NOTE: Images in this archived article have been removed.

Presentation to the American Geophysical Union fall meeting, December 17, 2015, San Francisco; Union Session on “Is Peak Oil Dead and What Does It Mean for Climate Change?”

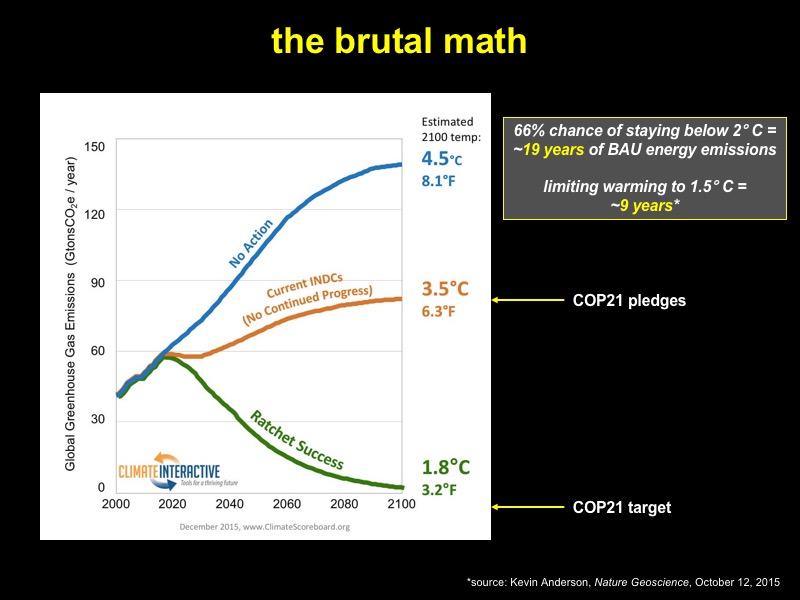

According to the IPCC’s Synthesis Report, achieving a 66 percent chance (or better) of Earth surface temperatures warming only 2 degrees Centigrade over preindustrial times requires emitting no more than 1,000 Gigatons of CO2 between 2011 and 2100. However, as climate scientist Kevin Anderson has pointed out, emissions from energy production between 2011 and 2014 were about 140 Gt. Subtracting realistic emissions budgets for deforestation and cement production, the remaining budget for energy-only emissions to 2100 is about 650 Gt of CO2. That equates to just 19 years of continued business-as-usual emissions from global fossil energy use. The recent Paris agreement states the aspirational goal of not exceeding 1.5 degrees, which would translate to less than a decade’s worth of fossil fuel consumption at current rates—though some climate scientists would argue that we may reach 1.5 degrees and higher on the basis of carbon already released into the atmosphere and oceans.

In any case, as we have heard, some estimates of global fossil fuel reserves—including unconventional oil and gas—imply several times that 650 Gt budget of potential greenhouse gas emissions. While, as previous speakers noted, there is cause to be skeptical of these estimates, it is clear that the carbon budget available to stay within a 1.5 degrees or even 2 degrees warming limit is small. That means a lot of fossil fuels will have to be left in the ground. What socio-political, technological, or economic forces might keep these energy resources from being burned?

There are at least four key potential drivers:

1. Under-investment and the economics of unconventional oil and natural gas.

As Jim Murray has explained, tight oil and shale gas—which offer the greatest and most immediate promise of increased production rates for oil and gas—suffer from high decline rates and the resulting need for high rates of drilling.

