NOTE: Images in this archived article have been removed.

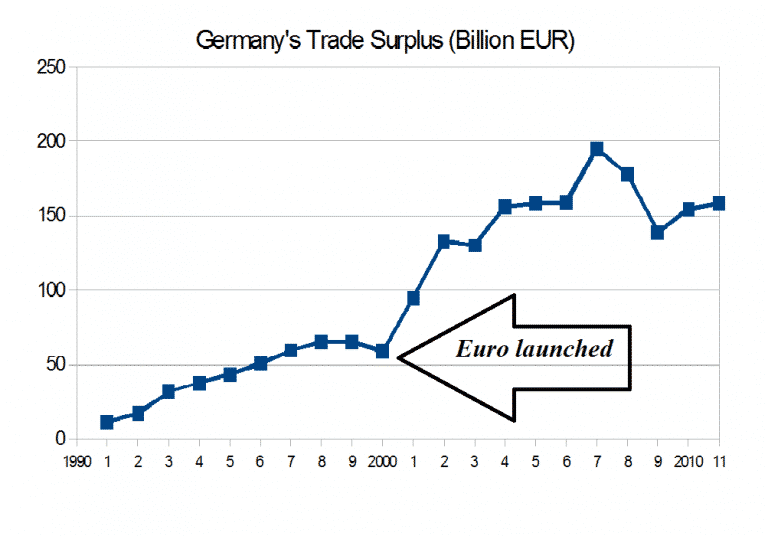

Any country that joins the single European currency immediately gives up control of its monetary policy and its exchange rate. With exchange rate risk seemingly removed, interest rates in many of the countries deemed previously to be of higher risk such as Portugal, Italy, Ireland, Greece, and Spain (PIIGS), fell significantly and foreign investment inflows increased substantially. With much lower interest rates and large incoming flows of foreign investment these countries experienced rapid economic growth. Without the ability to devalue their currencies against those countries reducing unit costs faster than themselves, such as Germany, their trade deficits widened. The net result of the Euro was to make Germany more competitive, as the Euro traded lower than the Deutschmark would have, but higher than the previous PIIGS currencies. Without the Euro, and the large investment flows into these countries, such a widening trade deficit would have forced a crisis much earlier.

As the financial crisis of 2007-2009 took hold investors became more and more conscious of any risks to their investments, and investment funds started to exit the riskier European countries. The scale of the movements forced up local interest rates, and removed significant funding from the economy. The impacts of these changes were exacerbated by the number of financial and property bubbles that had been produced by the previously low interest rates and large financial inflows. The collapsing world economy also reduced exports to other countries, adding to the trade balance issues.

The end result was a collapse in the economies of PIIGS and the requirement for extensive monetary and financial restructuring activities provided by the European Union and International Monetary Fund to forestall outright defaults. These actions have not remedied the situation though; rather they have only delayed the bigger crisis, at the expense of large reductions in government expenditures and general living standards. In essence, the general population of these countries is being used to protect the heavily exposed European banks and other major investors. These countries would have done much better to leave the Euro zone, take back control of their monetary and foreign exchange policies, and devalue their currencies to regain competitiveness. This would have created a short period of severe pain, beyond which recovery could commence, compared to the current long drawn out road to penury. A good example of this penury is the Greek Health Minister’s statement that cancer treatment “is not urgent unless in the final stages”1.

In the 1990′s the very same process was played out in Argentina, which put in place a fully convertible fixed exchange rate with the United States dollar to defeat the hyperinflation of the 1980′s2. For most of the 1990′s it worked, as foreign investment poured in and interest rates came down, and Argentina showed the same rapid growth that the five European countries were to show in the following decade. Then late in the 1990′s a series of financial crises caused foreign investors to pull money out of the country. This placed great strain upon the economy and the ability of the central bank to maintain the fixed convertible exchange rate. A strong appreciation of the US dollar caused the pegged Argentinian currency to also rise, making Argentinean exports less price competitive. This was exacerbated by a Brazilian currency devaluation, the destination for nearly 30% of Argentina’s exports2.

The end result was a major currency devaluation, and sovereign debt default, by Argentina. By both devaluing, and defaulting on its external debt, the country was able to set the stage for a vigorous recovery through the following decade2. This example was followed by Iceland during the 2007-2009 financial crisis as it refused to pay the foreign depositors of its banks and severely devalued its currency. Again, growth was restarted after a very painful, but short, crisis period3. Both the Argentinean and Icelandic governments were forced to act in the interests of their people, rather than the financiers, by extensive public protests and pressure. In Iceland the intervention of the president to force a referendum that reversed the decisions of the politicians was also required. In PIIGS the interests of the financiers and European Union were put ahead of those of the citizens. Another parallel case is that of the countries caught in the Asian financial crisis of 1998, where the one country which implemented exchange controls and banned offshore currency trading (Malaysia) managed to ride out the storm while Thailand, Taiwan, and South Korea had to submit to significant economic and financial liberalization in exchange for International Monetary Fund lead rescue packages4,5,6.

The same script of unregulated capital flows rushing into a country, causing asset bubbles, supporting untenable current account deficits, and causing other economic and financial problems, has been repeated many times. When sentiment changes a crisis ensues as many of the foreign investors rush for the door at the same time, exacerbated by any attempts to support fixed exchange rates. Malaysia, Argentina and Iceland have shown that the neo-liberal beliefs are not sacrosanct, and in many cases are simply self-serving myths. Capital controls can be put in place, debts can be defaulted on, financiers can be punished for their risky behaviors, and the sky will not fall.

What does all this have to do with the issues of climate change, peak resources and ecological destruction? As these issues become a greater and greater impediment to the functioning of modern economies and their financial systems the flow of investment monies running from one chaotic system to another will have to be corralled to protect economies and provide the relative stability required for a successful transition to a sustainable future. In addition debts, which are a call upon future output that will not take place, will need to be renegotiated to allow for an equitable sharing of pain between the rich and the rest. Thus, exchange controls, debt restructurings, etc., will become a thing of our future. The assumptions of effortlessly moving money and wealth around the world will become a thing of the past, just as the physical world will shrink so will the financial one. Local investments, and investments in real productive assets like a productive farm, may prove to be much more resilient in the future crises than investments in financial assets in far-away places.

References

1. Faiola, Anthony (2014), Greece’s prescription for a health-care crisis, The Washington Post. Accessed at http://www.washingtonpost.com/world/greeces-prescription-for-a-health-care-crisis/2014/02/21/adabb7ac-8db1-11e3-99e7-de22c4311986_story.html

2. Zaza, Rosanna (2010), Argentina 2001 – 2009: From the Financial Crisis to the Present, Amazon Digital Services.

3. Jonnson, Asgeir (2010), Why Iceland?: How One of the World’s Smallest Countries Became the Meltdown’s Biggest Casualty, McGraw Hill.

4. Lim, Mah-Huih & Goh Sooh-Khoon (2012), How Malaysia Weathered The Financial Crisis: Policies and Possible Lessons, The North-South Institute. Accessed athttp://www.nsi-ins.ca/wp-content/uploads/2012/09/2012-How-to-prevent-the-next-crisis-Malaysia.pdf

5. Gidwani, Krishna (n/a), Korea and the Asian Financial Crisis, Stanford University. Accessed athttp://www.stanford.edu/class/e297c/trade_environment/global/hkorea.html

6. Nanto, Dick (1998), CRS Report to Congress: The 1997-98 Asian Crisis, Federation of American Scientists. Accessed at http://www.fas.org/man/crs/crs-asia2.htm

{kind=link}

{kind=link}