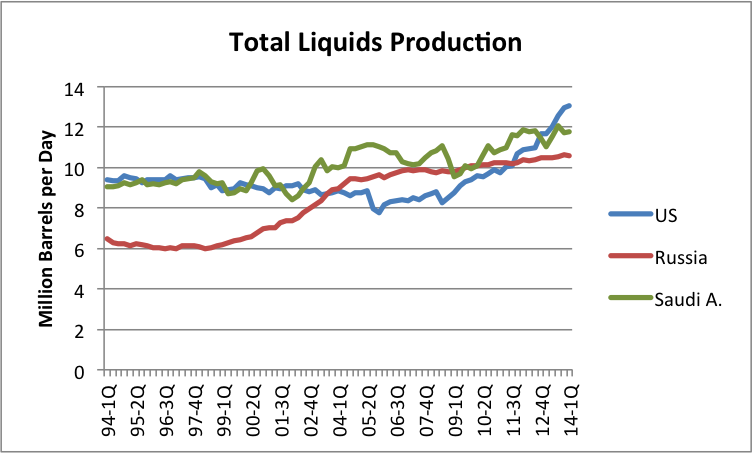

We frequently see stories telling us how well the United States is doing at oil extraction. The fact that there are stories in the press about the US wanting to export crude oil adds to the hype. How much of these stories are really true? If we believe the stories, the US is now the largest producer of oil liquids in the world. In fact, it has been the largest producer since the fourth quarter of 2012.

Figure 1. US Total Liquids production, including crude and condensate, natural gas plant liquids, “other liquids,” and refinery expansion.

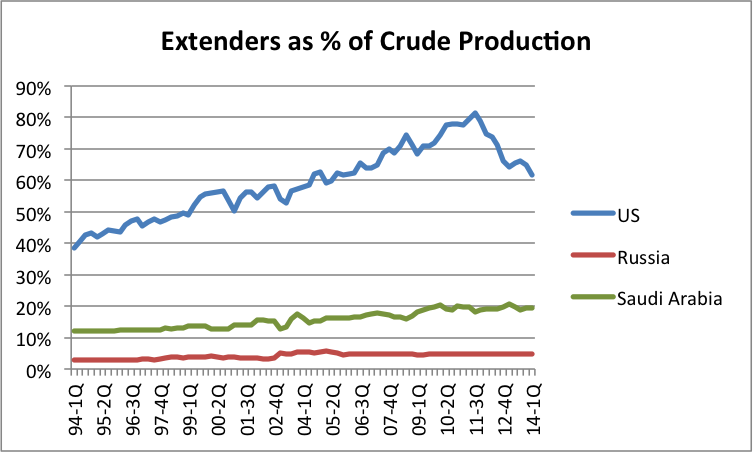

Oil “Extenders”

One of the issues is that a few years ago, the US created a new oil-related grouping, combining valuable products with much less valuable (lower energy content, less dense) products. Using this new grouping, the US was able to show much improved growth in total “oil” supply. The US EIA now calls the grouping “Total Oil Supply.” I refer to it as “Total Liquids,” a name I find more descriptive. Besides “crude and condensate,” the mixture includes “other liquids,” “natural gas plant liquids,” and “refinery expansion.”

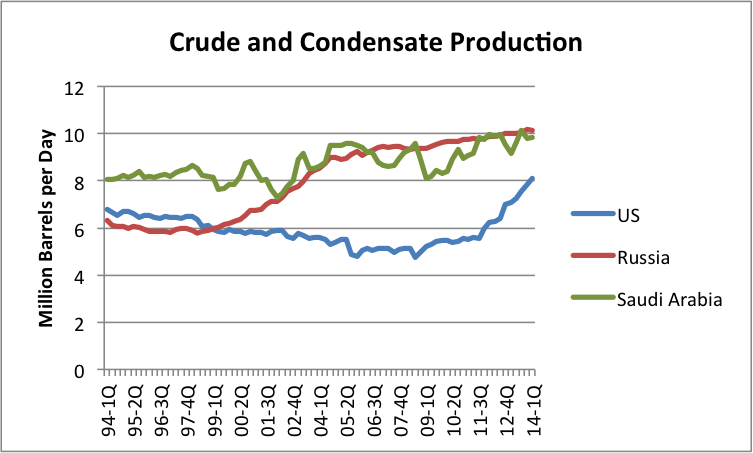

“Crude and condensate” is the original grouping. Often, it is just referred to as “crude oil.”

