In this post I present an analysis of how OPEC oil supplies have responded to changes in crude oil prices during the last 10 years. My objective was to estimate OPEC’s probable marketable crude oil capacities as of May 2010, based on responses of OPEC oil supplies to price changes.

This approach suggests that as of May 2010, OPEC’s marketable spare crude oil capacity was approximately 2 Mb/d and that a majority of this spare capacity is most likely in Kuwait, Saudi Arabia and UAE.

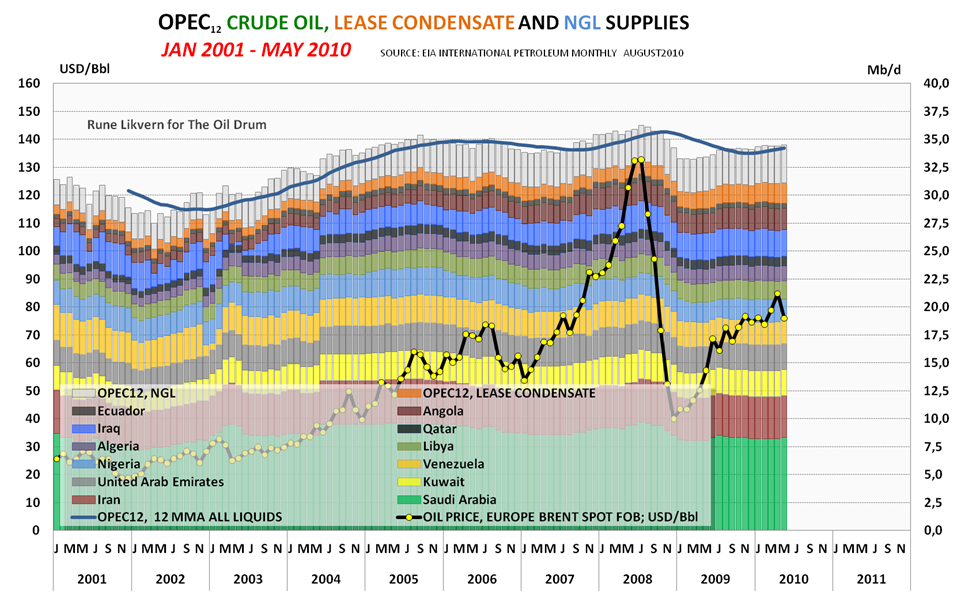

The stacked columns show each OPEC member’s crude oil supplies and OPEC’s supplies of lease condensates and NGLs between January 2001 and May 2010. The average monthly oil price is also plotted using amounts on the left hand y-axis.

I also briefly present a recent history of OECD and Non OECD oil supplies/consumption. Based on this analysis, it is probable that demand for OPEC supplies could grow by approximately 2 Mb/d between 2010 and the end of 2011. Putting the estimated current OPEC spare capacity of 2 Mb/d together with the expected increase in demand for OPEC oil supplies of 2 Mb/d suggests that during 2011, OPEC’s spare capacity may be completely eroded–a very serious situation.

DISCLAIMER: The author holds no positions in the oil/energy market that may be affected by the content of this post.

Two energy subjects that often fuel lengthy debates are

- The oil price and its future trajectory

- OPEC’s present marketable spare capacity for crude oil

IEA Oil Market Report for August 2010 estimates OPEC’s crude oil spare capacities at around 6,0 Mb/d, while the EIA Short Term Energy Outlook for August, 2010 provides a corresponding estimate of 5,1 Mb/d for 2010.

Oil prices and OPEC spare capacities are closely linked, and therefore monitored closely by companies planning to invest in new supplies that presently are at the margin–for example, some oil sands developments. Most analysts seem to agree that OPEC presently has spare marketable crude oil capacity, and that this spare capacity could be used to maintain an oil price in the present “comfort zone” of $70-80/bbl. The amount of the this spare capacity would thus define how long investments in new supplies at the margin are deferred.

In this post, I use the same definition of OPEC spare capacity as the IEA. This is capacity that can be reached within 30 days and sustained for 90 days.

Further, it is important to acknowledge that OPEC spare capacities are not static numbers. These amounts are subject to change over time as result of new developments and declines.

NOTE: Scaling among the various diagrams shown in this post varies.

