With the release of Why the “Peak Oil” Theory Falls Down — Myths, Legends and the Future of Oil Resources by Peter M. Jackson, Cambridge Energy Research Associates (CERA) attempts to cast doubt on the credibility of those with imminent, empirically-based concerns about our future oil supply.

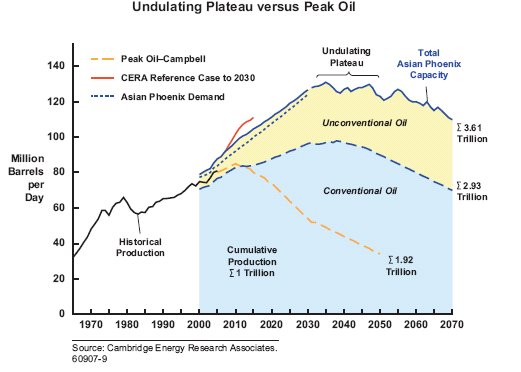

CERA’s “Decision Brief” requires a response because since 1870, the health of the world’s economies have hinged on a secure, dependable and growing flow of “conventional” oil. Their forecast, shown in Figure 1, predicts that the oil supply will continue to grow and sustain economic growth.

Figure 1 — Click to Enlarge

We shall have much more to say about CERA’s forecast later. For now, it is sufficient to note that CERA’s analysis is lacking. The world’s oil supply will not continue to grow to meet ever-rising global demand, and worse, the consequences could irrevocably damage global economies. Such an outcome would have harmful effects on people’s lives. So, this debate is not “academic” — much depends on a correct analysis of the future oil supply.

1. What is “Peak Oil”?

Peak Oil is the theory, with resulting hypotheses, tested with data, that the world’s incremental production of conventional oil over time will reach some high water mark and decline thereafter. There are a number of ways to define “conventional” but, for our purposes here, such oil consists of crude oil, condensate and natural gas liquids.

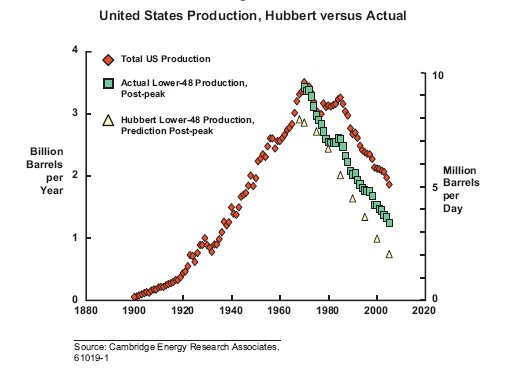

Conventional oil production is usually measured as the quantity extracted over time. For example, the United States produced 6.88 million barrels per day (mbd) of conventional oil in August, 2006 according to data provided by the Energy Information Administration (EIA). The world as a whole produced 81.55 mbd during the same month. The peak oil hypothesis claims that world production will reach an apex and decline, analogous to the production profile shown in CERA’s graph for the United States in Figure 2 below.

Figure 2 — Click to Enlarge

As Figure 2 clearly demonstrates, the peak of United States oil production measured in billion barrels per year for crude oil plus condensate occurred in 1970. We will have more to say about CERA’s analysis of this graph in section 3 below. Notwithstanding any subtleties of interpretation, it is impossible to deny that the U.S. peak did occur and thereafter, production never reached the 1970 high water mark ever again.

No one, including CERA, doubts that a peak in world conventional oil production will eventually occur; it is only a matter of when it will occur. As Figure 1 shows, CERA believes that the apex of production will happen circa 2040. Those putting forth the peak oil hypothesis simply disagree about the timing. Although estimates vary, most of us agree that the peak will occur sometime before 2015, a scant 9 years from now. Within that range, some think the current plateau in oil production signals that the peak is now while others put the peak elsewhere in the coming decade. If this hypothesis is correct, the world will have little time to mitigate the problem, as outlined in Peaking of World Oil Production: Impacts, Mitigation & Risk Management by Robert L. Hirsch (SAIC), Roger Bezdek (MISI), Robert Wendling (MISI) published in February, 2005.

