p>I had intended starting my country-by-country detailed analysis this week, but with the publishing of the EIA compendium on world gas shale deposits, and a little controversy I got into in comments elsewhere, I thought it worthwhile spending a post looking at the global prospects for gas shale. I am indebted to Art Berman for first bringing some of the problems to my attention, though I have since looked into the issue sufficiently to draw my own opinions, which this article reflects.

The EIA document (actually prepared on their behalf by ARI) begins by noting the importance of this new resource to the US Energy picture:

The development of shale gas plays has become a “game changer” for the U.S. natural gas market. The proliferation of activity into new shale plays has increased shale gas production in the United States from 0.39 trillion cubic feet in 2000 to 4.87 trillion cubic feet (tcf) in 2010, or 23 percent of U.S. dry gas production. Shale gas reserves have increased to about 60.6 trillion cubic feet by year-end 2009, when they comprised about 21 percent of overall U.S. natural gas reserves, now at the highest level since 1971.

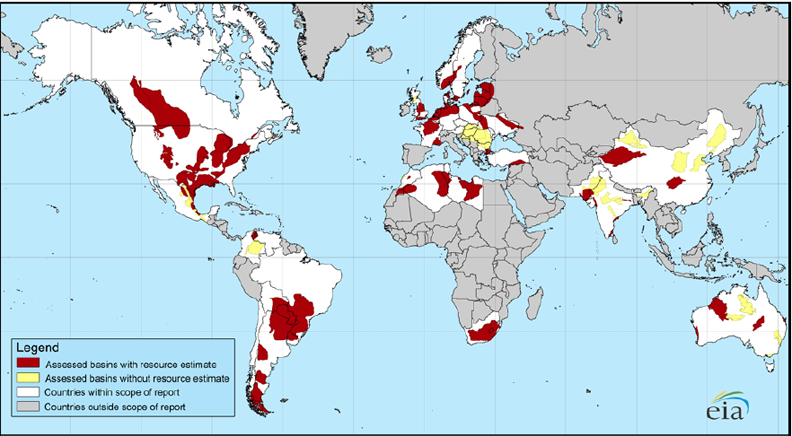

Development of US shale deposits began to be aggressive around 2005, and “technically recoverable” gas resources in the USA are now considered to be 862 Tcf. With this discovery of this potential future domestic supply, it became wise to see what the equivalent potential was elsewhere, and thus the report which looked at some 32 countries, 48 shale basins, and 70 formations. The assessed basins (in red with an estimate, in yellow without) are shown in the map below.

Gas Shale resources evaluated by the EIA

Combined, the total resource base is then assessed to be 6,622 Tcf. Now, it is important to draw a distinction at this point, because this is a resource. There is a considerable difference between a resource, which is something out there of value that may or may not be economical to develop, and a reserve, which is that fraction of the resource that is considered viable to develop. In the case of the USA for example, out of the 862 Tcf that makes up the resource, only 60 Tcf (6.9%) is considered to be viable as an addition to the US reserves.

Further (and a point I will get to later), gas from shale is somewhat more expensive to produce, relative to more conventional natural gas deposits. So, when the new volumes developed are put in context of the total natural gas resource available, while gas shales now provide a gain of 40% in the total volume of gas technically available, it may well be that the larger more conventionally available natural gas volumes may be less expensive to produce, and so will be developed preferentially in the next few years.

On the other hand, a domestically available reserve that does not require a nation to expend money on foreign fuels can have considerable benefit, even though it may be comparatively expensive. (And that is a judgment that brings in a lot of additional caveats, but it may very well drive development in countries without many other natural resources, and one thinks of countries such as Ukraine and Poland – where the alternate coal is becoming increasingly politically disfavored). In countries such as Russia and parts of the Middle East where there are already large reserves of comparatively inexpensive natural gas not considered in the study –it is possible that the total volumes available long-term may be understated.

