The following guest post is from Jonathan Callahan, a PhD chemist currently working as a data management / information access consultant. Jonathan writes on energy issues and data management at Mazamascience.com.

On June 6 and 7, I attended Opal Financial’s Clean and Green Investment Forum. I was invited to take part in a panel on “Green Energy in Emerging and Frontier Markets”. The forum brought together clean tech entrepreneurs and investors as well as a few academics and analysts and proved very stimulating. The overall vibe was one of optimism and opportunity — we’re talking entrepreneurs and investors here. This post will discuss presentations in the following categories:

- Government policies and private investment

- Utilities and grids

- Electric vehicles

- Batteries and fuel cells

- Biomass and algae

- Wind

- Solar

Disclaimer — Opal Financial paid my airfare and hotel room and waived the conference fee.

Government policies and private investment

Several speakers addressed the importance of government policy action in supporting the adoption of renewable energy during their talks.

The keynote speech was given by Suedeen Kelly, who served three terms as FERC commissioner under Bush and Obama. Kelly emphasized how energy is different from other markets in that it is highly regulated by the government. She foresees significant action on the energy policy front but admits that change can be slow. Kelly described the Federal government’s role as providing the 3 M’s: Money in the form of grants and tax credits; Markets where the government is a large buyer of renewables; and Mandates ranging from open data requirements for public utilities to energy efficiency requirements in government agencies.

Patty Hargreaves described Ontario’s 2009 Green Energy Act (GEA) which aims to position Ontario as a leader in the adoption of renewable energy and the creation of clean tech jobs. Important features include a generous feed in tariff (20 years at 8x market rate) which has resulted in the creation of 15,000 jobs in the local solar industry. Also found in the GEA are simplified regulations for installation of solar panels as well as the closure of all coal fired plants by 2014. (By comparison, Washington state residential incentives amount to $0.54/KWh (7x Seattle retail) until 2020 for systems with Washington sourced components. Washington also plans to phase out coal by 2025.)

Ed Trello said “These are exciting and scary times for utility executives.” He described our aging energy infrastructure and suggested that $1 Trillion in capital will need to be spent on new generating capacity in the coming decades. Utility executives are unsure of what role renewables will (must?) play as there is no national energy plan. The US still has lots of coal and natural gas and these are the safe bets for many executives. (I’ll add my voice to those complaining about the lack of any Federal Renewable Portfolio Standards (RPS) or of any national policies aimed at decoupling utility revenue from electricity sales.)

Other speakers emphasized the importance of tax incentives and RPS in jump starting the US renewables market. Unfortunately, these are implemented primarily at the state and local level resulting in around 1900 financially separate electricity markets in the US. (Check out the DSIRE database.) Investors in energy technology have a difficult time penciling out returns with all this complexity, especially given the temporal nature of credits, rebates and RPS. All of these are subject to change every election cycle.

A few speakers described how venture capital has been slow to move into the renewables space as rates of return are perceived to be low despite the fact that the energy market in the US is a multi-Trillion dollar market. Clean tech is capital intensive and slow moving. It’s hard to imagine Google- or Facebook-like returns when manufacturing solar panels is a lowest-cost commodity market and returns on utility grade systems are subject to regulation.

Several institutional investors, on the other hand, described seeing increasing demand for “green” investment choices in retirement plans. Large net worth family funds are also seeking out green investments as a younger generation takes the reigns and demands alternatives to their parents’ investment choices. With limited investment options, some fund managers seem to see today’s green investments as “getting in early” on what they suspect will be a much broader generational shift in investor sentiment.

Utilities and grids

Based on what I heard from several speakers it seems like focusing on utilities and their electric grid is an excellent place to look for significant efficiency gains.

Lanny Sinkin of Solar San Antonio described how CPS Energy, the nations largest publicly owned utility, did an about face on conservation when they hired a new, younger director a few years back. (There’s that generational issue again.) Instead of lobbying for a new nuclear reactor, the utility now promotes energy conservation and distributed generation with wind and solar projects.

John Loporto of Power Tagging described their technology for sending packets of metadata around on the grid itself, making it easier to know how to reroute during outages and where voltage dips occur. Currently the grid operates near ~120 Volts in order to guarantee that ~110 V is available to each household. By knowing where additional voltage regulators are needed, utilities can reduce operating voltage throughout the grid to ~110 V resulting in a 6% efficiency gain. (Impressive!)

Another speaker talked about investment opportunities for fast-response, grid-scale storage — big batteries. He sees a whole new field of “digital electricity management” emerging and suggested that security concerns may push the development of “micro-grids”.

“Smart grids” didn’t get that much play at this conference even though a couple of people did mention the need to tread very lightly with respect to demand side management. For 100 years, utilities have been intensely focused on customer expectations of reliability and any whiff of intermittency goes against everything they stand for.

