On January 23, 2012, Chesapeake Energy announced that it would curtail drilling in shale gas plays in the United States. Subsequently, other operators have followed suit. While the outcome of this announcement is unclear, it is a signal that the industry is in distress. One can argue that this distress stems from a lack of discipline as market price began to decline.

After gas prices collapsed in mid-2008, U.S. operators continued to drill as if price did not matter. Many reasons were given to justify the economics of ongoing activity including to hold acreage by production, to fulfill contract obligations to build new pipelines, and since well economics remained favorable at lower prices because of forward hedging. Now, with gas prices below $2.50 per thousand cubic feet (mcf), an adjustment in producer behavior is overdue. Despite statements that shale gas is a profitable venture at low gas prices, it is now clear that the reality has imposed limits on these claims.

Also on January 23, the Energy Information Administration (EIA) released its Annual Energy Outlook 2012 (early release overview). It projects that gas supply will exceed consumption and the U.S. will become a net exporter by 2021. The agency also forecasts gas prices to remain below $5.00 per thousand cubic feet (mcf) until 2022.

In his State of the Union address on January 25, the President stated that the United States has 100 years of natural gas supply. While these events are not related, they reflect the dominant view among analysts that shale gas has fundamentally changed supply and price for the foreseeable future. The purpose of this analysis is to show that there may be an alternate perspective.

U.S. Shale Plays

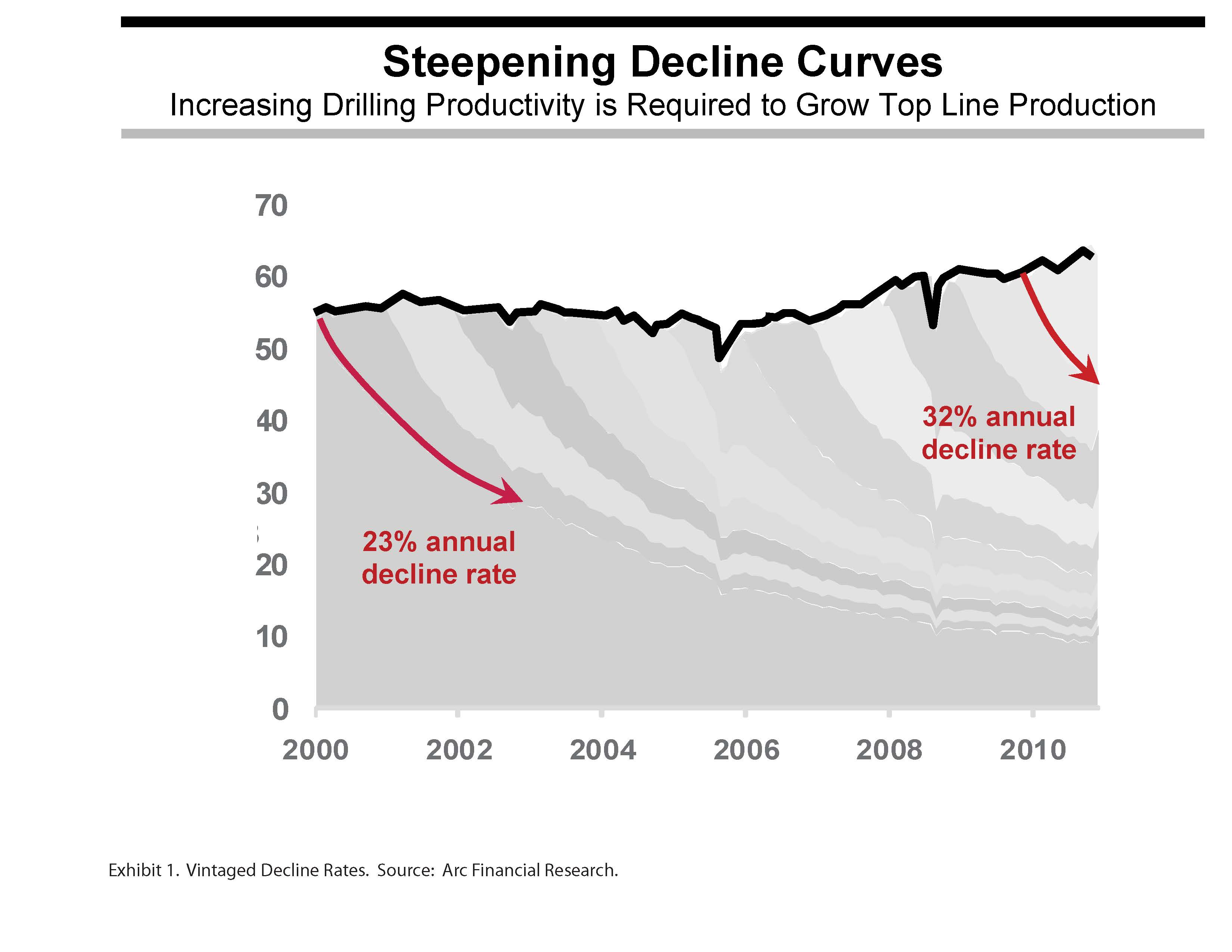

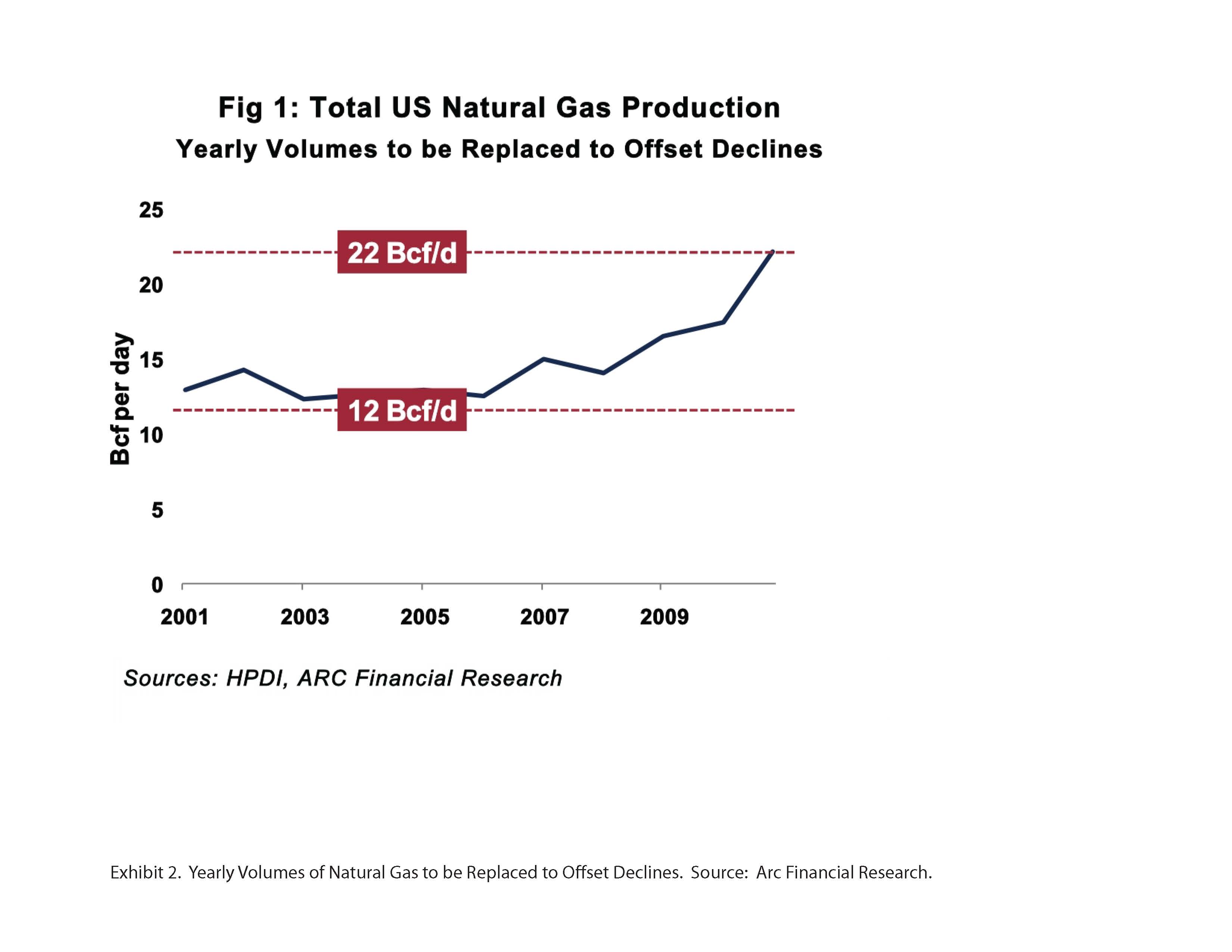

The advent of shale plays provided an important new source of gas. Yet this new supply is characterized by high decline rates which means that wells must be continuously drilled to maintain supply. In 2001, the U.S. natural gas decline rate was about 23% and the annual replacement requirement was 12 Bcf/d when total consumption was 54 Bcf/d. Today, the decline rate is estimated to be 32% and increased consumption of gas means that approximately 22 Bcf/d must be replaced each year (Exhibits 1 and 2).