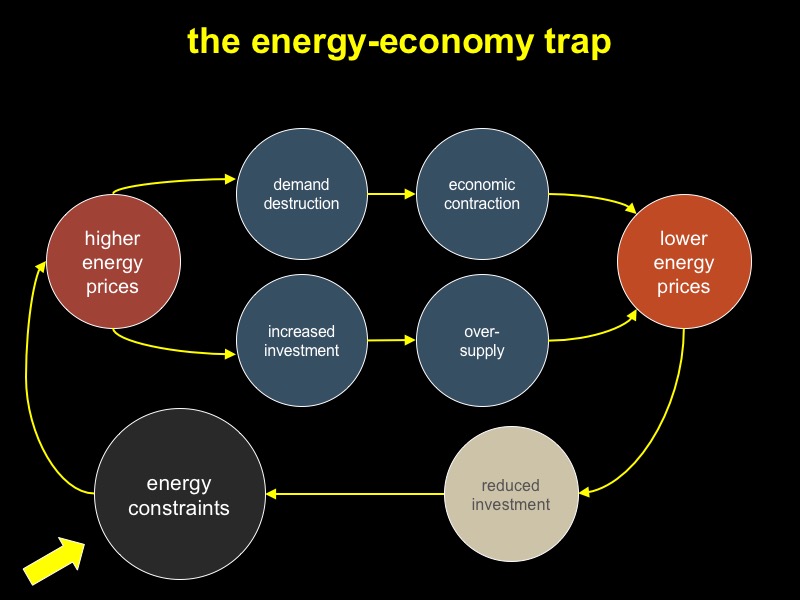

These resources also need high oil and gas prices and cheap, abundant investment capital. But as economist James Hamilton has shown, periods of high oil prices correlate with historic recessions and presumably helped cause them. Recessions reduce oil demand. This may mean that unconventional oil and gas booms are self-limiting.

The assumption of those who do not accept the peak oil reference frame is that when the market rebalances, currently depressed gas and oil prices will go up, leading to more drilling and more production. Subsequently, overall rates of oil and gas production will continue to increase for many years or decades, with prices rising incrementally to support this. But as we heard from Jim Murray and David Hughes, tight oil and shale gas wells are of variable quality, and choice drilling locations are limited in number. Production rates from these resources may already have maxed out regardless of price.

It is probably safe to say that most peak oil theorists assumed until recently that fossil fuel depletion would lead to steadily higher prices. But now different understandings of price dynamics are common. One possibility is that depletion will lead to increasing price volatility, as boom and bust cycles within the industry become more extreme. Another view is that prices may become permanently depressed due to suppressed demand. In either of these cases, investment and production would be constrained, leading to large portions of existing oil and gas resources remaining untapped.

The oil industry needs higher investment per unit of output: between 2009 and 2014, production costs rose at 10.9 percent per year, according to Steve Kopits of energy analysis firm Douglas-Westwood. This is due to the inherent challenge of producing non-renewable resources at ever-increasing rates: Once the low-hanging fruit are gone the next increment of production requires more effort, more technology, and more research and development. Recent industry cutbacks on investment are not because new prospects are cheaper; they’re simply due to low prices. Thus ebbing investment will inevitably mean declining production during the next few years.

The situation for coal is murkier: consumption is rising in India, the Philippines, and some other Asian nations, though China has apparently reached, or nearly so, its peak of consumption of this fuel, and global prices are depressed. Even though very large resources remain, if current prices persist it is entirely possible that most of those resources will stay put.

2. International policy, driven by citizen demand and leadership from key nations.

The results of COP 21 are in, and are mixed at best in the view of many climate activists. While the inclusion of a 1.5 degrees Celsius aspirational target was a welcome surprise, current national pledges to cut emissions put us on a path to 2.7 degrees of warming or more.

Nevertheless, the world is inexorably on the road to adopting carbon taxes, carbon caps, and other policy measures to reduce emissions and hence fossil fuel use. Not only are nations doing so, but also states (such as California and Vermont) and even localities like San Diego, hundreds of which have signed on to goals of achieving significant greenhouse gas reductions.

At the same time, climate activist organizations, notably 350.org, have mounted efforts to persuade investment funds to sell their shares in fossil fuel companies. So far, 350.org claims to have secured promises from funds with a total of $3 Trillion in assets to divest from coal, oil, and natural gas. Fiscal responsibility, it is argued, requires acknowledging that most of these companies’ assets are unburnable under the likely terms of existing and future emissions limits agreements. Of course, this divestment strategy works only with publicly traded companies (which amounts to about a tenth of the industry), not with state-owned companies like Saudi Aramco, Pemex, or Statoil.

