Steve Sorrel, Senior Fellow, Sussex Energy Group, University of Sussex in the UK has recently published a 25 page paper called Energy, Growth and Sustainability which can be downloaded at this link. This post provides some excerpts from the paper, which summarize its findings. Readers are encouraged to read the entire paper.

According to the introduction to the paper:

This paper questions the conventional wisdom underlying climate policy and argues that some long-standing and fundamental questions regarding energy, growth, and sustainability need to be reopened. It does so by advancing the following propositions:

1. The rebound effects from energy efficiency improvements are significant and limit the potential for decoupling energy consumption from economic growth.

2. The contribution of energy to productivity improvements and economic growth has been greatly underestimated.

3. The pursuit of improved efficiency needs to be complemented by an ethic of ‘sufficiency’.

4. Sustainability is incompatible with continued economic growth in rich countries.

5. A zero-growth economy is incompatible with a debt-based monetary system.

These propositions run counter to conventional wisdom and highlight either blind spots or taboo subjects that deserve closer scrutiny. While accepting one proposition reinforces the case for accepting the next, the former is neither necessary nor sufficient for the latter.

1. Rebound effects are significant and limit the potential for decoupling energy consumption from economic growth

This is basically Jevons’ paradox, which has been discussed quite a few times on The Oil Drum. As technology increases the efficiency with which a resource is used, use of the resource tends not to decline as predicted. Instead, there tends to be a rebound effect, and the amount of the resource used may even increase instead. The section concludes:

In sum, rebound effects will make energy efficiency improvements less effective in reducing overall energy consumption than is commonly assumed. This could limit the potential for decoupling, although by precisely how much remains unclear. In principle, increases in energy prices should reduce the magnitude of such effects by offsetting the cost reductions from improved energy efficiency. This leads to the policy recommendation of raising energy prices through either carbon taxation or emissions trading schemes. Price increases will induce substitution and technical change , but their impact on total factor productivity and economic growth remains disputed (Jorgensen, 1984; Sorrell and Dimitropoulos, 2007c). This leads to the second proposition, discussed below.

2. The contribution of energy to productivity improvements and economic growth has been greatly underestimated

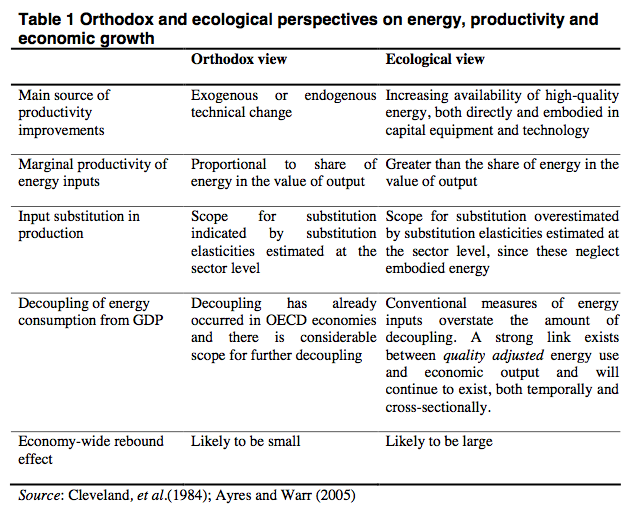

Many of the arguments in favour of Jevons Paradox focus on the source of productivity improvements and the relationship between energy consumption and economic growth. Orthodox and ecological economics provide very different perspectives on this question with correspondingly different conclusions on the potential for decoupling.

