I decided to write another rather basic level article because there are so many people I meet who have heard a bit about the oil situation, and it is hard to point to one single article to give an overview of some of the current issues. Regular readers will find many repeats of graphs. There are some new ones, as well, from the Denver ASPO-USA conference. Because there is so much to tell, the story gets a little long.

We live in a finite world. It is clear that at some point, we will eventually start hitting limits—we won’t be able to extract as much oil, or we won’t be able to mine as much silver or platinum, or fresh-water aquifers that have built up over millions of years will run dry.

We are reaching limits in several areas, but the one I would like to talk about here is oil production. Oil is essential, because nearly all transportation depends on oil, and because a huge number of goods use oil in their manufacture (including textiles, pharmaceuticals, pesticides, asphalt, plastics, lubricating oils, and computers). Oil is also essential for our current agricultural system–growing food and transporting it to market.

Why people are concerned about a decline in oil production

Quite a few people are familiar with the peak oil story. If you haven’t heard it, here it is in a few graphs.

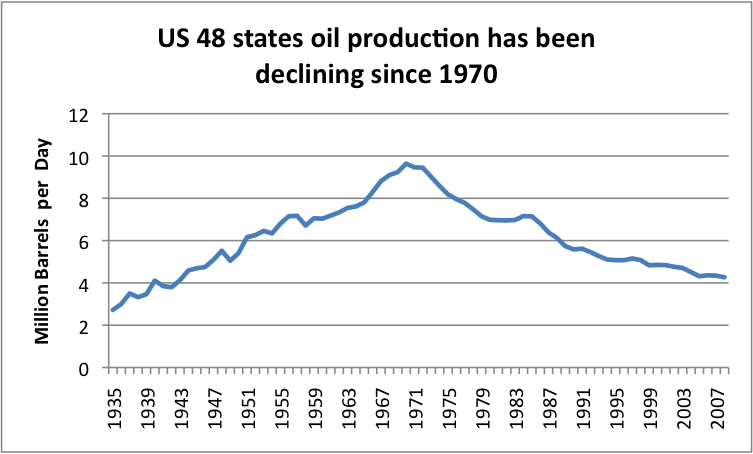

Once upon a time, the US was the biggest producer of oil in the world. Our production was growing rapidly—until suddenly, oil production began to decline:

Oil companies had generally not realized that anything was amiss prior to the decline, and in fact, were forecasting continued growth for many years. This decline in production for the US had been predicted by M. King Hubbert in 1956, but few believed him. He also made predictions that world oil production would begin to decline around 2000. His prediction was based on the fact that it was a finite resource, and it would become more difficult to extract over time.

