs or oil derived from other unconventional resources should be thought of as an indication of peak oil, not the opposite—that technology has enabled the production of oil from NGLs and other unconventional resources, thus disproving peak oil theory.

If we are to consider NGLs and other unconventional resources of oil as substitutes for oil, than we should also consider conventional oil a substitute for whale oil. After all, whale oil and the oil sands are both chemically similar to crude oil, and crude oil production offset the decline in whale oil production due to depletion of whales just like NGLs and unconventional oil may offset the decline in crude oil production due to the depletion of conventional crude. Thus, by this transitive property of economics, we are really still waiting for a peak in whale oil production!

The economists’ argument—that resource constraints will be abated by technology and substitution—confuses substitution for increasing supply. The usual way that substitution occurs in a market is that the substitute has some sort of competitive advantage (i.e. better product, cheaper, etc.) compared to the item that it is replacing; think supplanting human labor with robots in the construction of cars, or replacing vacuum tubes with integrated circuits. It is difficult to think if there are any advantages in producing oil from oil sands in northern Alberta when compared to production of oil from either East Texas or Ghawar. For example, the cost of production in Saudi Arabia is roughly $20 per barrel while it is over $80 per barrel in the tar sands (Figure 1). But prices are set at the margin for oil (at least in theory), so that if demand for oil increases enough, the price may increase to a point at which unconventional oil production becomes profitable. If this occurs, then oil will be produced from unconventional resources because they are profitable too, not because they are a “substitute,” in the economic sense, for conventional oil.

Figure 1. Estimates of the cost of production for oil production form various locations. Data from Cera.[4]

Arguing that unconventional oil will be a good substitute for the depletion of conventional crude is like saying that human labor will serve as a good substitute for robotics, or that a depletion of MacBooks will be offset by an increase in UNIVAC production.” Though these are both technically feasible, they do not provide any competitive advantage, ceteris paribus. The point is that oil production from the tar sands and other unconventional resources occurred in response to increasing demand which in turn elevated prices, not because they offer some competitive advantage when compared to conventional crude oil.

What does this mean?

It means that to grow the economy for the next few decades on an oil energy base would require very high prices. But if the recessions of 1973, 1980, and 2008 have taught us anything, it is that high energy prices cause problems for the economy. Noting the inevitable transition to unconventional resources, the IEA reports that: “the average IEA crude oil price reaches $113 per barrel (in year-2009 dollars) in 2035 — up from just over $60 in 2009. In practice, short-term price volatility is likely to remain high.” Other data from the BP statistical review support this upward trajectory in prices: the average price of a barrel of oil from 1861-1969 was $23, $40 from 1970 – 1999, and $53 from 2000 – 2008 (all in real 2008 dollars).[5]

Clearly demand destruction (and a financial crisis) has the ability to lower oil prices, as prices plummeted from 140 to 30 dollars per barrel during the fall of 2008 and winter of 2009. But now, two years later, oil price is again back in the range of $90 per barrel. In a society like ours, where economic growth is touted as the solution to almost every societal problem (see more or less any op-ed on how to fund the U.S. deficit), peak oil presents a paradox: the growth of the economy requires an increasing oil supply, but increasing the oil supply, due mainly to a peak in conventional crude oil production, will require high prices which tend to undermine that growth. The billion dollar question is: at what price of oil does the economy stop growing?

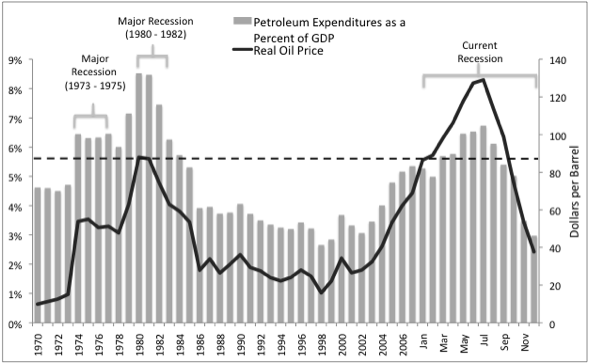

Over the past 40 years, when petroleum expenditures as a percent of GDP increased much beyond 5.5%, the economy tended towards recessions (Figure 2). This tendency is due mainly to the fact that oil infiltrates almost every facet of an industrial economy, from personal disposable income, to manufacturing, to service sectors. Therefore higher oil prices restrain growth via declining discretionary consumption as individuals allocate more money towards gasoline and home heating, or as the cost of producing a good increases, etc.[6] Chris Nelder of getREALlist has described this situation succinctly, writing: “The true import of peak oil, therefore, may not be sustained high prices, but economic shrinkage. Demand will be destroyed long before oil gets to $200 a barrel…”

Figure 2. Petroleum expenditures as a percent of GDP. Figure created by Steve Balogh and published here.

In sum, although it is technically feasible to increase the production of “oil,” peak conventional oil, as it was first envisioned by Hubbert in 1956, has manifested itself almost exactly as predicted.[7] As Campbell described, peak oil will bring about short bouts of economic growth and contraction as oil demand and prices play tug-of-war, creating what has been referred to as an undulating plateau.[8] We seem to be experiencing these economic conditions right now. So the question is no longer “when will peak oil occur,” but “how long will the effects of peak oil last?”

References

1. IEA. 2010. World Energy Outlook 2010. International Energy Agency.

2. Radetzki, M. 2010. Peak Oil and other threatening peaks – Chimeras without substance. Energy Policy, 38:6566-6569.

3. Barnett, H. and C. Morse. 1963. Scarcity and Growth: The Economics of Natural Resource Availability. Johns Hopkins University Press.

4. CERA. 2008. Ratcheting Down: Oil and the Global Credit Crisis. Cambridge Energy Research Associates.

5. Hayward, T. 2010. BP Statistical Review of World Energy. British Petroleum.

6. Hall, C. A. S., R. Powers and W. Schoenberg. 2008. Peak Oil, EROI, Investments and the Economy in an Uncertain Future. In Biofuels, Solar and Wind as Renewable Energy Systems: Benefits and Risks. Pimentel, Ed. Netherlands, Springer Netherlands.

7. Hubbert, M. K. 1956. Nuclear Energy and the Fossil Fuels. Spring Meeting of the Southern District Division of Production, San Antonio, Texas. 1956.

8. Campbell, C. 2009. Why dawn may be breaking for the second half of the age of oil. First Break, 27:53-62.

{kind=link}