The International Energy Agency issued its annual energy forecast today for 2010. It consists of a three volume report, plus an executive summary and a press release. The website can be found here.

In the next few weeks, we will be analyzing the report. At this point, we can only point to a few of the summary findings. One clear concern is that demand will be rising–especially from China and India. Another is that prices (in inflation-adjusted terms) will be rising. A third concern is that conventional oil production will no longer be able to rise.

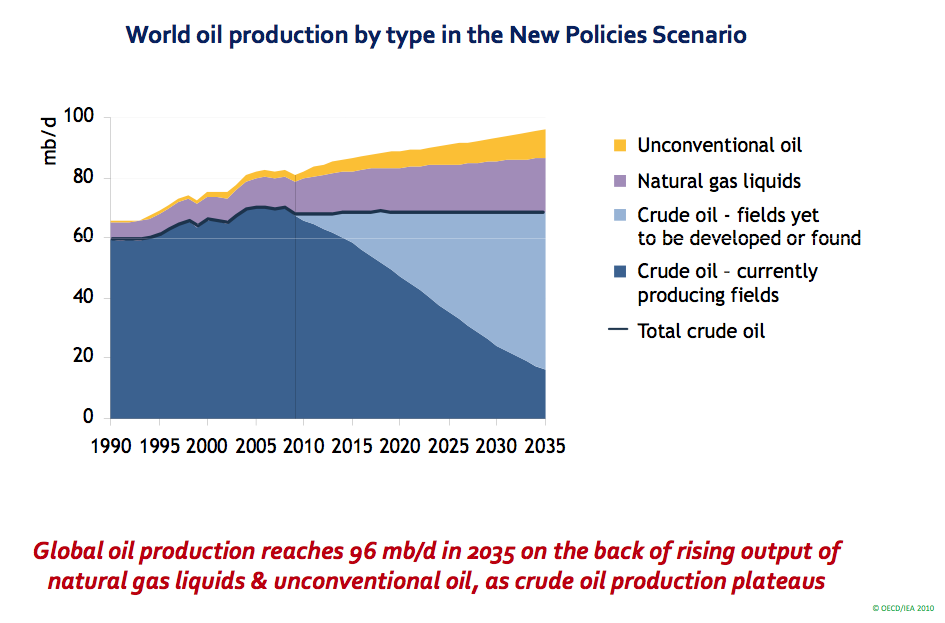

The above scenario shows conventional crude oil on a plateau to 2035 at a level below recent production. This graph is from the “New Policies” scenario, so reflects some cutback in demand as a result of governmental policies from what the reference scenario would assume.

With respect to rising prices, the press packet shows this slide, indicating that “real” prices are set to rise, unless there is a very major cutback in demand as would be required under the “450 Scenario” (referring to the CO2 limit aimed for):

The Executive Summary says:

The oil price needed to balance oil markets is set to rise, reflecting the growing insensitivity of both demand and supply to price. The growing concentration of oil use in transport and a shift of demand towards subsidised markets are limiting the scope for higher prices to choke off demand through switching to alternative fuels. And constraints on investment mean that higher prices lead to only modest increases in production. In the New Policies Scenario, the average IEA crude oil price reaches $113 per barrel (in year‐2009 dollars) in 2035 — up from just over $60 in 2009. In practice, short‐term price volatility is likely to remain high.

Oil demand (excluding biofuels) continues to grow steadily, reaching about 99 million barrels per day (mb/d) by 2035 — 15 mb/d higher than in 2009. All of the net growth comes from non‐OECD countries, almost half from China alone, mainly driven by rising use of transport fuels; demand in the OECD falls by over 6 mb/d. Global oil production reaches 96 mb/d, the balance of 3 mb/d coming from processing gains. Crude oil output reaches an undulating plateau of around 68‐69 mb/d by 2020, but never regains its all‐time peak of 70 mb/d reached in 2006, while production of natural gas liquids (NGLs) and unconventional oil grows strongly.

The plan in all of this is for OPEC oil production to rise.

The executive summary says:

Total OPEC production rises continually through to 2035 in the New Policies Scenario, boosting its share of global output to over one‐half. Iraq accounts for a large share of the increase in OPEC output, commensurate with its large resource base, its crude oil output catching up with Iran’s by around 2015 and its total output reaching 7 mb/d by 2035. Saudi Arabia regains from Russia its place as the world’s biggest oil producer, its output rising from 9.6 mb/d in 2009 to 14.6 mb/d in 2035. The increasing share of OPEC contributes to the growing dominance of national oil companies: as a group, they account for all of the increase in global production between 2009 and 2035. Total non‐OPEC oil production is broadly constant to around 2025, as rising production of NGLs and unconventional oil offsets a fall in that of crude oil; thereafter, total non‐OPEC output starts to drop. The size of ultimately recoverable resources of both conventional and unconventional oil is a major source of uncertainty for the long‐term outlook for world oil production.

