Monday, November 2, Arthur Berman wrote in his blog:

Pressure from Petrohawk helps cancel World Oil column

In an act of extraordinary courage, a top Petrohawk executive threatened to cancel his free subscription to World Oil if the magazine continued to publish my column. Today, John Royall, President and CEO for Gulf Publishing, cancelled my November column.

I have accordingly resigned as contributing editor.

Heading Out (Dave Summers) and I have been talking about the issues Arthur Berman raises for quite a while now. Most recently, Dave wrote a post called Shale Gas Estimates Perhaps Optimistic – An Interesting and Worrying Talk at ASPO.

So what are the issues involved?

What Arthur Berman is saying is that natural gas companies that extract shale are mis-estimating how quickly natural gas production will decline in the future–they are assuming gas production will decline more slowly than evidence indicates it will. As a result of their optimistic assumptions about decline rates, they are assuming that shale gas can profitably be extracted for as long as 50 years, when Berman believes the average well life is only about 8 years.

Part of the controversy revolves about what price is needed for shale gas to be profitable. The gas companies are saying that natural gas is already profitable, or near profitable, at today’s low prices. As Heading Out notes, Chesapeake testified before congress that the company could operate with a price of $4 per thousand cubic feet. Arthur Berman is saying that prices need to be much higher.

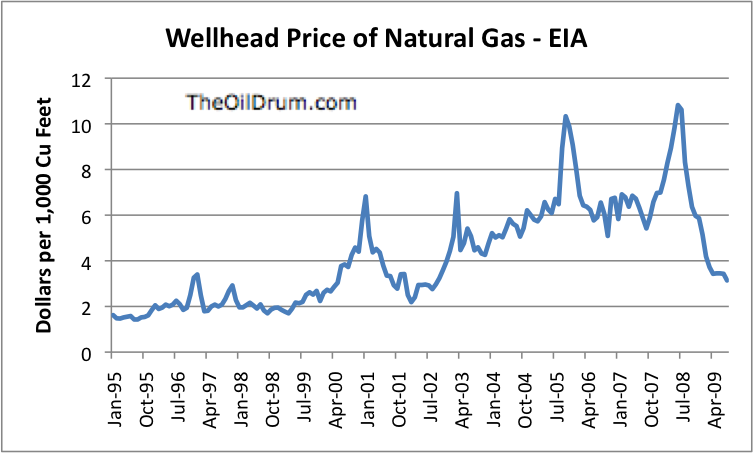

Berman puts the necessary price for operators to earn a reasonable profit at about $9 a thousand cubic foot. One can see from the graph that in the past, prices have rarely hit this level. If the quality of resources goes down over time, the necessary price could rise from this point.

Based on the analysis of Dave Murphy, we have seen recently that it is difficult for the price of oil to go much over $80 without it causing a recession. Natural gas is a smaller part of the economy, but I suspect it still has issues with too high a price being recessionary.

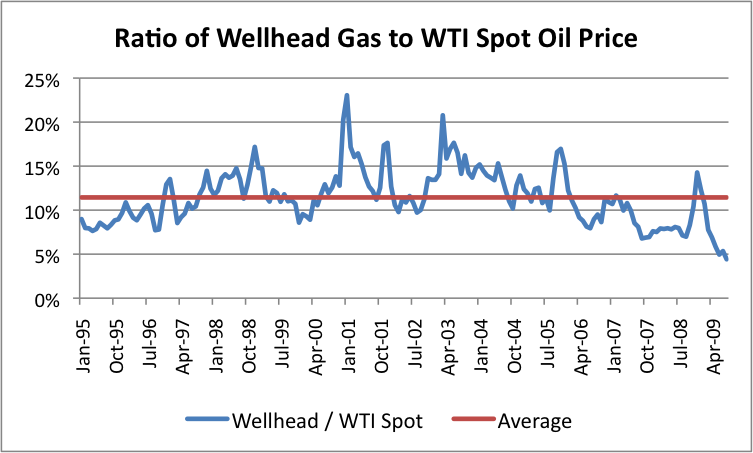

Historically, natural gas wellhead prices have averaged about 11.4% of West Texas Intermediate oil prices. If this ratio holds, one would expect the threshold at which the economy starts reacting negatively to high natural gas prices would be about (11.4% x $80) = $9.12, which is uncomfortably close to what Arthur Berman says is the necessary price for profitability of shale gas. Arguably, the average ratio could be distorted by the high ratios during the periods when there were natural gas shortages, but oil prices were quite low (2001, 2003). But if we choose a lower ratio excluding these points, say 10%, the threshold for gas comes out to (10% x $80) = $8.00 per 1,000 cubic feet.