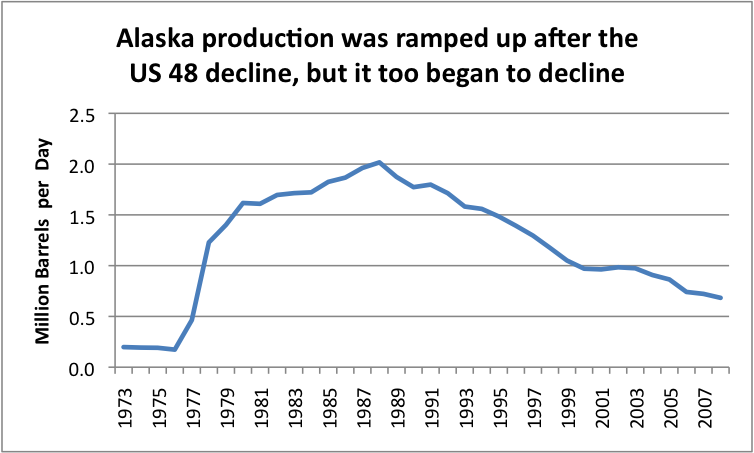

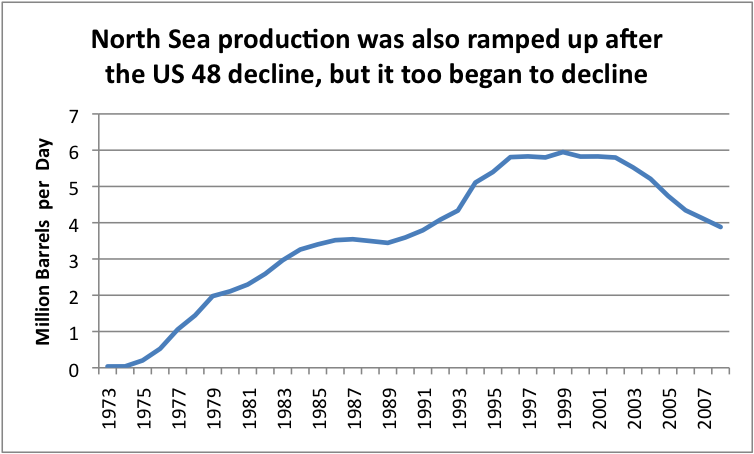

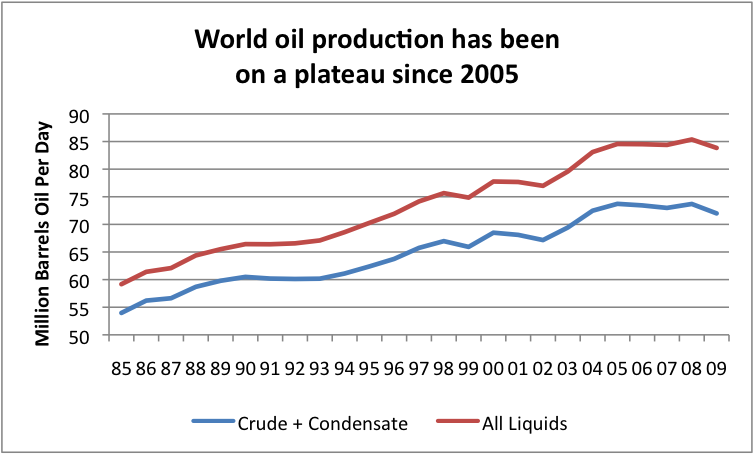

After the decline in oil production in the US 48 states took place, production was expanded elsewhere, but after not too long, these too, began to decline:

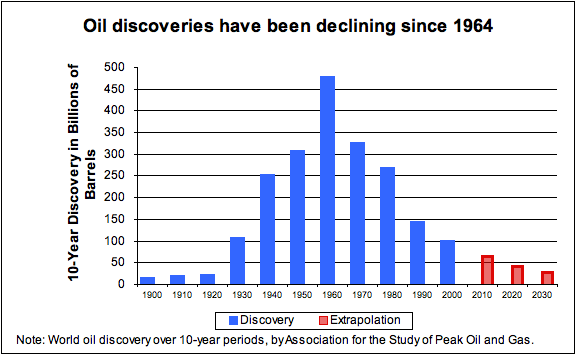

Finding new inexpensive places to drill became more and more difficult, as the world got better explored, and the easy-to-exploit areas were tapped first. One problem was that new discoveries of oil in liquid form kept getting smaller and smaller:

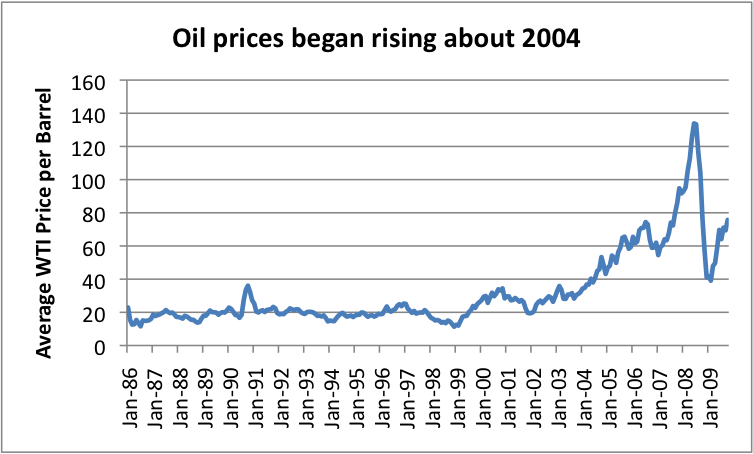

One might think that at some point, world oil production would start running into difficulties. Not too surprisingly, between 2004 and 2008, we experienced a long-term rise in oil prices.

During the period when the price for oil was rapidly rising, one might think that oil production would be rapidly ramping up to meet demand, but this was not in fact the case.

