I was thinking about Paul Krugman’s Cross of Rubber column, and in particular the associated blog post Commodities: This Time is Different. My take on Krugman is that he’s an extremely brilliant guy who’s been thinking about economics for a good long time. His enormous knowledge and insight are invaluable, and I pay close attention to his writing. However, I also think he’s gotten into some pretty deeply scripted habits of thinking based on past events and isn’t paying close enough attention to the ways in which the present and the future are likely to be different than the past. In particular, his frame of reference for the events of the last few years has been past deflationary episodes such as the Great Depression in the 1930s and Japan in the 1990s.

However, he’s smart and pragmatic enough that he at least pays attention to facts that don’t altogether fit his narrative, and in particular in recent weeks, he’s been paying increasing attention to the fact that commodity prices are rising rapidly, even though the US and European recoveries have barely gotten going. To me, ever since I started thinking about economic issues five or six years ago, these “finite world” issues have seemed to be a central fact of the current era that we need to come to grips with, but to Krugman, it’s a bit of a distraction from his main theme: our biggest problem is lack of aggregate demand in the advanced economies, and we need more government fiscal stimulus and more liberal monetary policy to solve that problem.

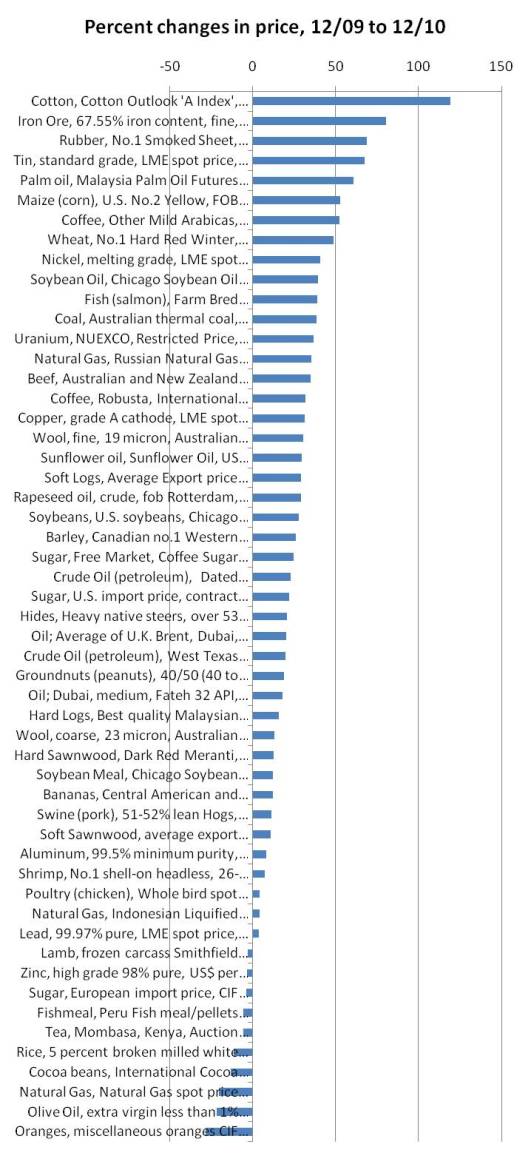

So in the blog post he linked above, he starts by looking at the last 12 months change in prices of a range in commodities, and orders them according to that:

Obviously, many commodities are going up in price, and this reflects in part the fact that China, and to a slightly lesser extent, other developing economies are trying to raise their standard of living to western levels, and the global economy is struggling to come up with the raw materials to make that happen.

Now, obviously, some of these commodities are not in any long-term supply shortage. Iron, for example, is #2 on the above list, and yet iron represents about 5-6% of the earth’s crust. It’s going to be a very long time before humanity runs short of iron in some absolute sense. Any price rises have to be due to basically temporary factors that can be ameliorated by opening some more mines (at some environmental cost in digging up some more of our beautiful planet). Obviously, by focussing on a 12 month time frame, Krugman also opens the possibility of just meaningless noise getting into the list.

Still, looking at the systematic list caused me to think more deeply about my own focus on oil as the central commodity to worry about (with food second). Why is oil more important than rubber, or iron, or cotton?

The answer comes from thinking: what happens as commodity prices get higher? What is the economic effect? For the most part, consumers aren’t directly exposed to commodity prices. No-one goes to the mine and buys iron ore (well, except this guy), or buys raw latex from rubber plantations. Instead, we buy cars and toasters with these things in, and we are only going to modify our behavior with respect to buying and selling if the price of cars and toasters changes, not the price of iron and rubber. And of course, inflation in the price of finished goods like cars and toasters is extremely subdued in the western world. The reason is that commodities are (currently) a small part of the cost structure of most manufacturers, and since there is overcapacity in the economy, manufacturers cannot pass increases in their input costs onto consumers. So these commodity price increases aren’t going to have a visible effect on measures like core inflation for a while. And as long as they don’t, they can basically be ignored in thinking about macro-economic issues (which is exactly what Krugman would prefer to do – ignore them).

However, oil is the exception! We may not buy raw rubber or sheet steel very often, but we do buy gasoline and diesel, and those products have very limited value-add over straight crude oil. Refining margins are a small fraction of the final cost of those products, and crude oil and gasoline prices move in very close tandem. And we really, really, want the oil that we want. We aren’t indifferent and willing to happily substitute something else – instead we pay and pay and insist on driving anyway. In economist language, oil demand is very inelastic in the short term (the elasticity in recent years has been about -0.05, though I wouldn’t be surprised to see it get a bit more elastic in the next decade, now that we can’t put it on the credit card quite so easily).

So oil is the one commodity price that cannot be ignored in the developed world. If the world economy does indeed continue to recover rapidly, oil supply is not going to keep pace, oil prices will go up sharply, and that is something that will have macroeconomic consequences that Krugman will not be able to ignore. I wouldn’t be at all surprised to see the shock come this summer, but it could be delayed another year or two. But come it will.

Food commodities are slightly different in their impact. In the western world, we largely eat processed foods which behave economically more like cars and toasters – they only respond slowly and moderately to commodity prices. Where food commodity prices really hit is in the urban third world. The average resident of a big developing world city is poor, so they have to eat more basic foods with a high input of commodities, and, unlike their rural brethren, cannot grow much food of their own. So, when food prices go up, we get riots in big poor cities. This is something rulers have had to understand since the Roman Empire (which subsidized wheat for the poor in Rome). The wave of hasty food buying and subsidy increases across the Middle East in recent weeks is a symptom of rulers quickly relearning this fact in response to events in Algeria, Tunisia, and Egypt.

But still, that does not mean that we in the privileged west can ignore these increases either. In an interconnected global world, revolutions in far away countries can cause strategic realignments or economic problems that will affect us all.

So, it’s not rubber, cotton, and iron we need to worry about. It’s oil and food.