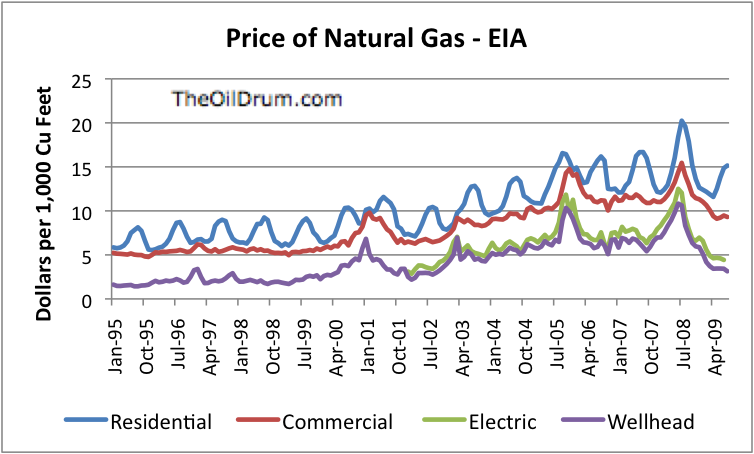

Arguably, the maximum price for gas should be about 1/6 of the price for oil, because its energy content is about 1/6 that of a barrel of oil. But transport and distribution costs for natural gas are higher than for oil, so perhaps the lower empirically derived ratios are reasonable. (The high residential prices during summer reflect the fact that little gas is sold during the summer, but overhead for the companies selling the gas continues. Also, many homeowners opt for level billing all year, to smooth out differences in the amount of fuel used in the summer and winter, and this distorts monthly price per BTU indications.)

There is a second problem with natural gas price. If one ramps up natural gas production, one has to simultaneously ramp up infrastructure for end uses (for example, natural gas busses and fueling stations) plus pipelines and storage to enable the new end uses. If one doesn’t do this, the extra natural gas has nowhere to go, and prices drop precipitously. This is what has happened recently. Adding new infrastructure is slow and expensive, so this may mean that natural gas prices may languish for many years before production and infrastructure finally match (especially if the country is in a recession, and this holds back demand).

At this point, North America really needs to know how much natural gas is producible, and at what price, in order to make good decisions on infrastructure. It doesn’t make sense to add a lot of natural gas infrastructure unless enough natural gas will be available, over a long enough period, to make the investment a reasonable one. If Berman’s calculations are right, not only is quite a high price is needed, but the amount that can be produced is quite a bit lower than other estimates suggest. One really needs to know the right answer.

Obviously, there are individual company issues as well. If long term natural gas production from existing and new wells is expected to be very good, the value of a gas company’s land is much higher. Natural gas companies can borrow more money against the higher value of the land, enabling new investment. The value of the stock is also likely to be higher.

Fortunately, whether or not Berman is writing about the issue, he has raised enough questions that one might expect auditors to be somewhat diligent about the issue this year end.

What are the some of the arguments against Berman’s approach?

Berman, in his blog, quotes a rebuttal by Tudor, Pickering and Holt. This is an excerpts:

Technical credentials. In any technical discussion, one must establish technical credibility. The TPH equity research team is staffed with engineers that have worked at Shell, Tenneco, Arco, Exxon Mobil, reservoir consultant Holditch & Associates and reserve auditor Netherland & Sewell. Dave Pursell has taught petroleum engineering courses at Texas A&M. Not only do our guys know words like non-linear flow and pseudo-steady-state..they actually understand what they mean. We’ve done decline curve work for 10-20 years. Our A&D team on the ibanking side has another group of engineering talent just like us – and they make technical assessments of reserves for a living. We know how to do this type of work.

