The issues we are confronted with today seem to be a subset of the issues foretold in the book Limits to Growth back in 1972. At some point, the economy cannot continue to grow as rapidly as it did in the past. It appears to me that the most immediate limit we are hitting today is inadequate low-priced oil, but there are other limits lurking not far away–inadequate fresh water and excessive pollution, for example. When the economy cannot grow as fast, or actually starts declining, recession sets in. Governments start having debt problems. Financial markets start behaving strangely.

This issue is a difficult one to talk about, because there really is no good solution. I have talked to a couple of groups recently (one a church group; one a peak oil group), about this issue. This is a copy of the presentation I used (Bumping up against the Growth Ceiling (PDF) or Bumping up against the Growth Ceiling (PowerPoint)). In this post, I will discuss my presentation.

Slide 1

Slide 2

The world is finite. We know that, logically, the amount of any resource extracted from the world’s crust cannot continue to increase year-after-year, forever. But most of us have never thought about the idea that economic growth might eventually stop because of limits we hit.

Slide 3

It seems to me that the financial problems we are reaching today reflect a fundamental mismatch. We have a financial system that requires growth. At the same time, world oil supply has stopped rising enough to keep oil prices down. This mismatch threatens to put a cap on economic growth, especially for large users of oil such as the United States and many European countries.

Slide 4

Let me start by describing why our economy needs economic growth.

Slide 5. Image by Tony Wrigley http://www.voxeu.org/index.php?q=node/6781

Europe has used coal for about 450 years, according to Tony Wrigley. The use of coal helped reduce the amount of firewood needed (cream-colored area), and thus helped prevent deforestation. The use of coal also led to economic growth, because its energy could be put to many uses. According to Wrigley’s analysis, wind and water never produced a large share of the total energy supply.

In recent years, oil and natural gas have been added to the energy mix. All of these fossil fuels have helped increase the amount of food produced and the quantity of manufacturing done, and thus, economic growth.

The fact that we have had fossil fuel driven economic growth for such a long time–at least 450 years–has helped create the belief that economic growth is the natural state of affairs. It is easy to believe that it will always continue.

Figure 6.

Our financial system today depends on the use of debt, and the repayment of that debt with interest. We don’t usually think of it, but in a growing economy, it is much easier to repay debt with interest than in a declining economy, because, on average, things are getting better over time. This is easiest to see for an organization like the government that funds its borrowing with taxes. These taxes tend to rise when the economy is growing, making it easier to repay debt and the interest on that debt.

The same principle works for other individuals and businesses. If an economy is growing, a person is more likely to be able to keep his job, to get a new job if he is laid off, and to get promotions, so it is easier to repay loans and the interest on those loans.

Slide 7

Of course, the reverse is true in a shrinking economy, or even a level economy. The loan plus interest leaves the borrower with less money left over for other things, so is more difficult to repay.

Slide 8

Reinhart and Rogoff wrote a well-known academic paper, and made the observation quoted in Slide 8, apparently not understanding why this relationship existed. It seems to illustrate the relationship that a person would expect, based on Slides 6 and 7.

Figure 9

Economic growth provides many types of benefits. If the economy is growing, people have jobs, and many are getting raises. People can afford to buy bigger homes, so home prices tend to rise. The stock market tends to rise, because companies are making increasingly large amounts of money, and people believe that they will continue to make more money in the future. The number of people employed tends to rise, because of rising demand for goods and services.

Governments find that taxes rise, even without raising tax rates, because citizens are prospering. Charitable organizations, like churches, see rising contributions.