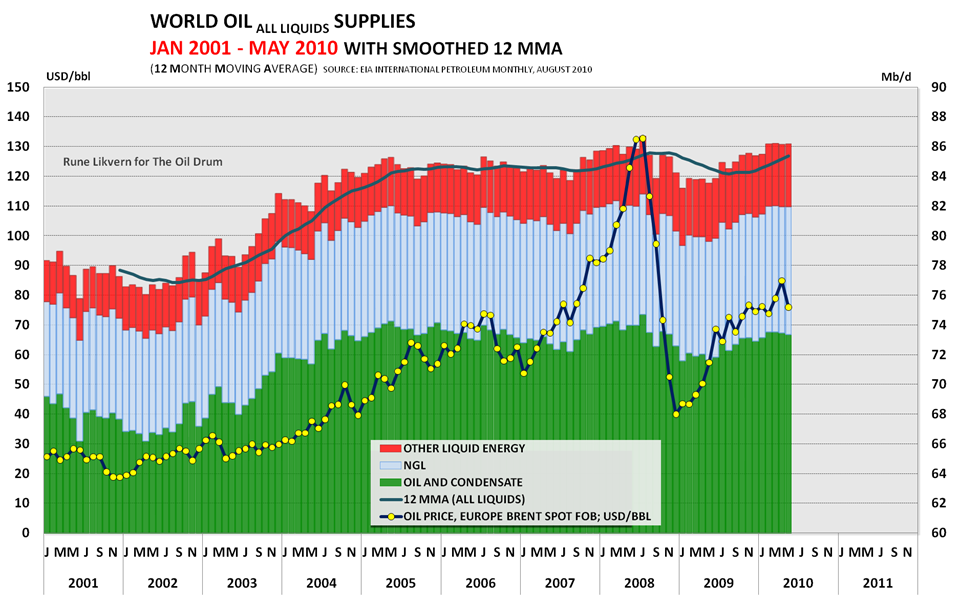

Figure 01: The stacked columns in the diagram above show development in global supply of crude oil and condensates, NGLs and other liquid energy between January 2001 and May 2010. The development in the average monthly oil price is plotted using the scale on the left hand y-axis. NOTE: Diagrams based upon EIA data may be subject to future revisions.

The reason why I start with the above diagram is also to illustrate that if the demand for more oil were present, then new highs of global supplies for both crude oil and all liquids would have occurred. For anyone who has looked at the data, it is apparent that OPEC has spare capacity. What seems to be debatable is how much.

OPEC supplies

Figure 02: The stacked columns show each OPEC member’s crude oil supplies and OPEC’s supplies of lease condensates and NGLs between January 2001 and May 2010. The average monthly oil price is also plotted using values on the left hand y-axis.

What the above diagram illustrates is that OPEC crude oil supplies for all practical purposes remained on a moderately bumpy plateau between July 2004 and late 2008. During this period, crude oil prices grew from around $40/Bbl to more than $140/Bbl. The steep rise in prices are now thought to be the combined result of physically tight supplies and speculators detecting these tight supplies. With the collapse of crude oil prices, OPEC met during the fall of 2008 and agreed to cut supplies to support the oil price. What is interesting is that total OPEC crude oil supply increased by approximately 0,72 Mb/d (using IEA’s criteria of a production that may be sustained for 90 days) during the oil price spike in the summer of 2008 compared to the summer of 2005. It required a doubling of the price to bring this increase in supply into existence.

This suggests that OPEC had little spare crude oil capacity during the summer months of 2008. Despite this increase in supply, data shows that OPEC net exports were lower in 2008 than in 2005, ref Figure 09 below.

Below I present a closer look at groups of OPEC members that will hopefully make it easier to see how crude oil supplies from these groups have responded to crude oil prices in recent years.

Figure 03: The stacked columns shows developments in crude oil supplies from Angola, Ecuador and Iraq.

The reason I chose to show Angola, Ecuador and Iraq separately is that Angola is a new member of OPEC, Ecuador reentered as a member, and Iraq is presently not subject to OPEC’s quota arrangements. Angola was raising its oil production before becoming an OPEC member, as was Iraq after the war.

Total supplies from these 3 countries have recently reached the same level as during the summer of 2008, and recently this has been driven by growth in Angolan supplies. Supplies for Ecuador have been in a slight decline.