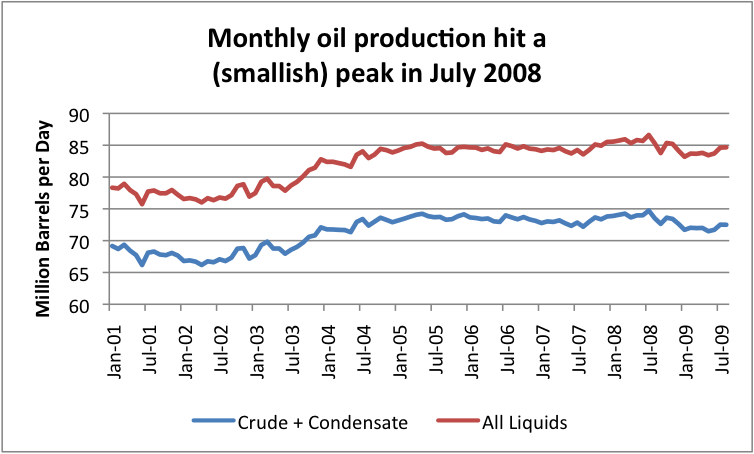

Oil production was in fact quite level during this time period, with only a slight uptick in production in 2008, about the time prices hit their highest point.

Oil production hit its highest point ever in July 2008, the same month that oil prices peaked.

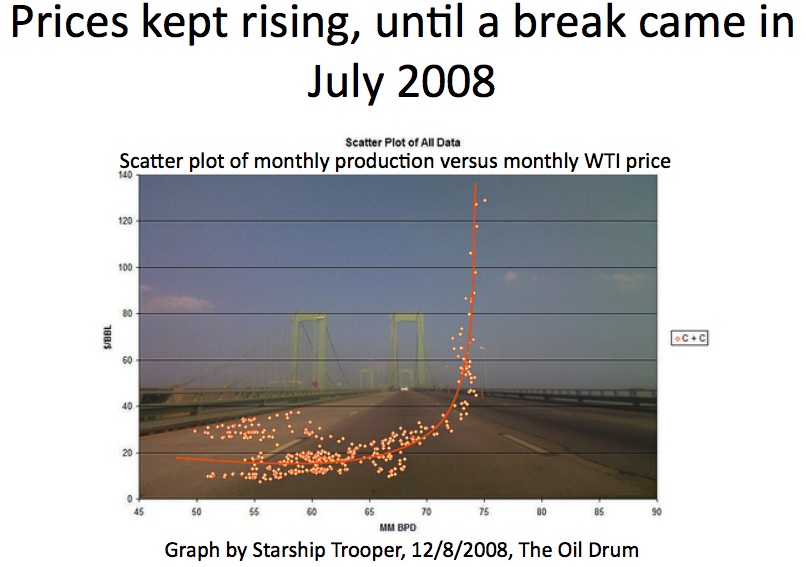

Figure 8 compares something that most of us wouldn’t think of plotting together—monthly oil production (crude and condensate in million barrels per day) versus oil price. What one can see from the graph is that oil production just barely increased, even as prices rose rapidly. One gets the impression that oil supply is extremely inelastic—no matter how much price rises, supply doesn’t increase by much. This is what one might expect if oil production is reaching its limit.

All of these graphs seem to point in the direction of world oil production approaching its limit. There are a lot of suspicious signs—particularly the virtually flat volume, with rising prices.

I’ll continue with what happened recently, but let’s stop first and look at the connection between oil and the economy.

Oil and the Economy

If oil is essential to the economy, because it is used for food and transportation and many other things, one might think that lack of oil might have an adverse impact on the economy. There are many ways of seeing this is in fact the case.

