The story of oil limits is one that crosses many disciplines. It is not an easy one to understand. Most of those who are writing about peak oil come from hard sciences such as geology, chemistry, and engineering. The following are several stumbling blocks to figuring out the full story that I have encountered. Needless to say, not all of those writing about peak oil have been tripped up by these issues, but it makes it difficult to understand the “real” story.

The stumbling blocks I see are the following:

1. The quantity of oil supply available is primarily a financial issue.

The issue that peak oil people are criticized for missing is the fact that if oil prices are high, it can enable higher-cost sources of production–at least until these higher-cost sources of production prove to be too expensive for potential consumers to buy. Thus, high price can extend oil production for longer than would seem possible, based on historical patterns. As a result, forecasts based on past patterns are likely to be inaccurate.

There is a flip side of this as well that economist have missed. If oil prices are low (for example, $20 barrel), the economy is likely to be very different from what it is when oil prices are high (near $100 barrel, as they are now).

When oil prices are low, it is likely that oil production can be expanded rapidly, if desired, because it takes little effort to extract an additional barrel of oil. In such an atmosphere, it is easy to add jobs, because new technology, such as cars and air conditioners made and transported using such oil, is affordable. Growth in debt makes considerable “sense” as well, because additional debt enables more oil use. It is likely that this debt can be repaid, even with fairly high interest rates, given the favorable jobs situation and growing economy.

With high oil prices, there is a constant uphill battle against high oil prices that rubs off onto other areas of the economy. Businesses tend not to be too much affected, because they can fix their problem with high oil prices by (a) raising the prices of the finished goods they sell (thereby reducing demand for their goods, leading to a cutback in production and thus jobs) or (b) saving on costs by outsourcing production to a lower-cost country (also cutting US jobs), or (c) increased automation (also cutting US jobs).

The ones that tend to be most affected by high oil prices are wage-earners, who find that their chances of obtaining high-paying jobs are lower, and governments, who find it increasingly difficult to collect enough taxes from wage-earners to pay for all of the promised benefits.

2. The higher cost of oil extraction in the future doesn’t necessarily mean that the price consumers can afford to pay will rise.

In peak oil groups, I often hear the statement, “When oil prices rise, . . .” as if rising oil prices are a given. Businesses may be afford to pay more, but individuals and governments are finding themselves in increasingly poor financial condition. Quantitative easing isn’t getting money back to individuals and governments–instead, it is inflating the price of assets–a temporary benefit until asset price bubbles break, as they have in the past, or interest rates rise.

The limit on oil supply is what I would call an affordability limit. Young people who don’t have jobs can’t afford to buy cars. If young people graduate from college with a huge amount of educational loans, they can’t afford to buy houses either. Within the US, Europe, and Japan, we seem to have already hit the affordability limit on the amount of oil we are consuming. Economic growth is low, as oil consumption declines.

The risk, as I see it, is that the price consumers can afford to pay will drop below the cost of extraction. It is this drop in oil price that will cause supply to fall. If the drop in price is very great, we could see a very rapid decline in oil production, especially in countries with a high cost of production, such as the US and Canada. Some oil exporters may find themselves in difficulty, because they are no longer able to collect the tax revenue they were depending upon. This could lead to uprisings in the Middle East and possibly lower oil production in affected countries.

I should point out that it is not just the peak oil community that seems to think rising oil prices can continue indefinitely. Economists and those forecasting climate change seem to share this view. If oil and other fossil fuel prices can rise indefinitely, then a very large share of fossil fuels in the ground can be extracted.

3. There is widespread confusion about what M. King Hubbert really said about the shape of the decline curve.

M. King Hubbert is known for showing images of world oil supply which seem to show that oil supply will rise and then fall in a symmetric pattern. In other words, if it took 50 years for oil production to rise from level A to level B, it should also take 50 years from oil production to fall from level B back to level A. This relatively slow downslope gives comfort to many people concerned about peak oil because they believe that the slow downward path in oil production will be helpful in mitigation strategies.