To derive the “technically recoverable” volumes the consultants looked at the volumes of free and absorbed gas available, after having decided the size of the shale deposit, and then used their best judgment as to how much of this could likely be recovered. In general, they though it technically possible to recover between 20 and 30 percent, with some higher and some lower estimates within an additional 5%. They did not consider offshore deposits, nor critically did they consider production costs or accessibility.

‘Free gas’ is gas that is trapped in the pore spaces of the shale. Free gas can be the dominant source of natural gas for the deeper shales.

‘Adsorbed gas’ is gas that adheres to the surface of the shale, primarily the organic matter of the shale, due to the forces of the chemical bonds in both the substrate and the gas that cause them to attract. Adsorbed gas can be the dominant source of natural gas for the shallower and higher organically rich shales.

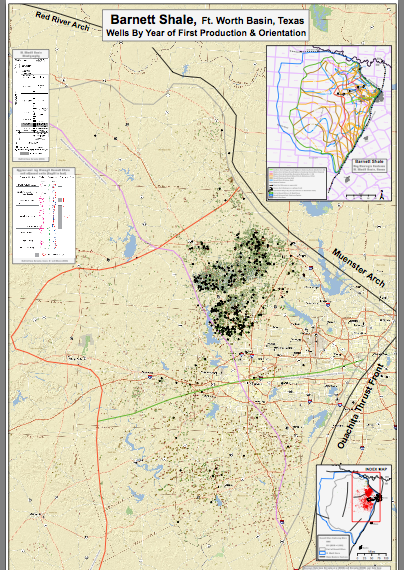

I am not going to go into the details of the report as it pertains to individual countries, though this is the bulk of the information provided within it. Rather, I am going to include those resource values and the related discussion as I come to discuss the resources available to different countries. But as an illustration that not all the shale is likely to be productive, once could consider, for example, the drilling pattern for the Barnett Shale where most activity is concentrated in the area north of Fort Worth. And there are significant areas with very little activity at all.

Drilling activity in the Barnett shale (EIA)

However, I will comment about the immediate significance of the resource, its size, and what I see as the short-term impact that these volumes will have on the global energy market. My sense is that they won’t make that much difference, once the initial hype and gasps over the size of the numbers has passed.

The reason for this is that this new resource is not cheap to develop. The initial cost comes in sinking the well in which once the initial vertical segment has been drilled, the driller must bend or deviate the drill until reaching the formation with the gas, and it is drilling sensibly horizontally. The driller must then hold the drill in the formation (which may be less than 50 feet thick) while the bit opens a hole that runs out perhaps two miles or more. The ability to sense where the bit is and to guide it along that path is a complex, expensive process, and you can’t take someone off the street and have them run a good well in a week. Over time, the number of qualified drillers who can do this has grown, so that in the week of April 8, Baker Hughes reports that of the 1782 rigs drilling in the USA some 50% were drilling for gas, and of the total 57% were drilling horizontal wells. It has taken some time for that level of expertise to develop.

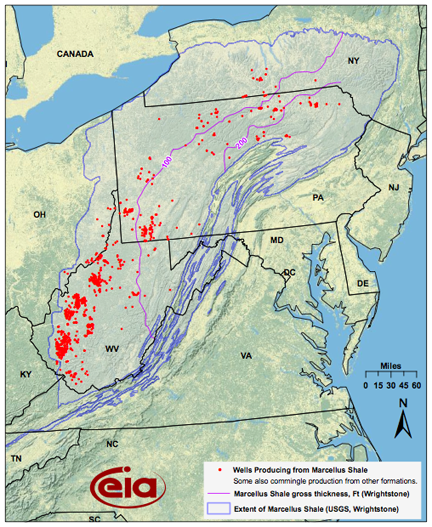

Yet even with the right rig and crew, success is not assured, or even permission to drill the wells. One has also to get the right permits, and the right prospect. And here one can look to the map of the current producing wells in the Marcellus Shale in the Eastern U.S. to illustrate the point.

Wells in the Marcellus Shale (EIA)

You can see that the activity has concentrated much more in West Virginia than, say, New York State. This is partially due to the different compositions and inclinations of the state legislature in each state.