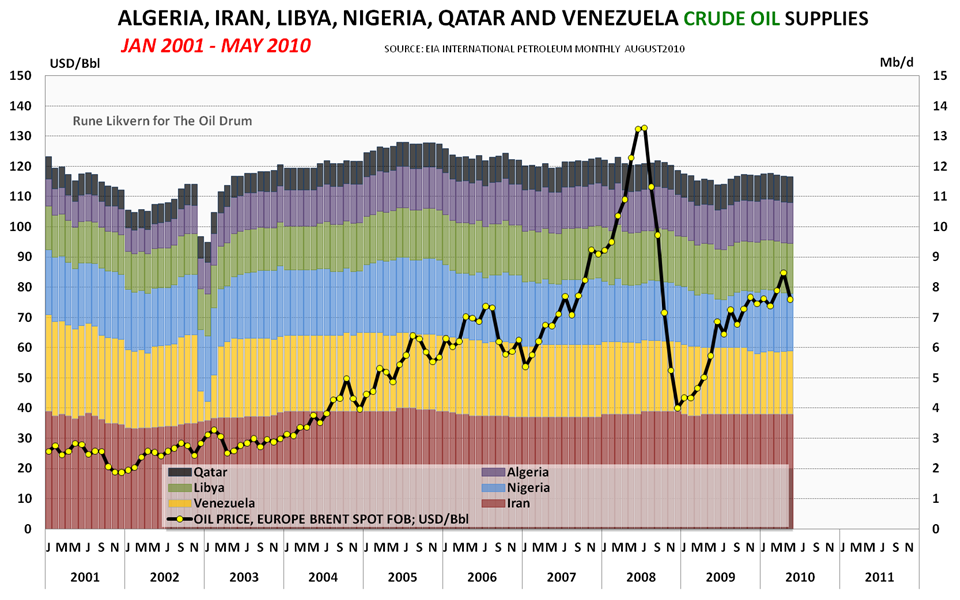

Figure 04: The stacked columns shows development in crude oil supplies from Algeria, Iran, Libya, Nigeria, Qatar and Venezuela. The average monthly oil price is plotted against the left hand y-axis.

The diagram illustrates that the crude oil supplies for these 6 OPEC members reached what appears to be a plateau during the oil price growth in late 2004 and 2005. Note that the increase in oil prices towards their high in 2008 did not increase supplies from these 6 OPEC members.

Apparently these 6 countries contributed in holding back supplies early in 2009, but the recent growth in oil prices seems to have resulted in some supply growth until they reached what appears as a new and lower plateau.

Could this suggest that total supplies from the 6 OPEC members included above are in decline?

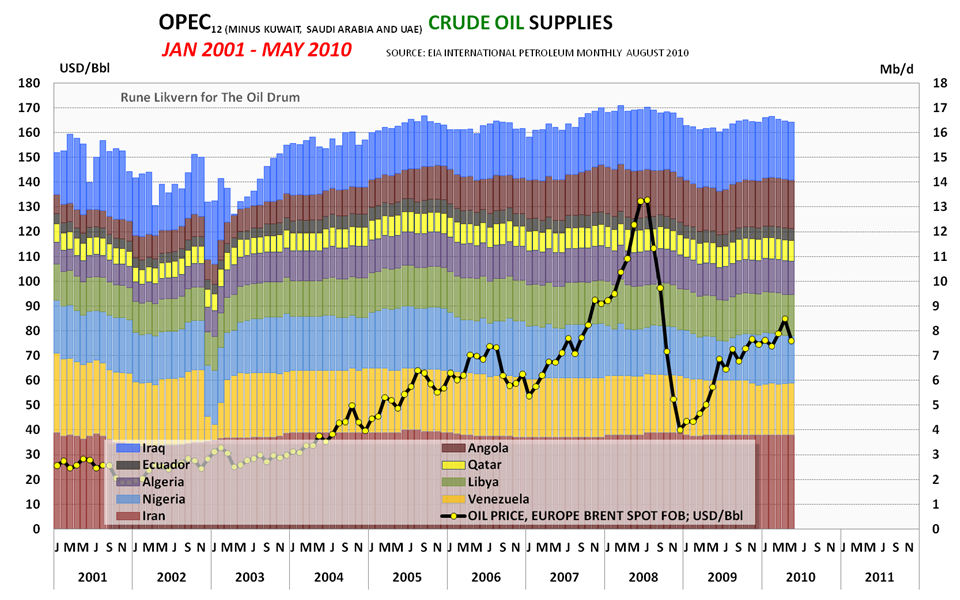

Figure 05: The stacked columns shows developments in crude oil supplies from the 9 OPEC members presented in Figures 03 and 04. The average monthly oil price is plotted against the left hand y-axis.

If the 9 OPEC members shown above were pumping flat out to benefit from the high prices during the summer of 2008, then recent responses of oil supply to the recent price growth suggests these countries now have little, if any, spare crude oil capacity.