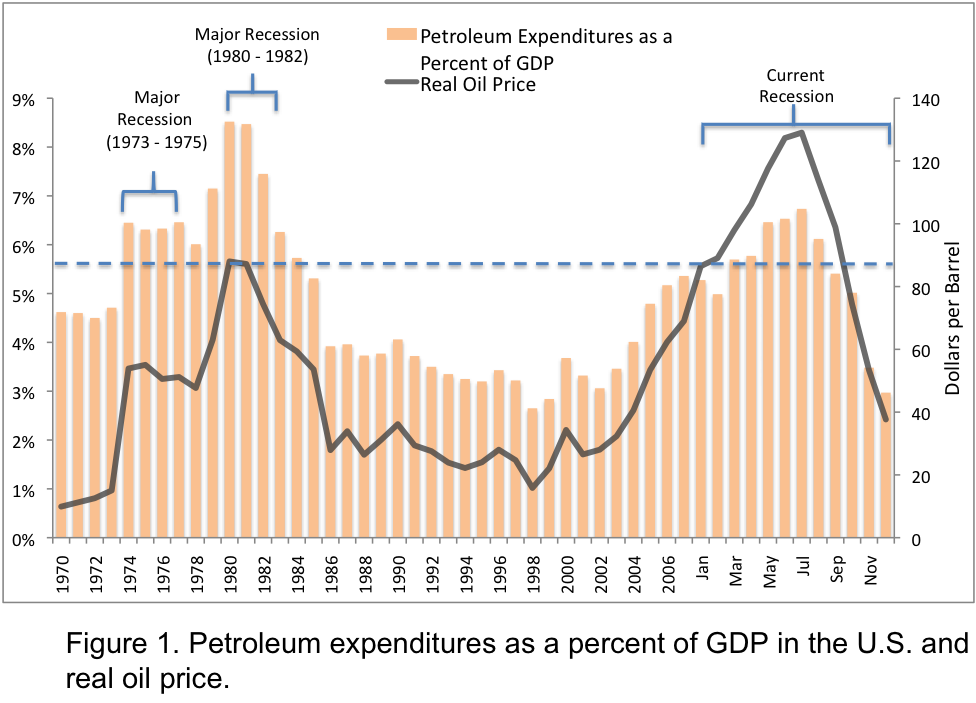

Dave Murphy of The Oil Drum has shown that if the oil price goes much above $80 or $85 in inflation adjusted terms, the economy tends to go into recession.

The problem with $80 or $85 barrel oil sending the economy into recession is the fact that much of the oil that remains is “difficult oil”, that is expensive to extract. If producing oil at this price is an issue, then much of the remaining oil may throw the world further into recession—because when people spend so much money for oil, (and indirectly for food, and for all things that have a transportation cost component), they don’t have enough left over for everything else. People cut back on non-essentials, and soon the economy goes into recession.

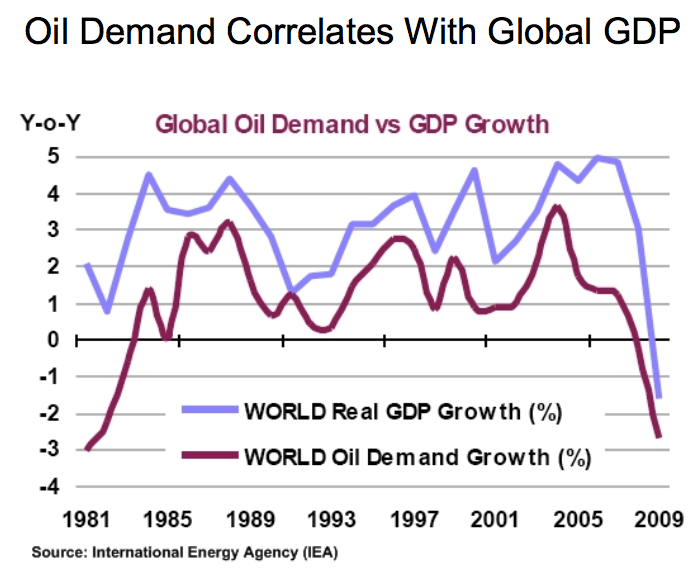

Dave Cohen of ASPO-USA shows in Figure 10 that growth in global GDP seems to be highly correlated with growth in global oil consumption. This would tend to mean that if oil production actually starts declining, the world economy is likely to begin declining as well.

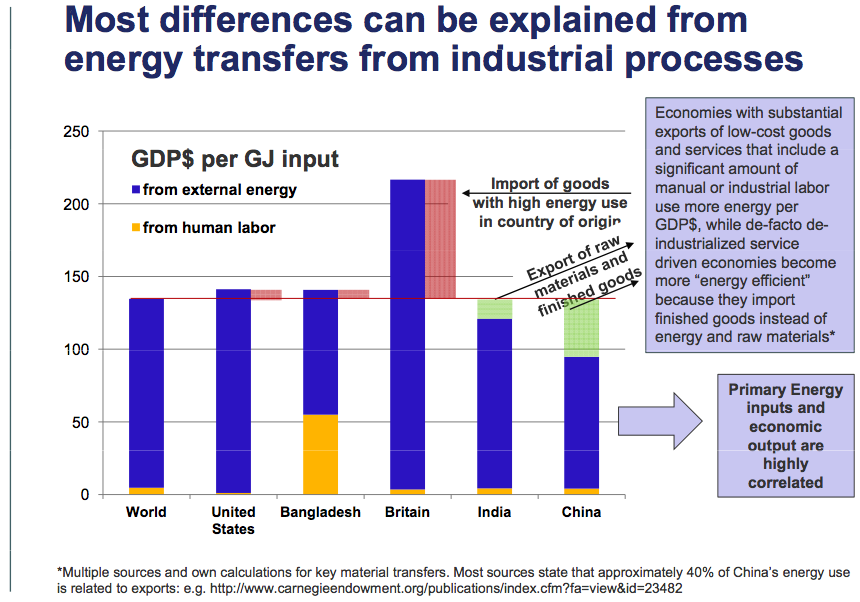

Figure 11 – Graph by Hannes Kunz from ASPO-USA presentation.