“Other liquids” is primarily ethanol from corn. If we produced coal-to-liquids, it would be in this category as well.

Natural gas plant liquids (NGPL) are the liquids that condense out of natural gas when they are chilled and compressed in the natural gas processing plant.

Refinery expansion occurs when a refinery breaks long chain hydrocarbons into shorter ones. The resulting products take up more volume, but don’t really have more energy content. In some ways, the process is like making whipped cream out of whipping cream–more volume, but not really more product. The new products tend to be more valuable–say, diesel and lubricating oil made from something close to asphalt.

The process of breaking (cracking) long hydrocarbon chains is a valuable service to those producing heavy oils, because it makes valuable products from crude that otherwise would not have been useful for most purposes. The cracking process uses natural gas. Because natural gas in the US is inexpensive relative to its price in most other countries, the US can perform this process more cheaply than other countries. Because of this, it makes financial sense for the US to import heavy crude oil and process it in this way, whether or not US citizens can afford to buy the finished products. (Cracking is not useful on very light oil, such as Bakken oil, since it has primarily short chains to begin with.) If US citizens can’t afford the finished products, they are exported to others.

Whether or not the US should be credited with this expansion of volume is somewhat “iffy,” since the process doesn’t add energy content. Quite a bit of the oil processed in this way uses imported oil, such as oil from the Canadian oil sands.

If we look at the base figure reported by the US Energy Administration, that is, “Crude and Condensate”(Figure 2), the US does not come out as well in original comparison (Figure 1).

The United States makes much greater use of extenders than do Russia and Saudi Arabia. If we calculate the ratio of extenders to the base (crude and condensate), the ratios are as follows:

Figure 3. Extenders as a percentage of crude oil production, based on EIA data.

Both Russia and Saudi Arabia have much lower ratios of extenders. For both of these countries, the extenders are Natural Gas Plant Liquids.

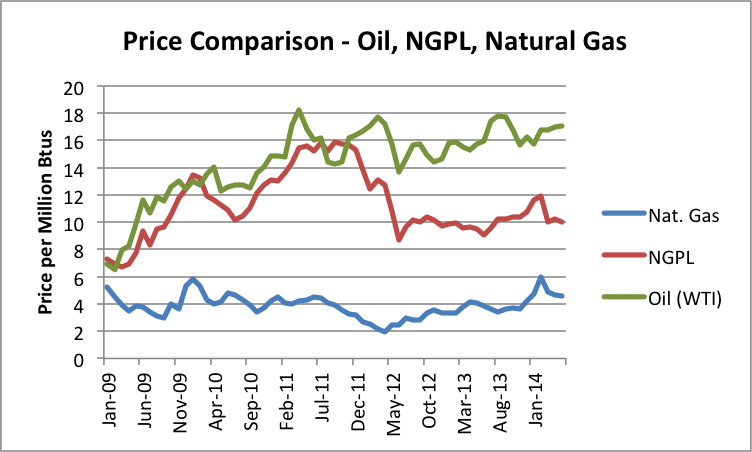

Natural Gas Plant Liquids (NGPL), have varied in price. For a while, the price was up with the price of crude, but as supply increased, the US price dropped during 2011 (Figure 4).

Figure 4. Price Comparison per Million Btu for Oil (West Texas Intermediate), Natural gas plant liquids, and natural gas, based on EIA data.

This drop in NGPL price occurred because the US market for at least some components of this grouping became saturated. With too much supply for demand, prices dropped. Excess ethane, for example, could be sold to be burned as natural gas, putting a floor under its price. As a result, recent prices seem to be influenced by changes in natural gas prices.

With the drop in NGPL prices, we hear more talk about the need for exports. We don’t really have use for all of the low value products that are being produced, other than to burn them as part of natural gas. Perhaps someone else does. If someone else does, it might get the price back up.

What is the Real US Trend in Production/ Consumption?

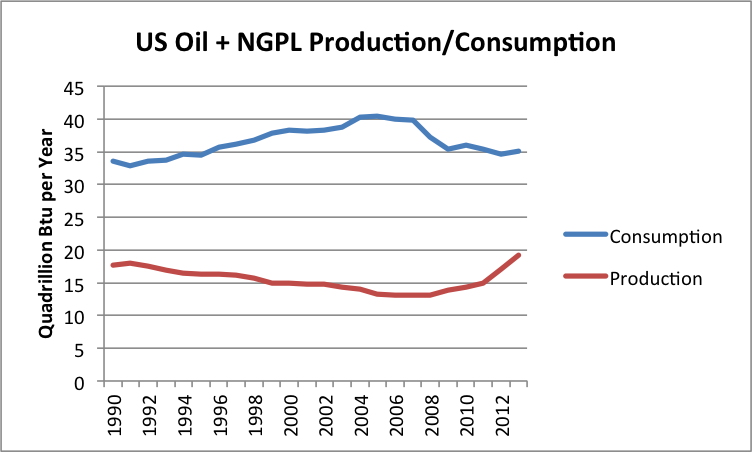

The US EIA makes fuel comparisons based on Btu energy content. This approach makes it easy to see how much of our fuel is US produced, and how much is imported (Figure 5).

