Global gas flaring–the burning of natural gas associated with oil extraction processes–remains stubbornly high. We examine the determinants of gas flaring in three prominent cases: Russia and Nigeria as the two largest emitters of flare gas, and the United States as a rapidly expanding newcomer to the club.

Introduction

When you drill for oil, you also get gas. In an ideal world this associated gas would be sold to consumers, or it would be used to generate power and then resold as electricity. But this requires costly investment into pipelines, power plants, and other infrastructure. Therefore, in practice, some oil producers opt to sell the oil and burn the gas. This is known as gas flaring. Every year, approximately 140-150 billion cubic meters (bcm) of natural gas is flared into the atmosphere. According to calculations by the World Bank, that’s equivalent to three quarters of Russia’s gas exports, or almost one third of the European Union’s gas consumption.

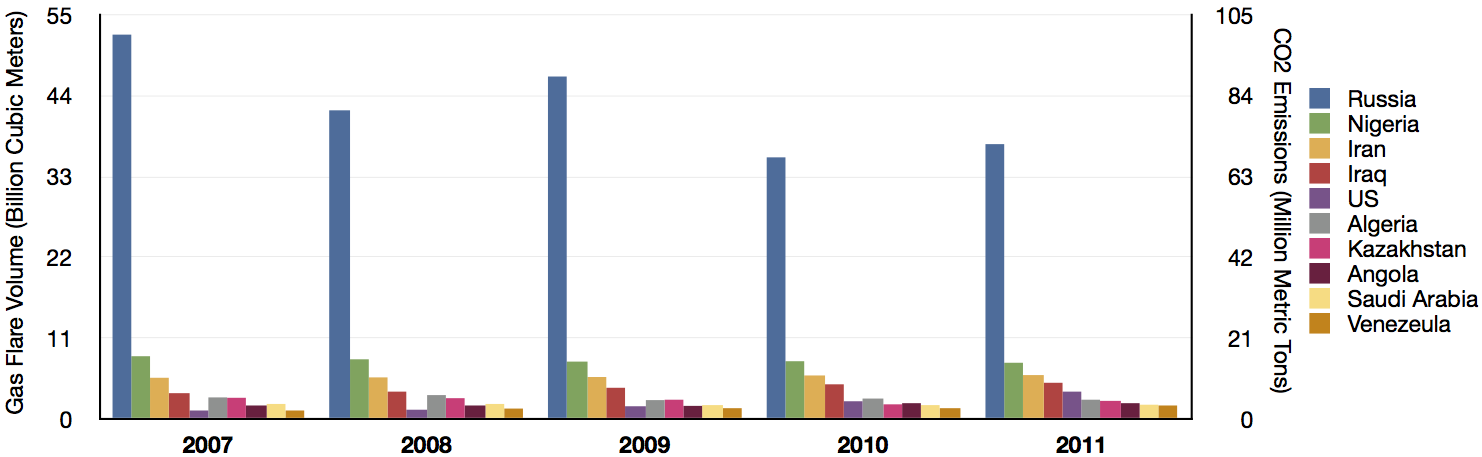

Figure 1: Volume of gas flared (left axis) and equivalent CO2 emissions (right axis). Source: World Bank data, recalculated by authors from BCM to MMT.

Gas flaring is regrettable from an economic viewpoint because a valuable resource is wasted. It is even more regrettable from an environmental perspective because 140-150 bcm of flared natural gas translates into 270-290 million tons of C02 emissions per year. Accounting for roughly 1% of global carbon emissions, gas flaring is only a minor contributor to climate change. Even so, the practice is highly deplorable because no economic wealth and/or human welfare is generated in the process.