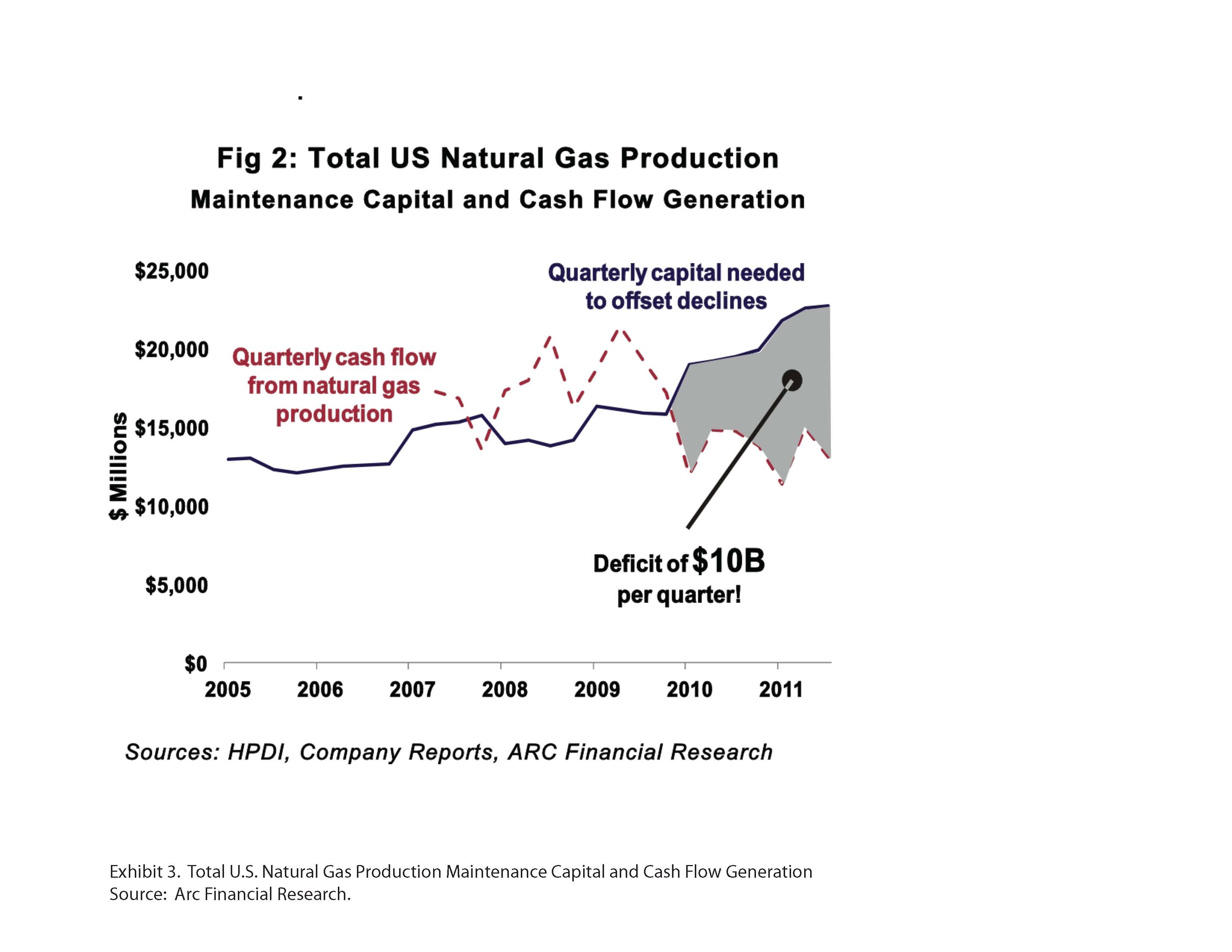

According to ARC Financial Research, $22 billion per quarter is needed to maintain domestic gas supply based on analysis of the 34 top U.S. publicly traded producers. Cash flow for those companies is $12 billion per quarter so there is a $10 billion quarterly cash flow deficit (Exhibit 3). The important factor here is that on a whole there are no retained earnings, and historically growth stems from retained earnings. Without retained earnings, companies must borrow money or sell assets into joint venture agreements to raise cash in order to drill.

While the continued drilling has been funded by debt, share offerings and joint venture agreements thus far, the trend is unsustainable given the steep decline in prices, despite some favorable hedges. Drilling, therefore, must decrease in order to shrink the present over-supply and so that prices can rise.

U.S. shale plays share many characteristics with the gold rushes of the nineteenth and early twentieth centuries. Both phenomena result from extreme promotion. Anyone can join. Every participant believes that they will get rich. Great amounts of capital are destroyed as entrants try to get a position. The bonanza is exhausted sooner than most expected (Andreoli, 2011) and few profit in the end except for the vendors that serve participants.

For several years, we have been asked to believe that less is more, that more oil and gas can be produced from shale than was produced from better reservoirs over the past century. We have been told more recently that the U.S. has enough natural gas to last for 100 years. We have been presented with an improbable business model that has no barriers to entry except access to capital, that provides a source of cheap and abundant gas, and that somehow also allows for great profit. Despite three decades of experience with tight sandstone and coal-bed methane production that yielded low-margin returns and less supply than originally advertised, we are expected to believe that poorer-quality shale reservoirs will somehow provide superior returns and make the U.S. energy independent. Shale gas advocates point to the large volumes of produced gas and the participation of major oil companies in the plays as indications of success. But advocates rarely address details about profitability and they never mention failed wells.

Shale gas plays are an important and permanent part of our energy future. We need the gas because there are fewer remaining plays in the U.S. that have the potential to meet demand. A careful review of the facts, however, casts doubt on the extent to which shale plays can meet supply expectations except at much higher prices.

One Hundred Years of Natural Gas

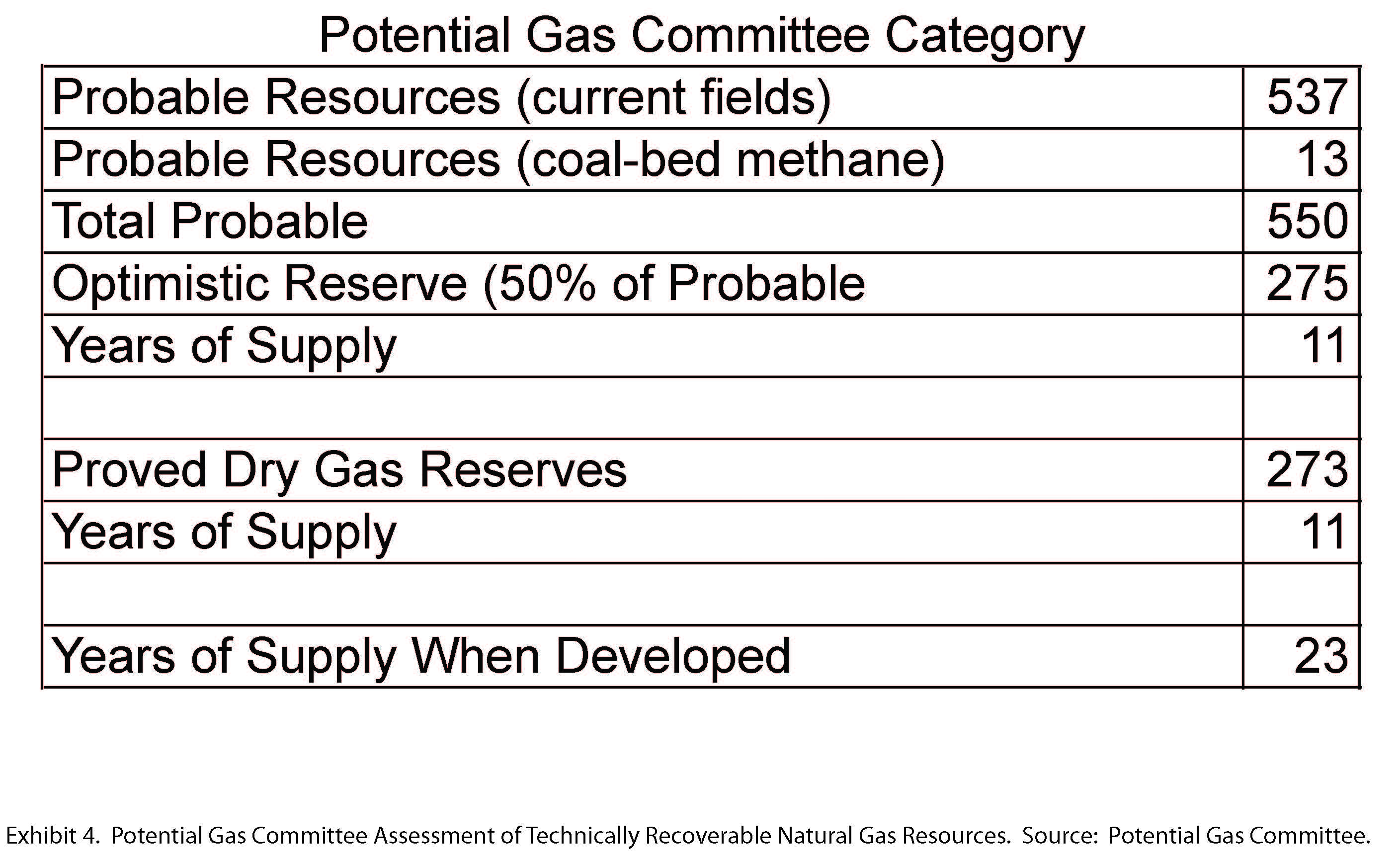

The U.S. does not have 100 years of natural gas supply. There is a difference between resources and reserves that many outside the energy industry fail to grasp. A resource refers to the gas or oil in-place that can be produced, while a reserve must be commercially producible. The Potential Gas Committee (PGC) is the standard for resource assessments because of the objectivity and credentials of its members, and its long and reliable history. In its biennial report released in April 2011, three categories of technically recoverable resources are identified: probable, possible and speculative.

The President and many others have taken the PGC total of all three categories (2,170 trillion cubic feet (Tcf) of gas) and divided by 2010 annual consumption of 24 Tcf. This results in 90 and not 100 years of gas. Much of this total resource is in accumulations too small to be produced at any price, is inaccessible to drilling, or is too deep to recover economically.

More relevant is the Committee’s probable mean resources value of 550 (Tcf) of gas (Exhibit 4).

If half of this supply becomes a reserve (225 Tcf), the U.S. has approximately 11.5 years of potential future gas supply at present consumption rates. When proved reserves of 273 Tcf are included, there is an additional 11.5 years of supply for a total of almost 23 years. It is worth noting that proved reserves include proved undeveloped reserves which may or may not be produced depending on economics, so even 23 years of supply is tenuous. If consumption increases, this supply will be exhausted in less than 23 years. Revisions to this estimate will be made and there probably is more than 23 years but based on current information, 100 years of gas is not justified.