But even with the rigs, the crews the political support, and a well located in a decent spot in the formation, success is not assured, or even the most likely outcome, because of the nature of the host rock. The major concern that I have had with the expectations regarding shale gas relates to the rock in which it is found. Most natural gas deposits are found in relatively permeable rock, so that it is relatively easy for the gas not intersected by the well or the fractures to travel through the rock to those free spaces, and thus out of the well. The permeability of shale is, to be blunt, pathetic. That is, after all, why the expensive fracturing of the well, and the slick-water injection of proppants into those fractures is so critical. But poor host rock permeability causes a fairly dramatic fall in production from gas shale wells after they are first brought on line. The easily accessible gas close to the fractures and the well makes its way out, and then the rest must struggle through increasingly thick layers of rock to reach the well. As a result there is a dramatic drop in production.

One of the wells that was cited in the comments debate I mentioned at the start of the post was the Day Kimball Hill #A1, which was the highest initial producer that Chesapeake ever drilled, at 12.97 mcf/day when it was brought on line. But:

The Day Kimball Hill #A1 is located in Southeast Tarrant County, Texas, and produced an average of 12.97 million cubic feet of natural gas per day in October 2009. Since shale gas wells decline sharply during the first few years, this Barnett Shale well has seen its production fall to 8.66 million cubic feet in November and 6.79 million in December.

That is a 47% decline in production in 3 months.

It was followed by White South #1H which came in at 17.8 mcf/day, last September. However, because of the low price of NG at the moment, the well has been partially shut-in to produce only 4 mcf/day since. Most shale gas wells don’t produce in this league. There are roughly 15,000 wells in the Barnett, and the wells in Arlington are an exception.

To join (the “monster” wells), a well’s output must average more than 8 million cubic feet of gas per day during its peak month.

Fewer than 1 in 1,000 Barnett wells has attained such a lofty yield for a month, which is enough gas to meet the heating and cooking needs for about 3,300 homes for a year, based on American Gas Association usage data.

While the Barnett Shale underlies more than 20 North Texas counties, the top “sweet spots” are in Tarrant and Johnson counties. All of the 35 biggest wells are in those counties, according to a new report by the Fort Worth-based Powell Barnett Shale Newsletter.

Day Kimball Hill site from Google Earth (Barnett Shale Drilling Activity)

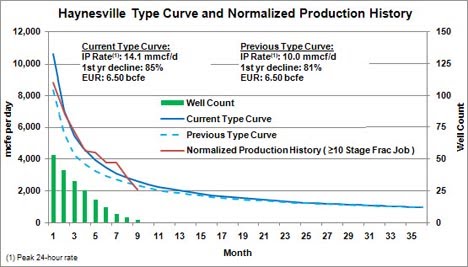

Obviously, if you were a partner in these wells, you made your investment. There is a discussion of well economics which suggests that $5 per kcf is the minimum price (in 2005 costs) at which the wells can profit. But that assumes a 60% decline rate for well production over the first year. But in all the others, even as with these, decline rates from the initial numbers can be dramatically higher. And this is not just true for the Barnett shale. For example, there is a report of a decline curve for the Haynesville shale that shows declines of up to 85% in the first year.

Haynesville shale decline curve (Haynesville Shale)

These high decline rates make it more difficult for the well to generate the return on investment that folk expect when they consider only the initial production volume.

The main problem that I see for the average shale gas well, in the short run, is that (as noted above) the producer really needs a price of better than $6 per kcf (and Art would argue higher) to make any money on the well. But there is a globally sufficient supply of natural gas more conventionally obtainable, and increasingly available as LNG at perhaps $4 a kcf delivered into the United States, so that it is difficult to see the short-term viability of the industry.

On the other hand, with alternative sources of fuel failing to live up to various promises made for them, it may now be that natural gas is seen as the next hope for broad use vehicular fuel. Legislation has been introduced to encourage this use, and if this becomes more widely adopted then it may be that the market may rise in this way, and that prices will hopefully rise with increased demand to make the shale gas more viable sooner than I think.

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.