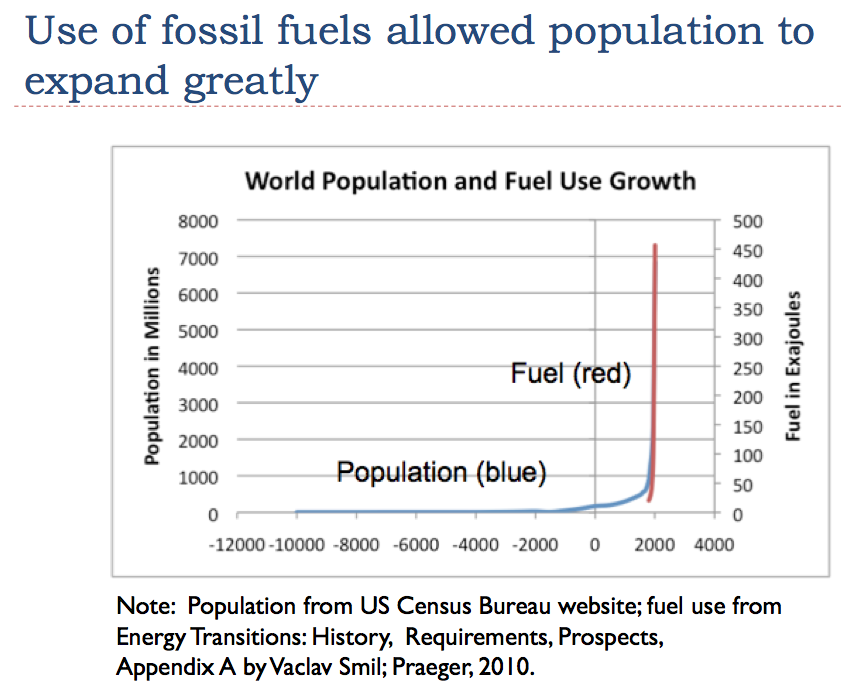

Slide 10

With the use of fossil fuels, it was possible to greatly increase food production. Population grew in the same time period that fuel use grew. World population is now about 7 billion, compared to about 450 million in 1500 . Thus, population is now more than 10 times as high as it was in 1500.

Slide 11

In this slide, I show a few of uses of oil. Oil is especially important for growing and transporting food. Thus, its use helps explain the recent population rise.

Slide 12

Thee unfavorable outcomes shown on slide 12 are just the reverse of the favorable outcomes mentioned earlier, when there was adequate economic growth. We recognize them as problems we have seen during recent recession.

Slide 13

Next I would like to talk about how limited oil supply is constricting economic growth.

Slide 14

On this slide, I divide world oil production into two parts–oil produced by the Organization of Petroleum Exporting Countries (OPEC) and oil produced by Non-OPEC countries. OPEC countries claim to have plenty of spare capacity, but it is hard to see that such capacity actually exists from their actions. Neither OPEC or Non-OPEC production has increased very much since 2005, even when prices spiked very high in 2008. OPEC cut back production somewhat when oil prices dropped, but that is more or less expected, because at a low price, some extraction may no longer be profitable.

Readers should be aware that statements made by OPEC countries are not audited. When US oil companies were involved in the Middle East prior to 1980, oil reserves were much lower than today. After state-owned oil companies took over, there was competition to raise reported reserves. Some of these increases may be simple exaggerations; others may be correct, if a person includes oil that can be produced at a dribble a year, over many, many years. But we are likely kidding ourselves if we think the high reserves indicate spare capacity, or likely higher production in the future.

Also, statements about OPEC raising oil production aren’t necessarily very truthful. If they do raise production, it may only be to cover rising internal consumption, with virtually no impact on exports.

Slide 15

We often read that there is a huge amount of oil available, in the oil sands in Canada or in the oil shale in Colorado, for example. The problem is that not all oil is equivalent. Some oil is a liquid, and is easy to extract. Other oil is not a liquid, or is in very inconvenient locations. Our problem is that a lot of the easy-to-extract, cheap-to-extract oil from the top of the triangle was extracted first, and is now gone. What is left is mostly oil that is much harder to extract. As an example, some oil is very “heavy” and oil companies may need to use steam to heat the oil, and then collect the dribbles of melted oil.

Slide 16

To elaborate a bit further on why we can’t get the oil out, one problem is that quite a bit of the cheap oil has been extracted, and expensive oil (which we have plenty of) seems to cause recession. Economist James Hamilton has shown that 10 out of 11 of the most recent recessions occurred in conjunction with oil price spikes. (We will talk a more later about why high oil prices tend to cause recession.)