Depth of analysis on this topic. Within the past six months, we’ve looked at 32 subsegments of US production, including individual analyses of various historical shale results (Barnett, Fayetteville, etc). The culmination of the analysis was our US Natural Gas Supply Study. We’ve got data coming out of our ears…we haven’t published it all (and won’t), but it confirms the technical work being done by literally hundreds of industry folks.

10 Reasons Why Skeptics Are Wrong:

1. Technical stuff matters – The skeptics claim Estimated Ultimate Recovery (EUR) in shales is much lower than stated by industry, analysts and reserve engineers. This is because their decline method is technically flawed and is biased to under-estimate recovery. They suggest that it is appropriate to assume Barnett Shale wells exhibit exponential decline after one year (and not apparent hyperbolic behavior). Reality – it takes many years for a very tight (low permeability) gas reservoirs to exhibit exponential decline behavior. Thus, hyperbolic decline can and should be used to approximate/extrapolate EUR’s. Whew – got through that explanation without a mind numbing discourse of transient vs. pseudo-steady-state flow.

2. Type Curves work – Skeptics further suggest that it is inappropriate to use type curves because it makes the data look smoother than it really is…and suggest that all wells should be analyzed individually. This is wrong for multiple reasons: (1) It is accurate/widely accepted to use normalized curves as long as there is a relatively stable well count and vintage/area effects are accounted for. (2) Projecting individual wells without checking the type curve trends will lead to overly pessimistic projections (see Reason #4). Type curves actually normalize for a negative bias that might be driven by individual well declines. (3) Reserve auditors project EUR’s on a by-well base…supplemented with type curves. Their by-well analysis is consistent with the type curve methods reported by companies. The answer is generally the same either way if the work is done correctly!

3. High Terminal Decline Rate is wrong – Skeptics state that terminal declines will be high in shale plays (>15%). Without 10-20 years of Barnett history (the oldest shale play), this cannot be disproved. However, there are literally thousands of data points (actual well production) that show low terminal decline rates in tight gas reservoirs. Read the technical papers. Look at the data. Enough said.

4. Reality bites – We loaded the skeptics Barnett ~1bcf EUR type curve (which are called optimistic) into our Barnett Shale model. We applied their type curve to the ~3,000 wells drilled in 2008. During 2008, actual Barnett production grew by 1.2bcf.day. The skeptics “optimistic” EUR curve estimated growth of only 0.7bcf.day – which says it underpredicted actual incremental production by 0.5bcf/day or 70%. This is only for one year. If we went back to 2005/2006 and applied the type curve to all Barnett wells drilled, there is NO WAY this low type curve would match actual Barnett production of 5bcf/d. Scoreboard!

Berman also quoted some comments by Chesapeake Energy:

“We do feel like we have the No. 1 resource base in the nation,” said Steve Dixon, Chesapeake’s chief operating officer.

Dixon said Chesapeake’s shale holdings will continue producing for years to come, despite “misguided” predictions from an analyst at an industry conference in Denver earlier this week.

“We’re very confident that these types of rocks will continue to bleed gas for decades and decades,” he said.

Jeff Fisher, the company’s senior vice president of production, said the unique size of Chesapeake’s assets will allow the company to develop new technology to maximize production.

“We’ve achieved great results to date, and we’re just getting started,” Fisher said.

I found an analysis of Berman’s approach by Drilling Info Inc., Energy Strategy Partners, which seems to be better. One of their big concerns is that Berman takes results from the earliest period, and projects them forward. Natural gas companies refine their techniques over time, but this is not really reflected in the analysis.

This post also suggests that the initial wells drilled likely included more marginal producers. These are less likely to continue:

MARGINAL PRODUCER– Unlike conventional reservoirs, the economics of shale plays highly favor operators that invest in engineering and ongoing experimentation in optimizing their drilling, completion, and stimulation practices. The saying “One Man’s Gold is another Man’s Garbage” is especially true for these plays. For an equivalent grade of acreage, the best operators statistically produce 40% or more than the average operator, and up to 4 or 5 times more than an inefficient operator. Learning curves and operator comparisons are real and quantifiable throughout. As acreage expires, and the “land rush” acreages are released, the optimal operators will successfully step into “another man’s garbage”.

