In a November 15 press release, the United States Geological Survey (USGS) announced that there might be lot more oil in Texas than previously estimated:

The Wolfcamp shale in the Midland Basin portion of Texas’ Permian Basin province contains an estimated mean of 20 billion barrels of oil, 16 trillion cubic feet of associated natural gas, and 1.6 billion barrels of natural gas liquids. . . . This estimate is for continuous (unconventional) oil, and consists of undiscovered, technically recoverable resources. The estimate . . . is nearly three times larger than that of the 2013 USGS Bakken-Three Forks resource assessment, making this the largest estimated continuous oil accumulation that USGS has assessed in the United States to date.

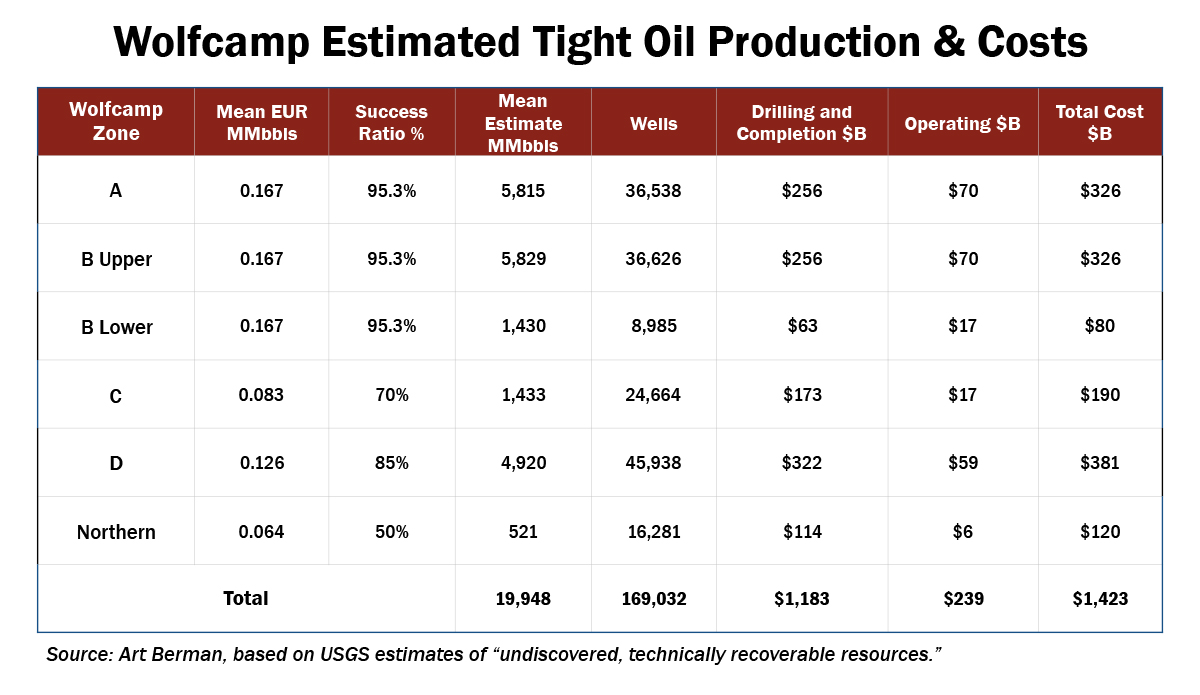

Energy journalists and bloggers gushed in response; one headline read, “Nearly a Trillion Dollars’ Worth of Oil Was Just Discovered in Texas.” Well, technically speaking, the oil wasn’t actually “discovered.” The USGS announcement was of an estimate of the possible (50 percent likelihood) presence of 20 billion barrels of “undiscovered technically recoverable resources.” Translation: this is oil that has a fair likelihood of existing, and that could be recovered with existing technology if cost is no object. But, of course, in the real world the costs associated with resource discovery and extraction are always a consideration. Geologist Art Berman did some quick calculations and found that the Wolfcamp formation would lose $500 billion at today’s oil prices. Based on Berman’s post, we put together this table, which indicates costs of $1.4 trillion—not counting taxes and royalties—for oil worth $900 billion at $45 per barrel.

A few years ago another, rather similar announcement was made about the Monterey shale in California; in that case, the EIA published a report suggesting the presence of 15.4 billion barrels of oil. On the basis of this announcement, the University of Southern California published a report concluding that the development of the Monterey shale could—by 2020—boost California’s GDP by 14 percent, provide an additional 2.8 million jobs (a 10 percent increase), and provide $24.6 billion per year in additional tax revenue (also a 10 percent increase). We did a thorough analysis of the Monterey play, using production history and data from existing wells, and concluded that the EIA’s estimate was “likely to be highly overstated.” The EIA later lowered its estimate by a whopping 96 percent. Subsequent activity in the Monterey shale hasn’t seen a significant uptick. We think the situation with regard to the USGS estimate for the Wolfcamp in Texas may play out similarly.