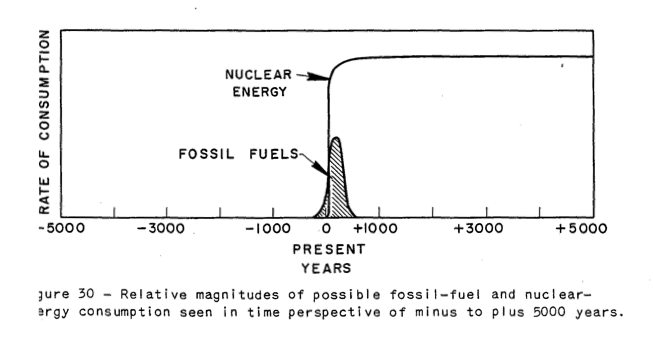

In fact, if we look at Hubbert’s papers, we discover that Hubbert only made his forecast of a symmetric downslope in the context of another energy source fully replacing oil or fossil fuels, even before the start of the decline. For example, looking at his 1956 paper, Nuclear Energy and the Fossil Fuels, we see nuclear taking over before the fossil fuel decline:

Hubbert’s 1976 paper talks about solar energy being the substitute, instead of nuclear. In Hubbert’s 1962 paper, Energy Resources – A Report to the Committee on Natural Resources, Hubbert writes about the possibility of having so much cheap energy that it would be possible to essentially reverse combustion–combine lots of energy, plus carbon dioxide and water, to produce new types of fuel plus water. If we could do this, we could solve many of the world’s problems–fix our high CO2 levels, produce lots of fuel for our current vehicles, and even desalinate water, without fossil fuels.

Clearly the situation today is very different from what Hubbert was envisioning. Neither nuclear or solar energy is providing a sufficient substitute for our current economy to continue as in the past, without fossil fuels. We have a huge number of cars, tractors and trucks that would need to be converted to another energy source, if we were to move away from oil.

If there is not a perfect substitute for oil or fossil fuels, the situation is vastly different from what Hubbert pictured. If oil supply drops (perhaps in response to a drop in oil prices), the world economy must quickly adjust to a lower energy supply, disrupting systems of every type. The drop-off in oil as well as other fossil fuels is likely to be much faster than the symmetric Hubbert curve would suggest. I wrote about this issue in my post, Will the decline in world oil supply be fast or slow?

4. We do have an estimate of the shape of the downslope when there is not a perfect substitute the resource with limits.

There are many historical examples of societies that found a way to greatly increase food supply (for example, by clearing land for new fields, or by learning to use irrigation). Peter Turchin and Sergey Nefedof researched the details underlying eight agrarian societies of this type, documenting their findings in the book Secular Cycles.

These researchers found that at first population was able to increase, because of the greater ability to grow food. Population typically increased for well over 100 years, as population gradually expanded to match the new capacity for growing food.

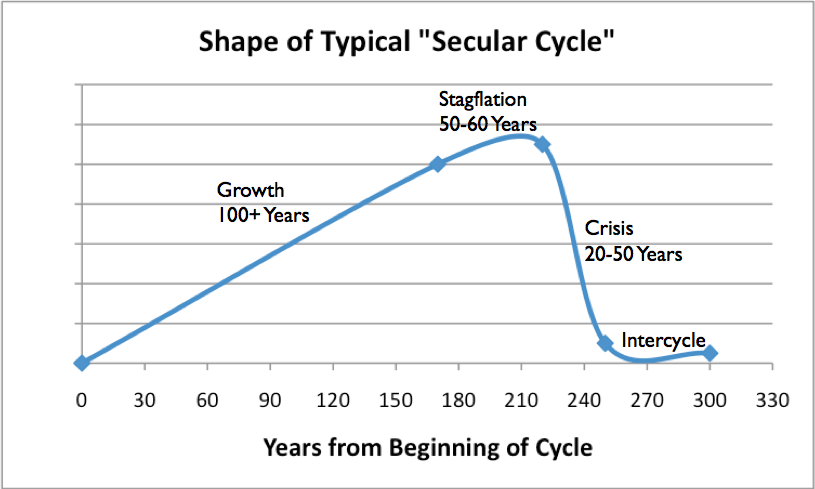

At some point, the economies analyzed entered a period of stagflation, during which wages of the common worker stagnated, because an early limit had been reached. Population had reached the level the new resources could comfortably support. After that point, growth slowed. New babies were born, but additional area for crops was not being added. Adding more farmers didn’t increase output by very much. Debt also increased during the stagflation period. The chart below is my estimate of the general pattern of population growth found by Turchin and Nefedov, in the years following the addition of the new capability to grow food.