Orthodox economic models imply that the economy is a closed system within which goods are produced by capital and labour and exchanged between consumers and firms. While such models can be extended to include natural resources, ecosystem services and wastes, these remain secondary concerns at best. Economic growth is assumed to derive from a combination of increased capital and labour inputs, changes in the quality of those inputs (e.g. better educated workers) and technical change (Barro and Sala-I-Martin, 1995; Jones, 2001). Both increases in energy inputs and improvements in energy productivity are assumed to make only a minor contribution to economic growth, largely because energy accounts for only a small share (typically <5%) of total input costs. It is also assumed that capital and labour will substitute for energy should it become more expensive. From this perspective, improvements in energy efficiency are unlikely to have a significant impact on overall productivity, so the corresponding rebound effects should be relatively small. Hence, there seems to be no reason why energy consumption could not be substantially decoupled from economic growth.

Ecological economists consider that the orthodox models ignore how economic activity is sustained by flows of high quality energy and materials which are then returned to the environment in the form of waste and low temperature heat. The system is driven by solar energy, both directly and embodied in fossil fuels, and since energy cannot be produced or recycled it forms the primary input into economic production. In contrast, labour and capital represent intermediate inputs since they cannot be produced or maintained without energy. So far from being a secondary concern, energy becomes the main focus of attention.

Ecological economists claim that the massive improvements in labour productivity over the last century have largely been achieved by providing workers with increasing quantities of high quality energy, both directly and indirectly as embodied in capital equipment and technology . . .

Ecological economists also claim that the indirect energy consumption associated with capital and labour (e.g. the energy required to manufacture thermal insulation) limits the extent to which they can substitute for energy in economic production (Stern, 1997). The energy embodied in capital goods is commonly overlooked by studies that estimate energy-saving potentials at the level of individual sectors and then aggregate the results to economy as a whole. Furthermore, many energy-economic models assume a greater potential for substitution that is allowed for by physical laws (Daly, 1997). Hence, from an ecological perspective, the potential for decoupling energy consumption from economic growth appears more limited (Table 1).

The paper provides considerable discussion and gives empirical support for the ecological perspective. This section concludes:

In sum, orthodox analysis implies that rebound effects are small, improvements in energy productivity make a relatively small contribution to economic growth and decoupling is both feasible and cheap. In contrast, the ecological perspective suggests that rebound effects are large, improvements in energy productivity make an important contribution to economic growth and decoupling is both difficult and expensive. While the empirical evidence remains equivocal, the ecological perspective highlights some important blind spots within orthodox theory that are reflected in the design of economic models used to underpin climate policy. If this perspective is correct, both the potential for and continued reliance upon decoupling needs to be questioned.

3. The pursuit of improved efficiency needs to be complemented by an ethic of sufficiency

The key idea here is sufficiency, defined by Princen (2005) as a social organising principle that builds upon established notions such as restraint and moderation to provide rules for guiding collective behaviour. The primary objective is to respect ecological constraints, although most authors also emphasise the social and psychological benefits to be obtained from consuming less.

While Princen (2005) cites examples of sufficiency being put into practice by communities and organisations, most authors focus on the implications for individuals. They argue that ‘downshifting’ can both lower environmental impacts and improve quality of life, notably by reducing stress and allowing more leisure time. This argument is supported by an increasing number of studies which show that reported levels of happiness are not increasing in line with income in developed countries (Blanchflower and Oswald, 2004; Easterlin, 2001). As Binswanger (2006) observes:

“…the economies of developed countries turn into big treadmills where people try to walk faster and faster in order to reach a higher level of happiness but in fact never get beyond their current position. On average, happiness always stays the same, no matter how fast people are walking on the treadmills”.

It is possible that an ethic of sufficiency could provide a means of escaping from such treadmills while at the same time contributing to environmental sustainability.

The section concludes:

A successful ‘sufficiency strategy’ will reduce the demand for energy and other resources, thereby lowering prices and encouraging increased demand by others which will partly offset the energy and resource savings. While this ‘sufficiency rebound’ could improve equity in the consumption of resources, it will nevertheless reduce the environmental benefits of the sufficiency measures. But since the global ‘ecological footprint’ already exceeds sustainable levels in many areas the global consumption of resources needs to shrink in absolute terms (Rockström, et al., 2009). To achieve this and to effectively address problems such as climate change, will require collective agreement on ambitious, binding and progressively more stringent targets at both the national and international level.