Figure 5. Comparison of US production and consumption of oil plus NGPLs, based on EIA data.

Production is indeed rising, but it is still far below consumption–about 55% of consumption in 2013. Many articles make this situation confusing.

The emphasis in most news reports is the drop in imports–that is the difference between the blue line and the red line in Figure 5. If we look at the chart, though, we see that a big reason for the drop in imports is a drop in consumption, with the big step down coming in 2007 and 2008. Oil use is associated with jobs. It takes oil to make and transport goods. Also, workers with good jobs can afford cars and the oil to operate their cars. If they remain students forever, they can’t afford cars.

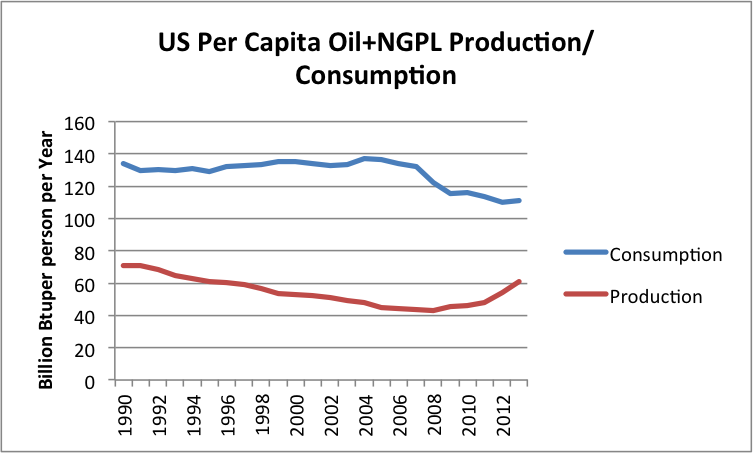

A person can better see the drop in consumption by looking at consumption on a per capita basis.

Figure 6. US per capita oil and Natural Gas Plant Liquids production and consumption, based on EIA data.

If prices don’t fall, consumers don’t feel the effect of more production. What they do feel the effect of is falling consumption-the top line. Young people especially have been finding it hard to get good paying jobs. With all of their student loans, it is hard to be able to afford to get married and buy a house. This holds down demand for new homes, and all of the things that go into new homes.

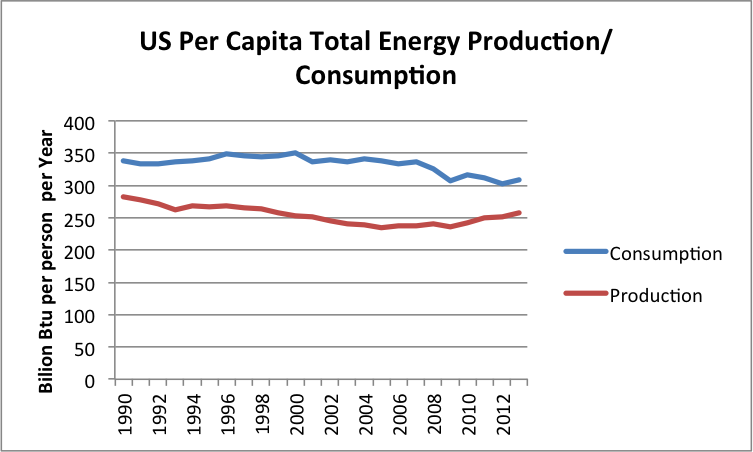

If we look at total per capita energy production and consumption in the US, we see even more of this trend. While production per capita is rising, an even bigger issue is falling consumption.

Figure 7. Total per capita energy production and consumption for the US, based on EIA data.

US per capita energy consumption has been dropping since 2000. 2000 is the year of peak US employment, as a percentage of the total population.

Figure 8. US Number Employed / Population, where US Number Employed is Total Non_Farm Workers from Current Employment Statistics of the Bureau of Labor Statistics and Population is US Resident Population from the US Census. 2012 is partial year estimate. (Sorry, not updated.)