Still, divestment campaigns do appear to be changing perceptions among the general public and among investors, sowing the opinion that fossil fuels really don’t have much of a future.

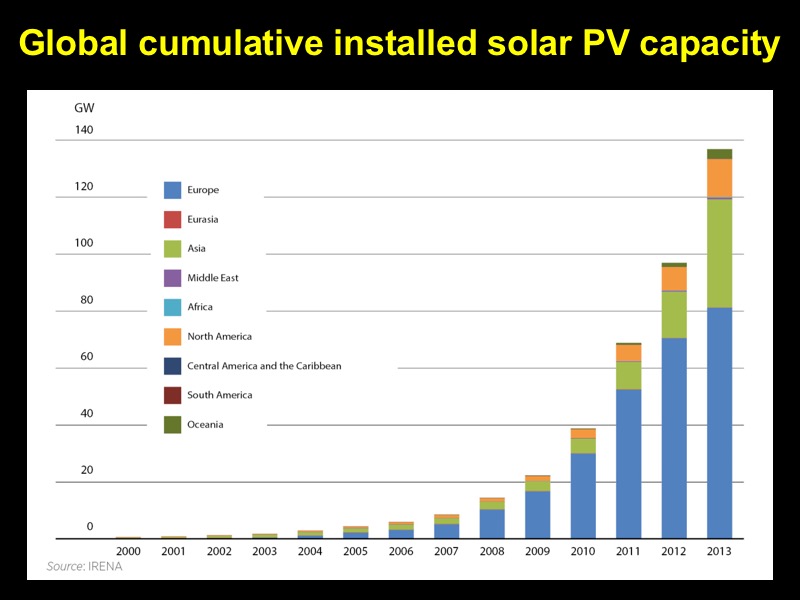

3. Massive deployment of renewable energy sources and other technological solutions.

Advocates of solar and wind power propose a massive deployment of these alternative energy sources to reduce fossil fuel use without attenuating the flow of energy to society.

The cost of solar and wind is falling and the rate of adoption is high, though not nearly high enough to avert catastrophic climate change. Since renewables mostly produce electricity, coal will be the fossil fuel impacted first and foremost. Then adoption of electric cars could reduce our oil consumption.