There has been much talk recently about the US economy becoming less tied to oil. A recent presentation by Hannes Kunz shows that much of what appears to be an improvement is related to “offshoring” of the more energy-intensive industries (Figure 11.) This further emphasizes the need for energy, if we are to have true economic growth.

We saw in Figure 5 that the price of oil went up in the 2004 to 2008 period. Sam Faucher has shown that a shortage of oil supply (relative to what one would expect the economy to use based on trend) can be shown to underlie this increase in price. A 1 million barrel a day shortfall in oil supply for OECD seems to correspond to a $20 barrel increase in oil price.

Growth and Credit

It is bad enough that a decline in oil production (or an increase in price above $80 to $85 barrel) tends to send the economy in recession. We will see in this section that the credit situation has the potential to make the situation very much worse.

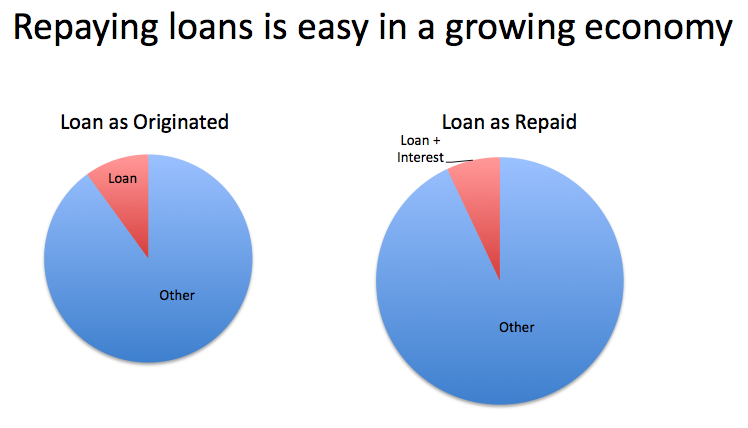

Buying goods on credit works much better in a growing economy than in a shrinking economy.

If a person (or business or government) takes out a loan in a growing economy, there is a good chance that the economy will be better when the loan is to be paid back with interest. The growing economy means that even when interest is repaid on the loan, there will still be enough for everything else.

In a shrinking economy, the reverse happens. Instead of being better of financially when it comes time to pay back the loan, one is likely to be less well off (for example, an individual would be more likely to have lost his job, or a government would be more likely to be collecting less revenue). Paying back the loan would be much more difficult, and would leave less for other needs.

As we have seen, there appears to be a very good chance oil supply will decline in the future. If oil supply declines, we are likely to have economic decline, and with economic decline, loans will be more difficult to repay.

The problem is that our whole economy is built on credit. Our monetary system is a credit-based system, in which money is loaned into existence. Our international trade system is based on credit. The US has been buying far more oil than it could pay for based on the value of the goods it exports—the difference is made up with more and more promises to pay in the future.

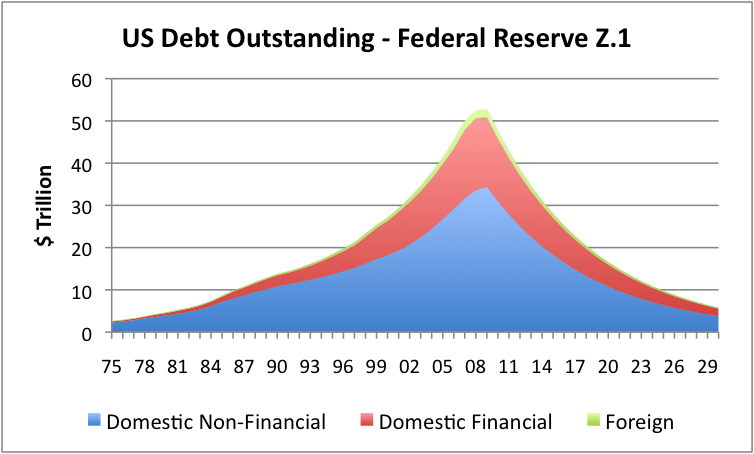

The amount of debt outstanding in the United States (and many other countries) has grown greatly in recent years. This growth in debt has had a beneficial impact on reported GDP, since GDP calculations reflect expenditures without subtracting out debt related to those expenditures. In fact, the loosening of housing credit in recent years may have been an attempt to cover up the lack of “real growth” after the growth in oil production started slowing about 2004 -2005. An increase in debt would give the illusion of growth, and have some of the same benefits—higher reported GDP, rising home prices, rising stock market prices, and increased ability of homeowners to draw down the rising equity or their homes, to use for yet more purchases.