Shale Gas Plays May Not Provide Sustainable Supply

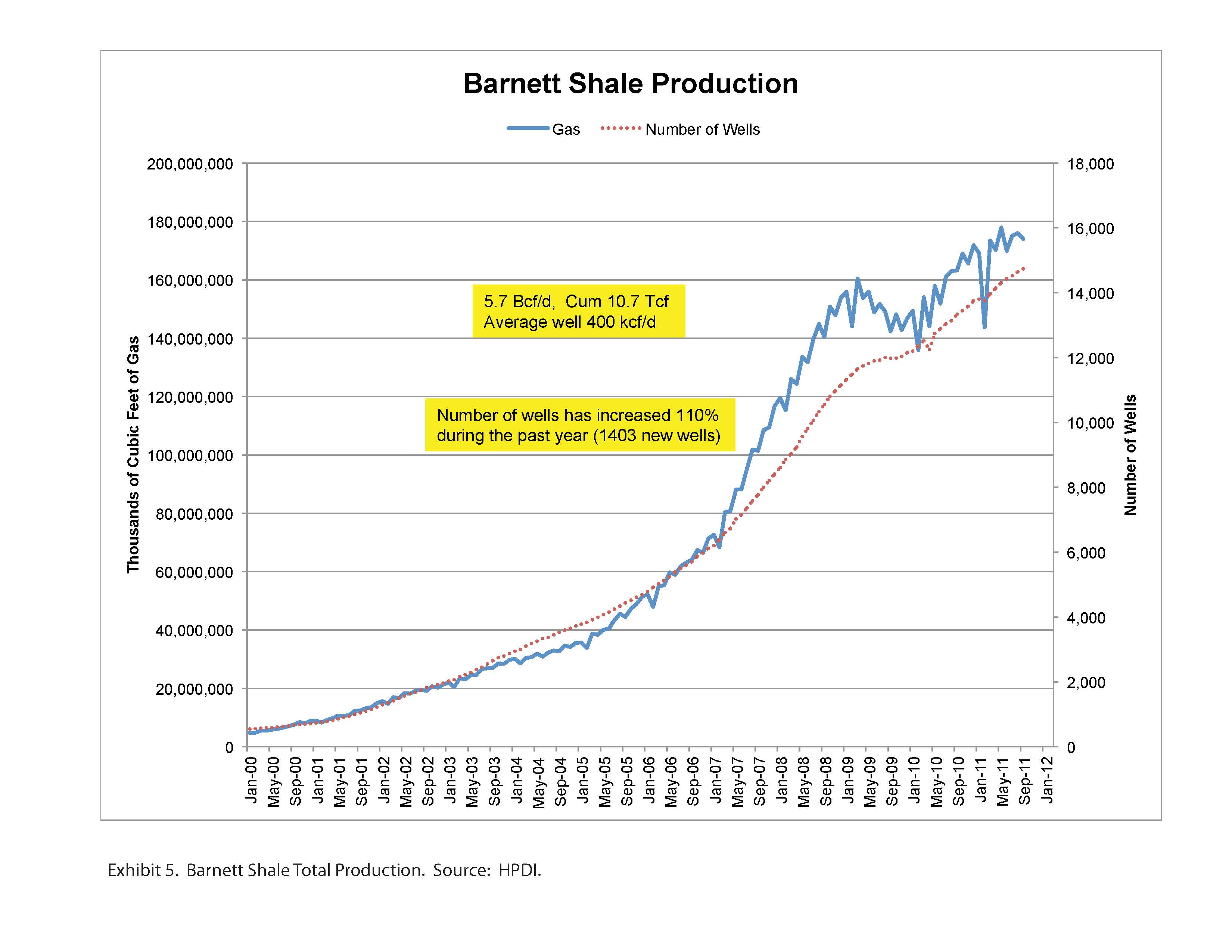

Several of the more mature shale gas plays are either in decline or appear to be approaching peak production. Exhibit 5 shows that total Barnett Shale production is approximately 5.7 Bcf per day (Bcf/d) and cumulative gas production is more than 10 trillion cubic feet (Tcf) of gas. It also shows that production may be approaching a peak at current gas prices despite the constant addition of new wells.

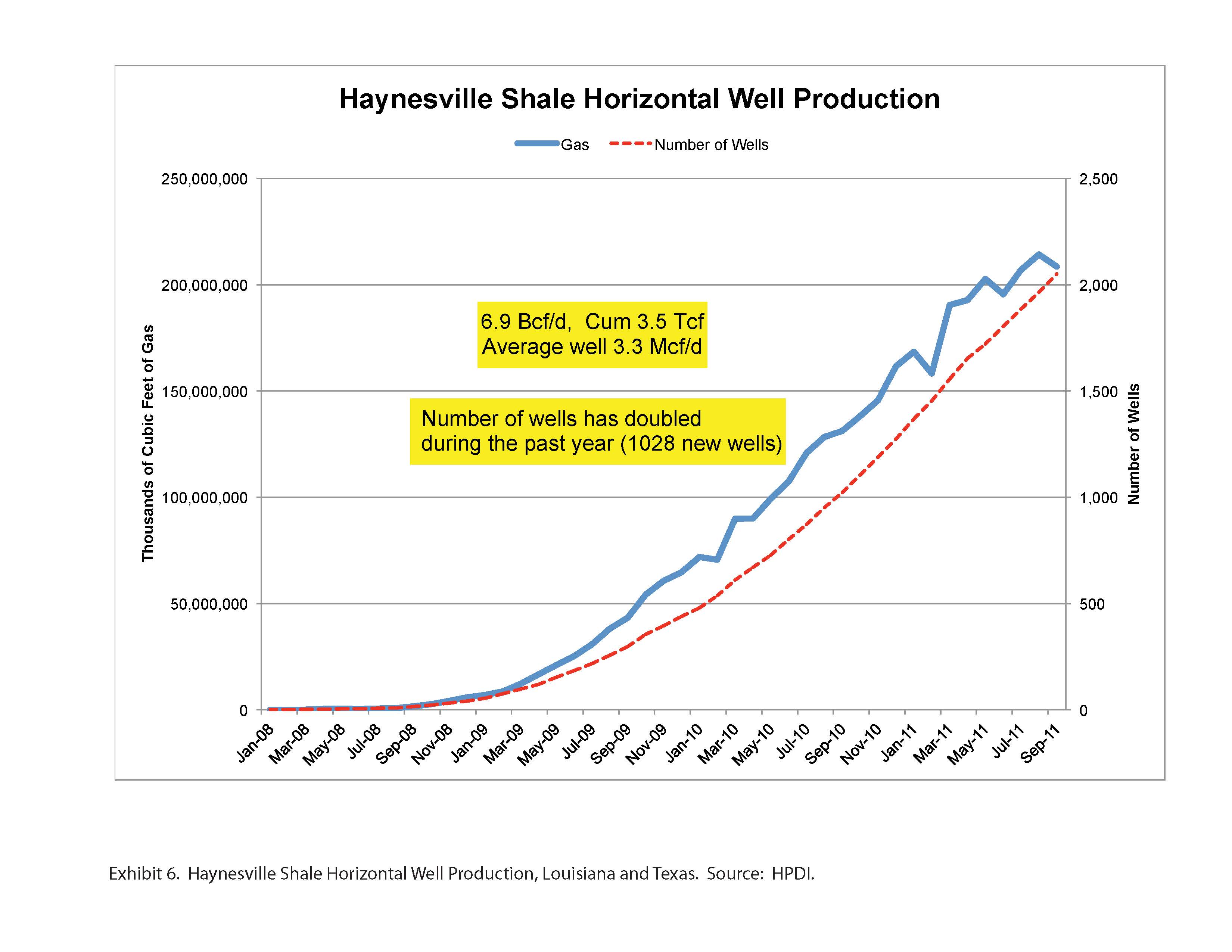

The Haynesville Shale surpassed the Barnett during 2011 as the most productive gas play in North America, with present daily rates of almost 7 Bcf/d and cumulative production of 3.5 Tcf (Exhibit 6).

This play is most responsible for the current over-supply of gas with the average well producing 3.3 million cubic feet per day (Mcf/d) compared to only 0.4 Mdf/d in the Barnett. It is too early to say for sure, but the Haynesville Shale may also be approaching peak production.

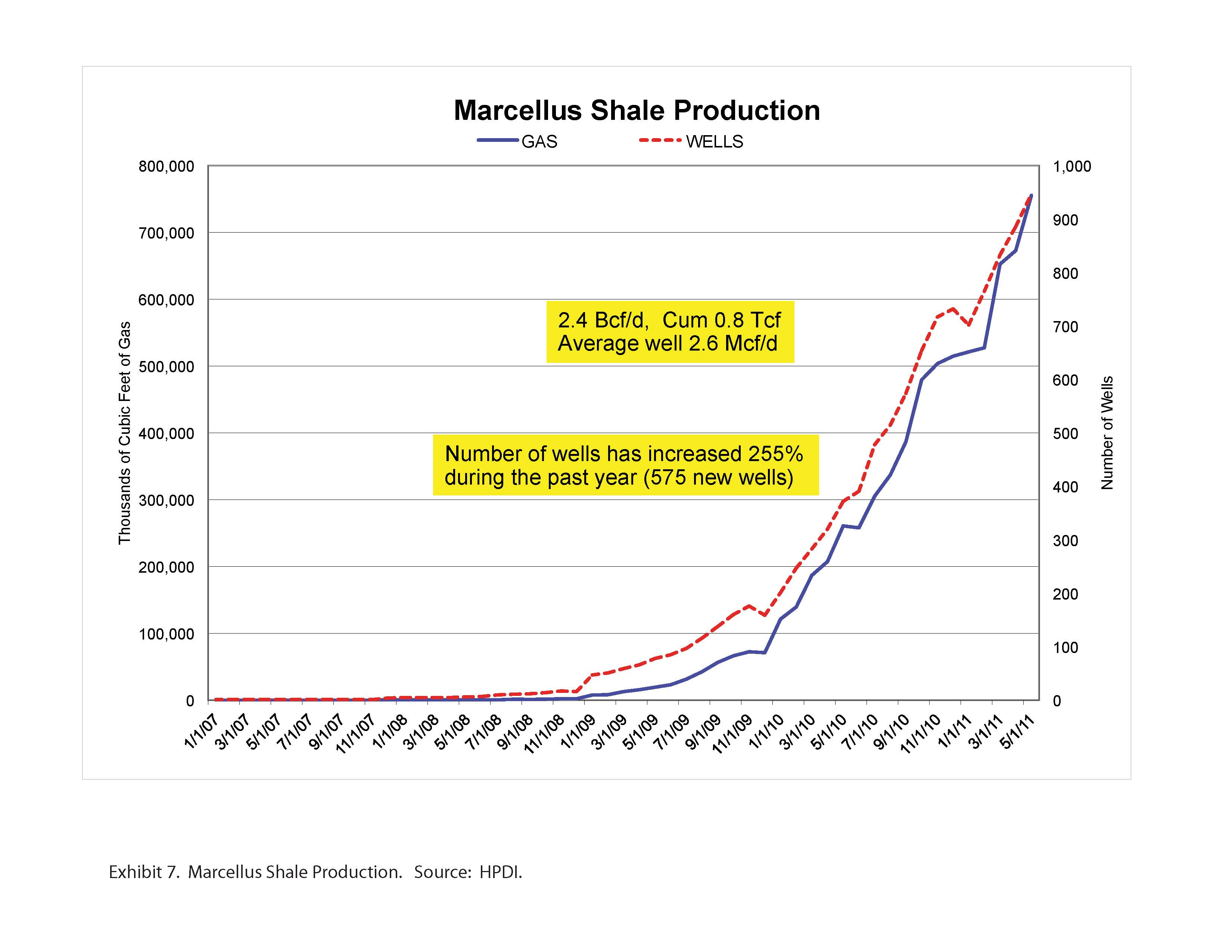

The Marcellus Shale is presently producing 2.4 Bcf/d and has produced a total of about 0.8 Tcf (Exhibit 7).