Global trends

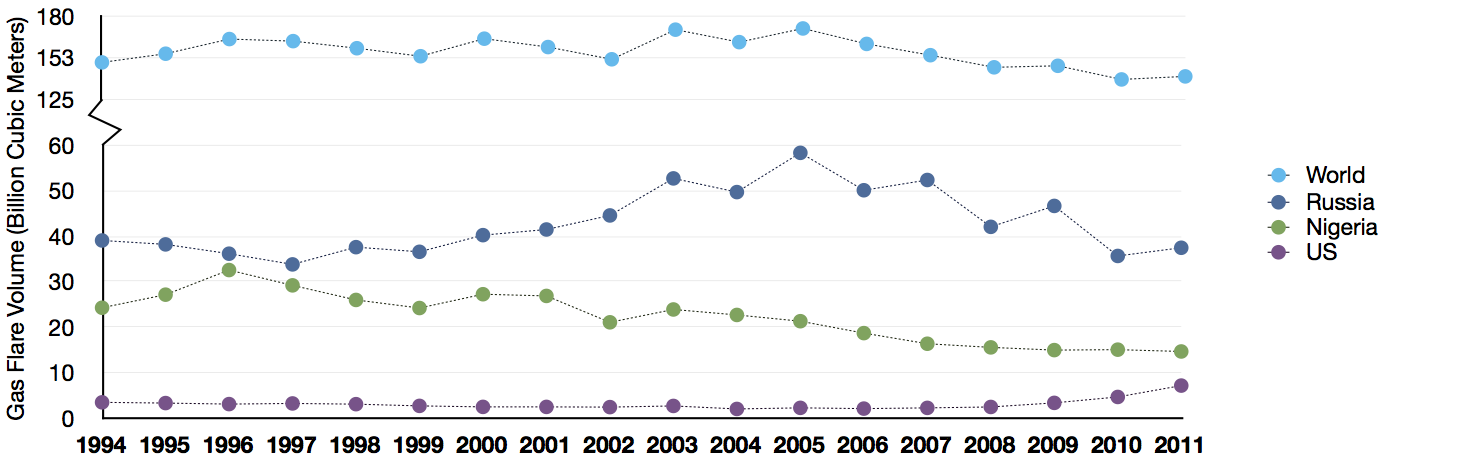

While global gas flaring has declined, albeit modestly, in recent years, the trend seems rather weak and far from irreversible. Gas flaring fell by around 20% from 2005 to 2010, only to increase again from 138 bcm in 2010 to 140 bcm in 2011 (the latest year for which data is currently available). Be that as it may, the total amount of gas flared globally remains broadly in line with 1994 levels.

Figure 2: Gas flaring trends. Sources: NOAA (1994-2006); World Bank (2007-2011).

So what explains the continued prevalence of gas flaring in recent years? Of the top-five flaring countries, let us examine Russia and Nigeria as the two largest emitters of flare gas, plus the United States as a newcomer to the group of the world’s largest emitters (the US is now the fifth largest flaring country, after Iran and Iraq, having displaced Algeria in 2011).

Russia

Gas flaring is an embarrassment to Russian leaders. As the then President Dmitry Medvedev stated on 12 November 2009,

“One of the most glaring examples of ineffective energy resource use is the flaring of gas extracted alongside oil. This pollutes the environment and sends tens of billions of rubles up in smoke.”

Political will to tackle gas flaring has contributed to a significant decline in Russian flaring volumes since 2005. Nevertheless, Russia continues to flare more gas than any other country in the world.

A first reason for this has to do with the geography of Russian oil and gas resources. Russia holds the world’s second largest natural gas and ninth largest crude oil reserves,[1] but most of its oil and gas fields are in remote and hard-to-access areas. Additionally, these fields are often very far away from one another. As a result, long pipelines are needed for access to both domestic and international markets. So when the resource exploited is oil, building an additional pipeline for associated gas, or a gas firing power plant plus power lines, often makes little or no commercial sense.

Vintage photo of gas flare in the Siberian taiga. Source: Copper Kettle.

Another reason is straightforward economics. Due to the easy availability of natural gas and an explicit policy of subsidization, domestic gas prices are extremely low in Russia. Since commercializing associated gas tends to be more expensive than producing natural gas,[2] flaring it is often the cheapest option. Pipelines are indeed expensive to construct. According to an estimate by the Russian investment company Finam, in Siberia a kilometre of pipeline costs about $1.5 million. Unsurprisingly, infrastructural investment to exploit associated gas has generally been outpaced by growth in oil production.