The problem if debt availability starts decreasing is that we start getting to all kinds of unpleasant results. People are less able to buy houses and cars. Housing values drop and defaults rise. The value of commodities, including oil, drop, because they are less needed for producing houses and cars.

Investment for many kinds of things—not just oil–becomes more difficult, because debt financing is not available. Also, cash flow that might be used for investment is down, because of the price of commodities, and because of the inability of consumers to spend. If oil production and credit both decline, real GDP will tend to drop even more than it would have based on the relationship shown in Figure 10, because an increase in debt helps GDP; a decrease hurts it.

What happened to oil after July 2008?

We saw in Figure 5 that oil prices reached their peak value in July 2008. But why?

It seems to me that a major part of the reason must have been a change in the credit markets. Credit markets started unwinding about then, and this brought the support for the price of oil down. Without credit, consumers could not buy all the consumer goods that use oil, and businesses, even intermediaries in the oil business, couldn’t necessarily buy the goods they want.

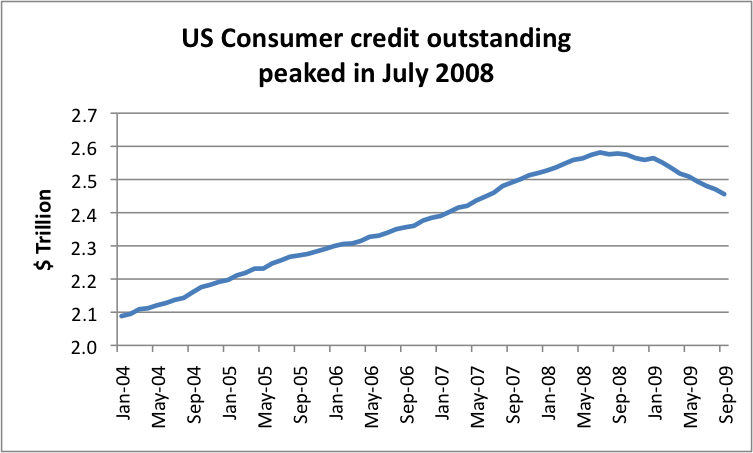

Figure 15 shows that US consumer credit peaked at the same time as oil prices. The amount of mortgage debt also began falling about the same time. Lending in generally became tight, especially later in 2008.

Even now, we read in Platt’s report Hedging in the Oil Markets –Challenges in 2009 and Beyond:

Unsurprisingly it is credit and counterparty risk that tops the list of concerns amongst energy professionals when talking about managing cost. Almost without exception it is these two themes that are at the forefront of everyone’s mind. Market risk is still prevalent, but it has taken a backseat to credit as the major influence on decision making.

“Counterparty risk and credit risk are still the big areas to look at. Banks cannot necessarily sustain all of their back to back hedges. Who can you go to?” a market analyst said. “With counterparty risk – who will be there in a few months time? People are trying to aggregate credit risk rather than market risk now.”

The unwinding of credit and the associated drop in demand would explain the sharp drop in price in July 2008 (Figure 5). Even now credit has not fully recovered. Given the problems one would expect with credit when oil is declining in availability and exerting a downward impact on economic growth, it is not at all surprising that credit is still a problem.

Prices have not risen to their previous level, because of credit issues holding demand down. Funds available for investment have dropped because (1) less credit is available for financing, (2) the lower commodity prices leave less for cash flow, and (3) at the lower prices, more expensive types of investments no longer look profitable.

Looking Ahead

I don’t think anyone doubts that there are huge resources theoretically available to the oil and gas industry, including oil sands, shale oil, polar oil, and very deepwater oil.

The problem is that most of the oil available, especially to the Independent Oil Companies, is either has a very slow flow rate, or is quite expensive to extract, or both. The flow rate of any oil that has to be melted (such as oil sands or very heavy oil) is never going to be very high. Oil that is very expensive to produce, such as deep sea oil, very likely will not be profitable except at a price which puts the US economy into recession.

There is a fairly long lead-time on new projects—typically six to 10 years—so one knows a to some extent how much oil is likely to be available in the next few years.