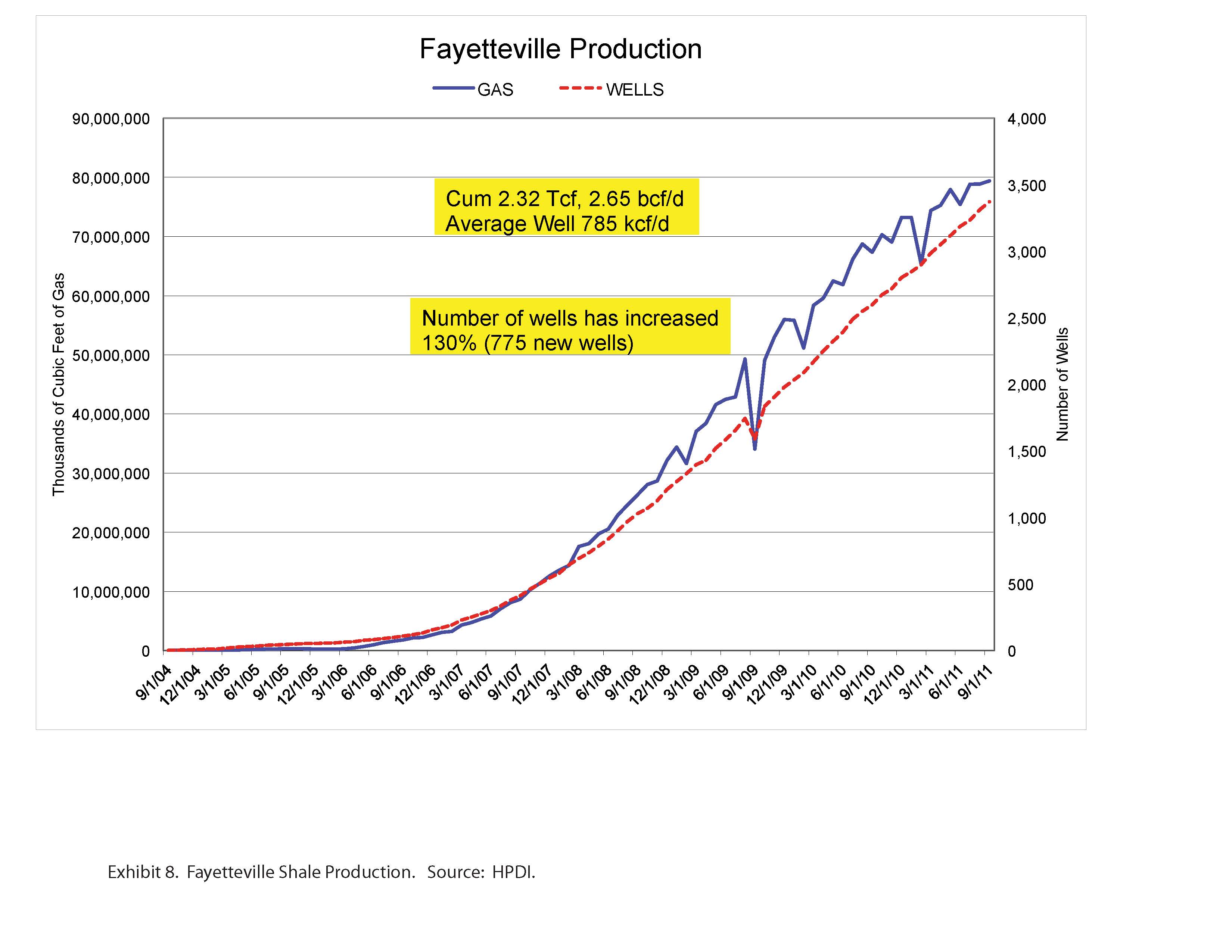

In this play, production shows no sign of leveling off, as it does in the Barnett and Haynesville, and production in the Fayetteville Shale may also be approaching a peak (Exhibit 8).

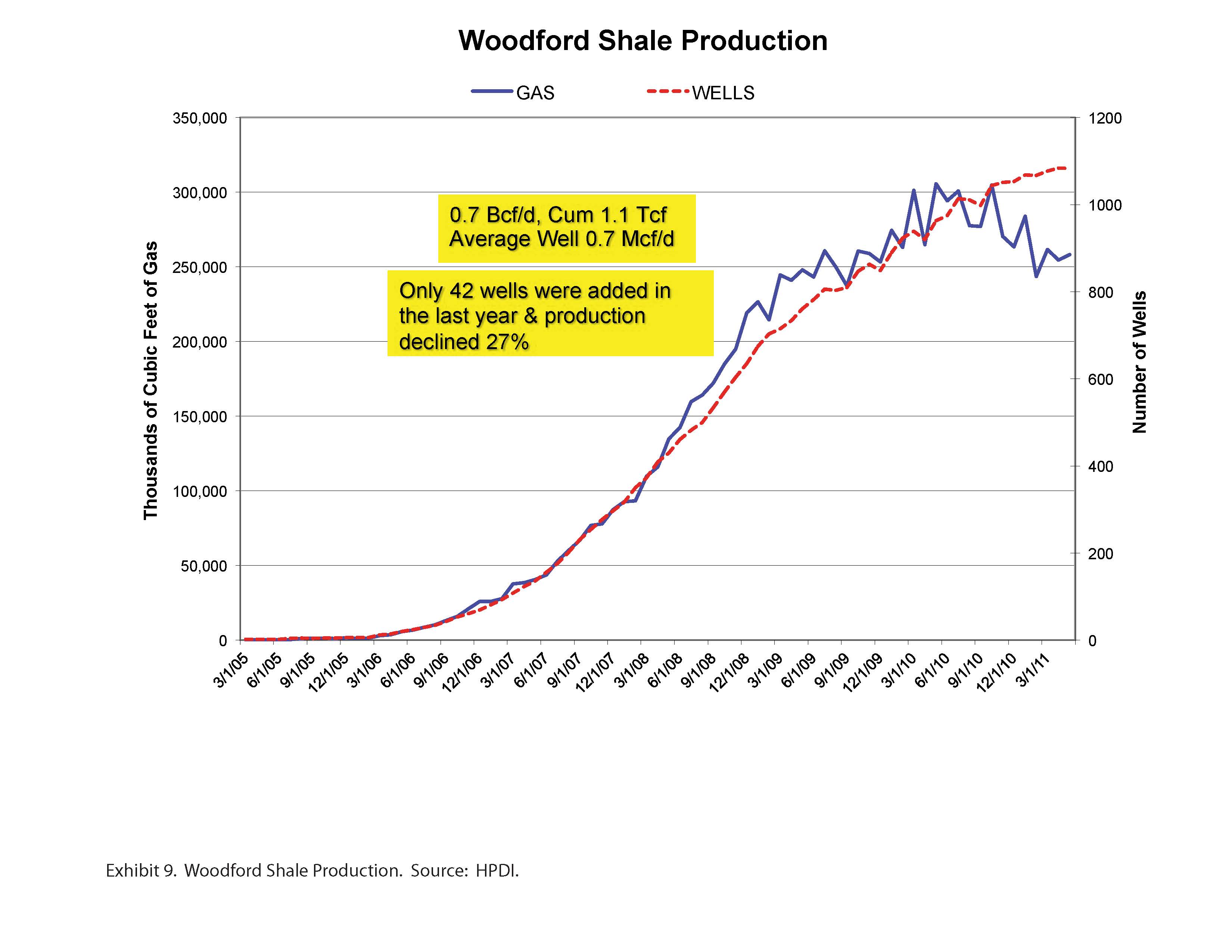

The Woodford Shale is already in decline (Exhibit 9).

If some existing shale gas plays are approaching peak production after only a few years since the advent of horizontal drilling and multi-stage hydraulic fracturing, what is the basis for long-term projections of abundant gas supply?

What Publicly Available Data Indicates About Supply

Data for this analysis is from publicly available sources provided by government agencies such as the Texas Railroad Commission (TX RRC), the Louisiana Department of Natural Resources (LA DNR), the Oklahoma Corporation Commission, and the Bureau of Ocean Energy Management, Regulation and Enforcement (BOEMRE). This data is available on web sites maintained by these agencies but is also collected and compiled for a fee by service companies, specifically IHS and HPDI (DI Desktop). All of these sources provide access to individual well, field, county, and state production.

The EIA provides valuable data on oil and gas production but not at finer than state level, and state production is only current through 2010. EIA gas production data differs somewhat from state data and from the data collected by service companies, and is generally more optimistic. The EIA uses a model to calculate gas production based on a sample of large gas producers, and then applies a correction to reconcile production with underground storage volumes.

