The most curious natural gas story of the year so far comes out of Boston and seems to have echoes of a deepening Russia-related scandal in Washington. A liquefied natural gas (LNG) tanker bearing natural gas produced in part in Russia delivered its cargo to the Boston area for insertion into the natural gas pipeline system there. Apparently, the Russian company that supplied some of the gas may fall under U.S. sanctions against the financing and importation of Russian goods.

One of the many ironies of the delivery is that the United States is simultaneously importing LNG in one place even as it exports LNG from another. (I’ll explain later why this may become a more frequent occurrence in the years ahead.)

The hue and cry from the natural gas partisans blamed Boston’s predicament on the lack of pipelines to carry growing gas production from the nearby Marcellus and Utica shale deposits to needy Bostonians whose gas supplies had been depleted by a deep winter freeze.

Within the context of this narrow appraisal, the partisans are mostly correct. Attempts to bring more pipeline gas to New England have come to grief, especially in New York state where residents have strongly opposed new natural gas pipelines and storage facilities.

In addition, the state banned hydraulic fracturing—the main method for extracting gas from the Marcellus and Utica deposits—in 2014, claiming the process threatened water supplies. That ban, of course, prevented any shale gas development in southern New York under which the deposits lie. And, it brought into disrepute all things related to hydraulic fracturing or “fracking” including natural gas pipelines and storage facilities.

What lurks behind the outrage of the partisans is the assumption—widely touted in the media and by the U.S. Energy Information Administration (EIA)—that the country is about to become a large exporter of LNG for the long term as its natural gas production grows ever skyward. Energy abundance, they like to say, has arrived in America.

There’s just one problem—or should I say four? Of the six major U.S. shale gas plays that are the basis for the optimism about supply, four are already in steep decline. (Gas produced from other types of deposits has been either flat or in decline for many years.) As of the end of 2017 the rate of natural gas production in the Barnett play in Texas, the Fayetteville play in Arkansas, and the Haynesville play spanning the area where Arkansas, Louisiana and Texas meet are all coincidentally down by about the same 44 percent from their peaks years ago. The Woodford play is down about 25 percent from its 2016 peak.

That leaves only the Marcellus and Utica plays mentioned previously to carry the United States into an era of continuously climbing overall natural gas production. That’s an unlikely prospect and one rated as such by David Hughes, author of “Shale Reality Check.” For his analysis Hughes meticulously checked the actual well production histories of shale gas wells—rather than merely scanning misleading energy headlines as most other analysts seem to do.

Even the Marcellus is showing its age as the rate of production from new wells sags, a sign that the most productive prospects have already been drilled. In addition, a preliminary production peak in the Marcellus in early 2017 waits to be confirmed.

If the optimistic scenarios for U.S. natural gas production fail to materialize as seems likely, we will almost certainly see more LNG-related irony as imports and exports occur simultaneously at the country’s LNG terminals. This is because long-term delivery contracts entered into by LNG export terminals will prevent any rerouting of gas bound for export to domestic use, possibly even under emergency conditions. If the shale gas boom fizzles, we will discover that government approvals for U.S. export terminals were wildly ill-advised as more LNG delivery ships dock near Boston and other places to make up in part for outgoing U.S. LNG cargoes .

__________________________

P. S. I suggested the possibility of the scenario outlined above in a piece in 2013 and discussed the Australian experience with the same predicament in 2017.

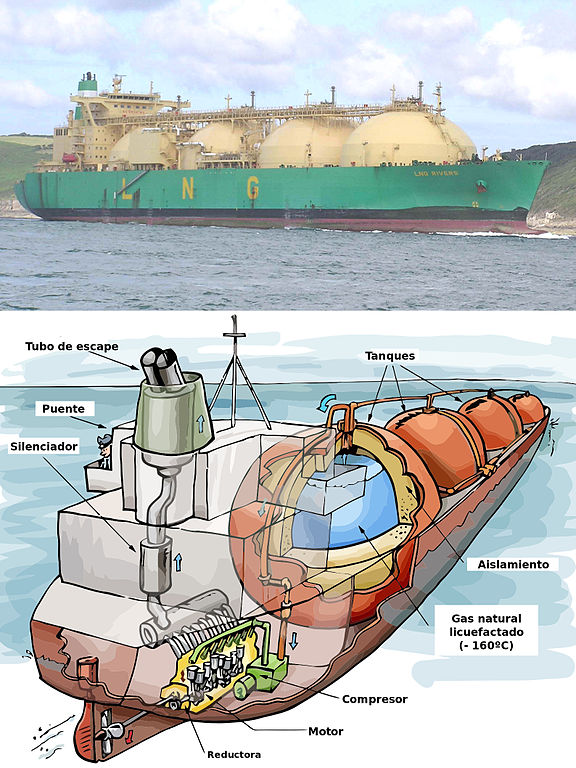

Image: Cartoon of the insides of a LNG carrier. A combination of two images by Peter Welleman (2012). Wikimedia Commons.

{kind=link}