A final word about what peak oil is not: the hypothesis set forth here is not a catastrophist prophecy that the world is running out of oil. Once the world production does peak, views vary as to how severe the decline rate will be thereafter. Many reputable people from the oil & natural gas industry and elsewhere are concerned about peak oil. We are not a doomsday cult.

[editor’s note, by Dave Cohen] It will not be possible here to cover all the necessary arguments which a neutral observer might wish to see in order to make a judgement in this debate. In particular, aboveground political risks that might “limit upstream investments” as CERA put it, such as in Russia and elsewhere, are not covered here. Nor have we addressed potentially explosive geopolitical situations such as the Iraq civil war or Iran’s nuclear ambitions —Middle Eastern tensions could have catastrophic effects on global oil production. We have not been able to include logistical concerns eg. the global shortage of drilling rigs. The alarming trends in world oil exports and declining discoveries which cause us genuine concern are not covered either; for example, conventional oil discoveries peaked in the 1960’s and, as a result, the world’s largest oil fields, which were found first, are now decades old and aging more with every passing year.

2. Reserves Versus Production Flows

The question of recoverable reserves estimates versus production flows is central to the argument about the timing of peak oil. CERA states that “Reserves/Resource Definitions and Estimates Cloud the Debate”. We agree. You will note that our definition of “peak oil” above does not mention reserves at all but, rather, focuses on production flows measured as the quantity extracted over time. Recoverable reserves are almost orthogonal to the debate outside the simple observation that these must exist before any oil can be extracted. The peak oil hypothesis focuses on realistic geological, technical and economic constraints on current & future oil production. A detailed example pertaining to future production will suffice.

Great fanfare in the press accompanied Chevron’s successful Jack #2 test well in the ultra-deepwater Lower Tertiary basin of the Gulf of Mexico. Press accounts such as Business Week’s Plenty of Oil–Just Drill Deeper: The discovery of reserves in the Gulf of Mexico means supply isn’t topping out highlighted the estimated recoverable reserves numbers, which were given in the range 3 billion (Gb) to 15 billion barrels of oil with emphasis on the latter figure. Press releases related to the new “Decision Brief” have been similar, for example MSNBC’s World oil supply still plentiful, study shows in which it is stated that

Cambridge Energy Research Associates said in a report that the world has some 3.74 trillion barrels of oil left — enough to last 122 years at current consumption rates and triple the amount estimated by “peak oil” theorists.

Although CERA states that huge reserves estimates cloud the debate, they continue to promulgate them.

Reading the “fine print” about Jack #2, it became apparent that there were extremely challenging hurdles to overcome in order to actually produce this oil. These included, among other things, the need for drilling equipment beyond the limits of current technology, huge capital expenditure requirements before first production could begin and the further necessity of doing additional tests to find out whether the geology of the reservoirs would permit sufficient oil flow rates to make the play economic to produce. At this time, Chevron and its partners will do additional appraisals next year. No decision has been made yet as to whether development of the Jack field will go forward.

So, it was with some surprise that CERA asserted the following in a press release dated September 6, 2006, based upon their August, 2006 Private Report Expansion Set to Continue: Global Liquids Capacity to 2015.

The most material new resource in the deepwater Gulf of Mexico is the Lower Tertiary Eocene…. [includes the Cascade, Chinook, Saint Malo, Jack, Das Bump, Stones, Hadrian and Great White fields]

A production test [Jack #2] is under way to assess the producibility of the deep Wilcox reservoir. Assuming a successful test, a capacity of 800,000 barrels per day [kbd] is projected from the Eocene trend of fields by 2013-14, plus capacity from any subsequent discoveries. [passage from the CERA report referenced above]

As the text quoted indicates, with its private clients, CERA does not focus on reserves. The 800/kbd is a production rate, not a reserves based number. However, these are the take home points— CERA has added in productive capacity from the Gulf of Mexico, as shown in Figure 3, for the Wilcox play although it is not clear yet whether some of these fields will even be produced given the constraints on production mentioned above. Furthermore, CERA’s production flow estimate is at least 300/kbd higher than any other independent estimate we could find for production in the 2013 period.