4. Sustainability is incompatible with continued economic growth in rich countries

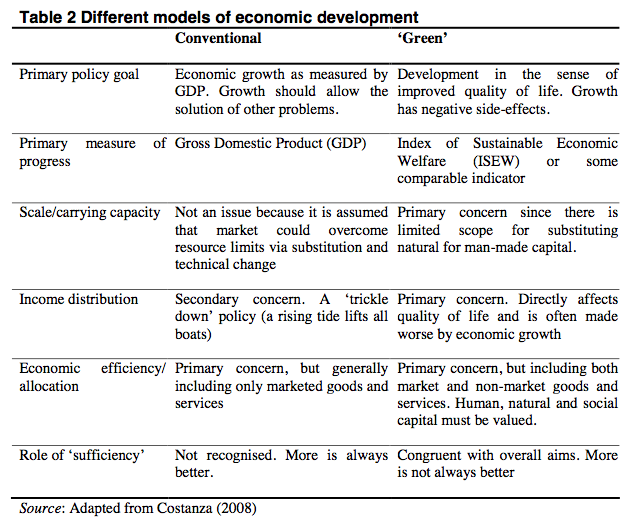

The preceding arguments highlight a conflict between reducing energy consumption in absolute terms whiles the same continuing to grow the economy. Recognising the importance of rebound effects and the role of energy in driving economic growth therefore re-opens the debate about limits to growth. This debate is long-standing and multifaceted, but a key point is that the goal of economic development should not be to maximise GDP but to improve human well-being and quality of life . . .

Table 2 compares this emerging ‘green’ perspective on economic development with the orthodox model. . .

Over the long term, continued economic growth can only be reconciled with environmental sustainability if implausibly large improvements in energy efficiency can be achieved. This point is easy to demonstrate with the I=P*A*T equation, which represents total environmental impact (I) as the product of population (P), affluence or income level (A) and technological performance or efficiency (T) (Ehrlich and Holdren, 1971). In the case of climate change, I could represent total carbon emissions, A GDP per capita and T carbon emissions per unit of GDP (itself a product of energy consumption per unit of GDP and carbon emissions per unit of energy consumption). The decoupling strategy seeks reductions in T that will more than offset the increases in P and A, thereby lowering I. . .

The required changes look even more challenging when rebound effects are considered. The I=P*A*T equation implies that the right-hand side variables are independent of one another – or at least if any dependence is sufficiently small that it can be neglected. But in practice the variables are endogenous. So while a reduction in the economy-wide emission intensity (T) may have a direct effect in lowering emissions (I), it will also encourage economic growth (A), which in turn will increase emissions. Over the long term and up to a certain level of income, rising affluence (A) encourages higher population levels (P), which will further increase emissions (I). Hence, a change in T will trigger a complex set of adjustments and the final change in emissions is likely to be lower than the IPAT identity suggests. This in turn, implies that greater changes in T will be required to achieve a particular reduction in I.

Hence, in an increasingly ‘full’ world, the goal of continued economic growth in the rich countries deserves to be questioned.

I have omitted several paragraphs of this discussion, taking about how reductions in emission would have to be vastly larger than assumed in the Stern report, to get both economic growth and 350 ppm of CO2. A direct calculation of the needed reduction in emissions would be 6.9% per year, but with the impact of Jevons’ paradox, the necessary reduction in CO2 emissions would need to be much larger that 6.9% per year. This is far outside the range of anything anyone has considered.