With a smaller percentage of the US population employed (and lagging salaries for those employed), US consumers cannot afford to buy as large a quantity of energy products. Rising US oil production is not really helping US consumers, because at its high price, we cannot really afford it.

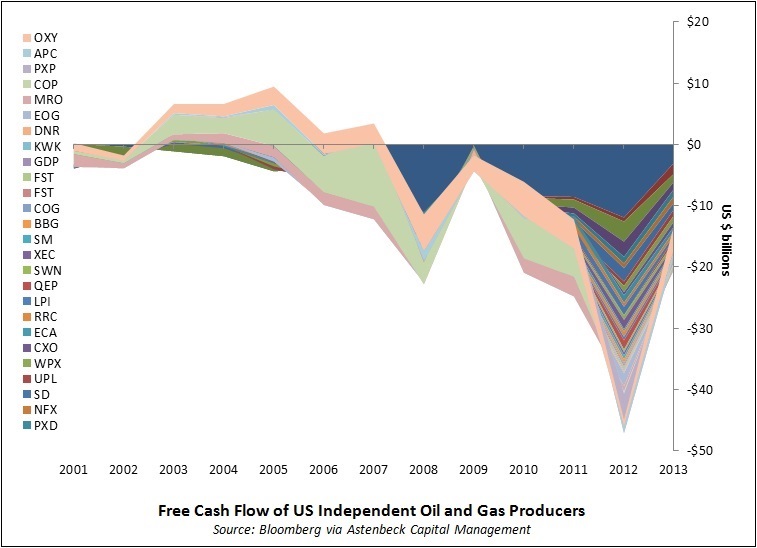

Rising oil production has not brought down oil price, making it more affordable. In fact, the situation is the reverse–high prices are needed for today’s oil production. It is questionable whether today’s prices are even high enough. Oil companies have to keep adding debt, to keep extracting oil. The EIA recently wrote an article about the situation called, As cash flow flattens, major energy companies increase debt, sell assets. Steven Kopits shows this chart of cash flows for Independent Oil Companies in a recent post.

Figure 9. Image by Steven Kopits showing Free Cash Flow of US independent oil and gas producers, from Platts Guest Blog.

With negative cash flows, companies have to keep increasing their debt levels–something that eventually becomes impossible.

When those producing the oil see that US oil prices are at times not as high as world oil price (Brent), they hope that selling their crude to world export markets, they will be able to get higher prices for their crude. If they are successful, there will be less crude available sold to US producers, perhaps raising the price of this crude sold in this country as well. The net impact may be higher prices for US consumers, making the US consumers even less able to afford the oil products.

Energy Growth is Needed for Economic Growth

There is a close tie between energy consumption and economic growth. Perhaps my statement “Energy growth is needed for economic growth,” in the header is a little too strong. Perhaps if energy consumption is flat, with the benefit of technological progress and efficiency changes, there can still be economic growth. There is definitely a connection, though. Energy of the right type is needed for every process we can think of–getting to work, shipping goods, operating our computers, heating metals when they are refined.

The problem comes when what we are facing is shrinkage of energy consumption, over and above what can be accommodated by technological progress and efficiency. Figure 7 hints that this is already happening. Then we have danger of a collapsing financial system, as the low energy consumption growth pushes the economy toward contraction. The economy has been held together since 2008 with quantitative easing and zero interest rates. The plan has been to allow consumers more income to spend, by keeping interest rates artificially low. I heard an excellent presentation on this subject recently called Global Financial System on Life Support by Roger Boyd.

Conclusion

I wrote a post recently called The Absurdity of US Natural Gas Exports. The situation with exports of crude oil is not quite as absurd. The issue is that current oil refineries are not configured for the influx of very light oil. Many of them are busy “cracking” long hydrocarbon chains, often using imported oil as their energy source. If US oil producers have the option of selling their crude oil abroad, perhaps they can get a higher price for it. If US oil producers can get higher prices for their oil, this may very well filter through to higher oil prices for US consumers, and less oil consumption by US consumers, but this is not the concern of oil companies.

A major concern with falling per-capita energy consumption it that the financial system may soon reach limits where it is stretched beyond what it can stand. The economy needs energy growth to grow, but the economy is not getting it.

US drilling teaser image via shutterstock. Reproduced at Resilience.org with permission.

US drilling teaser image via shutterstock. Reproduced at Resilience.org with permission.