Colin Barr at Fortune Magazine has some interesting discussion of the WTI-Brent spread (this is the difference in prices between the basic spot price of West Texas blend oil in Cushing Oklahoma, and the price of the Brent contract in Europe).

So how do you get $4 gas when oil is just $85? The answer starts with some unprecedented behavior in global oil markets, where the benchmark European oil standard, known as Brent crude, is trading at a $20-a-barrel premium to the U.S. benchmark, the West Texas Intermediate futures contract that trades on Nymex. The two typically trade within a few dollars of one another.

Increased flows from Canadian tar sands and the Bakken shale fields in the northern Great Plains have sent oil flooding into Cushing, Okla., where the WTI crude contract is priced. But because pipelines are set to run into Cushing, not out, much of that oil is going into storage rather than into refineries. Oil stockpiles in Cushing hit their highest level in seven years last month.

The glut has disconnected the widely quoted WTI market from a sobering energy market reality. “Cushing isn’t worth looking at,” says Steve Kopits of energy forecaster Douglas Westwood in New York.

and

Running off the WTI glut could ease the pressure on Brent and Louisiana Light prices. But the glut isn’t going anywhere any time soon.

Pipelines that take oil out of Cushing are at least two years away, and oil companies that stand to rake in fat refining profits aren’t exactly looking to rush that timeline.

Conoco (COP) chief Jim Mulva shot down talk about reversing a pipeline that feeds oil to Cushing from the Gulf Coast, saying, “We don’t really think that’s in our interest.”

Meanwhile, the steep contango in the WTI futures curve – the condition in which the near months are cheaper than future ones – creates incentives to add to the Cushing glut.

A refiner or trader with storage rights can buy the March future today, take delivery when it expires, sell the April contract — and lock in an easy $1.75 a barrel in practically risk-free profits, says Stephen Schork, who writes the Schork Report newsletter in Villanova, Pa.

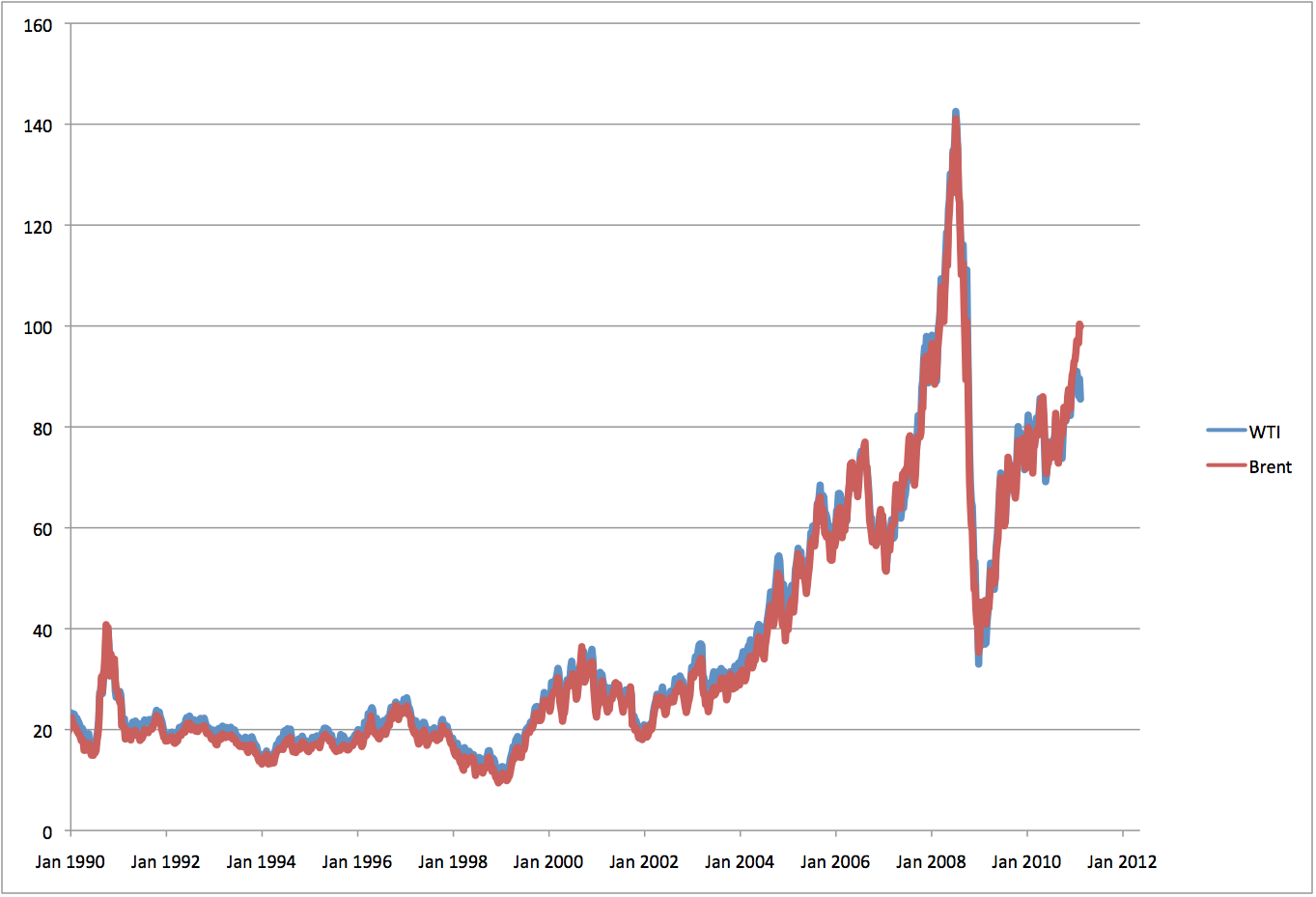

Let’s take a look at the data underlying this discussion. First, here’s the weekly spot prices for both WTI and Brent (from the EIA).

To make it easier to see what’s going on, let’s take the spread between the two, and plot that:

As you can see, the amount of spread is unprecedented. It’s also very recent – the spread was $2.20 as recently as the first week of January, this year. That makes me a bit wary of explanations based on long-term factors like the growth in Bakken oil, tar-sands production, or lack of pipelines out of Cushing – why would the market have been suddenly surprised in the last few weeks?

I don’t have a better theory though.