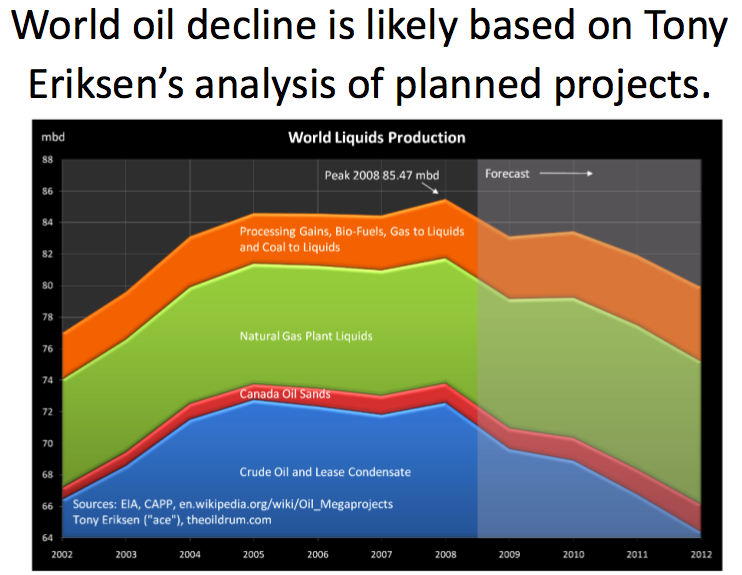

Tony Eriksen (ace) shows his forecast in Figure 16. Other analysts using a similar approach get somewhat different results. But even with more optimistic assumptions, this type of approach seems to indicate that world oil supply will be at best flat—or perhaps declining just a bit in the near future. If there is a huge improvement in technology, or a much higher level of investment, things could theoretically get better, but so far there doesn’t seem to be any indication of this. Investment is in fact down.

The problems we are seeing today in terms of recession and reduced credit availability are precisely the kinds of impacts we would expect to see from oil flow that does not meet society’s needs at an acceptably low price. While one cannot prove that our current economic problems are mostly related to the oil situation, it is hard to believe that the relationship could be happenstance. Even the crazy build-up in mortgage loans prior to the collapse may have been a way of disguising the real lack of growth in the economy, as world oil production stalled.

Going forward, it seems likely that the economic situation will generally trend downward, from the level we are currently at. Figure 10 showed that the increase or decrease in GDP tended to rise or fall with oil production. In Figure 10, the percentage increase or decrease in GDP tended to be somewhat higher than the percentage increase in oil production—but the graph relates to a period when debt was increasing. In a period of decreasing debt, one would expect the relationship to be more adverse—more downward trend in GDP for a given reduction in oil production.

In addition, if debt is decreasing, the price of oil is likely to stay on the low side, because of reduced consumer demand (layoffs and inability to by cars and new houses). The low price will make it difficult for oil companies to generate revenue from cash flow to use for investment, leading to less investment. The low prices will also discourage investment in places where oil is theoretically available, but the cost of extraction is too high.

I mentioned earlier (Figure 9) that above $80 or $85 a barrel, the economy tends to go into a recession. This is likely to be a barrier to developing much of the remaining oil resources. While there are a lot of resources in the ground, very little of it is easy-to-develop liquid crude. Most of it is in a tricky location (such as polar or very deep sea), or is a semi-solid that must be melted, or requires very specialized refining.

It is not clear that the $80 or $85 barrel threshold will remain either, in terms of being difficult for the economy to withstand. With reduced credit (still paying off old debt, but unable to obtain new), buyers will be less and less able to afford products made from oil. It is possible that the threshold for economic problems will occur at even a lower price level for oil—say $60 or $70 barrel.

I mentioned that credit is tied in with a huge amount of our economy—including our monetary system and our international trade system. So far, credit is down a little, but it still has a long ways to go. Also, while credit is down, the system is still holding up pretty well. The concern I have is that as oil production declines, it will be more and more difficult for the credit system to hold up.

For example, the US is buying oil on credit, because it does not have exports to pay for its imports. This has been going on for years, leading to more and more debt. At some point, it seems like this situation has to stop. Some exporter is going to catch on to the fact that we are likely never are going to pay our debts and change the system—cut off credit, or require that we offer needed goods in return—say a certain amount of wheat for a particular amount of oil.

If problems with international trade develop, they are likely to have a hugely negative impact on manufacturing of high tech equipment. Think about what is required for something as basic as a computer—petroleum to make the plastic case; several kinds of metals; a factory set up with precision equipment. Keeping the whole manufacturing system going requires a steady stream of imports from around the world.

