The following is a brief portion of a paper of the same title that we (Charles Hall and I) wrote and that is currently under peer-review. I will be presenting on this topic at this year’s ASPO conference in Washington, D.C. I hope that our readers will attend!

Numerous theories attempting to explain business cycles have been posited over the past century, each offering a unique explanation for the causes of–and solutions to–recessions, including: Keynesian Theory, the Monetarist Model, the Rational Expectations Model, Real Business Cycle Models, New (Neo-) Keynesian models, etc…

Yet, for all the differences amongst these theories, they all share one implicit assumption: a return to a growing economy, i.e. growing GDP, is in fact possible. Historically, there has been no reason to question this assumption as GDP, incomes, and most other measures of economic growth have in fact grown steadily over the past century. (Note: economic growth and “business as usual” economic growth are used synonymousy to mean an annual growth in GDP)

But if you believe as I do that the world is entering a unique period defined by flattening and then declining oil supplies, then for the first time in history we may be asked to grow the economy while simultaneously decreasing oil consumption, something that has yet to occur in the U.S. In this post I attempt to answer the following question: Is a return to long term economic growth possible?

Economic growth over the past 200 years has correlated highly with energy consumption (Figure 1). Even more telling, since 1970, 50% of the year on year change in GDP in the U.S. is explained by the year on year change in oil consumption alone (Figure 2). This is important because oil consumption per se is rarely used by neoclassical economists as a means of explaining economic growth. For example, Knoop (2010) described the 1973 recession in terms of high oil prices, high unemployment and inflation, yet omitted mentioning that oil consumption declined four percent during the first year and two percent during the second year. Later in the same description, Knoop claimed that the emergence from this recession in 1975 was due to a decrease in both the price of oil and inflation, and an increase in money supply. To be sure, those factors contributed to the recession and the emergence from the recession, but what was omitted, again, was the simple fact that higher oil prices led to less oil consumption and lower economic output during 1973 and lower oil prices led to increased oil consumption and hence greater economic output in 1975.

Figure 1. Energy production and GDP for the world from 1830 to 2000.

Figure 2. Correlation of YoY changes in oil consumption with YoY changes in real GDP, for the U.S. from 1970 through 2008. (Oil consumption data from the BP Statistical Review of 2009 and real GDP data from the St. Louis Federal Reserve.)

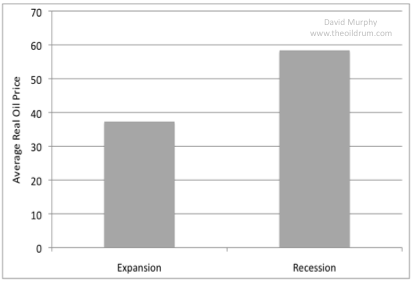

As this example indicates, it is not just simply having access to energy per se that causes economic growth, rather the energy must be accessible cheaply. For example, the inflation-adjusted price of oil averaged across all expansionary years from 1970 to 2008 was $37 per barrel compared to $58 per barrel averaged across recessionary years (Figures 3).

Figure 3. Real oil prices averaged over expansionary and recessionary periods from 1970 through 2008.

To summarize: economic growth requires not only energy per se, but inexpensive energy.

With that point in mind, we can address the previous question about whether or not a future of long term economic growth is possible by answering two sub-questions: 1) do we have the physical resources to supply a growing economy, and 2) can we reach those supply targets while maintaining a low price? Since long term economic growth requires an increasing supply of cheap energy, answering no to either of these sub-questions would indicate that long term economic growth is unlikely.

First, economic growth requires increasing oil supplies, so increasing GDP by 4 or 5 percent per annum will require a commensurate increase in oil supplies. Although most of the readers on this website are aware of Peak Oil, some argue that it is a red herring. I will not go into the numerous arguments rebutting the naysayers other than saying the following: what matters in the context of business as usual economic growth is whether we can continue increasing our oil supply into the future or whether oil supplies will be constrained. In this context, the actual date of the peak is irrelevant. Even a cursory examination would reveal that, at a minimum, oil supplies will be constrained in the future.

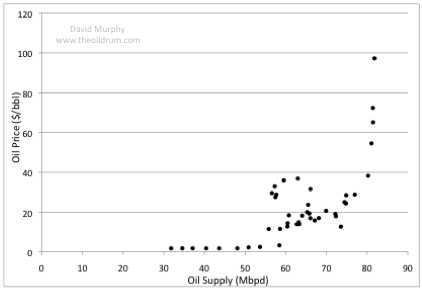

Second, increasing the supply of oil will require maintaining current production and discovering new sources of oil. This includes maintaining production in oil sands, exploring ultra deep water, and exploring even the poles. Let’s say, for argument sake, that we are able to find oodles of oil in these locations. The question then becomes: can we produce this oil cheaply? We can get a glimpse at how production costs change over time by relating the EROI of production to the financial cost of production (Figure 4). As resource quality declines, i.e. lower EROI, the cost of producing the resource increases. Alternatively, if we examine a supply graph for global oil production we can see an interesting relation between quantity and price (Figure 5). Both of these figures indicate that increasing oil production much beyond today’s level will create an exponential increase in price. In sum, increasing the oil supply, if in fact we can do such a thing, can occur only at high oil prices.

Figure 4. Oil production costs from various sources as a function of the EROI of those sources. The dotted lines represent the real oil price averaged over both recessions and expansions during the period from 1970 through 2008.

Figure 5. Real oil prices plotted as a function of global oil supply from 1970 through 2008.

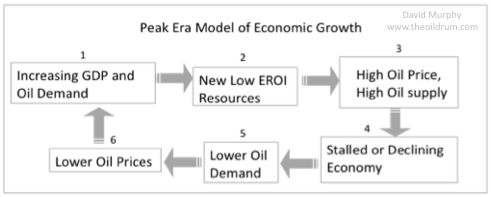

Due to the depletion of high EROI oil (and hence cheap oil), the current economic situation can be described by the following feedbacks (Figure 6): 1) economic growth increases oil demand, 2) higher oil demand increases oil production from lower EROI resources, 3) increasing extraction costs leads to higher oil prices, 4) higher oil prices stall economic growth or cause economic contractions, 5) economic contraction leads to lower oil demand, 6) lower oil demand leads to lower oil prices which spur another short bout of economic growth until this cycle repeats itself.

Figure 6. Peak era model of the economy.

This system of insidious feedbacks is aptly described as a growth paradox: maintaining business as usual economic growth will require the production of new sources of oil, yet the only sources of oil remaining require high oil prices, thus hampering economic growth.

The growth paradox leads to a highly volatile economy that oscillates frequently between expansion and contraction periods, and as a result, there may appear to be numerous peaks in oil production (a so-called “undulating plateau”). In terms of business cycles, the main difference between economic models of the past and the this model is that in the past business cycles appeared as oscillations around an increasing trend whereas in this model they appear as oscillations around a flat trend. In other words, our baseline economic models may be switching from an implicit 1 or 2 percent growth to a steady-state, or dare I say, declining trend.

So arguments that cite vast oil reserves 10,000 leagues under the sea or in the poles as evidence that peak oil will not matter need to realize that in terms of economic growth, oil per se isn’t enough. Cheap oil is needed for economic growth, and we are simply running out of the good, cheap crude.