A third reason has to do with market structure. The decentralization of the Russian petroleum sector in the 1990s fractured existing links between oil producers and gas processing companies. Since then, oil producers have found themselves increasingly detached from gas collection, transportation, and utilization networks. Unsurprisingly, this sharp division has increased the incentive to flare rather than to produce.[3]

Fourth and finally, the market structure of the Russian energy sector is anti-competitive: Gazprom, the majority state-owned natural gas company, holds a clear monopoly over the national gas transportation network. So, while in theory one might expect international market prices to set an incentive for the commercialization of associated gas, an oil producer looking to do this would first have to negotiate a fee for the utilization of the pipeline. Needless to say, many Russian oil producers decide that it makes better economic sense to simply flare their gas and sell their oil.

Nigeria

Starting from a very high baseline, gas flaring has more than halved in Nigeria since 1996. Despite this, Nigeria remains the second largest flaring country in the world and emits around $1.8 billion worth of gas annually.[4] But what is more surprising than the eye-popping economic loss is the fact that so much gas is wasted despite the country’s rampant energy poverty: The entire Nigerian population uses little more grid power than the area immediately surrounding Tokyo’s Narita airport.

Like Russia, Nigeria has significant hydrocarbon resources. But these are far more accessible, with most of them located in the Niger Delta. So why is the outcome—wasteful gas flaring—identical, despite dissimilar geographical circumstances?

Satellite picture of gas flares in the Niger Delta. Source: NOAA.

The answer is that Nigeria is deeply afflicted by what economists call the resource curse: countries with a rich resource endowment are often less well governed, have lower growth rates, and are less socially developed than resource-poor countries. In the Nigerian case, one manifestation of the resource curse is seen in poor national governance: the Nigerian administration is often more concerned to cater to demands from international buyers of commodities (mainly oil) than to meet the needs of its citizens (for example, providing affordable gas-fired power).

This is not to deny that, due to extensive consumption subsidies, Nigeria still has one of the lowest pump prices for gasoline in Africa (44 US cent per liter in 2010/11).[5] And this is only the official price. The effective price for illegal fuel, such as oil stolen from pipelines in the Niger delta, is likely to be even lower. Even so, many of Nigeria’s impoverished citizens are still not able to afford oil, and instead rely on biomass. Most businesses and those Nigerians who are wealthy enough to do so burn diesel or petrol on privately owned generators, rather than opting for gas which is relatively expensive and difficult to handle. Given the sorry state of public utilities, private diesel generators are the workhorses of Nigerian power generation.

In short, a critical lack of political goodwill and institutional capacity prevents gas from being harnessed in a way that might benefit and improve the welfare of the population. But fuel poverty in an oil and gas-rich country like Nigeria is just one of the ironies of the resource curse. Weak institutions and poor governance also make Nigeria less attractive as a destination for foreign direct investment and as a source of Liquefied Natural Gas (LNG) for international markets. In July 2013, for instance, Nigeria’s maritime security agency blocked all LNG exports for 17 days, despite the fact that the blockade had been declared illegal by a federal court.[6]

Lastly, although flaring has been legally banned in Nigeria since 1984, measures to enforce the ban have been lackluster. NGOs and environmental organizations, for instance, point towards the fact that fines for flaring are much too low per cubic meter to deter companies from burning gas. Under such circumstances, there is little incentive for entrepreneurs to make the huge infrastructural investments required for the commercialization of gas. Gas flaring, in this context, makes perfect sense from a business point of view. It’s simply one aspect of Nigeria’s dysfunctional petroleum sector, which is rife with distributional inequality and tragic energy wastage.

United States

The amount of gas flared in the United States has more than doubled since 2000, primarily due to growing flaring volumes in Wyoming and, most recently, North Dakota. Together, Wyoming and North Dakota now account for more than half of the gas flared in the United States. This is despite the fact that the US is the biggest market for natural gas in the world, with its domestic consumption amounting to over a fifth of global demand. So what explains this increasing gas wastage in America?

