One of the inexorable results of the developing shortage of oil is that prices will rise. It is a prospect that does not particularly concern the Saudi Arabian Administration, Minister Al-Naimi having recently inflated the acceptable range for crude up to $90 a barrel, and JP Morgan has recently predicted an imminent rise to $100, a theme apparently now also taken up by Libya. Higher oil costs lead to higher fuel bills, and there is already a report in the United Kingdom that, in consequence , there may already be an increase in winter deaths.

Because demand for imported oil in countries such as China and India continues to increase at a steady rate, it will only be through the increase in production from the exporting nations that supply can meet such demand, and prices can be held at a relatively stable level.

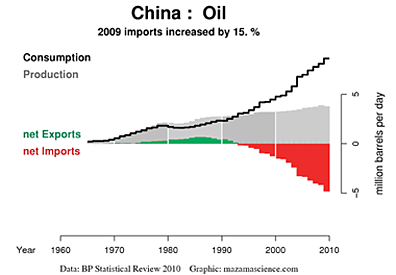

Chinese changes in oil flows (Energy Export Databrowser )

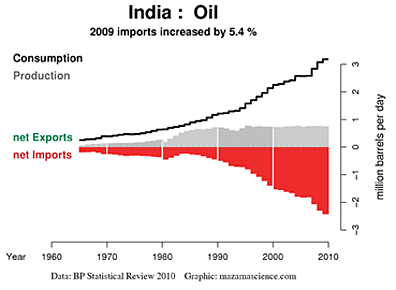

Indian changes in oil flows (Energy Export Databrowser )

The two plots above are only illustrative of the problem, given that the volumes and relative import/export flows change around the world continuously. However, the world’s two largest producers of oil are Saudi Arabia and Russia.

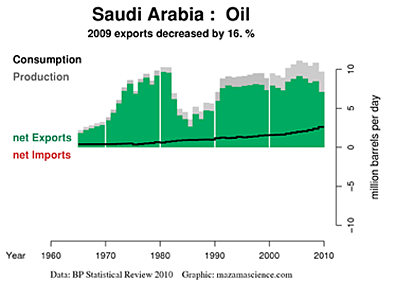

Given the likely continued increase in the world thirst for oil, it is worth reviewing again the potential for increased exports from these two countries. The first is Saudi Arabia, whose oil Minister I quoted at the beginning of this piece.

Saudi Arabian changes in oil flows (Energy Export Databrowser )

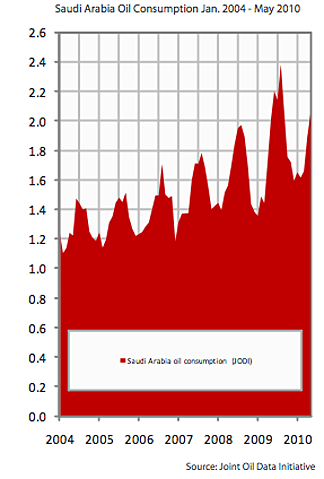

While it is likely that a significant proportion of the oil export drop in 2009 was due to the world recession, the steady rise of the black line, that showing internal consumption, is also contributing to a reduced volume available for export. That rise is perhaps better illustrated with a plot from The Oilwatch Monthly for August.

Whether Saudi Arabia will increase production, and if so by how much, is now one of the more interesting questions for 2011. They have indicated that they are increasingly more concerned with maintaining the long term potential for higher ultimate yield, which requires lower daily production rates, and have already cut their maximum planned production rate to 12 mbd in consequence. If they do not increase flows significantly, then the focus swings to Russia.

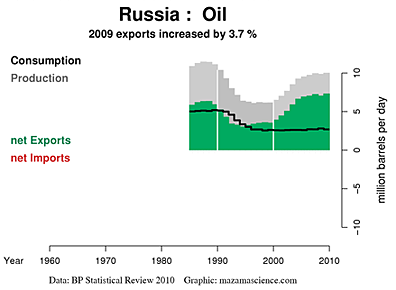

Only today Russia was announcing that production had reached a new record of 10.26 mbd for October. The gain was achieved with increased production from Sakhalin Island, and oil exports increased to 4.97 mbd. Whether this level can be sustained, however, remains a critical question.