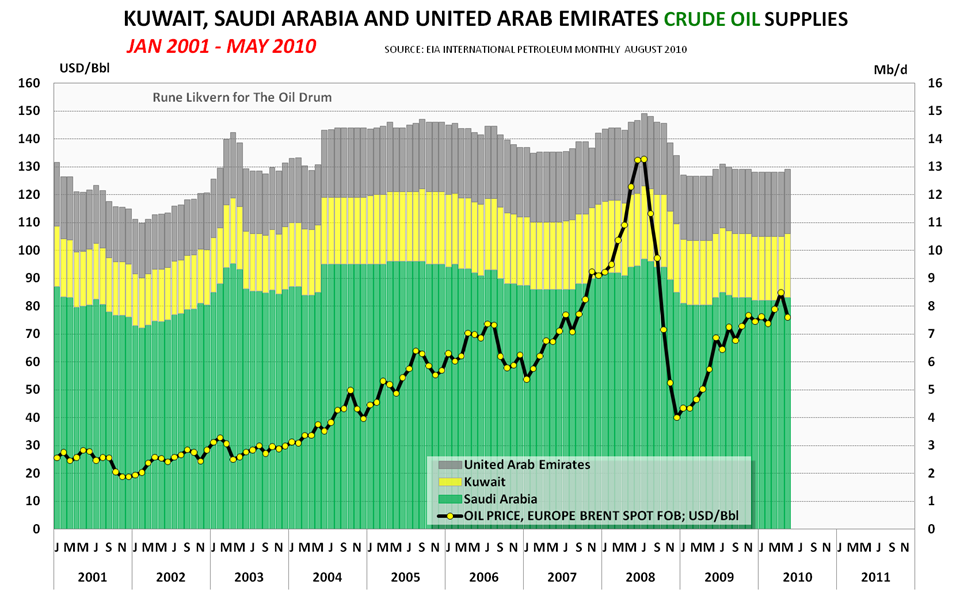

Figure 06: The diagram above shows crude oil supplies (based upon data from EIA International Petroleum Monthly as of August 2010) between January 2001 and May 2010 (data may be subject to future revisions) for Kuwait, Saudi Arabia and United Arab Emirates.

Total crude oil supplies for these three oil exporters showed some response to the price growth of 2008 and these three were able to increase their total supplies by 0,20 Mb/d relative to 2005 (if only monthly data is used….0,05 Mb/d if IEA’s definition of sustainable capacity is used) as a response to a doubling of the oil price.

Using IEA’s definition for a sustainable capacity these three had a total crude oil capacity of 14,65 Mb/d during the summer of 2008. These numbers then need to be adjusted for additions and declines since then. As of May 2010, these three exporters supplied 12,9 Mb/d, which is 1,75 Mb/d below their sustainable supplies from the summer of 2008.

The net exports from these three declined from 2005 to 2008 due to growing domestic consumption, ref figures 08 and 09.

Actual data suggests that most of present global spare crude oil capacities is to be found amongst the three producers presented above. And if the most recent data is to be believed, it looks like as of May 2010 they have started to eat into their spare capacity.

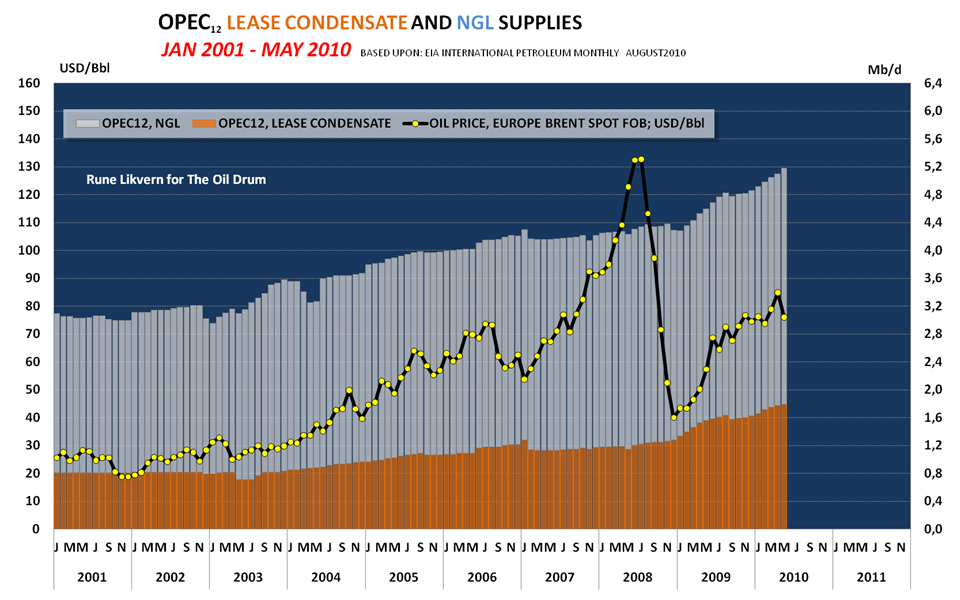

Figure 07: The diagram above shows total lease condensate and NGL supplies from the 12 OPEC members between January 2001 and May 2010.