Figure 3 — Click to Enlarge

What Figure 3 highlights, which is not found anywhere in the CERA’s peak oil “Decision Brief”, is their assumption —shared by us— of a 5% decline rate in existing oil production over time. As you can see, what CERA calls the “Upstream Oil Challenge” is a race between bringing new conventional oil production on-stream and declining production in existing oil fields such as Mexico’s giant offshore Cantarell field. The assumed global decline rate is crucial. The hard & expensive problem of bringing new oil production on-stream is compounded over time by an exponential decline rate which requires the world to run faster to stay in-place, let alone move forward to meet increasing demand. Moreover, some of the conventional oil CERA is counting on to meet the demand challenge involves fields under appraisal or “yet to find” resources — this is oil that does not yet exist. Of the 3.74 trillion barrels of oil CERA claims remains to be exploited —see section 3 below— 0.758 trillion barrels comes from “exploration potential” ie. it has not yet been discovered but, presumably, is recoverable despite unknown geological, technical and economic constraints on production of a non-existence resource.

For Saudi Arabia, now the world’s 2nd biggest producer, Kjell Aleklett, President of ASPO (Europe) has this to say:

As an example, CERA thinks that Saudi Arabia needs more than 2 million barrels per day from fields that not have been found today. Shaybah is the latest giant field that Saudi Arabia started up in 1998 with a production capacity of 500,000 barrels per day. In principle, CERA is saying that the production equivalent of 4 Shaybah fields will be found and put into production during the next 9 years in Saudi Arabia.

As you can readily see, there is more to the peak oil problem than meets the eye as detailed in CERA’s latest “Decision Brief”. The peak oil hypothesis is both complex and worrisome.

3. Unconventional Oil — Substitutes

As shown in Figure 1, the ability of the world to bring substitutes for conventional oil on-stream figures prominently in CERA’s analysis both now and in the future. They define these substitutes as follows —

However, demand for refined products could outstrip conventional crude oil production. Conventional crude oil production excludes liquids production from heavy oil sands, ultra-deepwater oils, gas-related liquids (condensate and natural gas liquids), gas-to-liquids (GTL), and coal-to-liquids (CTL).* This means that additional sources of liquid fuels will be needed in abundance and in a timely manner, assuming relatively strong global economic and oil demand growth. Technology will promote a widening of the concept of conventional oil, as has occurred over the history of the industry.

Let us get some clarifications and additions out of the way. First, in our more generous definition of conventional oil, condensates and natural gas liquids are already included. Second, whether ultra-deepwater production is conventional or not is a red herring —it makes no difference to the debate. Heavy oil sands —sometimes called tar sands— refers to both the production of oil sands in Alberta, Canada by means of in situ heating or mining methods and the production of heavy tar in Venezuela’s Orinoco Basin. Additional substitutes CERA considers include ethanol from cellulosic biomass or corn, from sugar cane (as in Brazil), diesel fuel from soybeans, and the like. Also not mentioned directly in the quote above is future production from oil shales. Taken altogether, these new sources plus additional conventional oil production are the source of the numbers quoted in the mainstream press.

CERA believes that the global inventory is some 4.82 trillion barrels of resources of which about 1.08 trillion barrels have been produced already. Therefore, there is as much as 3.74 trillion barrels of conventional and unconventional resource remaining, and this order of magnitude of resources will allow productive capacity to continue to expand well into this century.

