Ed. note: Please click on the charts to see larger version.

There seems to be a lot of conflict among folks attempting to make plans for the future. I think the basic cause is different views regarding where we are headed, and how fast changes may take place.

The most popular view among the general public, including research scientists, is that growth will continue practically indefinitely. Let’s call this Scenario A. This forecast by Price Waterhouse Coopers might be typical of what one would expect:

These growth rates don’t look all that high when presented on an annual basis, but they really add up over time. At an annual growth rate of 7.6%, India’s GDP in 2050 can be expected to be 27 times its real GDP in 2005. At an annual growth rate of 0.8% per year, by 2050, India’s population can be expected to 43% higher than in 2005.

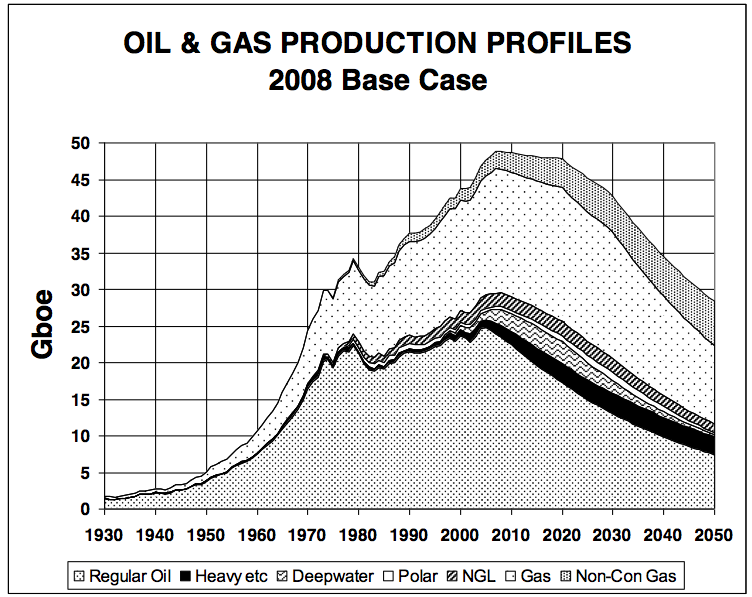

A second scenario, which I call Scenario B, is one that is held by quite a number of people who have been studying oil and gas depletion models. It is focused on an expectation that oil and gas production in the future will follow a pattern such as this one prepared by Colin Campbell, taken from the April 2009 ASPO-Ireland Newsletter.

Note that in this scenario oil production starts dropping off about now by about 2% a year. Natural gas production doesn’t drop off as quickly. Substitutes, such as ethanol and coal aren’t shown on the chart, but many think they will help cushion the decline. With this view, the big concern is adapting to having a little less oil and gas each year.

A third scenario, which I call Scenario C is a very rapid drop off in fossil fuels of all types, such as might happen if a financial crash, or a major disruption of international trade, suddenly affected world economies. This is a graph I made for an Oil Drum post in 2009:

Under this scenario, the big concern is that the exponential growth we see in many things–real GDP, bank deposits, world population–will suddenly (or perhaps over a period of, say, 20 years) come to an end, and may in fact lead to collapse. As Kenneth Boulding was quoted in saying in yesterday’s post, “Anyone who believes that exponential growth can go on forever in a finite world is either a madman or an economist.”

We are depending on fossil fuels to maintain and increase our food supply. It is doubtful that with a much smaller fossil food supply, the world will be able to continue to support a population of 6.9 billion people.

The Connection between Oil Supply and World GDP

One other thing that it is helpful to understand is the apparent connection between oil use and GDP.

This graphic indicates that for the historical period shown, a rise in the world oil consumption of a given percentage seems to be associated with an increase in World GDP that is about 2.5 times as large. No doubt, increases in the supply of other fossil fuels play a role in this GDP growth as well.

We are not really certain precisely how the relationship between GDP and oil consumption will work on the way down. At least part of the growth in GDP is from oil substituting for manual labor. If we start moving the other direction–toward more manual labor–will that bring GDP down more quickly, since manual labor does not produce a very large quantity of goods and services, in comparison to oil? Efficiency gains and substitution of natural gas and coal may work to keep GDP from dropping as quickly, but these require investment–for example, building electric cars to replace gas-powered ones.

Looking at the three scenarios

Scenario A – Economic and Population Growth continues almost indefinitely

This is the scenario that underlies the pronouncements in the press. Even most mainstream scientists seem to believe this view of the future.

With this view, oil, natural gas, and coal use continue to rise, practically indefinitely, and forecasts of CO2 levels are very high. Climate change is a major concern, as is getting countries to voluntarily cut back on their fossil fuel use. The expectation is that economic growth will continue forever (although perhaps at a bit lower rate) even if major cutbacks in fossil fuel use are made.

One detail that is sometimes raised by those in the peak oil community is that it is not entirely clear where all the fossil fuels assumed in the climate change models will come from, since climate models seem to assume more fossil fuels (oil, natural gas, and coal) than are available.

Figure 5 is from this Oil Drum post by Luis de Sousa. This difference will not be an issue to many people, because of concern for being near a climate change “tipping point,” but it does give rise to differing viewpoints on how urgent it is to cut back.

The other detail that “peak oilers” raise is that oil production seems likely to decline on its own. While there is still a need to limit coal use, and perhaps natural gas use, a large share of the oil problem perhaps will naturally take care of itself. If there is a way to ease the transition away from oil, for example through tax structure, that perhaps makes sense, but the reason for the move away from oil may be as much because the oil won’t be there, as it is for climate change reasons.