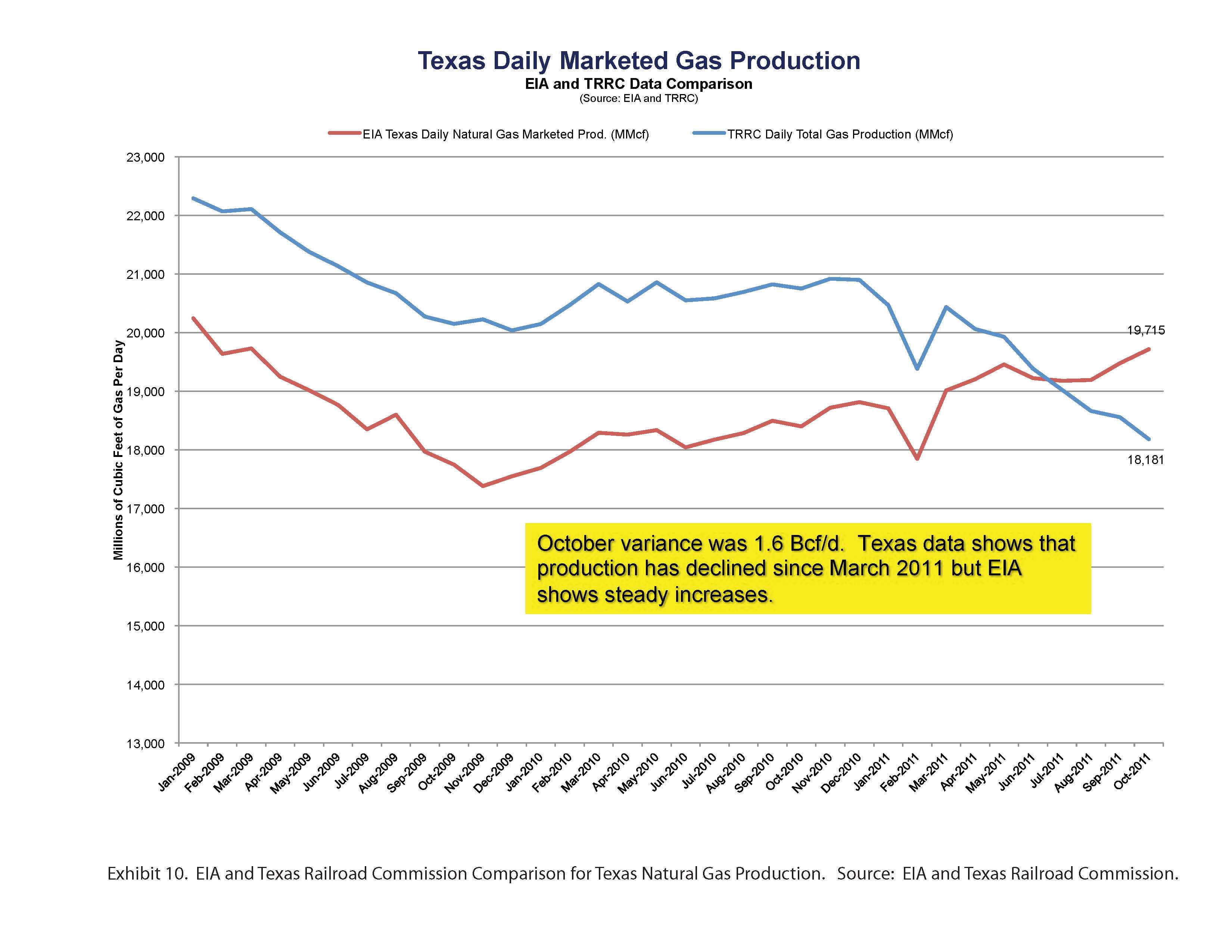

Exhibit 10 shows the discrepancy for Texas gas production between EIA and TX RRC data.

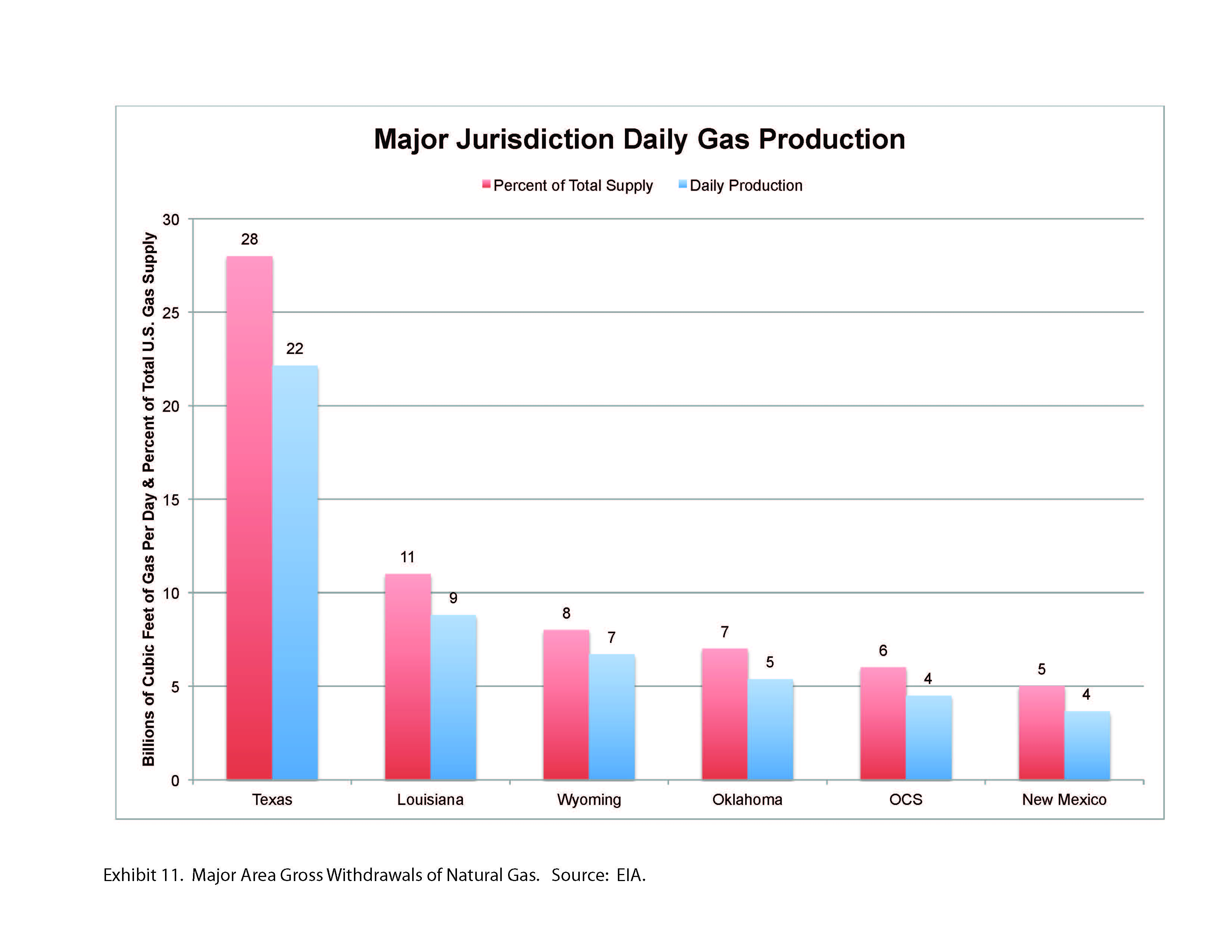

The October 2012 difference was 1.6 Bcf/d. Although TX RRC Data indicates that Texas gas production has declined each month since March 2011, EIA reports show consistent increases. This difference is important because Texas produces 28% of U.S. gas supply (Exhibit 11). Similar differences have been noted for other major gas-producing regions. It should be noted that the EIA data in Exhibit 11 represents marketed production while the TX RRC data shows total gas production.

These accounts should have different values but also should have similar trends. The trends are similar through March 2011 but then diverge producing the present noted variance (The November difference, not shown on the graph, is 2.6 Bcf/d).

We have studied Texas production reporting and find that it is generally reliable and accurate in areas that we follow closely in our oil and gas exploration and production business. Revisions are common for the first and second most recent months of production but are not statistically significant at the state or field level. Data going back three reporting months is reliable. Studies of other major gas-producing states show similar results. Our intent to is to point out the differences between state and EIA data, and to suggest that EIA data is not particularly useful to track individual play or some state production on a current basis.