The strong growth in lease condensates is now believed to also be related to the increased natural gas production from North Dome/South Pars. The growth in OPEC NGL supplies has been more moderate.

Lease condensates and NGLs are presently not part of OPEC quota arrangements.

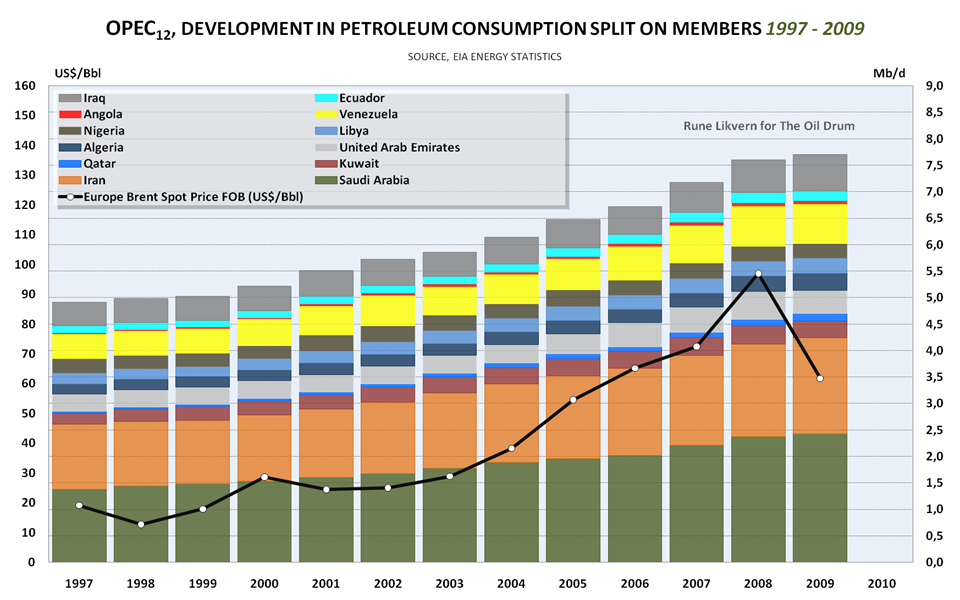

Figure 08: The stacked columns shows how domestic petroleum consumption has developed for each OPEC member between 1997 and 2009.

Data from EIA shows that between 2005 and 2008, petroleum consumption within OPEC increased by more than 1 Mb/d, from 6,5 Mb/d to more than 7,5 Mb/d.

High income from petroleum exports and a growing population have given rise to growth in OPEC petroleum consumption. If the trend in recent years provides any guidance, it should be expected that this trend will continue and thus take up more of OPEC’s capacities.

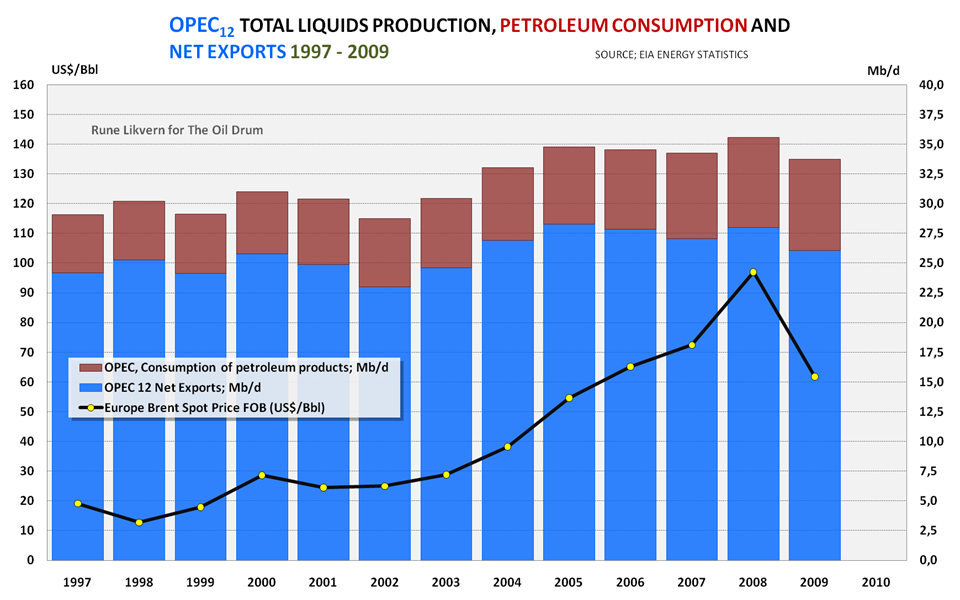

Figure 09: The stacked columns above show developments in OPEC net exports of petroleum, OPEC’s consumption of petroleum and thus also OPEC’s total liquids supply.

