Yesterday, I was musing over the fact that global oil supply has pretty much stopped growing in 2012, and that this seems strange given that prices are falling. My hypothesis yesterday was: the global economy is still growing so oil demand must be still growing. Thus with flat supply, prices should be growing. The fact that they are falling must thus represent fears about the future (Eurozone triggered financial implosion).

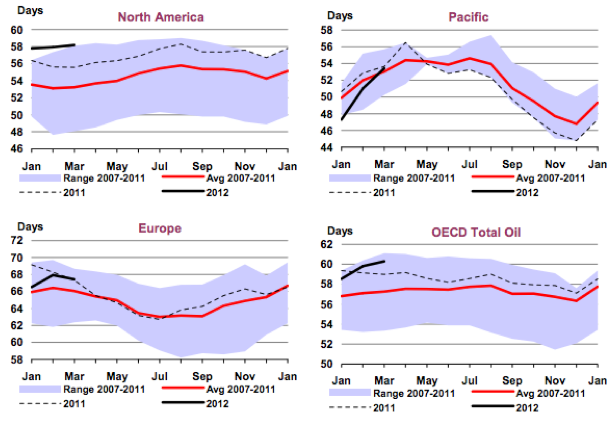

If this were true, we’d expect it to show up as oil inventories getting tight (as current demand was out of line with prices being reduced by feared future collapse in demand). The data on global oil stocks are highly imperfect – they only extend to the OECD, and they are generally several months behind. Such as they are, the graph above (from the May IEA OMR and expressed as days of demand) shows the picture. It does not appear to be consistent with the hypothesis above – stocks are very high in the US (presumably a continuation of the WTI-Brent anomaly), and normal to above average elsewhere. The data extend through the end of March.

That leads me to question the idea that global oil demand is growing in 2012. Roughly speaking my reasoning for thinking that it would be is:

- The US economy is still growing (albeit sluggishly)

- Europe is contracting (but only very mildly)

- Asia is still growing strongly (albeit not at quite as insane a rate as in recent years).

- On balance, then, the global economy must still be growing.

- Generally, when the economy is growing, oil demand grows.

I guess there are two places where the chain of reasoning could break down – either the global economy has been worse off in recent months than I realize, or, the global economy is still growing at a moderate pace but oil efficiency is increasing fast enough at the moment that oil demand is not growing regardless (presumably due to the cumulative effect of the last seven years of high and volatile prices).

Of course, it’s also possible that OECD stocks through March paint a misleading picture – the OECD is only half of global demand these days; maybe the other half is doing something else altogether, and maybe the picture changed substantially in April and May – after all, that’s when the price drop mainly happened:

More to follow, I’m sure, as I remain a bit mystified.