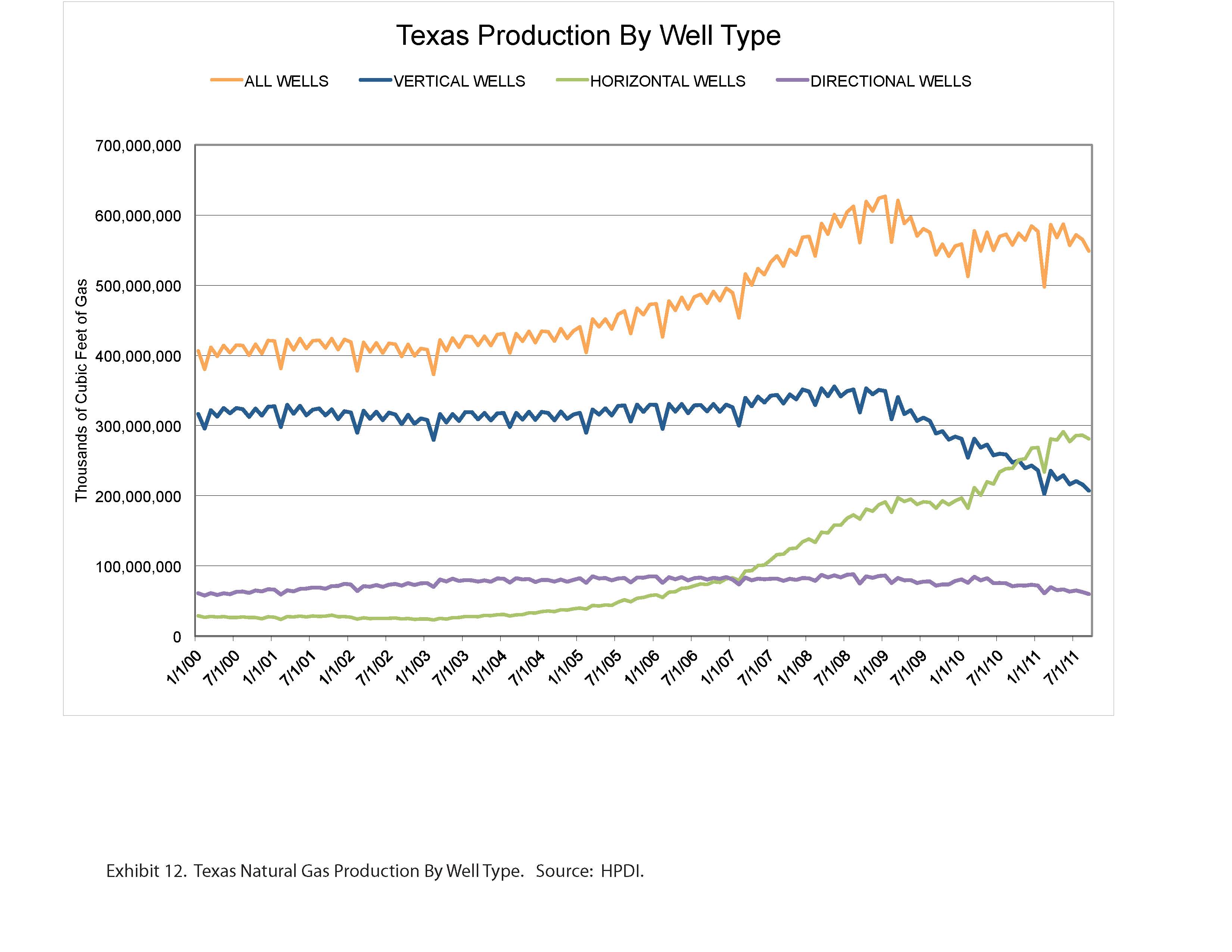

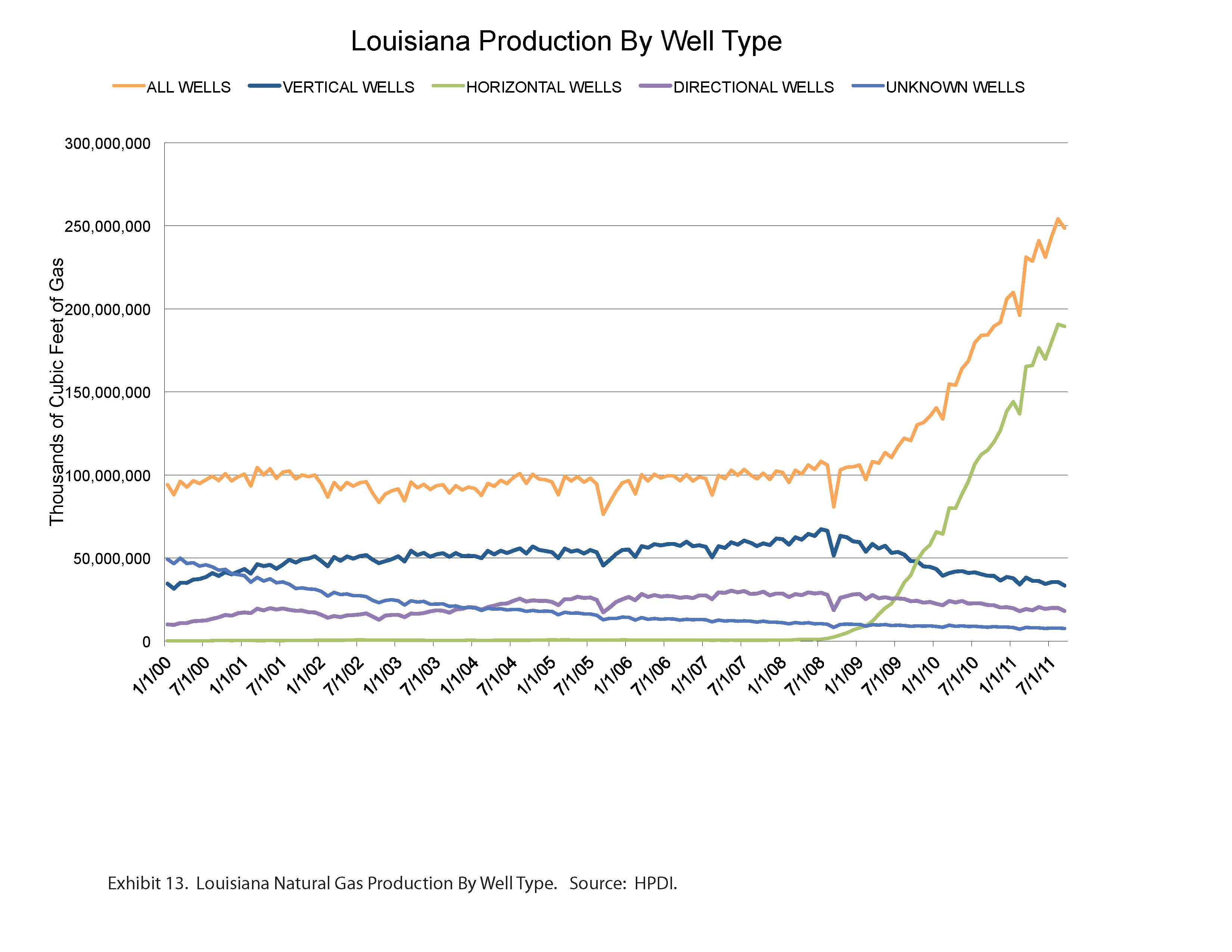

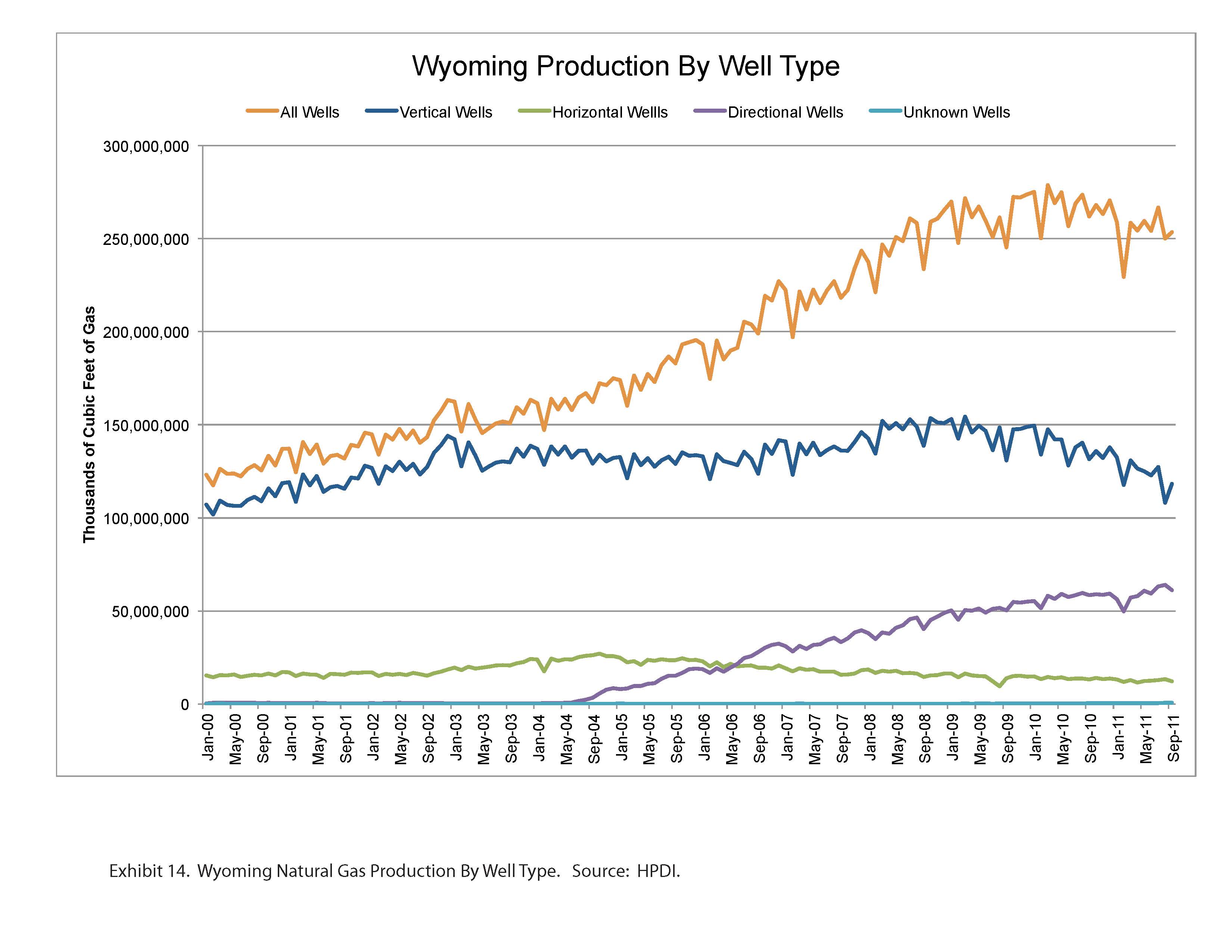

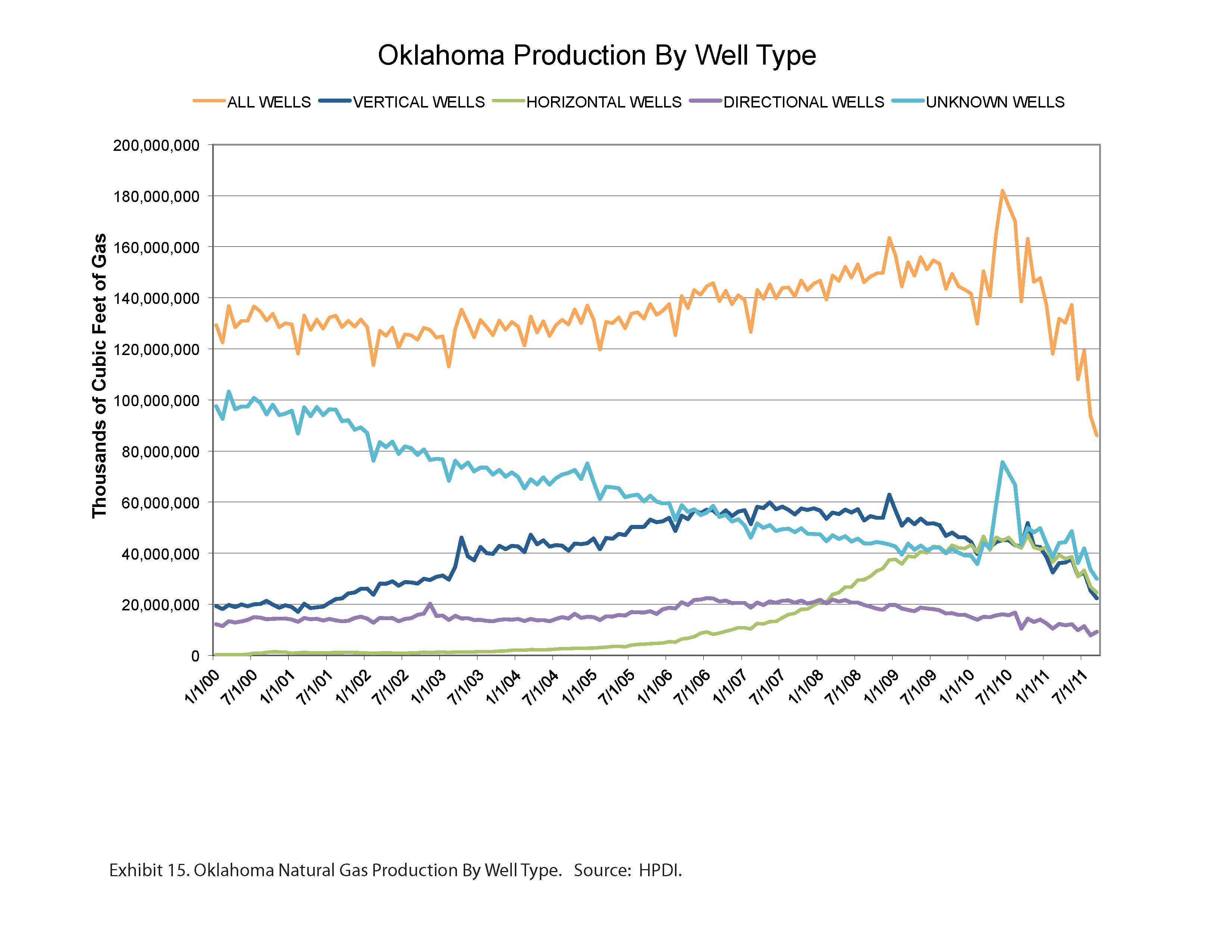

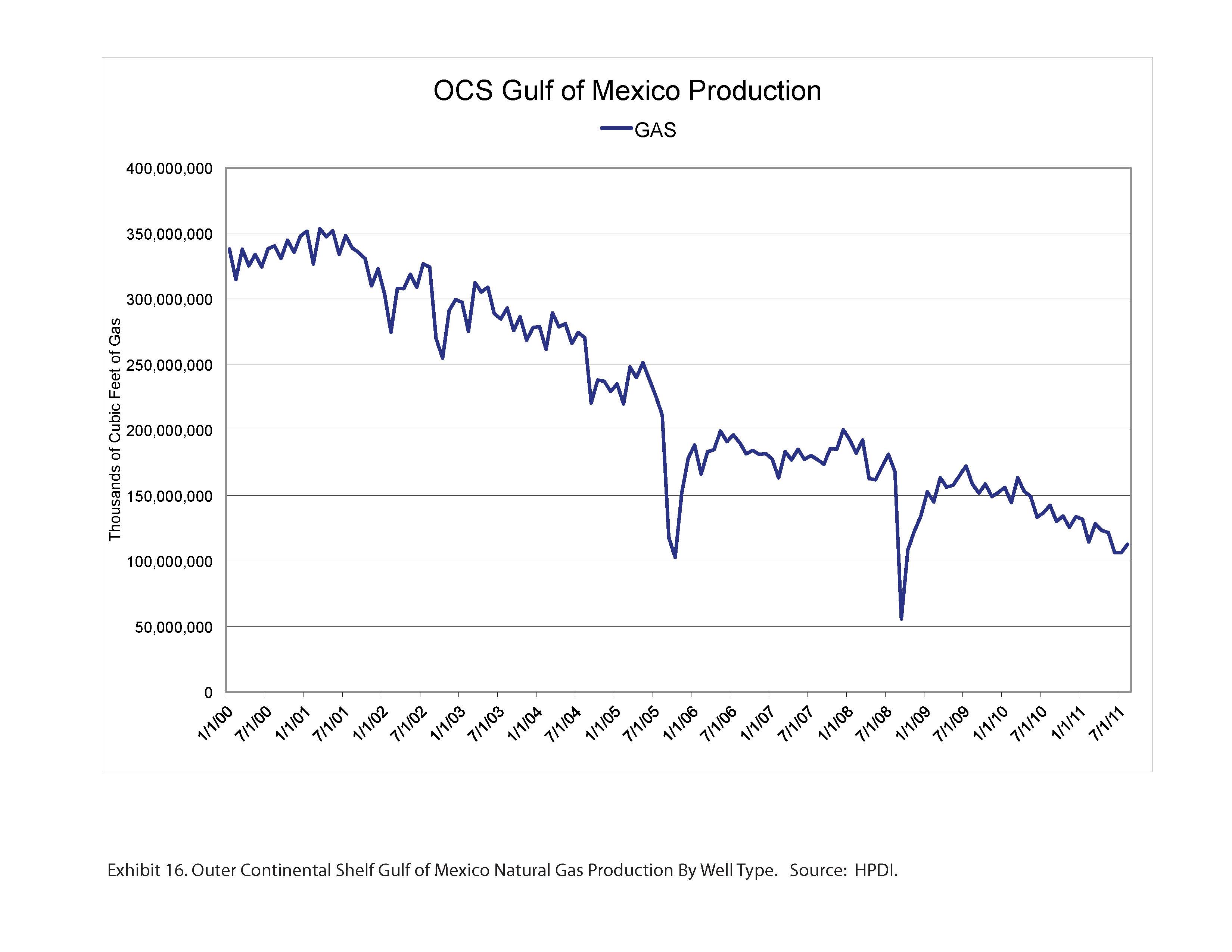

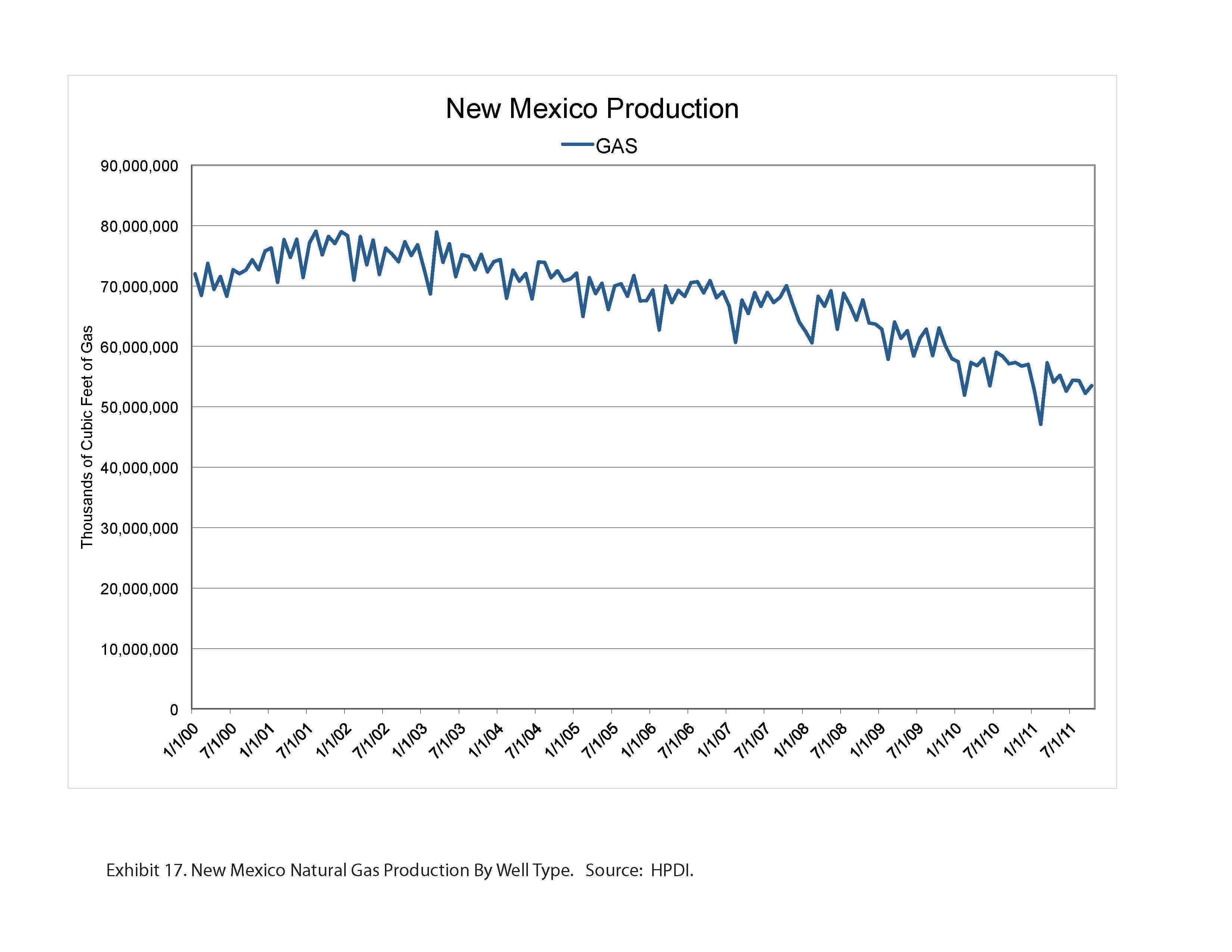

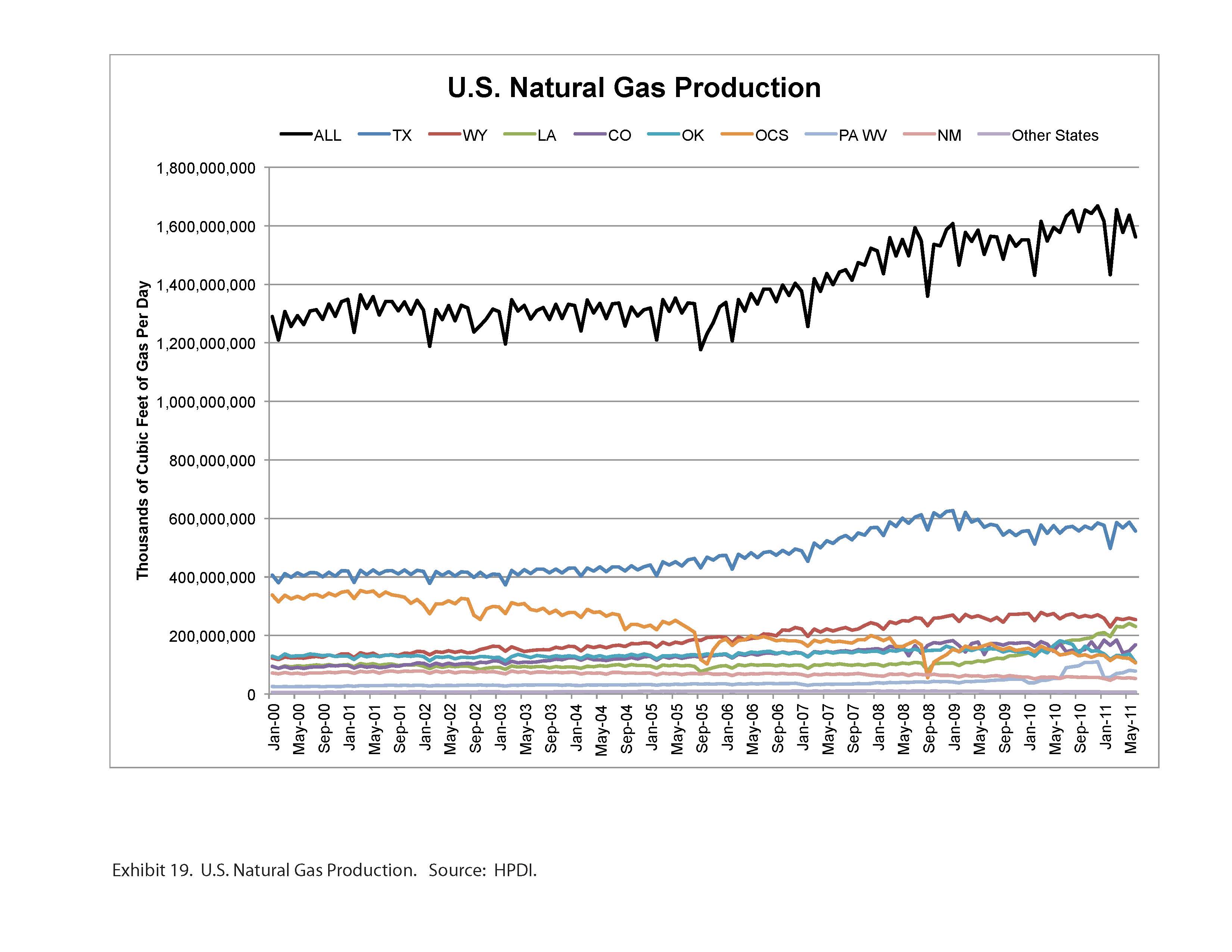

Texas, Louisiana, Wyoming, Oklahoma, Gulf of Mexico Outer Continental Shelf, and New Mexico account for roughly 75% of U.S. natural gas supply and, therefore, provide a useful proxy for total U.S gas production. Exhibits 12 through 17 show natural gas production for these regions.