Development in net petroleum exports is what really matters for petroleum importing countries. The diagram illustrates that as prices started to grow (suggesting a growing demand) OPEC’s net exports grew between 2002 and 2005. As oil prices continued to grow OPEC’s net exports declined. This suggests price rationing was taking place. As oil prices reached their apex in 2008, net exports from OPEC grew a little relative to the previous years, but did not surpass the high from 2005.

Non OPEC supplies

Inasmuch as the development in total global liquids energy supplies was presented in Figure 01 and a more detailed presentation of OPEC was presented above, I will just briefly present development of Non OPEC supplies of crude oil, condensates and NGL’s.

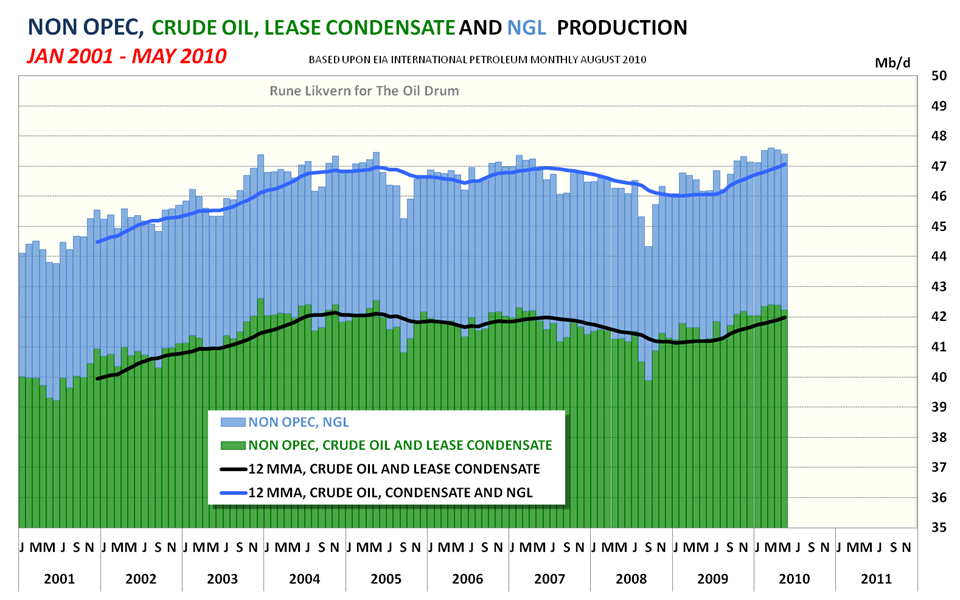

Figure 10: The stacked columns above show development in Non OPEC supplies of crude oil, condensates and NGLs between January 2001 and May 2010. Note scaling of y-axis.

Non OPEC supplies apparently were able to grow to meet demand until supply reached a plateau in 2004. After that, growth in OPEC supply and prices balanced the supply/demand equation. The decline in OPEC net exports, from 2005 to 2007, coincides with the continued growth in oil prices and flat supplies from Non OPEC.

The growing prices seem also to have stimulated more investments amongst Non OPEC producers (even though there is a time lag from the price signal to invest arrives and the oil developed by the investment flows) to bring on new capacity and slow decline rates. The hurricanes hitting Gulf of Mexico had some effect on Non OPEC supply, but recently supplies have grown mostly from Russia and the US.

The most recent data shows a slight decline in Non OPEC oil supplies, and the question is: will this continue?