[Note: for example, CERA estimates 0.707 trillion barrels to be produced from oil shales]

Although CERA asserts that “those who believe that a peak is imminent tend to consider only proven remaining resources of conventional oil, which at present they believe to be approximately 1.2 trillion barrels”, any cursory glance at stories on The Oil Drum or much of the published peak oil literature will readily see that substitutes for oil are analyzed all the time. The reason for this is both simple & compelling —since we believe the timing of peak oil is sooner rather than later, we are very concerned about whether substitutes will be available to ease the transition away from conventional oil to create a different energy mix in the future.

Unfortunately, our analysis reveals the same worrisome pattern over and over again for substitutes. The three principal problems with substitutes are listed below.

- Scalability by volume —new liquid fuel resources can generally only provide a small percentage of the total volumes of liquid fuels supplied by conventional oil. For example, a National Academy of Sciences report came to the following conclusion.

The real risk from all these planned ethanol plants is that they’ll use up vast quantities of corn. America’s entire corn and soy crop could supply fuel volumes equal to just 12% of gasoline demand and 6% of diesel demand, notes a University of Minnesota ecology professor, David Tilman, an author of the July 25 Proceedings article.

- Scalability in time —even where there is a vast resource, liquid production flows from substitutes are slow to ramp up. As a result, in the case of exponentially declining oil production not replaced by new conventional oil sources, substitutes will not make up shortfalls incurred in the short-term. To make matters worse, similar remarks apply to production of new conventional oil eg. recovering stranded oil by means of CO2 injection enhanced oil recovery (EOR).

- Low Energy Returns —this refers to energy returned by a production process for a fuel divided by the energy required to produce the fuel —standardly abbreviated as the EROEI. Both substitutes and, increasingly, new conventional oil production, have lower EROEIs tending toward the limit = 1. The closer one gets to the limit, the smaller the marginal returns. The EROEI term need not be confined to fossil fuel energy inputs but may include all of the economic costs associated with developing an energy fuel resource, depending on where the boundaries for the calculation are set. The general idea here is that the world is not like Spindletop in the Southeast of Texas anymore. You can not just sink a drillpipe and get a gusher anymore. The so-called “low hanging” fruit is gone and what is left is energy-intensive to develop & produce.

In an example of points #1 & #2 above, CERA believes that “GTL and CTL collectively may well represent 6 percent of global productive capacity by 2030”, an unimpressive fraction of liquids production as estimated for that time period. Obviously, in the shorter term within the next decade, the percentage of gas-to-liquids or coal-to-liquids that will substitute for conventional oil will be negligible. Similar remarks apply to oil shales. If you believe, as we do, that the peak of production will come sooner rather than later, there is genuine cause for deep concern.

CERA explicitly acknowledges the scalability problems as the timescale of Figure 1 indicates. Despite their belief that the economics of unconventional substitutes is favorable, however, CERA does not seem to take net energy returns into account. These are already problems with the production of the oil sands in Canada, our most successful substitute so far. Capital expenditure costs are soaring to support new incremental production measured in increments of 100/kbd, thus making it harder to attract capital investments. Total production from the sands may be in the 2 to 3/mbd range by 2015, although estimates vary given the ongoing environment, logistic and net energy concerns there.

The bottom line as shown in Figure 1 from the CERA “Decision Brief” is that conventional oil production will conveniently increase until substitutes are ready to come on-stream much farther down the road, thus providing a seamless transition to the new liquid fuel sources. If CERA is mistaken about that production, substitutes will be of little avail in making up shortfalls.

4. Peak Oil Modeling Theory & Data

CERA berates those concerned about peak oil, labeled peakists in their document, for using questionable data and analysis methods. This passage is worth quoting in full.

We are also struck by three characteristics of the current debate:

- The peakist argument is not grounded in a credible systematic evaluation of available data.

- The peakist arguments cluster around the questionable model described by the late American geologist M. King Hubbert. This is a technique that fails to recognize both that recoverable reserves estimates evolve with time and are subject to constant and often significant change. It also underplays the far-reaching impact of technological advances.

- Some of the peakists are, interestingly, shifting their emphasis away from running out, in terms of physical resources, to issues that we believe are significant–infrastructure and aboveground risks.