In order to justify extracting the very expensive-to-extract oil, companies need very high prices for a long time, so that they have reasonable confidence that prices will be sufficiently high when the oil is extracted and ready to sell. But oil prices don’t seem to stay high long enough–high oil prices seem to lead to recession, and recession brings them back down again.

I might mention, too, that there is a theoretical upper bound for prices. Just as you wouldn’t use more than one barrel of oil to extract a barrel of oil, at some point, the resources that go into extracting the oil become too high, relative to the benefit to be obtained from using that oil. If this happens, there is no point in extracting the oil–it makes more sense to leave it in the ground. For some of the oil resources, we may be approaching the too-expensive-to-extract limit.

Slide 17

The fact that world oil production is more or less on a plateau is not entirely unexpected. In many countries, oil production has risen, reached a peak or plateau, and then begun declining. If the world is the sum of production of individual countries, the world might also eventually get to a peak or plateau.

For the United States – 48 states (blue on Slide 17), oil production suddenly started declining in 1971, after hitting a peak in 1970. When we realized that there was a problem, we quickly got to work on extracting oil from other areas. We ramped up production in Alaska in the late 1970s (red “layer” on the map), and added a pipeline so that the oil could be transported better. The amount of oil obtained from Alaska has now dropped to less than half of its peak amount.

Eventually, we started drilling in the area designated as “Federal offshore,” mostly in the Gulf of Mexico (light green layer on graph). The oil from the Federal Offshore area is still increasing, but no one expects that it will bring us back up to the 1970 level of peak production. Last year’s oil spill occurred in the Federal offshore area.

The decline in US oil production had been predicted in advance, although oil companies did not believe the forecasts. M. King Hubbert had predicted in 1956 that oil production in the United States would peak between 1965 and 1970. In the same paper, he also predicted that world oil production would reach a peak around the year 2000.

Hyman Rickover, a four star admiral in the US Navy, gave a speech in 1957 in which he explained the importance of oil, and talked about the fact that oil supplies were expected to run short around 2000, and natural gas and coal not too much later. Because of the likely shortfall, he said the nation should conserve its resources and should tell its children about the upcoming problem, so that planning could be made for the difficult transition away from fossil fuels. Needless to say, schools have not taught much about this problem.

Slide 18

On Slide 18, I show oil production of two areas that were brought on-line after it became clear that US oil production was falling shortly after 1970. The top graph shows European crude oil, which is mostly oil from the North Sea. Its production was on a plateau from 1996 to 2001, but is now declining.

The bottom graph shows Mexican crude oil production. It was ramped up quickly after it became clear that US crude oil production was declining. The graph indicates that since 2004, Mexican oil production has been declining as well.

With all of these areas experiencing declining production, it is not surprising that world oil production has been close to flat. There theoretically is non-liquid oil that could be steamed out, and very deep oil that could be extracted at great cost, but all of this would require huge expense, long lead-times, and assurance that oil prices would be high at the time the oil was finally extracted.

Figure 19

Having flat (or close to flat) world oil production wouldn’t be a major problem, if world demand for oil weren’t rising. But what is happening is that countries like China and India are using a greater percentage of the available oil. Oil exporters are also using more, because their populations are growing rapidly. When these countries use more, this leaves less oil for the United States and other “developed” nations to consume.

Slide 20

I’d like to talk a little now about what happens when an economy doesn’t have enough inexpensive oil.

Slide 21

One thing that tends to happen when oil prices rise is that food prices tend to rise as well. This occurs mostly because oil is used in food production and transport. The fact that food and fuel prices rise at the same time causes a double problem for consumers, since food and fuel for commuting are both necessities. As a result, consumers tend to cut back on discretionary expenditures when oil prices rise.

Higher food prices can have other impacts as well. If people’s incomes haven’t risen and the increase in food price is severe, or if many are unemployed, there may be riots, and governments may be overthrown. We have already seen this in the Middle East and North Africa. If governments cut back on programs for the poor, as in London, this may further raise the potential for riots.

Slide 22

The graph shows that there tends to be a tie between world economic growth and growth in oil use. The tie may be less close after 2005, because of greater coal use in recent years.