Eventually, it seems likely that we will have to move back to a system similar to that of many years ago, where food is grown locally, and goods are manufactured locally, with local materials. It is not clear how much of modern transportation can be maintained—we may need to look at methods used centuries ago.

Why didn’t anyone tell us about this problem?

Common sense tells us that at some point, a finite world is going to run into limits. M. King Hubbert predicted the problem in 1956. A year later, 1957, Rear Admiral Hyman Rickover spoke about the problem:

I suggest that this is a good time to think soberly about our responsibilities to our descendants – those who will ring out the Fossil Fuel Age. Our greatest responsibility, as parents and as citizens, is to give America’s youngsters the best possible education. . . . We might even – if we wanted – give a break to these youngsters by cutting fuel and metal consumption a little here and there so as to provide a safer margin for the necessary adjustments which eventually must be made in a world without fossil fuels.

The fact that resources were limited was known, but there seemed to be reasons not to bring up the issue. M. King Hubbert wasn’t really believed until after US production began to fall in 1970. And even if he was believed, with such a distant event, it probably seemed likely that technological advances would increase the amount of oil that could be quickly and cheaply extracted, for many years.

Also, it seemed like there would be other energy sources that would be able to replace our current energy sources. But so far, none of these is working out very well. Natural gas recently has looked like it may have potential to be a temporary partial solution, but even this is “iffy”. It may very well prove to be equivalent to $150 oil—more expensive than we really can make use of.

There have been many other energy ideas that have been looked at as well (biofuels, wind, solar, hydrogen, wave, etc.) but none is really a very adequate substitute for oil, and all are expensive, especially when one considers the entire “package” of upgrades that would be needed to make them act as a substitute for oil.

One would think that a magazine like Scientific American would bring this issue to the American public, but in recent years the magazine have tended to bring the public fanciful solutions, without pointing out the difficulties of these solutions. Their latest is in the November 2009 issue. My analysis can be found here.

There are two major organizations that forecast future oil production—the International Energy Agency (IEA) and the US Energy Information Administration (EIA). Both put out rosy forecasts of future oil production, year after year, even though the problems have been plain for quite a few years to anyone who looked at the situation very closely.

The UK Guardian published an article recently called “Key oil figures were distorted by US pressure, says whistleblower.” The article says that indications have been distorted under pressure from the Americans, and one senior official is quoted as saying, “We have [already] entered the ‘peak oil’ zone. I think that the situation is really bad.” Similar reports about IEA distortions have been reported elsewhere.

If the IEA has been pressured by the Americans into giving overly-optimistic numbers, one can only guess that as much, or more, pressure has placed on the US organization, the EIA. The result is the very optimistic numbers published widely, and frequently cited to show there is no problem.

One factor that has helped to confuse the matter is the optimistic reserve numbers published by the Organization of Petroleum Exporting Countries (OPEC). These reserve amounts are unaudited, and are quite likely overstated. Over a long enough time frame (hundreds of years) and at a high enough price, these numbers are perhaps correct, but it is very questionable whether OPEC can really ramp up production hugely in the next few years—or that they would want to, if it is clear that some of the world’s buyers really are not very credit-worthy.

Most of the analyses regarding oil production from the “peak oil community” have looked at the future decline in oil production strictly from a geological decline point of view. Geological decline is part of the issue—how much will production drop because the oil that is extracted is mixed with more and more water, and it is not possible to bring sufficient new production on line to offset the decline?

But, in my view, an equally big question is how much economic factors will influence future production. Will the international credit situation hold up adequately? Will lack of credit keep prices so low that investment in new extraction is greatly reduced? Will buyers of homes and cars be in sufficiently good financial condition to keep demand for oil and other products up? None of us really know the extent these factors will affect production, so it becomes difficult to have good numbers to give the American public.

The Task Ahead

There are many views of the task ahead. Some think more research is the answer, or more nuclear, or improved electric transmission plus wind turbines, or electric trains. To a significant extent, these views depend on a person’s view of the timeframe involved, their analysis of where we are now, and their view of how much or how little international trade will be affected in the years ahead.

My personal view is that the main task we should be focusing on now is how to move to a much simpler system—one that depends mostly on locally grown food and locally manufactured goods. This will likely mean a much lower standard of living. Limiting population should probably be a goal, because it will be easier to have enough for all if there are fewer mouths to feed.

I do not see climate change legislation as terribly helpful. Cap and trade will add huge overhead to the system—something we really cannot afford right now. Peak oil is likely to mean a continuing major recession, and a natural decline in fossil fuel use. To me, we would be better off spending our resources developing local agriculture and local manufacturing, and perhaps even sailing ships.