For those addicted to more roads, airports and the sweet smell of gasoline, the IEA’s 2010 World Energy Outlook includes some pretty sober reading. As they did in last year’s Outlook, the IEA forecasts that OECD demand for oil has already peaked. Consumption of oil in the United States, Europe, Japan, Australia and other ‘developed’ OECD nations is set to decline permanently, starting about.. now.

A few short years ago the IEA saw nothing but comfortably increasing oil supplies up to and beyond 2030 for everybody. But they have come a long way since then. The IEA now directly addresses peak oil in WEO 2010, including this one remarkable quote:

If governments put in place the energy and climate policies to which they have committed themselves, then our analysis suggests that crude oil production has probably already peaked.

While that quote and their scenarios include a number of caveats and subtleties as far as the IEA is concerned, their forecast for oil demand in OECD countries is even more direct and confronting.

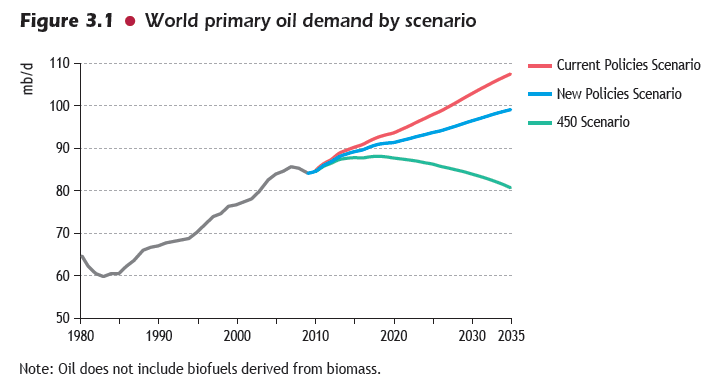

Starting with their forecast of primary oil demand, things might appear rosy for the merchants of economic growth, as long as no serious attempts are made to limit CO2 levels:

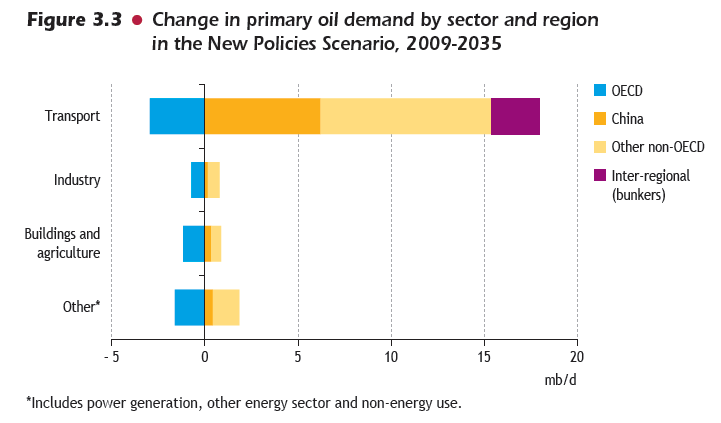

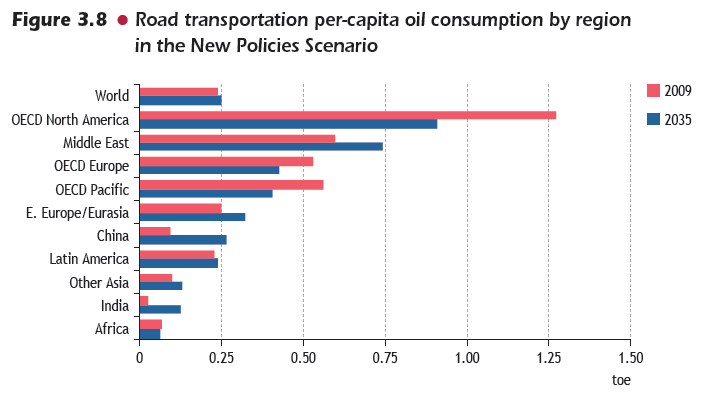

But the IEA does not try to obscure the facts about how that oil is shared around:

In the New Policies Scenario, demand continues to grow steadily, reaching about 99 mb/d (excluding biofuels) by 2035 — 15 mb/d higher than in 2009. All of the growth comes from non-OECD countries, 57% from China alone, mainly driven by rising use of transport fuels; demand in the OECD falls by over 6 mb/d.

