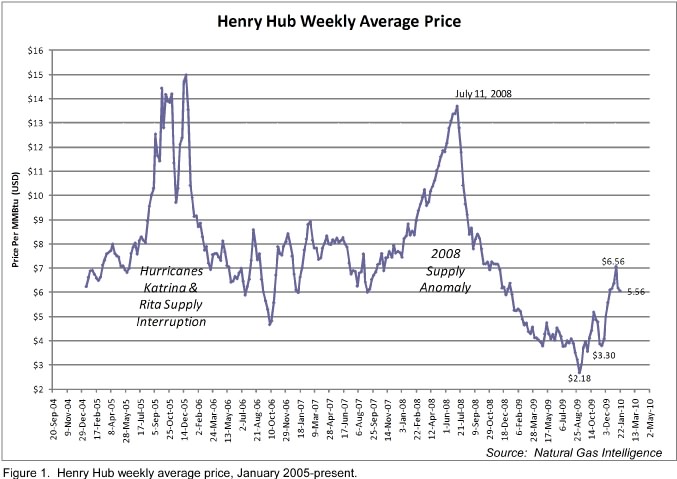

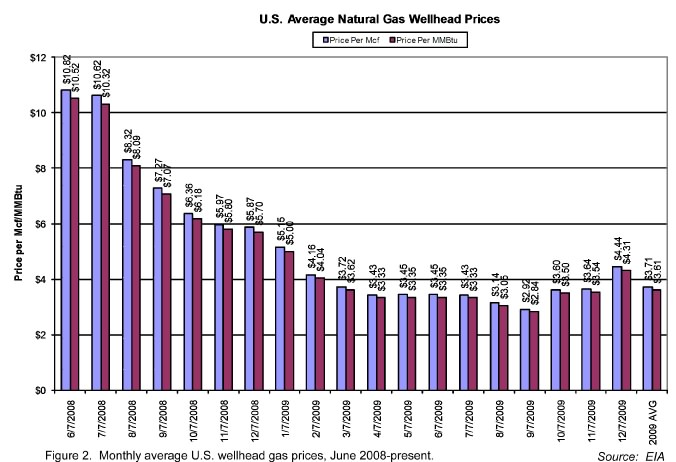

Natural gas prices continue their recovery. Cold weather has caused high levels of space heating that have resulted in reduced gas storage inventories. Henry Hub spot prices have recovered from their September $2.18 low to an average price of $5.56/MMbtu in the week ending January 22, 2010 (Figure 1). The average daily spot price for 2009 was $3.95/MMbtu. Average wellhead gas prices increased in December 2009 to $4.31/MMbtu from a September low of $2.84 (Figure 2). The average wellhead price for 2009 was $3.61/MMBtu.

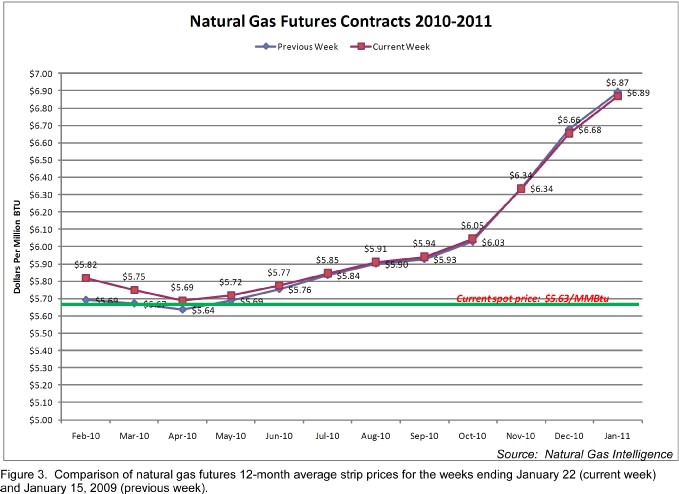

Natural gas futures contracts suggest that gas prices will remain in the $5.50-6.00/MMBtu range through Q3 2010, and then increase toward $7.00 in Q4 2010 (Figure 3). The contract for February 2010 delivery closed this week at $5.82/MMBtu.