Here we must take exception to CERA’s characterization of peak oil research, especially here at The Oil Drum. Not only have we tracked CERA’s bottom-up project- by-project analysis in the past —a complete list of stories is too long to enumerate here— but we also avail ourselves of whatever data we can find, such as the Megaprojects Database compiled by Chris Skrebowski, editor of the Petroleum Review.

Space limitations preclude going into much detail here, but suffice it to say that it is a bit disingenuous for an organization such as CERA, a wholly-owned subsidiary of IHS Energy, to charge money for its reports for paying clients and then turn around and tell us that we are unfamiliar with the current & future oil production data. This points up a larger issue which Matt Simmons has brought to the forefront of public attention: data transparency in the world’s oil industry. Just as we can not see some of CERA’s field-by-field production projections, we also can not see an historical production profile or this year’s monthly production data for Ghawar in Saudi Arabia, the world’s biggest oil field. For an issue so crucial to the health of world economies, the lack of readily accessible data is scandalous. A pro bono approach would make data available to independent organizations that have an interest in analyzing it.

CERA’s critique of Hubbert modeling is quoted below.

Despite his valuable contribution, M. King Hubbert’s methodology falls down because it does not consider likely resource growth, application of new technology, basic commercial factors, or the impact of geopolitics on production. His approach does not work in all cases–including on the United States itself–and cannot reliably model a global production outlook. Put more simply, the case for the imminent peak is flawed. As it is, production in 2005 in the Lower 48 in the United States was 66 percent higher than Hubbert projected [see Figure 2].

M. King Hubbert’s logistic production curve is not a physical model, so naturally it does not take into account technology, geopolitics or economics. It is simply a modeling tool which provides one more independent line of evidence that peak oil analysts use to investigate their hypothesis. Other lines of evidence, as discussed above, do take into account “real world” data. We accept CERA’s criticism that such production data do not always follow the logistic (bell) curve that forms the basis of the model. However, unless some geopolitical perturbations occur or the oil producing region is relatively immature, it is usually the case that deviations from the logistic are seen in the tail end of the curve after the apex of production has already occurred. See the Graphoilogy weblog for additional information.

However, the criticism that the United States does not follow Hubbert’s predictions does not hold water. While it is true that Hubbert did not foresee Prudhoe Bay and other Alaskan production, or the deepwater developments in the Gulf of Mexico, it is nevertheless the case that 1) U.S. production did indeed peak just about when Hubbert said it would and 2) despite reserves growth during the subsequent period in the tail end of the curve, actual oil production never again reached its 1970 peak —it has declined ever since. These are the salient observations to bear in mind.

Moreover, CERA makes some observations that cast doubt on their understanding of Hubbert’s methods and further refinements to it. CERA makes the following claim:

Hubbert’s method also requires an accurate knowledge of the ultimate recoverable reserves of any area. However, numerous studies point to the fact that, during the life of oil fields, resource estimates often increase as understanding of the field improves and new technology is applied.

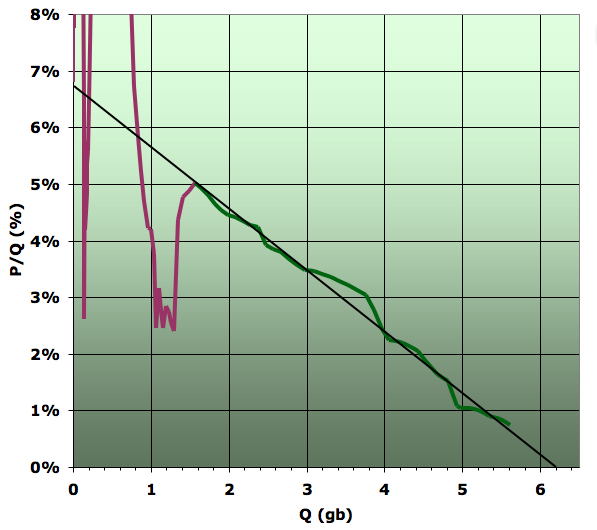

In fact, a Hubbert Linearization based on cumulative production yields an estimate of the ultimately recoverable reserves (URR) —these are not known in advance. For example, this linearization for Romania indicates that the URR will be 6.2 billion barrels and that there is a decline rate of approximately 6.7%.