In the 2009 report and public statements since then, the IEA has been crystal clear that the transition to declining consumption of oil in OECD countries starts now:

“When we look at the OECD countries — the U.S., Europe and Japan — I think the level of demand that we have seen in 2006 and 2007, we will never see again,” Fatih Birol told Reuters in a telephone interview.

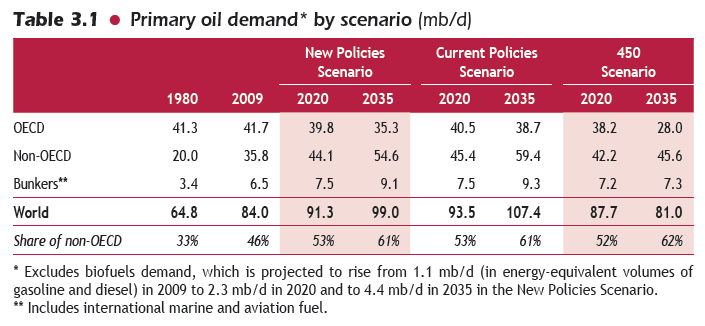

But of course, the IEA has placed greater emphasis on scenarios in their outlooks, so perhaps this is just one outcome and readers could choose themselves a happier adventure in other scenarios. Unfortunately not. While the ‘Current Policies’ only scenario is more moderate, OECD oil consumption is set to decline in all three scenarios modelled. This is quite remarkable given that all scenarios are optimistic with respect to reserves, resources and recovery of conventional oil and only differ signifcantly in terms of climate change policies or lack of them.

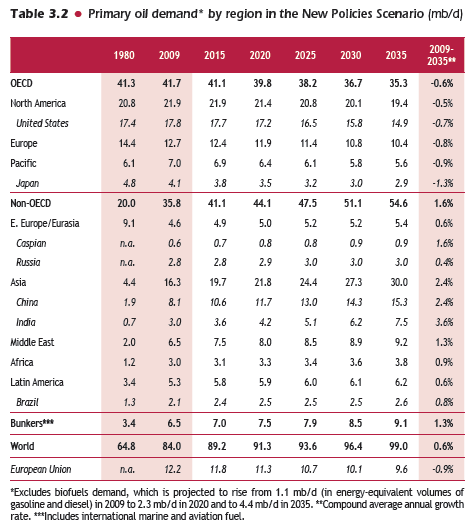

What this means for your particular part of the world may be made clearer by the table below. For the United States, oil demand is not quite flat from 2009 but falls more substantially after 2015. For Europe and Japan the declines start a little earlier, which the IEA partly attributes to choices they have made of their own free will.

To make this a little more personal for those (like me) in the west, the IEA helpfully shows what this means for you as in individual. ie. You, the reader, will be using less oil next year, and the year after that (even in the IEA’s economically calm and happy view of the world):

All of this is completely contradictory to the road building, car-loving enterprises of the western world. While the IEA has moved ahead in leaps and bounds over the last few years, most of the individual member nations of the IEA (Australia being a particularly bad example) are still running with internal forecasts and assumptions that support more roads, airports and other oil intensive infrastructure.

The IEA is still too optimistic about OPEC reserves and future reserves growth and discovery rates. But peak oil campaigners in OECD countries could do worse than take the IEA 2010 World Energy Outlook at face value and ask their own Government why their policies and actions are so disconnected from the forecasts in this report.

Living with less oil tomorrow is no longer an idea of those on the fringe – the International Energy Agency now says that is the reality for most of the developed world. Pass it on.