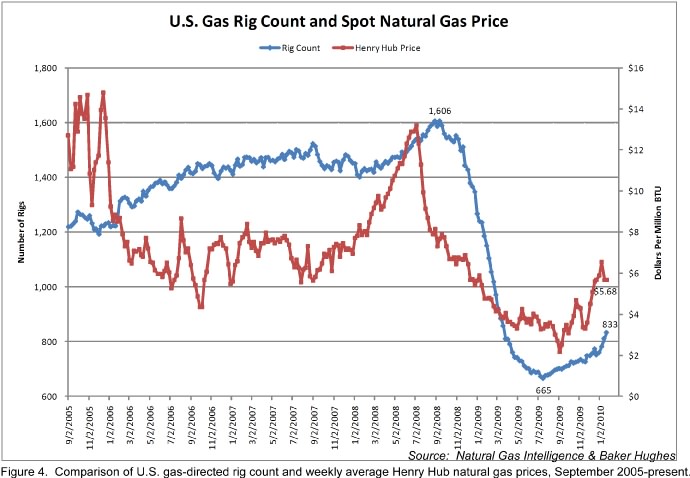

The gas-directed U.S. rig count increased by 22 during the week ending January 22, and is 168 more than the low of 665 rigs in mid-July 2009 (Figure 4). Most of the increase is due to shale gas drilling in the Louisiana Haynesville and Texas Eagle Ford Shale plays. Current levels of gas-directed drilling to not seem warranted by either gas prices or storage inventories, and are likely to contribute to relatively low natural gas prices through 2010, which will probably average $6.30/MMBtu (Bodell, personal communication).

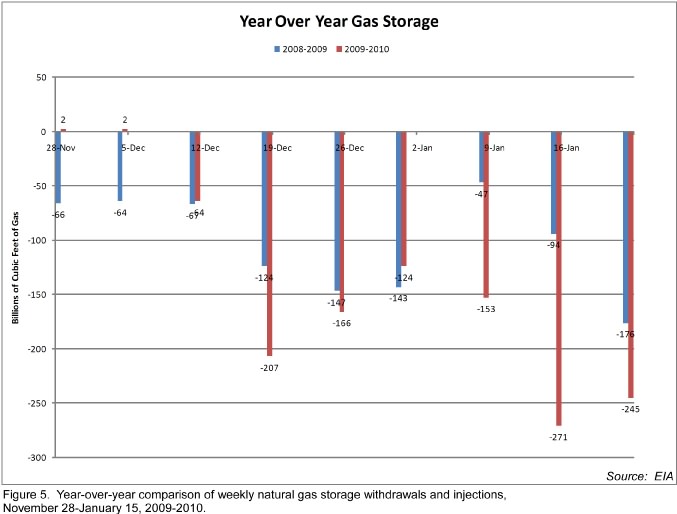

Gas storage for the week ending January 15 was 2,607 Bcf following a withdrawal of 245 Bcf compared to a 176 withdrawal during this week a year ago. Withdrawals have been generally higher for 2010 than for 2009 during the past two months (Figure 5).