As in the Russian case, the key drivers are basic economics and resource geography. Mainly due to the shale gas boom, the US overtook Russia in 2009 as the world’s biggest producer of natural gas. The gas glut in the US has depressed domestic prices, making the commercialization of associated gas relatively less attractive. So, as in the Russian case, it is usually more cost effective to flare than to produce.

The other key reason is resource geography. Infrastructure to transport, process, and utilize associated gas has not grown in line with US oil production. The most striking example of this comes from North Dakota. Flaring there increased sevenfold over the past decade (2000-2010) and more than doubled from 2010 to 2011 (the latest year for which data is available), mainly due to increasing tight oil production. In fact, North Dakota advanced from being the ninth largest state producer of oil in 2006 to the second largest state producer in 2012 (after Texas and before Alaska).

Table 1: Gas vented and flared in key jurisdictions, million cubic feet. Source: EIA.

Much like in Russia, long and expensive pipelines would be required to transport associated gas to the primary domestic consumption markets (California, Florida, Louisiana, and so on), which are all very far from North Dakota. Aside from the sheer cost involved, it would take many years if not decades to build the infrastructure necessary to commercialize gas from places like North Dakota.

Nighttime view of North Dakota. Source: NASA Earth Observatory.

An additional problem is that the tight oil industry is highly fugacious. To put it bluntly, a lot of holes are drilled over a vast area during a short period of time, because production is subject to a high depletion rate. As a result, the industry moves on swiftly from one play to the next. The pattern is fairly unpredictable, and this means that US tight oil production is a moving target. Therefore, planning the appropriate infrastructure for the commercialization of associated gas is a tall order.

Bottom Line

To explore the determinants of gas flaring, we have outlined three prominent cases: Russia and Nigeria as the top two flaring countries in the world, and the US as a rapidly expanding newcomer to the flaring club.

The specific economic, geographical, and institutional reasons that underpin flaring are quite diverse. Sometimes, as in Russia, associated gas from oil fields is hardly needed locally and markets can rely on cheaper gas from dedicated gas fields. Sometimes, as in Nigeria, economic underdevelopment and dysfunctional institutions lead to a situation where the local economy cannot absorb associated gas, while traders can source their liquefied natural gas more cheaply and more efficiently from other countries. Sometimes, as in the United States, a sudden glut makes it difficult to immediately commercialize flare gas from remote regions.

Ultimately, the underlying cause is always the same: an oversupply of associated gas in a place or at a time where the demand for gas is too low and commercialization is too difficult. This points us back to the wider phenomenon of the resource curse: especially in developing countries, resource abundance is often not a blessing but a curse. While the resource curse is largely about socioeconomic development and institutions, fuel abundance comes with serious environmental challenges, especially when we consider climate change, and it often confines countries to carbon intensive developmental pathways —what Friedrichs and Inderwildi call the carbon curse.[7]

Data Sources

Datasets on gas flaring are subject to significant variation, due to inconsistencies in estimation methodology and shortcomings in measurement. As the safest bet, our analysis is largely based on the latest data from the World Bank. The World Bank data is based on measurements by the US National Oceanic and Atmospheric Administration, which relies on satellite observations. A supplementary flaring database is available from the Energy Information Administration.

References

[1] BP (2013) Statistical Review of World Energy, June 2013.

[2] PFC Energy (2007) Using Russia’s Associated Gas, Washington, DC: PFC Energy.

[3] Julia S.P. Loe and Olga Ladehaug (2012) Reducing gas flaring in Russia: gloomy outlook in times of economic insecurity, Energy Policy 50: 507–517.

[4] See Aminu Hassan and Reza Kouhy (2013) Gas flaring in Nigeria: analysis of changes in its consequent carbon emission and reporting, Accounting Forum 37 (2).

[5] GIZ (2012) International Fuel Prices 2010/2011, Bonn and Eschborn: Deutsche Gesellschaft für Internationale Zusammenarbeit.

[6] Xian Rice (2013) Nigeria maritime agency extends gas blockade, Financial Times, 9 July 2013.

[7] Jörg Friedrichs and Oliver Inderwildi (2013) The carbon curse: Are fuel rich economies doomed to high CO2 intensities?, Energy Policy 62, forthcoming.

{kind=link}