Clearly, there is a lot of work and a lot of opportunity for engineers and investors working at the utility and grid level.

Electric vehicles

As is already evident, Peak Oil will affect transportation much more severely than other sectors of the economy as it accounts for a large percentage of the energy used for transportation (95% in the US). The presentations on vehicles showed that steady progress is being made but cost is still a significant barrier to widespread adoption.

Ed Baxter described a new electric vehicle from China, the Zotye electric SUV, that he claims will do a much better job of meeting consumer expectations than current offerings. Marketing material claims it can travel up to 250 miles on a charge. The car should appear in the US sometime in 2012 with a 3 year/36,000 mile warranty as well as a 185,000 mile warranty on the batteries all for $30K. He expects 3 million EVs to be sold by 2015. (No wonder he’s investing in this!)

At a lower price point Mark Frohnmayer of Arcimoto presented their commuter vehicle which is designed to get a single person across town and back without getting wet. As a three-wheeled motorcycle it cuts a lot of corners compared to a real car but he is trying to design a “sustainable vehicle” for the sweet spot that meets perhaps 80% of driving needs — a single person traveling moderate distances without much stuff. Even though these vehicles will be hand built in Eugene, Oregon (of course) he expects to be able to sell them for under $20K.

Obviously Arcimoto is targeting a niche market but how low could the price get with a real manufacturing process and economies of scale? In the face of increasing fuel costs could an inexpensive enclosed electric 3-wheeler find a market among middle class commuters? I think the answer is a definite ‘maybe’. Both presenters agreed that EVs’ current role will be mainly as an extra vehicle for urban driving, not as a replacement vehicle. But urban driving accounts for a lot of miles!

Batteries and fuel cells

On the battery front we heard mostly about fuel cells though Phil Roberts of Ionex Energy Storage mentioned that lithium-ion battery costs are coming down and that graphene-enhanced lithim-ion batteries are moving out of the lab and into production and will dramatically improve charge-time, energy density and cycle life. One of the major uses for grid-scale battery systems is to store and even out the intermittent power coming from wind and solar. As battery technology improves, the viability of intermittent power sources will also improve as we learn to shape power on both the production and demand side.

Fuel cell presenters included folks from the California Fuel Cell Partnership, BTI/Fuel Cells 2000, UTC and First Element Energy.

I have not paid much attention to fuel cells recently after their failure to prove competitive in powering electric vehicles. I was surprised to find out that fuel cells are currently a $1 billion market (85 MW shipped in 2010) that is expected to grow to $5 billion by 2016. There are many different fuel cells with many different operating characteristics for different niche markets but they all offer high reliability, quiet operation and long operational periods. That’s why the military buys them. And telecom has been an early adopter of fuel cells for backup power. (Perhaps nuclear power plants should be required to have fuel cell backup power.)

It turns out there is one area of transportation where micro-fuel cells have caught on but it was a total surprise to me — fork lifts. Apparently, productivity is increased by longer run times and consistent voltage in cold storage. Recharge is only 2-3 minutes which means you no longer need the battery room, the recharge station or the guys manning either of these. Walmart sees an IRR (Internal Rate of Return) of 20% on capital spent on fuel cell forklifts.

Biomass and algae

Of the various sources of renewable energy, biomass is the one we hear the least about, probably because it doesn’t involve high tech innovation. Americans are fanatical about high tech solutions even when low tech solutions are more easily available. (We’ve all heard the US space pen vs. Russian pencil joke.) In northern Europe biomass is more in the forefront. The thing to remember about biomass is that it is baseload as opposed to intermittent wind and solar sources. This means that generators fed by biomass or biogas from animal waste digestors can operate when wholesale prices are high thus earning a higher rate of return on investment.

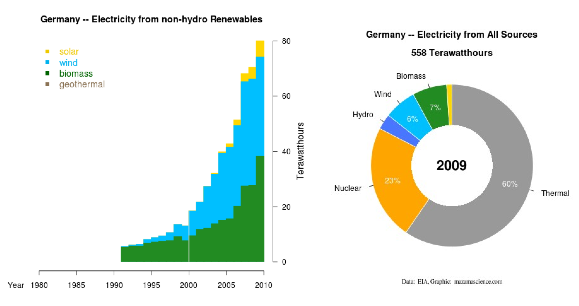

James Johnston of the Center for the Advancement of the Steady State Economy described how regulations in densely populated Europe de-incentivise landfills which thus increases the demand for incineration of waste. By comparison, Carey King of UT Austin stated that 50% of all municipal waste in the US is landfilled. He also described the animal waste resource as 1 billion tons annually — enough to generate over 50 Gigawatt hours of electricity per year (2% of US demand). (I wonder how much of that waste is currently used for fertilizer.) In my own talk on International Energy Trends I presented charts using EIA electricity data that clearly showed the importance of biofuels in some European countries. Figure 1), for example, shows the renewables trends and current state of German electric generation. Despite rapid growth in wind and solar, biomass still accounts for about half of renewable generating capacity.