5. A zero-growth economy is incompatible with a debt-based monetary system

An excerpt:

A purely private enterprise system can only function if companies can obtain sufficient profits which in turn requires that the selling price of goods exceeds the costs of production. This means that the selling price must exceed the spending power that has been ‘cast into circulation’ by the production process. Hence, to ensure sufficient ‘aggregate demand’ to clear the market, additional spending power is required from some other source. In a purely private enterprise system, this normally derives from investment in new productive capacity which will increase the amount or quality of goods supplied, but only after some interval. Investment therefore serves the dual role of increasing productive capacity and creating additional demand to clear the market of whatever has already been produced (Hixson, 1991). Importantly, the investment cannot be financed from savings since the resulting increase in aggregate demand would be offset by a corresponding decrease in consumption spending.

Aggregate demand is commonly expressed as the product of the amount of money in circulation and the speed with which that money circulates through the economy. Hence increases in aggregate demand require increases in the money supply or the speed of circulation or both. Increases in the money supply, in turn, lead to increases in aggregate output, the average price of goods and services or both.

The key issue is how the increase in the money supply is brought about. Governments could (and should) create the new money interest-free and spend it in to circulation in much the same way as coins and notes are created. But instead, the bulk of the money supply is created by commercial banks who print credit entries into the bank accounts of their customers in the form of interest-bearing loans. This system of ‘fractional reserve banking’ has its origins in the essentially fraudulent practices of the early goldsmiths who made ‘loans’ of a far greater quantity of gold that they actually held in their vaults. This gave them substantial profits and allowed them to increase their claims on wealth (in the form of collateral), but also served the essential function of increasing purchasing power in a growing economy. This practice gradually evolved into modern banking, with central banks imposing minimum reserve requirements and acting as a lender-of-last-resort.

A crucial consequence of this system is that most of the money in circulation only exists because either businesses or individuals have gone into debt and are paying interest on their loans. While individual loans may be repaid, the debt in aggregate can never be repaid because this would remove virtually all the money from circulation. The health of the economy is therefore entirely dependent upon the continued willingness of businesses and consumers to take out loans for either investment or consumption. Any reduction in borrowing therefore threatens to tip economies into recession.

Individual loans need to be repaid with interest, but the money required to pay this interest was not created with the original loan. While banks will recycle a large part of the interest payments in the form of wages, dividends, and investments, a portion will be retained as bank capital to underpin further loans (Binswanger, 2009). Hence, the only way that individual borrowers can pay the interest on their loans, without at the same time reducing the money supply, is if they, or other borrowers, borrow at least as much as is being removed (Douthwaite, 2000). As a result, the amount of money in circulation needs to rise each year which means that the value of goods and services bought and sold must also rise, either through inflation or higher consumption (Douthwaite, 2000). In other words, both debt and GDP must grow – with the former growing faster than the latter.

Slow or negative growth will leave firms with lower profits and unused capacity, discouraging them from investing. Less investment will means fewer loans being taken out and thus less money entering into circulation to replace that being removed through interest payments. And less money in circulation will mean that there is less available for consumers to spend, which will exacerbate the economic slowdown and cause more bankruptcies and unemployment. By such processes, the monetary system creates a structural requirement for continued growth and increased consumption.

Summary

This paper has advanced five linked and controversial propositions regarding energy consumption, economic growth and sustainability. These run counter to conventional wisdom and highlight either blind spots or taboo subjects within orthodox theory. Each raises numerous theoretical and empirical questions that deserve both detailed and critical investigation. This will take time, but that commodity is becoming increasingly scarce.

A sustainable economy needs to have much higher levels of energy and resource efficiency than exist today and policies to encourage this have a crucial role to play. But for the reasons outlined above, this is unlikely to be sufficient to meet growing environmental constraints. Instead of encouraging further growth and greater consumption, the benefits of improved efficiency need to be increasingly channelled into low carbon energy supply and improved quality of life. Quite how this can be achieved remains far from clear since a credible ‘ecological macroeconomics’ has yet to be developed. Most importantly, a crucial element of that macroeconomics – namely monetary reform – remains almost entirely overlooked. It is hoped that this paper will at least stimulate some thinking in that direction.