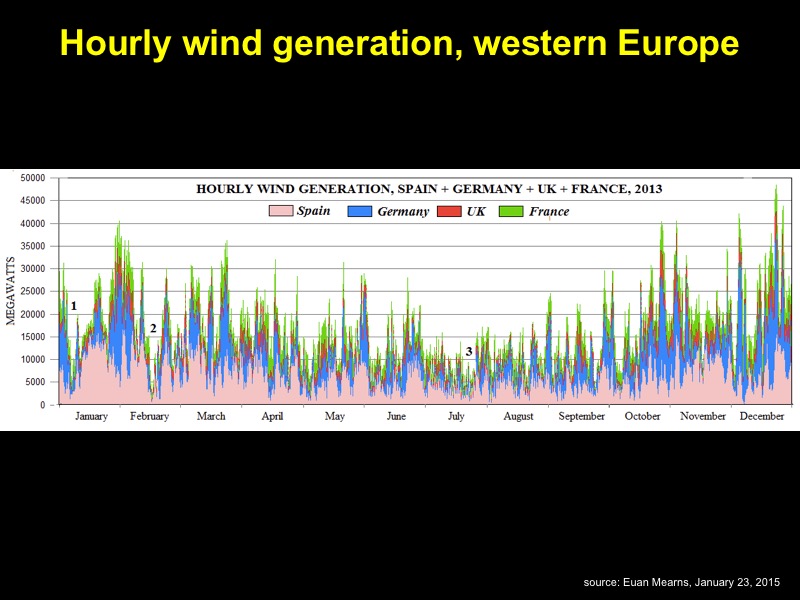

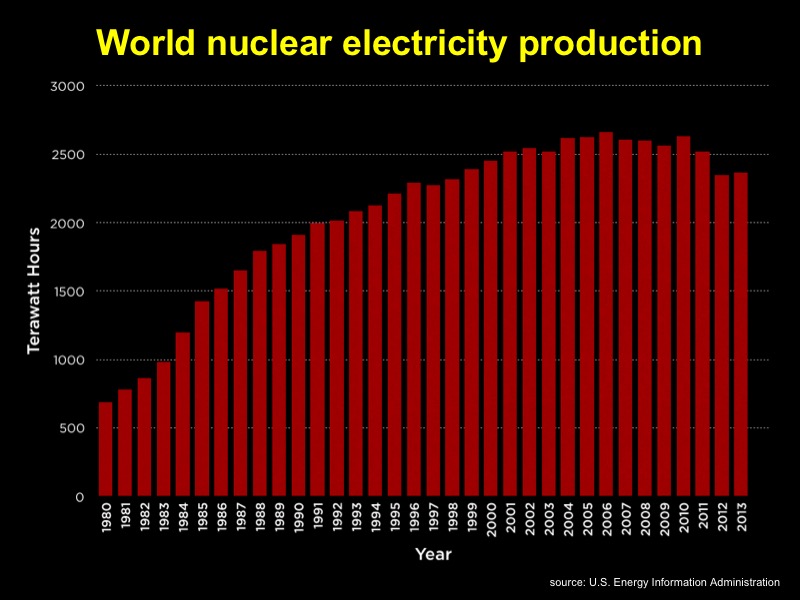

Some energy analysts say solar and wind are incapable of fully replacing fossil fuels in the time we have for the transition because they produce power intermittently; many of these analysts instead advocate a rapid deployment of nuclear power. New versions (modular mini-reactors, thorium reactors, fast breeders) are on the drawing boards and, if the promotional literature is to be believed, they will to be cheaper and safer than existing models.

However, nuclear power capacity is still expensive to build, and the nuclear waste problem is yet to be solved. Few nations are expanding their fleets of reactors, while the ongoing Fukushima crisis continues to highlight the risks and costs of existing nuclear technology. Tellingly, the nuclear industry seems incapable of delivering new plants on time and on budget. Given the expense and long lead-time entailed in plant construction, the nuclear industry may do well merely to build enough new plants to replace old ones that are nearing retirement.

Nevertheless, despite challenges with both renewables and nuclear, a major shift toward these energy sources is reflected in all but the business-as-usual IPCC scenarios.

