On Friday, we looked quickly at some estimates in the International Monetary Fund’s World Economic Outlook for oil elasticities, as well as their projections for economic growth. In this post, let’s go through some of the implications of these numbers for oil supply and/or oil prices.

First, from the detailed statistics in the WEO database, here are the IMF’s projections for world growth over the next five years:

This is annual percentage growth in total global world product, corrected for inflation, and expressed at Purchasing Power Parity (PPP: ie, in which goods and services from non US countries are corrected to US prices assuming equivalent goods and services should be priced the same, rather than using market exchange rates).

To give some idea of the context, here is the history of world growth since 1980, together with the growth projections:

You can see that the IMF is basically forecasting five years of pretty good growth – near the top of the historical range, but certainly not above it. They are not projecting any serious global slowdowns, still less an outright global recession (those are rare – 2009 was the only case in the last thirty years).

To turn this into a forecast for global oil supply, we can use the elasticities from their table 3.1:

Here, the income elasticity for the whole world is 0.685. What that means, is that when global income increases by X%, other things being equal, we expect global oil supply to increase by 0.685X%. When we say “other things being equal”, we particularly mean oil prices being equal. Since they have global economic growth at about 4 1/2%, an income elasticity of 0.685 implies a growth in oil supply of about 3% annually. In a spreadsheet, we can compute with their exact growth projections, and this results in the red curve here:

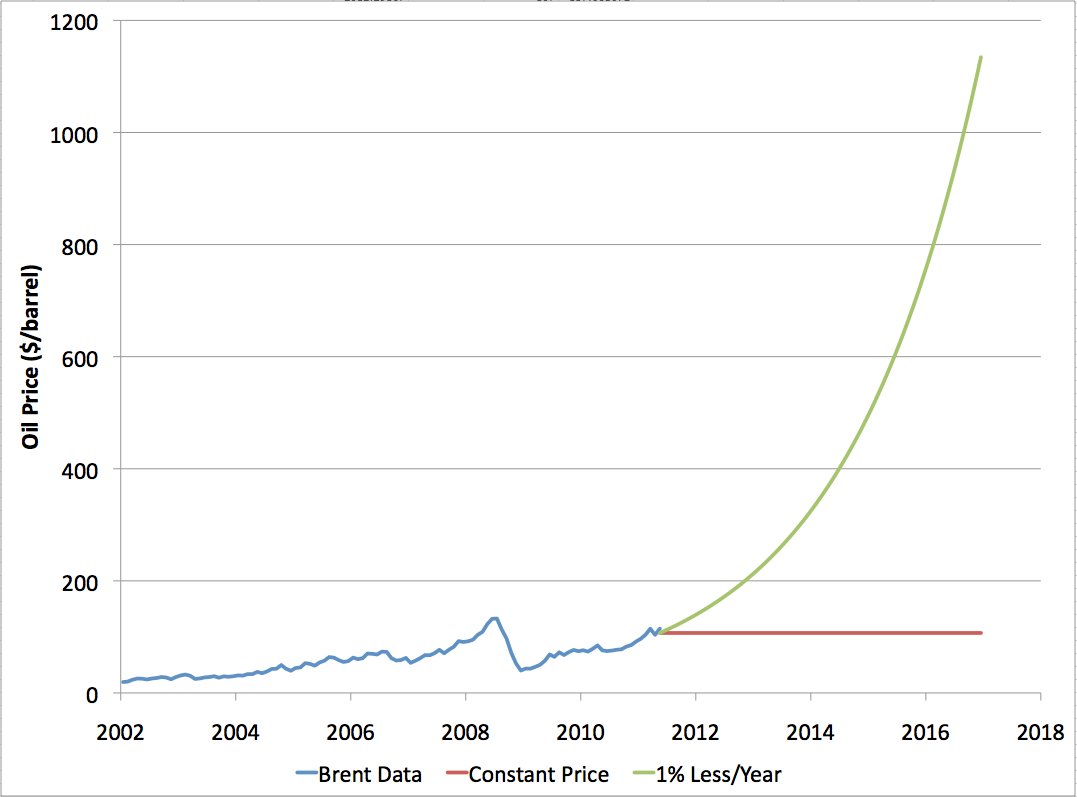

The blue curve there is actual data for global liquid fuel supply (the average from this post). Note that the graph is not zero-scaled to better show the changes. You can see that the red curve involves oil supply continuing to grow at a rate pretty similar to the rate since the depths of the recession, and much faster than the overall rate of the last six years (the “bumpy plateau”).

This requires the world come up with another 17mbd of supply in the next five years, though it only managed to come up with about 3-4mbd over the last five years, and that took a quadrupling of prices to achieve. I don’t see where this much oil can possibly come from. Saudi Arabia is saying they aren’t going to increase production much if at all in the next five years. Russia is pretty much plateaued. The US is long past peak, and will be lucky to avoid further declines. Iraq is the one hope for truly large increases in oil supply, but that increase has just barely started, and is not going to amount to more than a few mbd over the next five years.

The green curve looks at what happens if you say that oil prices will not be constant, but instead will increase by enough to make supply grow at 1% less per year than the red curve. That way we only need another 11mbd, instead of 17mbd. That’s still an implausibly large amount of oil. But even that causes huge problems if we take seriously the short term price elasticity of -0.019 in the IMF’s table 3.1 above. That means that to reduce supply by 1%, we need to increase price by 1/0.019 = 53%. Each year. As you might imagine, prices rise to ludicrous heights in no time:

And that’s just to hold global oil demand to only increase by 11mbd.

Clearly, nothing like these projections is going to happen. Instead, global oil demand is going to have to get a lot more elastic. To reconcile stagnant production with global demand, the world’s people are going to have to undergo a paradigm shift similar to that of the 1980s, in which the world makes major efforts to use oil much more efficiently. Because people have experienced a complete attitude shift, they will become much more responsive to moderate price shifts than they have been in the last twenty years.

The next question is whether this kind of global attitude shift could happen smoothly, without major disruption to global economic growth. I think that’s extremely implausible. Certainly, it didn’t in the 1970s when the big increases in efficiency were presaged by two major oil price shocks with ensuing recessions. And in general, my mental model is that people are creatures of habit who only change their way of thinking and operating when their existing approach starts to cause them serious pain.

So I think the IMF’s growth projections are seriously improbable. What is going to happen instead is that people will keep trying to grow without getting much more oil efficient, that won’t work, oil prices will go through the roof, another global recession, or at least a major slowdown, will ensue, and then people will begin in earnest the work of starting to transition away from oil dependence.

I can’t tell you the timing precisely. It could easily be this year, it could be next. It’s even possible that some other global crisis will intervene first (like the credit crash of 2008 did). But I will say categorically that there’s no way we are going to get through 2016, as the IMF projects, with business-as-usual economic growth.