The executive summary does not want to go as far as saying that oil supply will peak in the near future, unless policies are implemented to reduce demand significantly. The summary says:

Clearly, global oil production will peak one day, but that peak will be determined by factors affecting both demand and supply. In the New Policies Scenario, production in total does not peak before 2035, though it comes close to doing so. By contrast, production does peak, at 86 mb/d, just before 2020 in the 450 Scenario, as a result of weaker demand, falling briskly thereafter. Oil prices are much lower as a result. The message is clear: if governments act more vigorously than currently planned to encourage more efficient use of oil and the development of alternatives, then demand for oil might begin to ease soon and, as a result, we might see a fairly early peak in oil production. That peak would not be caused by resource constraints. But if governments do nothing or little more than at present, then demand will continue to increase, supply costs will rise, the economic burden of oil use will grow, vulnerability to supply disruptions will increase and the global environment will suffer serious damage.

The IEA seems to see a possible new role for natural gas:

The executive summary says this about natural gas:

Natural gas is certainly set to play a central role in meeting the world’s energy needs for at least the next two‐and‐a‐half decades. Global natural gas demand, which fell in 2009 with the economic downturn, is set to resume its long‐term upward trajectory from 2010. It is the only fossil fuel for which demand is higher in 2035 than in 2008 in all scenarios, though it grows at markedly different rates.

It has quite a bit more to say about natural gas than I have quoted here, especially about Chinese demand growing in the future.

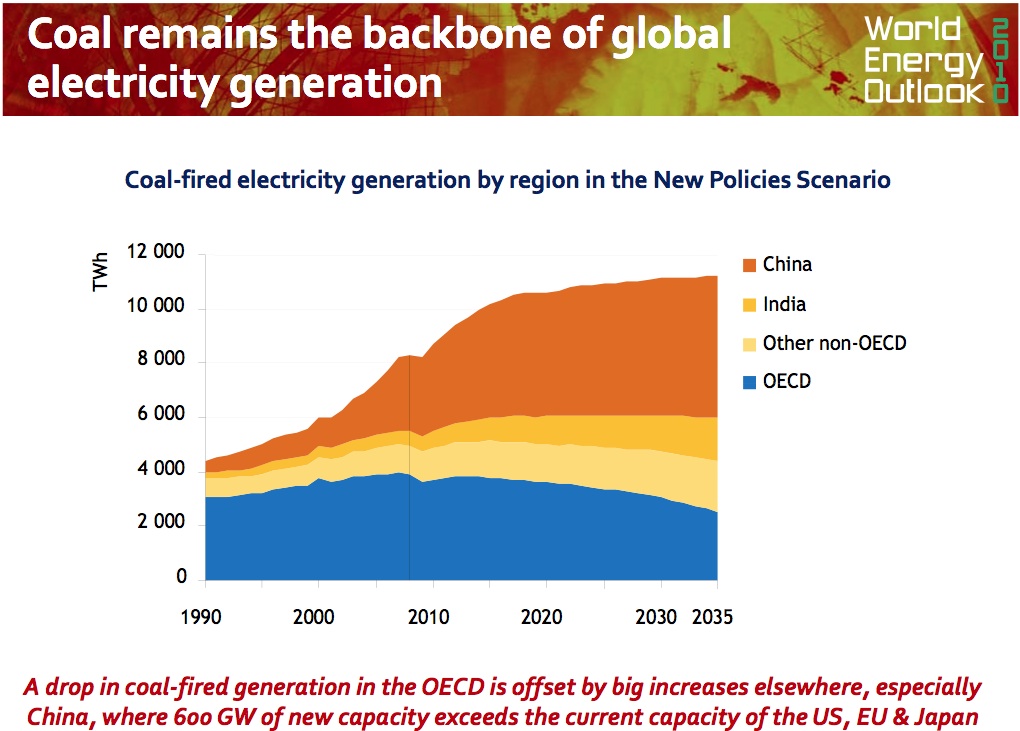

Coal use for electricity is seen as growing outside OECD:

The summary slide of the press packet shows these findings:

We will be examining the report in more detail in the near future, but we wanted to give you the “flavor” of what it is saying today.