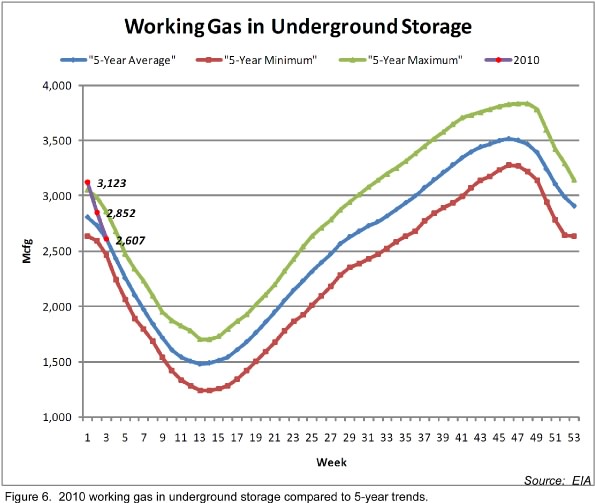

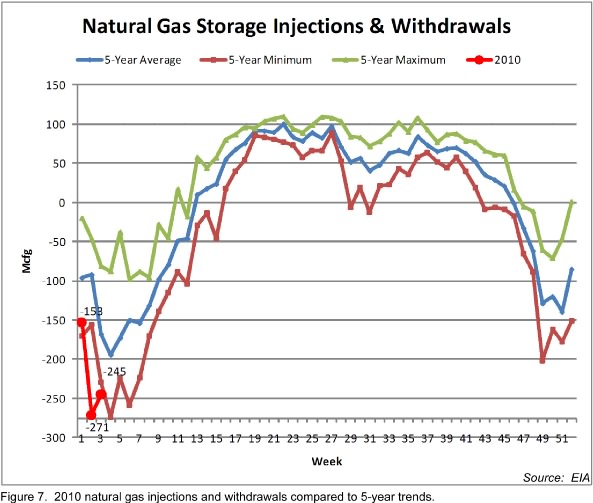

Gas storage inventories are 22 Bcf higher than a year ago, and 6 Bcf less than the 5-year average for this week (Figure 6). The 245 Bcf withdrawal was 69 Bcf more than that of a year ago, and 80 Bcf more than the 5-year average (Figure 7).

It is likely that depletion of gas storage inventories will continue through the winter, and supply will probably be at parity with recent years by the end of the first half of 2010 or sooner. This would ordinarily result in a price increase, and still may, but continued drilling of high initial-rate shale gas wells, and depressed industrial demand because of the recession will probably keep gas prices near their current level through the winter heating season. Additionally, gas prices are now high enough to cause switching from gas to coal for some electrical power generation plants, which will further lessen demand.

At the same time, the long period of declining gas-directed drilling from September 2008 to July 2009 should result in decreased supply, which may cause gas prices to increase. This dynamic balance continues to puzzle analysts, and results in average 2010 price forecasts that range from $5.25 to $9.00/MMBtu.

The wild card, of course, is the economy. Apparent improvements in the U.S. and other leading world economies are probably related in part to massive government spending and support programs that are now slowing or ending. Investors and consumers are worried and skeptical. This week, China indicated that it will decrease lending and increase interest rates. President Obama’s intention to limit investment banks’ ability to use federally insured funds for speculation dampened U.S. and other markets. Finally, concern about the solvency of Greece, Spain and Dubai threatens economic recovery. One analyst stated that now that the college BCS (bowl championship series) is over, we have the economic BCS to live with: banks, China and sovereign funds.

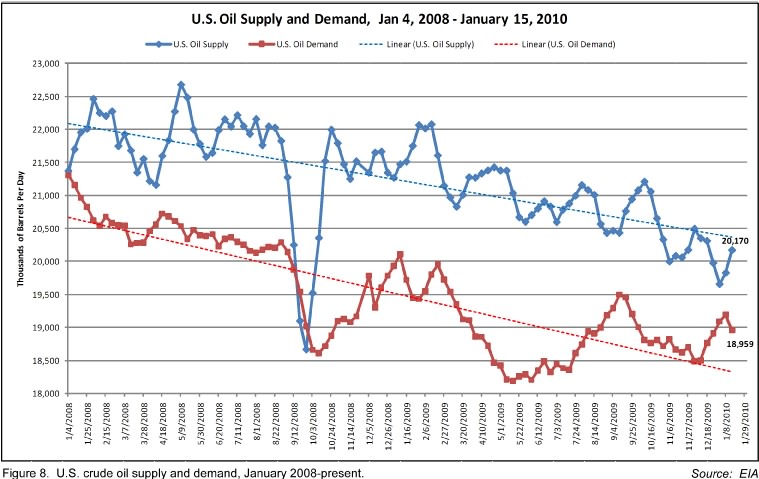

U.S. crude oil demand has been a useful gauge of economic direction for some time, and current trends suggest that the improvements of the past 5 or 6 weeks have reversed at least for now (Figure 8). Crude oil demand is currently 2.3 MMbopd less that levels in January 2008, and is almost 1 MMbopd below levels in January 2009. This suggests that, while the economy is improving, it has a long way to go before re-establishing pre-recession levels. Recoveries are like that.