Slide 23

Slide 23 shows the steps I see that lead from rising oil prices to recession. I might add that when discretionary spending drops–such as fewer trips to restaurants–employers tend to lay off workers. The fact that these workers have been laid off further adds to the cutback in the purchase of discretionary goods and further adds to debt defaults.

If many people are laid off from work, governments start finding themselves with increasing financial problems for several reasons:

- Lower taxes collected, because fewer people are working

- Higher expenditures, because there are more unemployed people

- Need for stimulus funds, to try to increase employment

- Need for funds to bail out banks and insurance companies

Slide 24

What seems to happen when there is a shortage of cheap oil is that the whole economy tends to shrink. The way I think of it is similar to making a batch of cookies. If a baker finds that he has a recipe that calls for four cups of flour, but he only has three, he needs to make a smaller batch. When he does this, he uses less of his other ingredients as well – sugar, eggs, shortening, and chocolate chips. If he had planned to use a whole bag of chocolate chips, he may only need to use part of a bag.

The economy seems to work in a similar fashion. If oil is too high-priced, the economy shifts to a mode of operation that uses less oil, but also employs fewer workers, uses less steel and copper, and uses less electricity. We call it recession.

Slide 25

Now I’d like to talk a little about what happens after an economy starts hitting the ceiling with respect to economic growth.

Slide 26

One thing that seems to happen is that oil prices seem to keep spiking.

The last recession ran from December 2007 to June 2009. This period started while oil prices were rising, before they hit a peak in July 2008, and ended after prices had collapsed and were again on the upswing.

We are now in the midst of another oil price (and food price) spike. We don’t know for certain that we are headed into a recession, but evidence is starting to point in that direction. Reported economic growth has been less than 1% in the first half of 2011. Given the past history of recessions being associated with oil price spikes, we shouldn’t be surprised if this spike leads to recession in the not too distant future.

Slide 27

Another thing that seems to happen as we start hitting limits is that private debt (blue on Slide 27) starts to decline. This is related to what I said on Slides 6 and 7 about the need for economic growth in order for debt to work out well. If oil prices are high, and recessionary forces are starting to hit, people don’t want to take out loans to expand their businesses, because it doesn’t look like there will be enough sales to support the expansion. Workers don’t want to move up to new bigger homes, partly because they haven’t gotten raises recently, and partly because future prospects don’t look all that good. Some credit card consumers find their cards cut off, because they have failed to make required payments.

Government debt (in red) tends to increase rapidly, but not rapidly enough to keep total debt rising the way it was prior to hitting growth limits. (Government debt in red is added to the private debt in blue, to produce the total debt.)

Government debt grows for a couple of reasons. First, tax revenues tend not to rise as rapidly, or to actually fall, because of higher unemployment rates. Second, government expenditures are higher, both for programs to help the unemployed, and for stimulus programs. This combination leads to the type of debt limit crisis that we recently experienced. Many European governments are experiencing similar difficulties.

Figure 28 – Source of Graph: Paul Chefurka http://www.paulchefurka.ca/Adaptive%20Cycles.html

We can’t know precisely how things will turn out, or exactly what the time frame will be. But at least some estimates are that things will turn out very badly. The shape of the graph shown in Slide 28 is sometimes called “Overshoot and Collapse.”

The problem we have is that the world’s population has grown to 7 billion people. If we substantially cut back on oil (or on fossil fuels in general), there is a question as to whether we will have enough food and water to support the 7 billion people alive today. If we had very many fewer people, we would have much less of a problem.

Some of the particular problems we are running into now relate to government debt, and inability to fund government programs for the unemployed at reasonable tax rates. It is not clear how these can be resolved. It is virtually impossible to raise tax rates enough to cover the cost of currently promised benefits, especially if unemployment rates rise even higher in the future. At the same time, cutting benefits can lead to riots–or even the overthrow of governments.

Slide 29

At this point, alternatives look like they will be too little, too late.