OECD

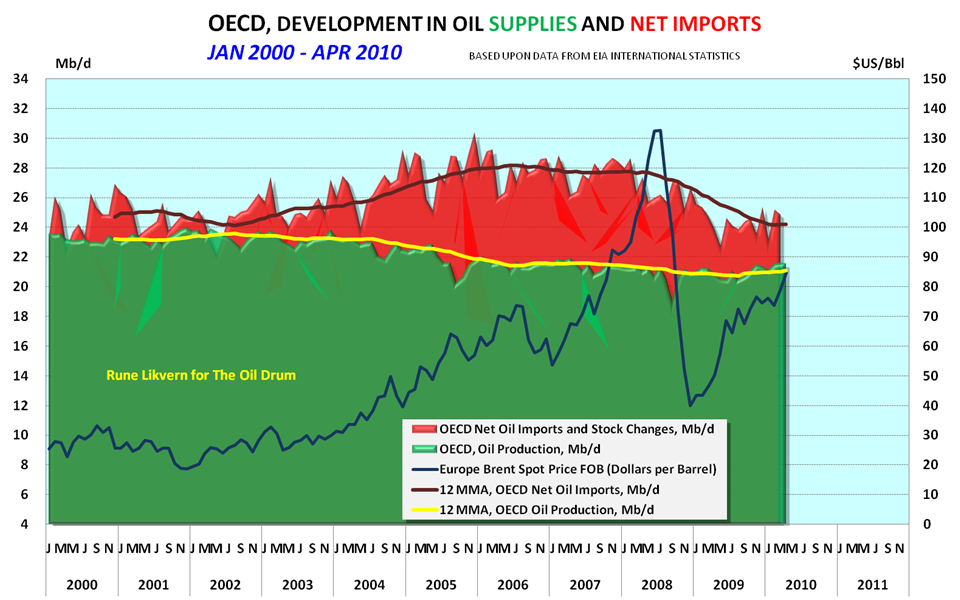

Figure 11: The diagram shows developments in OECD oil supplies and net imports of oil between January 2000 and March 2010.

The economic slowdown within OECD also affected oil consumption. The diagram illustrates that OECD net oil imports declined by approximately 4 Mb/d from their high around 2006.

EIA in their Oil Market Report for August 2010 has forecast a decline in OECD liquid energy supplies of 0,3 Mb/d and a growth in Non OECD supplies of 0,5 Mb/d between 2010 to 2011. A growth in OECD consumption over the next year of 0,5 Mb/d (which is not a lot considering it has declined more than 4 Mb/d in recent years) would thus eat into OPEC spare capacity. Add in uncertainties in the forecasts (which could work both ways) and the possibility exists that OECD demand for growth in supplies from OPEC could become higher than the 0,3 Mb/d as suggested here.

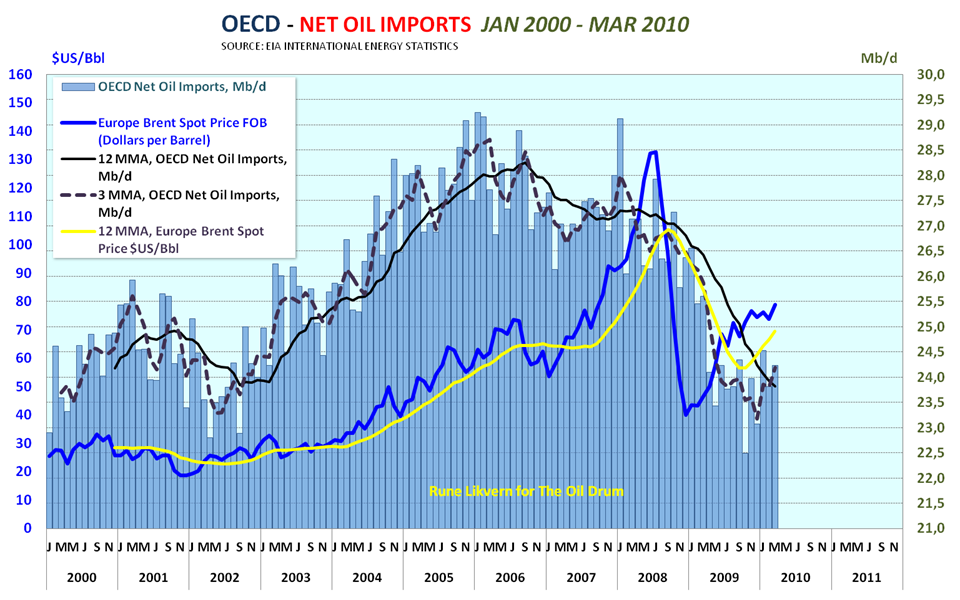

Figure 12: The diagram above shows development in OECD net oil imports between January 2000 and March 2010. Note scaling of right hand y-axis.

The diagram shows that recently net oil imports into OECD have been growing, and that this has coincided with the growth in oil prices. My current expectation is that for the near term OECD will continue to grow its net oil imports to offset declines within OECD and to feed a growing demand.