Scenario B – Oil and natural gas production estimates based on depletion analyses govern the likely future

With this view of the future, future oil price and technology changes are viewed as likely to have relatively small impacts. Oil and natural gas production are expected to progress in accordance with models which take into account the tendency of oil supply from oil fields to decline. Typically, the models assume that much of this natural decline is offset by infill drilling, development of new (usually smaller) fields, and very slow development of unconventional oil.

With this view of the future, the issue is to try to hold up GDP (or some other measure of prosperity) by substituting materials for material that are expected to be in short supply, such as oil–for example, building electric cars, to replace gasoline powered vehicles. The type of decline in GDP that perhaps might be expected is perhaps something like this:

Some with this view have focused on adding wind and solar to the electric grid, to increase electric capacity for electric vehicles and for general “growth” in the use of electricity. Some who are not concerned about climate change issues may also suggest an increased role for coal in electricity generation, or even coal-to-liquids, as a substitute for oil.

Most of the transition-type plans one sees for the future seem to follow the belief that the future will follow Scenario B. The plan is often to substitute approaches which use a little less oil for current approaches, which use more oil. Or the plan may try to substitute electricity for oil, or reduce electricity use.

Gardens or small farms will often have diesel operated equipment, and may be irrigated, perhaps using a solar pump. Electric fences may be used. Improved public transportation, such as long distance trains, may be part of the plan. Because the expectation is that the economic situation is not deteriorating too quickly, climate change is often a major consideration, because of its connection with coal usage.

Scenario C – Crash scenario, because the “system” does not hold together in some way.

The assumption in Scenario B, above, is that depletion will govern the amount of future oil and gas extracted. This implies that oil and gas companies will continue to do infill drilling, and will continue to drill in new fields they are developing. It also assumes that systems will work together pretty much as they do today–our electric system will keep operating; our governments will keep operating, and the markets (based on supply and demand) will continue to operate.

But it can be argued that the depletion models really set an upper bound for oil and gas production (assuming no new major innovations in extraction technology, and assuming prices remain high enough to encourage drilling at the level assumed in the depletion models). The question is whether our systems can in fact work together as well as we hope. If not, there could be a major disruption–perhaps not as soon as suggested by Figure 3 above, but it could be quite soon–certainly within the next 20 years.

One of the big concerns is whether the financial system will be able to continue to function as it does today, since it needs growth to maintain its current method of operation. Without growth, huge debt defaults seem likely, and growth is tied in with oil supply. Of course, even if the financial system does fail, there is the possibility that new system could be devised. Also, as long as the means of production remain, it is possible that other systems may be able to continue operating, even if, say, the banks fail.

The problem is that we have many vulnerabilities, and we may not even understand all of them. Our “just in time” delivery system is one. Another is our international trade system. Almost every high-tech product requires raw materials from around the world, so disruption in this system could be a major issue. If electrical companies go bankrupt, or are unable to pay their employees because of financial disruptions, this could lead to widespread electrical outages.

For a person who is concerned about these types of issues, the way to plan for the future becomes more problematic. One of the issues is just keeping the current system together as long as possible. Making major changes–and this could be as simple as adding a lot of wind and solar to our current electrical grid–could be the type of change that brings the system down.

Faced with possible immediate problems, climate change may move down the priority list for some. If a Scenario C type of situation should occur, it would likely pull down natural gas and coal production, in addition to oil production. Food and water supplies could easily be affected. One might expect population to decline–if not immediately, over a period of years.

It seems to me that one of the types of mitigations we would want to consider in planning for Scenario C is restoring technology of the type we had prior to the industrial revolution. At that time, there were wind turbines made with local materials that were used to power some factories. We also made use of canal boats for transportation of goods. Ropes and knots were also used to a significantly greater extent than they are used today.

Steps would also need to be taken to develop food production capabilities without using fossil fuels, and also for pumping or otherwise gathering water. Food storage would be another major area of concern.

If Scenario C is really an issue, one almost feels powerless. What politician would ever consider such an extreme scenario? But even if a Scenario B evolves toward a Scenario C because things start falling apart after many years, one would still need plans for local food and water production that do not depend on fossil fuels.

I should add that I do not see any way that wind and solar PV are, on their own, self-sustaining. To me, they can only be produced with fossil fuels. They will stop working not long after fossil fuel support ceases to be available. For example, suppose you have a solar PV panel. If it is part of a grid connected system, it will stop functioning when the grid stops. If it is separate, it will be useful only as long as the appliance to which it is connected still works. If we lose the ability to make new computers and light bulbs, the solar panel will have much less use.

Blending Scenarios

Most people would say that we really don’t know for certain which scenario is ahead. As a result, we perhaps need to look at both Scenarios B and C, weighted as we think appropriate, in terms of what types of planning we will do.

There are no doubt some variations I left out. If one sees financial markets as being able to mitigate Scenario B, perhaps this might lead to higher oil and gas prices, and more fossil fuel production. In this case, the result may be something between Scenario A and Scenario B. The reason I tend to discount this possibility is because high fossil fuel prices tend to cause recession, and bring oil and gas prices back down again. At this point we don’t have good substitutes (on any reasonable scale) for oil, gas, and coal, either. The substitute that comes closest is ethanol, and it is in competition with resources needed for food.

It is important that we think through which scenario(s) are most likely, and how this affects where we choose to place our priorities. While it would be nice to be able to do every type of mitigation, some may not be helpful, and may even be counter-productive. We also don’t have resources to do everything, so we need to make choices.