4. Large-scale energy curtailment resulting from global economic contraction.

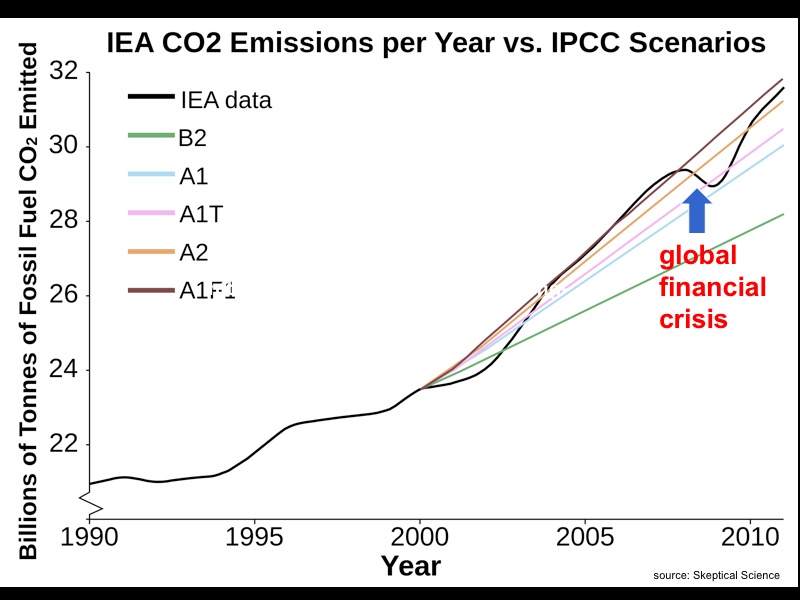

Among the lessons of the 2008 global financial crisis was that recessions result in falling energy demand and investment. In 2009 the oil price dove to $36, hundreds of energy projects were delayed, and carbon emissions dipped by 1.3 percent.

But the effect was short-lived. National governments and central banks quickly deployed quantitative easing, low interest rates, stimulus spending, and bailouts; some of these are still in place seven years later. The effects of these extraordinary efforts included rebounds in stock values and real estate prices, along with the inflation of asset bubbles, including one in the fracking industry. Oil demand and prices also recovered (until recently).

Some say when the next recession arrives, the same tactics can’t be deployed again at the same scale, or they won’t work as successfully. The notion that another de-leveraging recession might be on its way is supported by a study by McKinsey in 2014, which showed that total global debt last year had surpassed its 2007 level by $57 Trillion.

Peak oil theorists argue that depletion of the world’s top energy resource guarantees an endless energy-starved recession beginning at some point in the relatively near future, while climate scientists warn that extreme weather events will increasingly hammer national economies.

But peak oil and climate change are both elements within a larger dynamic described in the 1972 Limits to Growth scenario series, which explored the likely interactions between population growth, resource depletion, and environmental pollution. The standard run scenario, which a recent study confirms the world is following most closely, showed a peak and decline in world industrial output in the first half of the 21st century, followed by declines in food production and population. These trends of course imply a significant decline in energy use as well.

Discussion

From a climate perspective, our best-case future would likely be one in which world leaders negotiate global carbon caps, investment in fossil fuels is insufficient, and both of these developments together ensure reduced coal, oil, and gas production rates and an acceleration in renewables deployment, with the latter growing to replace fossil fuels seamlessly.

But such an outcome faces some impediments.

Even if solar and wind energy supplies could be increased sufficiently, our energy usage infrastructure would require major adaptation.

For example, either the cement production process would have to be completely redesigned, or society would have to learn to get by without concrete. The transport sector—notably trucking, shipping, and aviation—also poses hurdles to a no-carbon energy transition.

Also, solar and wind intermittency may present serious problems, depending on whose analysis you accept. If it does, then the cheapest and easiest renewable energy system to engineer would be one led by hydro, geothermal, and biomass, which do not suffer as much from variability. But because these sources do not have large potential for growth, a global energy system that relied primarily upon them would likely not provide nearly as much energy as we currently use.

Indeed, our biggest constraint to achieving a post-fossil energy economy is probably the assumption that we must continue industrial expansion and economic growth. The scale of energy use that we have gotten accustomed to, and that we insist upon expanding into the future, is vast and unprecedented. Economists and planners hate the idea of substantially reducing global energy use. But it is precisely the challenge of scale that poses the biggest hurdle to dealing with climate change.

Many analysts fudge the issue by appealing to decoupling—achieving more growth while using less energy. But according to a recent study by Wiedmann et al., past apparent evidence of decoupling is actually attributable to false accounting. So, apart from efficiency gains from phasing out coal and gas in the electricity sector, we probably can’t grow the economy more while using less energy.

This suggests world leaders should focus much more attention on how to maintain high levels of human development (which is not the same as economic growth) as energy supplies wane.

In summary

Fossil fuel limits might come from any of several directions. That would be good for the climate. But unless we are able to replace energy services from those fuels relatively seamlessly with energy services from alternative sources, we may have to figure out how to get by without economic growth. It might therefore be helpful for world leaders to begin now to examine how to manage the transition to a post-carbon and post-growth economy with the least negative impact to human welfare.