Figure 4 — Click to Enlarge

Linearization of Romanian production (the y-axis the ratio of annual production to cumulative production, x-axis is cumulative production. Linear fit is to the region for 1955 on (green data – plum data is prior to 1955).

Source: American Petroleum Institute (courtesy J. Laharrere) for 1857-1958, and BP for 1965-2005 (includes NGLs). Production data for 1959-1964 is linearly interpolated between the two data sets.

Kuwait provides another important example of using the Hubbert linearization to estimate recoverable reserves.

At the Oil Depletion conference (hosted by the Energy Institute) held in London on 7th November, Dr Kenneth Chew, a Vice President of IHS Energy [CERA’s parent company] reported proved and probable reserves (2P) for Kuwait of around 52 billion barrels… This is approximately 51% of the proved reserves reported in the BP statistical review that stand at 101.5 billion barrels. This tends to support recent reports of Kuwaiti reserves being substantially overstated.

A linearization for Kuwait yields an estimate of 40 billion recoverable barrels there, an number more in line with IHS Energy’s conclusions than OPEC’s “official” estimate of 101.5 billion barrels.

The bottom-line is that those studying the peak oil hypothesis are not wedded to Hubbert’s theory, which have been refined over the years. However, these mathematical tools provide a sometimes startlingly accurate model of real world production data, especially where the data set is completely known such as in the United States and Norway —which is also in decline.

5. Our Conclusions

In Figure 3, CERA shows current productive capacity at 88.7/mbd. This number was set in the Spring of 2006 and has not changed since, to our knowledge. In fact, according to the EIA, actual conventional oil production (as defined here) was 81.55/mbd in August, 2006, a figure which excludes the category other liquids —these include refinery gains, biofuels, etc. We can not know the source of the discrepancy between the two numbers. However, if actual production bears the same relationship to productive capacity in the future as it does today given CERA’s projected demand, there appears to be genuine cause for worry belying their rosy forecast.

To quote CERA’s Peter M. Jackson once more:

In these times of relatively tight supply, high and volatile oil prices, and anxiety about energy security, the peak oil debate is raging once more. This debate reflects one of the most important issues facing not only the energy industry, but the world at large. Those believing in a doomsday scenario argue that peak oil is near and that the world is ill prepared for it. If world oil production were to enter a sharp downward spiral in the next several years, the ramifications for the global economy and geopolitics would be severe and potentially catastrophic.

For many years CERA has maintained a consistent contrary view. CERA does not agree with the simplistic concept of an imminent peak in oil production nor with the idea that oil will “run out” soon thereafter.

We are concerned that CERA has “maintained a consistent contrary view” and not taken the peak oil hypothesis seriously until now. We can only agree that “this debate reflects one of the most important issues facing not only the energy industry, but the world at large.” We hope our response demonstrates that the peak oil hypothesis is anything but simplistic. Furthermore, no one here or elsewhere is claiming that conventional oil will “run out” anytime soon. Rather, the peak oil view is an evolving, sophisticated take on conventional oil production and the viability of substitutes to replace continuing demand for this paramount fossil fuel in the face of inevitable declines in available supply. Only the timing of such declines is at issue here. We can also only add that denial in the face of potentially very threatening events is a powerful force in the human psyche.

In conclusion, the peak oil debate is still alive and well, not moribund, as CERA and some mainstream media accounts would have you believe. We at The Oil Drum are not persuaded in the least by CERA’s often —and disappointingly— weak arguments which, ultimately, depend on many assumptions we consider unrealistic.

Dave Cohen

TOD Senior Contributor

News Contacts: theoildrum @ gmail.com

The Author: davec @ linkvoyager.com