Eventually, a crisis period hit. One major issue was a continuing need to pay for government programs had been added during the growth and stagflation periods. With the stagnating wages of workers, it became increasingly difficult to collect enough taxes to pay for all of these programs. Debt repayment also became a problem. Food prices tended to spike and became quite variable. Governments became increasingly susceptible to collapse, either because of outside forces or internal overthrow. Population was reduced through a combination of factors–more wars and a weakened population becoming more susceptible to epidemics.

It seems to me that our current situation is somewhat analogous to what has occurred in these secular cycles. The world began using fossil fuels in significant quantity about 1800, and reached the stagflation phase in the early 1970s, when US oil production began to decline. We are now encountering the classic symptom of resources not rising as fast as population–namely, wages of the common workers stagnating. Fossil fuel prices tend to spike and be quite variable. Government financial problems we are seeing today sound very similar to what past civilizations experienced, when they hit resource limits.

We don’t know that our current civilization will follow the same shape of downslope as earlier civilizations that hit limits, because our economy is not an agrarian economy. We are now dealing with a globalized civilization that depends on international trade. Jobs are much more specialized than the past. But unless there is a miraculous growth in cheap energy supply that can fix our problems with young workers not finding good-paying jobs, there seems to be a good chance we are headed in the same general direction.

5. High Energy Return on Energy Invested (EROI) is a necessary but not sufficient condition for an energy source to be a suitable substitute for oil.

We are dealing with a complicated financial system, but EROI is a one-dimensional measure. It can tell us what won’t work, but it can’t tell us what will work.

Any substitute for oil (for example, a transition to battery-operated cars) needs to be considered in the context of what the total cost will be of a transition to a new system, the timing of these costs, and who will pay these costs. It is important to consider what impact these costs will have on those who already are at greatest risk–namely, individuals who are having difficulty earning adequate wages, and governments that are finding it increasingly difficult to pay benefits that have been promised in the past. If individuals are being asked to pay higher costs, this will reduce discretionary income to be used for other purposes. If a government is already stressed, adding energy related stresses may “push it over the edge,” making it impossible to collect enough taxes for all of the promised programs.

6. It is easy to be influenced by the fact that everyone likes a happy ending.

People coming from a peak oil perspective often accuse the main street media of putting forth a “happily ever after” version of the oil story. But I think there is a temptation of the peak oil community to put together its own “happily ever after” story.

The main street media version says that the economy can continue to grow, and we can continue to drive cars and go to our current jobs, despite a need to change to different kind of fuel supply.

The peak oil version of the story often seems to say, “If we conserve, and learn to be happy with less, there won’t be too much of a problem.” Some seem to suggest that hoarding solar panels for our own use can be helpful. Others seem to believe that society as a whole can be transformed by adding more solar and wind power to our current electrical system.

The difficulty with adding a new energy source in quantity is that we don’t have any such energy source that can truly act as a cheap substitute for oil. If solar PV or wind, or some other new energy source were truly a good substitute for fossil fuels, such a fuel would be exceedingly cheap and could be used with today’s vehicles. Governments could improve their financial condition by taxing this new energy resource heavily. It would be obvious to everyone that by adding much more of this miraculous new fuel, we could add many more good-paying jobs, especially for our young workers.

Unfortunately, I cannot see that we have found a good oil substitute. Instead, quantitative easing is temporarily hiding financial problems of governments and individuals by forcing interest rates to be very low. This makes cars and homes more affordable, and keeps the amount of interest paid by the federal government very low. We know that these artificially low interest rates are temporary, though. Once they “go away,” tax rates will need to rise, and asset prices (stock prices, bond prices, and home prices) will drop. Oil prices may very well decline below the cost of production. We will again be at risk of heading down the “Crisis” slope shown in Figure 3.

The Oil Drum Going to Archive Status – Important Story Still to Be Told

The peak oil community is filled with many dedicated volunteers coming from a variety of backgrounds. I particularly commend The Oil Drum volunteers for sticking with the issue as long as they have. Many of them have discovered at least some of the pitfalls of the traditional “peak oil” story listed above.

I will continue to tell the story of oil limits on my site, Our Finite World. In the near future, I am also giving a number of talks about the issue to actuarial groups. I need to get the story documented in other formats as well–in book form and in the actuarial literature. The fact that The Oil Drum is going to archive status doesn’t mean that there isn’t a real, important story to be told. It isn’t quite the original peak oil story, but it is closely related.