Russian changes in oil flows (Energy Export Databrowser )

President Putin has noted that it will take $280 billion in investment to stop a 20% fall in production over the next 10 years, and that investment will only hold production at current levels. Russian consumption has also been relatively flat over the last decade, and one has to wonder if that will continue, given the flow of money into the economy that the sale of the oil is bringing. The increased funding has already stopped the decline in oil production in the country that had been forecast only a year ago.

Production is coming from the relatively new fields such as Vankor (270 kbd), South Khylchuyu, Verkhnechonskoye (51 kbd), Uvat (78 kbd). However production from these fields has been manipulated a little, apparently, by attempts to find helpful tax breaks. Production at South Khylchuyu being a current victim of that, since the field has a potential of 150 kbd, and started at 80 kbd. That production is now all slated to go to China and China has also funded a loan for pipeline construction to Vankor, scheduled to be completed next year, that will carry that production (scheduled to peak at 510 kbd in 2014) to China. Current Vankor production is about 10% above that anticipated last year, but with that gain going to China, and overall production being about level, this suggests that the declines in production from older fields will increasingly hurt exports to the West.

“Vankor say they will do 250,000 bpd next year, but unless you’re bringing on very sizeable fields every year, the five percent decline rate in western Siberia will take that out,” said Russian oil analyst Oswald Clint of Sanford Bernstein. (last year).

Clearly the current prices of oil are helping to justify the increased production practices from Russia, and their investment in maximizing production.

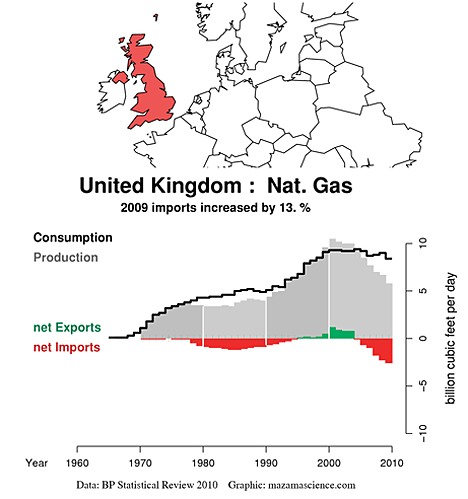

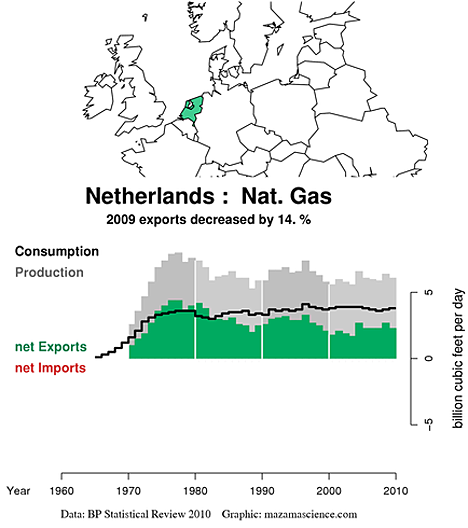

I am, however, drawn to remember Jonathan Callahan’s presentation at the ASPO meeting. Because that is not yet up on the ASPO site I am going to include my review of it, as it drew the same conclusion as I. The bit that is important is the contrast between the British way of developing their oil reserve, and that of the Dutch.

Jonathan used representative plots from the series for his talk, beginning with the UK.

Noting that the UK used town gas (made from coal) until 1959, when the first LNG was imported from LA, gas in the UK was privatized in 1986 and reached peak production in 2000, becoming a net importer of natural gas in 2004. This last winter it was necessary, on three occasions, for the National Grid to issue “Gas Balancing Alerts”, where industrial consumers should reduce use to protect domestic consumers. The situation is anticipated to get worse.

He contrasted this way of managing a resource with that of the Dutch, who have the large Groningen Gas field but which they have managed in a much more conservative way. With their different management philosophy they have retained a considerable margin for the future, over the same time interval.

I would suggest that we are increasingly seeing the Russians follow the British model, while the Saudi’s are moving toward the Dutch model. Such changes will likely impact future supplies.

I wanted to mention, too, that in the near future, I plan to shift the focus of my Tech Talks to cover issues more closely related to my discussions in this current post. I plan to start to write about the different countries that have oil reserves (or had) and what we know about them. The idea, in much the same way as with the technical talks, will be to provide an informative set of background notes, so that, for example, if the topic of the Yamal gas fields comes up, you would know a little about where they are (a peninsula in Russia), and how much gas (maybe 30 trillion cubic meters) is there, as well as how soon they will be developed (not this year).