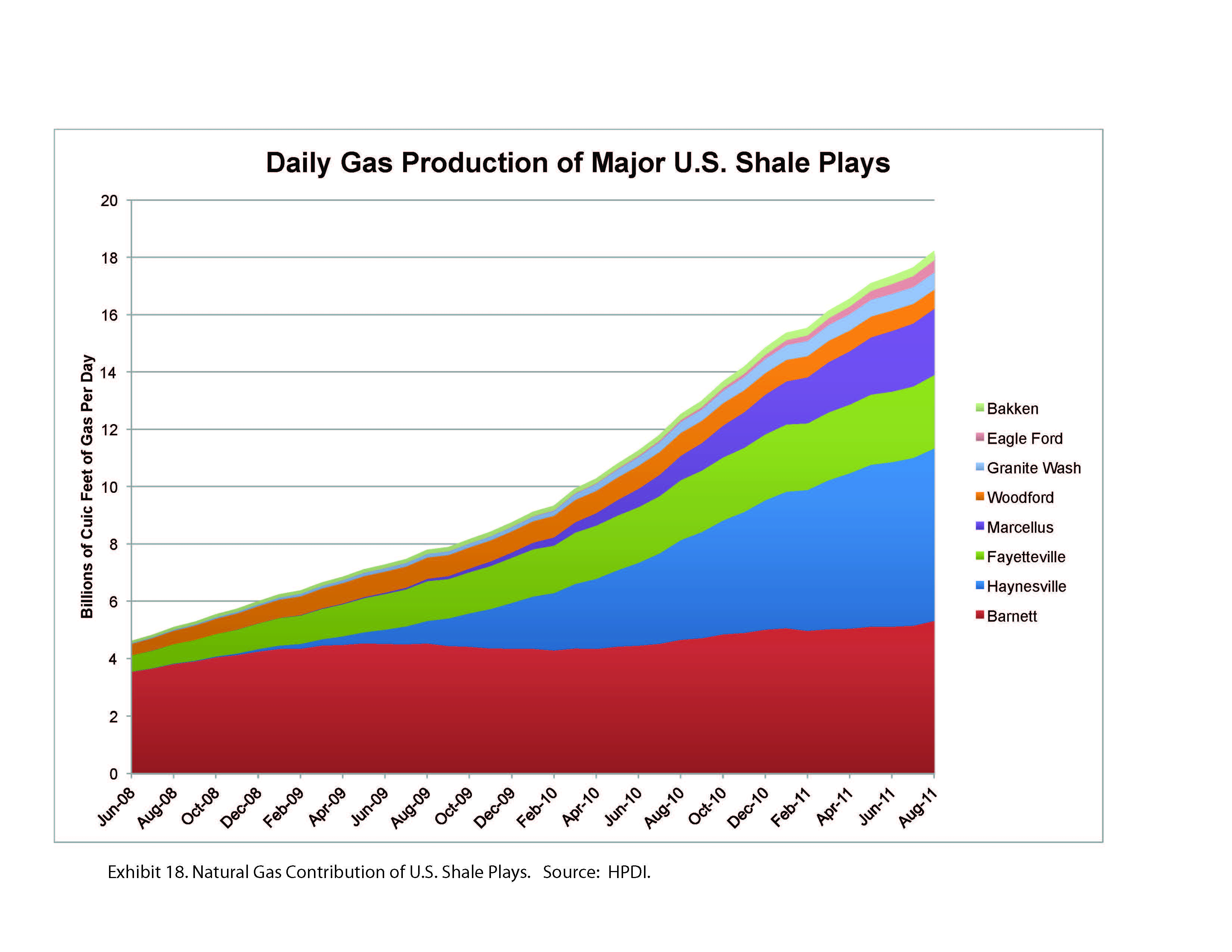

All of these major gas-producing areas except Louisiana are in decline. This is largely because non-shale production is declining rapidly since little new drilling in these reservoirs in recent years has occurred. While shale production volumes and initial rates are impressive (Exhibit 18), much of this new production is merely substituting for depleting conventional gas reserves.

With the shift to more oil-prone or “liquids-rich” shale plays, many observers have suggested that associated gas production from these plays is or will be a major contributor to the present over-supply of gas. Approximately 3% of total U.S. gas supply is from shale associated gas so, while this is a factor, it is not the cause of over-supply. Details of this analysis may be found in an earlier post. Overall, U.S. natural gas production using state-level data appears to have reached an undulating plateau (Exhibit 19).

Conclusions

A secular shift has occurred in the U.S. domestic gas supply by drilling mostly shale formations, formerly considered source rocks too costly to develop. The tremendous number of wells drilled in the last several years has contributed to an over-supply of gas. The shale revolution did not begin because producing oil and gas from shale was a good idea but because more attractive opportunities were largely exhausted. Initial production rates from shale are high but expensive drilling and completion costs make economics challenging. The gold rush mentality taken by companies to enter shale plays has added expensive leases and new pipelines to those costs, further complicating shale gas economics.

In the decades before shale plays, the exploration and production emphasis was on discipline. Science was used to identify the most prospective areas in order to limit the amount of acreage to be acquired and its cost. Shale plays have produced a land grab business model in which hundreds of thousands of acres are acquired by each company. Unprecedented lease costs have become the norm often based on limited information and science.

Operators have indulged in over-drilling these plays for many reasons but adding reserves, holding leases and company growth are among the main factors particularly with the low cost of capital. The inevitable result has been the collapse of prices as supply exceeded demand. Most analysts forecast that the future will be much like the present, and that natural gas will be abundant and cheap for decades to come. There are, however, strong and consistent indicators that natural gas supply may be less certain than most observers believe and require a higher price to be developed economically. Natural gas demand is growing as fuel switching for electric power generation continues, and will be increased by environmental regulation in the coming years. The U.S. will shift more of its future energy needs to natural gas in many sectors of the economy. The best justification, in fact, for the land grab and over-drilling spree is expectation of higher prices. Those companies that grabbed the land and held it by production will profit greatly once the true supply and cost of shale gas is recognized.

The financial survival of all companies in this position is not, however, certain. Price matters, and there is finally some response from shale gas producers with recent announcements to curtail drilling. While price was cited as the main reason for reduced drilling, it is likely that some companies now have financial constraints. The shale gas phenomenon has been funded mostly by debt and equity offerings. At this point, further debt and share dilution are less feasible for many companies. Joint ventures have provided a way for some to prolong spending but that now seems like a less likely source of funding. Capital availability in the near term will likely be tighter than is has until now. Acquisition and consolidation may become more attractive to companies with cash as producers become more extended.

Some of the shale gas plays may be at or near peak production at least at the current price of gas and technology. All major producing areas except Louisiana are in decline. Some doubt the accuracy of public data compared with EIA data, but it seems unlikely that the trends it shows are erroneous. In any case, the data the EIA makes available does not have sufficient resolution to evaluate individual plays or state-level trends.

Intermediate-term shale well performance is poorer than assumed previously . Continuous treadmill drilling masks this issue so play decline rates are not recognized. High decline rates are, however, a salient issue meaning that and most of a shale gas well’s reserve is produced in the first few years. Well life appears to be shorter than initial expectations. This means that an increasing number of wells must be drilled in order to maintain supply. Now, it appears that fewer wells may be drilled until price recovers to commercial levels. The argument for improved efficiency that cites increasing production with lower rig count is suspect. It is mostly because of the large backlog of previously drilled wells that are just now being connected to sales. This spare capacity provides a boost to supply during a period of falling gas-directed rig count.

The gold rush is over at least for now for the less commercial shale plays. The money and activity have moved to more oil-prone shale plays such as the Eagle Ford and Bakken or to higher potential gas plays such as the Marcellus. Improbable stories that great profits can be made at increasingly lower prices have intersected with reality. A painful adjustment is underway in the natural gas exploration and production industry. Fewer jobs will be created and projects may develop more slowly. This development may expose the notion of long-term natural gas abundance and cheap gas as an illusion. The good news is that this adjustment will lead to higher gas prices in a future less distant than most believe. Higher prices coupled with greater discipline in drilling will allow operators to earn a suitable return and offer the best opportunity for supply to grow to meet future needs.

References

Andreoli, D., 2011, The Bakken Boom – A Modern-Day Gold Rush. The Oil Drum: http://www.theoildrum.com/node/8697.

Berman, A.E. and L. Pittinger, 2011, U.S. Shale Gas: Less Abundance, Higher Cost. The Oil Drum: http://www.theoildrum.com/node/8212.

EIA Annual Energy Outlook 2011 Early Release Overview.

EIA Annual Energy Outlook 2011 Natural Gas Tables: http://www.eia.gov/oiaf/aeo/tablebrowser/#release=EARLY2012&subject=0-EA….

Gilbert, D. and R. Dezember, Chesapeake Energy Pulls Back Amid Natural-Gas Glut: Wall Street Journal, January 24, 2011: http://online.wsj.com/article/SB1000142405297020380650457717865173251197….

Potential Gas Committee 2010 Report: http://www.potentialgas.org/.