Non OECD

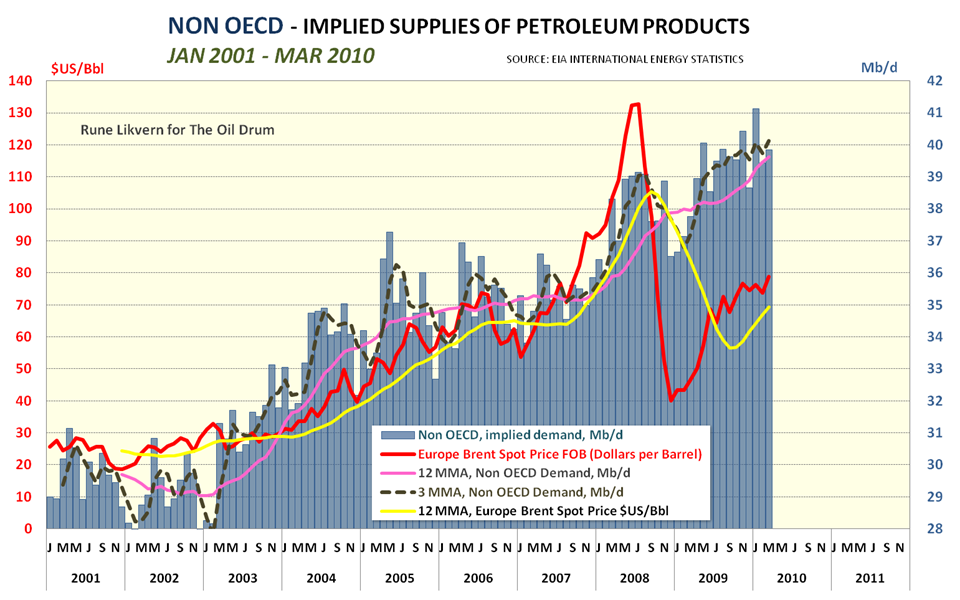

Figure 13: The above diagram shows implied demand for liquid energy from Non OECD countries between January 2001 and March 2010. (I describe it as implied demand as the diagram shows the difference between total global supplies of liquid energy and OECD supplies (production + net imports)).

The diagram shows that Non OECD demand (on an annual basis) grew by an astonishing 3 Mb/d during a period of a little more than a year, while oil prices almost doubled. This also suggests that demand very much contributed to the growth in oil prices during 2008. This growth was followed by what appears to have been a consolidation phase, and recently started a new and fierce growth cycle. Oil prices apparently were lifted by this continued demand growth for liquid energy from Non OECD countries.

Given this recent growth history, it should not come as a surprise if Non OECD demand for liquid energy grows by another 1 Mb/d over the next year.

The bulk of such a demand growth would most likely be met with increased OPEC supplies.

If we start from the assumption that present global spare crude oil capacity is around 2 Mb/d, then recent data on consumption and supply developments within OECD and non OECD suggests that present global spare crude oil capacities may become eroded by the end of 2011.

EIA STEO for August 2010 forecast a growth in global liquids energy consumption of approximately 1,5 Mb/d for both 2010 and 2011.

In the recent past, I expected oil prices to retreat to around $60/Bbl, and even envisioned they could drop further than that. My expectation of such a decline was anchored in an analysis that suggested that the US economy (that is a GDP related analysis) can now absorb oil prices of around $60/Bbl and still post some growth.

Inasmuch as oil prices have remained around $70 – 80/Bbl, this has suggested a stronger demand than what I expected (ref the diagram showing demand growth from Non OECD), but it may also reflect a combination of factors inclusive of more strained supplies than what is now widely assumed.

$70 – 80/bbl oil suggests a redistribution of spending within several economies; that is more money is used for oil/energy and less for spending on other things. If this is so, then this will show up in statistics from retailers, restaurants, car sales and other service industries. Reduced availability of credit and higher unemployment (amongst other factors) most likely also play a major part in declining discretionary spending.

The fact that prices have remained as high as $70 to $80 a barrel with only a modest rise in global oil demand/consumption suggests that as supplies become even tighter in the future, prices will rise even higher yet. This analysis suggests that we may continue to see strong oil prices as long as all the wheels stay on the major economies.

SOURCES:

[1] EIA, INTERNATIONAL PETROLEUM MONTHLY, AUGUST 2010

[2] EIA, INTERNATIONAL ENERGY STATISTICS

[3] EIA, SHORT TERM ENERGY OUTLOOK, AUGUST 2010

[4] IEA, OIL MARKET REPORT, AUGUST 2010

[5] OPEC, MONTHLY OIL MARKET REPORT, AUGUST 2010