I’ve been musing on the interaction between a) an extended period of economic stagnation/contraction due to deleveraging, and b) peak oil.

Let’s start with the above graph, which shows the global history of oil production as year-over-year percentage changes (taken from this 2006 Oil Drum post of mine), along with an orange box that highlights the years of the Great Depression. The Great Depression is the most recent analogy we have to a global deleveraging event. You can see that, overall, growth in oil production was lower during the depression than it was before (or after) but that it did grow except during the first few years of particularly sharp contraction. For comparison, here’s the level of US GDP during the years 1920-1940 (from here):

You can see that the main setback to US GDP coincides with the main setback of global oil production. Overall, the growth rate during major eras of global oil production was as follows:

| 1860-1891 | 13.9% |

| 1891-1929 | 7.9% |

| 1929-1942 | 3.9% |

| 1942-1973 | 7.4% |

| 1973-1979 | 2.1% |

| 1979-1983 | -4.0% |

| 1983-2004 | 1.5% |

Again, the depression years had the lowest growth until the 1970s oil-shock era.

So one approach would to be assume that the current deleveraging episode will have similar effects to the great depression (a few years of mild contraction of global oil production, followed by renewed but slower growth). There are a number of problems with that analogy, however:

- The policy response has been different this time around, with rapid injection of government fiscal stimulus in the early stages of the deleveraging (although it seems that political support for that might have run out of steam, at least for now)

- The global economy is very different than it was in 1930. In particular, the leading countries of 1930 were what we would now call developing economies in earlier stages of their adoption curve for oil powered machinery and oil products.

The first point may matter less than some people currently think. It appears we now have a political swing towards government fiscal austerity. I expect that will produce another round of global economic contraction. That will scare political elites back to more stimulus after a year or three (and indeed automatic stabilizers alone will tend to do that). However, a number of economies are probably running out of room for much more government indebtedness, and others will over time, and so the sovereign defaults will begin. Overall, I’m not sure how much more expansionary policy is really going to be, on a full-cycle basis, than it was during the 1930s, though the time course will certainly be different.

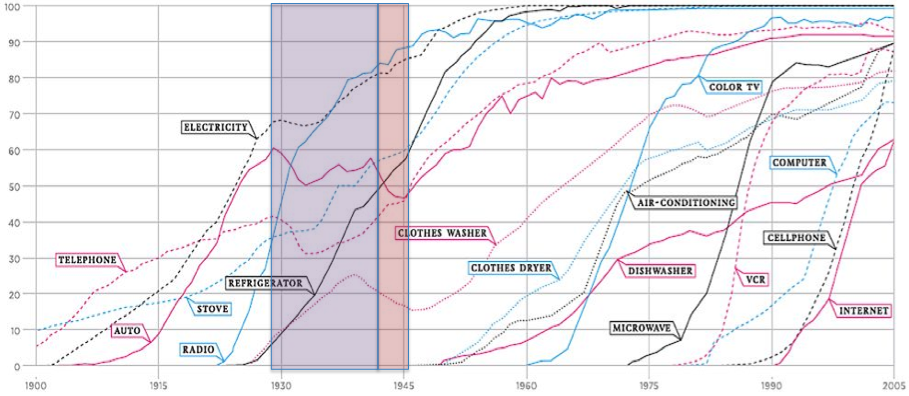

The second point, however, is pretty significant. In particular, let’s remind ourselves of the automobile adoption curve in the US, as a rough proxy for oil usage generally (see this post):

At the outset of the Great Depression, the auto had penetrated 60% of US households. This is probably higher than auto penetration on the global scale today (there are about 1 billion cars, but most of them are in multi-car households in the developed world). So we can probably think of oil usage today as made up of two components: the developed countries with substantially complete adoption of oil (which is going to have to get slowly unrolled in response to supply restrictions), and the developing countries, particularly the BRIC countries, which are in a much earlier stage of adoption and will probably continue to rapidly increase their oil usage as long as the price of oil is not completely prohibitive and the global economy is not completely in the tank.

So, recognizing there is a high degree of uncertainty here, overall I would expect global oil production to continue to grow over the next decade, supply permitting, but more slowly and interrupted by periods of contraction as the global economy falls into recession repeatedly due to the ongoing deleveraging process.

Under the circumstances, the general course of oil prices seems almost completely unknowable. One can imagine periods of relatively healthy recovery (a la 1934-1936) coinciding with supply restrictions and causing prices to shoot through the roof. One can also imagine the al-Shahristani plan bringing on a flood of new oil unluckily timed with a contractionary episode and depressing prices quite a bit below recent levels.