Algae was the other big biomass theme. Several speakers made the case for algae based biofuels with the following list of reasons (I’m just reporting here, not vetting them):

- algae is 25-50% lipids by weight

- algae produces more lipids per acre than soy or canola

- algae uses 1/7 the water of soy

- algae’s proteins are often more valuable than the biodiesel generated

- refinery costs are lower

Jonathan Trent of NASA Ames had perhaps the most interesting talk in which he described the OMEGA project. Thinking outside the box, his group looked at California’s 2 billion gallons of wastewater per year (water + fertilizer) and algae’s prolific growth rates and determined that the only impediment to large scale algae farms was the cost of land. But moving the algae farms to floating pens just offshore solves that problem along with the need to stir the algae and dissipate the heat generated. Given that much of the world’s population lives in coastal cities without adequate sewage treatment, this idea may have legs.

Wind

Wind advocates at the conference reinforced the notion that the cost of wind is rapidly approaching grid parity in many locations.

Mark Crowdis of Think Energy described how “large wind” is growing in Europe and China and how capacity factors in the US have increased from 30% in 2003 to 50% today as turbines get both larger and lighter. Another speaker described how wind farm capital costs have come down because of low priced generators from China and how wind power was approaching grid parity in many parts of the world including the Windy City (aka Chicago). Ward Lenz of North Carolina’s Dept. of Commerce described their efforts to promote offshore wind turbines in part as a jobs measure — wind energy creates many more permanent jobs than nuclear, for example. In a recession, the jobs angle helps policy makers stand up to utility interests.

Corwin Hardham of Makani Power gave a presentation describing his tethered “Airborne Wind Turbine” system. It’s basically a small remote controlled plane that can act as a tethered kite once airborne and carve out a large path at high altitude with a fraction of the materials and weight of a typical wind turbine. It’s a very clever idea for Megawatt scale power generation and their site has some lovely animations of the basic concepts.

One of the reasons a conference like this one is interesting is that you can have conversations with the wind folks and then the battery folks and then the smart grid folks to get a glimpse of what the end-to-end system might look like. As inventors and investors of course they are all optimistic about the opportunities. And they left even a skeptic like myself quite impressed with the possibilities.

Solar

The various panelists discussing solar energy were perhaps the most confident in the future cost effectiveness and global scope of their solution. And more than one pointed out the equally distributed nature of sunlight and the universal scalability of the solar solution from utility deployments down to Bangladeshi off-grid households.

Suvee Charma of Solaria Corporation described ongoing cost efficiencies in producing crystalline silicon panels. They have actually gained ground on supposedly cheaper thin film products in recent years and he suggested they are headed below $1/Watt in the near future. Modularity is one of solar PV’s greatest strengths because the manufacturing process is identical for both residential and industrial applications. Other speakers concurred with the < 1$/Watt figure and said that installation was now a greater expense than the panels themselves.

In the session on Residential Solar, Tom Faust of Redwood Renewables and Marc Irvin of Sungevity talked about the hurdles to adoption in the US including primarily financing and, especially among women, aesthetics. They see residential solar as a very young and vigorous market right now (100% growth in 2010) with the potential to grow into a multi-trillion dollar industry. Lanny Sinkin described how San Antonio has worked with local credit unions to provide financing for residential solar that brings the cost down to $35/month and how this has resulted in the installation of $2.5 million worth of residential solar in Bexar county with the resulting boost in jobs.

Indeed, the distributed nature of residential solar generation and the blue collar jobs it creates may be one of its biggest appeals.

Conclusion

I have tried to give a meaningful recap of what I found to be a very stimulating forum. In the interests of space I have not covered every forum, skipping important topics like green construction and utility scale solar thermal. What is presented above reflects my own personal interests more than the quality or content of the presentations.

I have included the names of speakers and their companies when I wrote them down not in order to promote them but rather as a resource for any further investigation or fact checking readers may wish to perform. This was, after all, an investment forum and one would expect to hear only the rosiest of scenarios.

Nevertheless, I came away impressed with the amount of human energy and potential sources of capital that are poised to address energy issues. The key themes I came away with were:

- Implementing solutions at the institutional level is very challenging.

- Societal perceptions are very important but we are currently experiencing a generational shift in those perceptions.

- Job creation needs to be an integrated part of any energy solution.

- Solar panel prices will continue to come down.

- Energy solutions may occur at a much more local level than we have previously imagined.

Perhaps “Power to the People” is more than just a metaphor.