The Permian Basin is one of the largest petroleum provinces in the U.S. Since the 1920s, 417,000 wells have been drilled—147,000 of which are still producing. Nearly 32 billion barrels of oil and 113 trillion cubic feet of gas have been produced in the Permian over the past century. And the advent of horizontal drilling combined with hydraulic fracturing has allowed the redevelopment of old plays like the Wolfcamp to squeeze previously unrecoverable oil from impermeable source rocks.

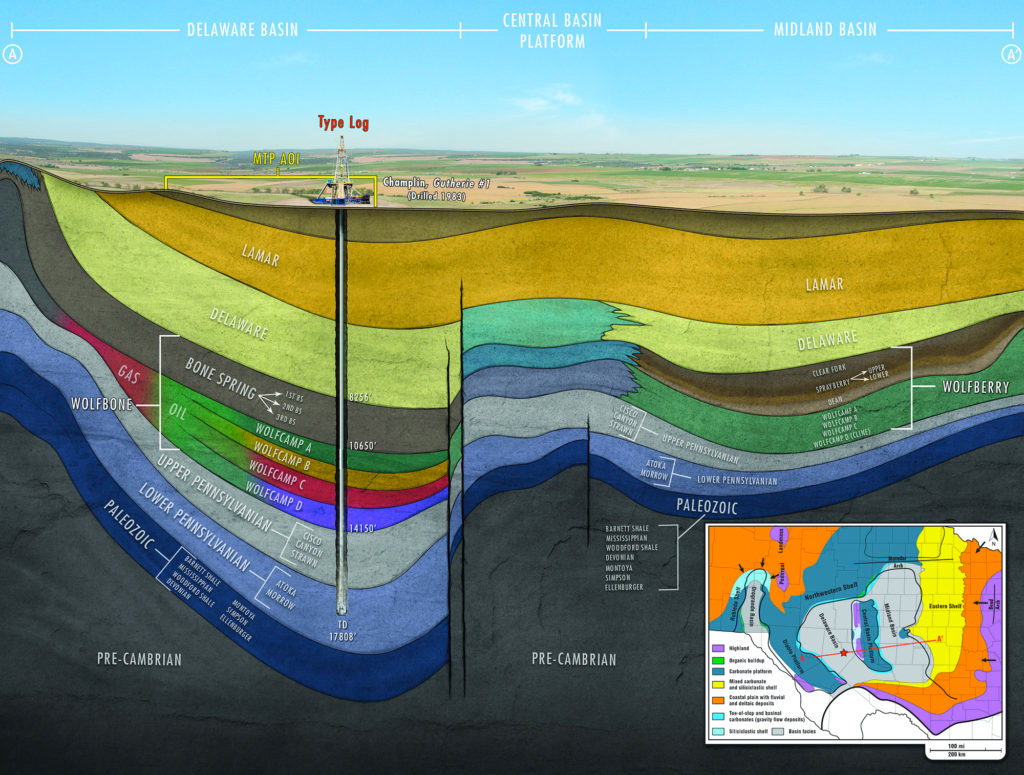

Geological strata in a portion of the Permian Basin, including the various zones of the Wolfcamp Play. Image source: Tarka Energy.

No doubt, there is a large amount of oil in the Wolfcamp. It is one of the best Permian Basin plays; it has produced just over a billion barrels of oil and 5 trillion cubic feet of gas since the 1950s. Some 13,700 wells have been drilled; 6,700 of these are still producing, many of which have been drilled in the past few years.

While oil production rates in other U.S. tight oil regions (including the Bakken play in North Dakota and the Eagle Ford play in Texas) are declining, the Permian is still seeing expanding output. Its prospects are moderately favorable, with actual future yields subject to oil prices and production costs.

However, those prospects must be viewed in context. We are talking about unconventional oil that will require high oil prices to justify high costs of production. The U.S. tight oil boom of the last few years depended on unique circumstances—including sky-high oil prices (in the range of $100 a barrel) and historically low interest rates. Small companies made impressive presentations to potential investors, borrowed heavily, leased thousands of acres, and rapidly drilled enormous numbers of wells. For a while the results looked great—production levels soared and investors kept the cash rolling in to bankroll still more drilling. Even with stratospheric oil prices many wells were unprofitable, but nobody seemed to care.

Then in mid-2014, oil prices collapsed. Since then, the balance sheets of companies specializing in tight oil production have been bleeding red ink. U.S. tight oil production has declined by 19 percent—or more than one million barrels per day—since peaking in March 2015, according to the EIA’s latest monthly Drilling Productivity Report. Only the Permian Basin has not peaked. If oil prices rebound dramatically, the industry may survive and drilling may resume at high rates; if not, investors will eventually sour on tight oil. Our analysis suggests that even if high prices had persisted, production from all U.S. tight oil plays would have peaked before 2020. The price collapse merely forced the issue.

The recent USGS announcement about the Wolfcamp play may inspire another round of company presentations to investors, and perhaps even a spurt of new drilling, but it probably won’t much change the overall picture.

Wolf howling image via shutterstock. Reproduced on Resilience.org with permission.