THE VOLUMES OF COMMERCIALLY RECOVERABLE RESERVES ARE GREATLY OVERESTIMATED – This is a very definitive statement for which the jury is still out. Mr. Berman is absolutely correct at current drilling and completion costs combined with $2.50 MCFG wellhead price. However, resource turns into undeveloped reserves fairly quickly as wellhead product price goes up or costs come down. Reducing the cost of drilling and completing a well by 50% is the economic equivalent of doubling the lifetime wellhead price. It helps to think of breakthroughs in reducing drill, complete, and stimulation costs as “permanent hedges”. One cannot address any play on wellhead cost alone. We know that there is a 80 to 100 x differential in play reserves between static D,C,&S costs and $7/MCFG at the wellhead and $2.50/MCFG at the wellhead.

HYPERBOLIC PREDICTIONS OVERESTIMATE RESERVES – Mr. Berman is absolutely correct here. This is also usually the case for conventional reserves. Hyperbolic predictions typically provide a ceiling estimate.

CONCLUSIONS – As we discovered when we began analyzing the Barnett, analyzing shale plays is like peeling onions. Once a layer is exposed, another presents itself. Many factors need to be normalized to really address the economics and behaviors of these plays in a predictive sense. Good acreage grade alone is not a recipe for success. Decent acreage grade needs to be combined with strong, holistic drilling, completion, and stimulation practices that are constantly tested for optimization to create a real repeatable recipe for success and large economic reserve accumulation. Great operations equate to better recoverable resources/reserves for these plays, not more operators or even more wells.

Raw data combines good operations with bad, early parts of the learning curve results with later, and good acreage with bad. Making forward-looking predictions of behavior from this soup assumes that every bad habit is propagated forward, and that no operator is better than another. Expanding that conclusion to other plays based on this assumption misses the big picture. What the Barnett is capable of producing is different from what it is producing now. How it can be optimized can only be determined by identifying who is optimizing it and by how much.

Conclusions

To me, the jury is still out on whether Berman’s answer is right. I think the review pointing out that there are likely gains in efficiency between the earliest wells drilled and later wells drilled likely has a point. But this may be mostly reflected in the cost per well, which is being reflected in costs that are easily measurable, and not in the long-term decline curve. It is difficult to know what the impact of large amounts of fracing will be on future production.

The TPH review mentions that long term production of tight gas (such as what I observed at Wamsutter, Wyoming). But this is not really comparable–it is a different rock structure, and did not receive anywhere near the level of fracking that shale gas resources have. Also, as the reviewer from Drilling Info says, the hyperbolic decline estimates provide “ceiling estimates”. So at least that part of the estimate is likely overstated, no matter how much technology improves.

I think it is likely that Berman is fairly close to right, but it would be good to have confirmation from others looking at the question in different ways. Hopefully, with greater diligence by auditors, there will be some convergence with company indications in the not too distant future.

Natural gas is one substance where there really does seems to be a lot of resource available, if the price is high enough. But for the price to be high enough, there needs to be a huge amount of debt based financing available, for all of the players involved: the natural gas companies obtaining the land and doing the drilling; the companies building pipelines and storage; and the companies building infrastructure for end use (adapting busses and cars to natural gas use; building fueling stations; installing natural gas home heating where oil was previously used). It may turn out that inability to obtain debt financing will be a big obstacle to development.

Natural gas policy is one where one really would like to have good information on how much resource is available at what price. One also needs to know what costs would be involved in new infrastructure development, and how many years these need to be amortized over to make the infrastructure worthwhile. There are other issues too–what should we really be using this resource for–chemical uses, fertilizer, commercial vehicle fuel, private passenger auto fuel? Or should we be saving it for use for balancing electrical power, when the wind is not blowing. At this point, I don’t think we really know enough to make good decisions.

If cap and trade legislation is passed, it will encourage use of natural gas over coal for electricity generation. This is yet another possible use for natural gas. But the amount of natural gas we have is likely to not go very far, if this is the use chosen for it. If this use is chosen for natural gas, the amount available for use in other areas (including long-term wind balancing) is likely to be greatly reduced. So this decision needs to be considered with other alternatives, and with total natural gas resource availability.