The closest substitute for oil is biofuels, but the ethanol we use today tends to use a huge amount of our corn crop, with very little ethanol yield. In 2011, ethanol is expected to use a little more than half of America’s corn crop. The energy content of a tank of ethanol is equivalent to the amount of food needed to feed a small person for a year. And of course, using a large amount of corn for ethanol tends to keep food prices up.

Most of the mitigations we hear about are electric–wind, and solar photovoltaic, and geothermal, and biogas. One problem with electric mitigations is that they don’t directly fix our oil shortage problem. The cars you and I drive today don’t run on electricity; they run on gasoline or diesel fuel.

Another problem with electricity mitigations is that they tend to produce only a small quantity of electricity. The layer I show as renewables includes all of the “new renewables” I listed above, plus wood scraps and sawdust, which are sometimes burned for electricity. The renewables line is getting thicker, but its growth is almost matched by the shrinkage in hydroelectric over the years. So in total, we aren’t getting very far, very quickly.

Also, I should point out that even if an alternate source of energy is called “renewable,” it doesn’t really mean that it could be maintained for very long, without the use of fossil fuels. Our electricity transmission wires are maintained using trucks and helicopters that use oil-based fuels. Wind turbines (and replacement parts for repairing wind turbines) are shipped using oil-based fuels. It requires fossil fuels to make solar panels.

Another issue is that alternative fuels are often expensive. If high-priced oil is leading to recession, it is difficult to see how even higher-priced alternatives will fix the situation.

Slide 30

Let me conclude by talking a little about where we go from here.

Slide 31

It seems to me that we have to take one day at a time. Worrying about tomorrow doesn’t do a lot of good.

I think we can probably expect another recession and more layoffs. The recession will probably be severe, because governments are in worse financial condition than they were last time around, and will tend to contribute to the recessionary problems, rather than offset them with stimulus funds.

It seems as if there is the possibility of a cutback of government programs. If this happens, there may be people who are hungry, and in need of assistance. There may even be riots.

If a bad recession occurs, almost every business, charity, and church congregation will be in similar circumstances. If sales or donations decrease, they will need to choose between laying off staff or defaulting on debt. Banks and insurance companies are likely to be faced with a large number of debt defaults. It is not clear that these debt defaults will necessarily result in evictions–it wouldn’t work for banks to own a large number of houses, and have people out on the streets.

Slide 32

It seems to me that we should do what we can do today, and not wait until sometime in the future, when the world situation may not be as good. My husband and I took a trip to China in May, figuring that our opportunity might not be as good in a few years.

We should also count our blessings. We live today with luxuries that even kings did not have a few hundred years ago. Life expectancies a few hundred years ago were only 30 to 40 years. Many readers have already lived longer than could be expected, not too long ago.

There is no real solution to our predicament. Even if a cheap liquid fuel could be found in abundance tomorrow, at most what it would do would be move the problem down the road a little way. Population would continue to grow. Pollution would become a greater and greater issue. We would have more problems with fresh water. We would likely come to another limit, in not too many years.

What should we do individually? One possible remedy is to keep some water and food on hand, in case of temporary unavailability. This can work for a short time, but it is really not feasible to store, say, 20 years worth of food and water.

I think that we should plan as if electricity may someday may not be available, or may be available only intermittently, because all of the various systems (financial, oil, electricity) are closely connected, so a disruption in one system may affect other systems. It is good to plan for windows that open, and non-electrical approaches for key business functions.

Gardening sounds like a good idea, and it is. But I don’t think we can count on a garden to save us, if there are starving people near by. In some sense, we really need a solution for everyone, but with 7 billion people in the world, this is difficult to do.

I would not count on paper investments, because of the potential for a large number of debt defaults. If governments are in poor condition, their guarantee of bank accounts and pension plans means less than it did in the past.

High population is clearly an issue. It would be great to be able to fix this problem through smaller family sizes, but doing so is not as easy as it sounds. If there is economic decline in the future, birth control may become less available and governments may not be able to continue to fund their retirement programs. These changes may lead to families having more children, rather than fewer.

I don’t know that any of us have the right answer as to what to do. The best we can do is pool our thoughts. Those who believe in a higher power may want to seek guidance from above, as well. But there are clearly no easy answers.