“Peak oil can be a very tricky topic, the way I talk about it and deal with it at the end of the day is: We need to revolutionize the way we consume and produce energy… We need to really be the leaders in saying: the future for our children and our grandchildren as far as energy consumption and as far as production, it looks like this” with those words Colorado Governor Bill Ritter started his closing speech at the ASPO conference in Denver that took place from 10 to 12 October 2009.

Telling our children and grandchildren where they will draw their heat, electricity and liquid fuels from was not a topic of discussion in Denver. Nonetheless, much information was conveyed on the relationship between the economics crisis and the future of oil. This post is an attempt to summarize the main points on oil and the economy from the conference presentations–concluding that there are three distinct future trajectories as we go forward.

At the Denver conference, world oil production was discussed from both the supply side (what flow rate can be reached) and the demand side (how much can the economy afford). It is really the combination of the two that is important–so I bring together both in this post.

Oil – the supply side – what flow rate can we reach?

An overview of the future of oil at the conference was given by Ray Leonard of Hyperdynamics Corporation (PDF) and Chris Skrebowksi of Peak Oil Consulting (PDF). Ray Leonard who has extensive experience as former Vice President of Yukos in Russia and Kuwait Energy Company in Kuwait, showed that conceptually dividing the world of oil into 3 segments makes sense:

– OPEC controlling 73.9% of world reserves and 44.9% of worldproduction

– The Former Soviet Union (FSU) controlling 12.7% of world reserves and 15.6% of world production

– The Rest of World controlling 13.4% of reserves and 39.5% of production.

This distinction makes sense from a political perspective, as OPEC and the FSU operate under much different political and economic circumstances than the Rest of the World. Ray Leonard estimates that Russian production could theoretically increase by another 4 million b/d with new field developments but that this is unlikely to happen due to the Russian tax system and Russian firms lacking the necessary capital. OPEC is in a similar situation of not being able to expand production due to a lack of capital as International Oil Companies are barred from investing in secondary and tertiary recovery. In Ray Leonard’s words: “Limitation on production level for OPEC is mostly due to politics, lack of motivation, investment level and type of crude; NOT shortage of reserves.” OPEC could hence be increasing production greatly by implementing secondary and tertiary production techniques such as water injection but this possibility is nigh impossible in his view. The division Ray Leonard made between these regions was neatly depicted by Chris Skrebowski in a chart reproduced here.

Ray Leonard showed that production in the Rest of the World peaked in 2002 and by 2008 declined by 7%. With OPEC and Russia unable to increase production significantly due to politics and economics, we are nearing World Peak Oil Production. “Production peak of ultra deep water fields will allow ‘peak’ to be a ‘plateau’ in the coming decade, followed by a sharp fall” according to Leonard. Unconventional production is not set to change this situation, as his expectation is that the contribution of this category of oil will be less than 3 million barrels per day in the short to middle term.

The specific path of future oil production was projected by Chris Skrebowksi using the oil megaprojects approach, wherein all the large fields expected to come on-stream in the next seven years are tabulated and compared with decline rates in current fields. In this approach, only the supply side is taken into account and the demand side is ignored. From that perspective according to Chris Skrebowksi the current plateau will continue until around 2014 when the decline sets in, shown in figure 2 below.

A similar approach was presented by myself in the first update of a new project where I showed a continued plateau with potentially a small increase before the decline starts around 2014. This date is based upon an analysis using a database of individual projects and the assumption that the decline rate will accelerate from 4.5% to 6.5%. The difference between my analysis and Skrebowski’s is that I use a more severe decline rate and also include many more projects. There are around 600 fields in my database versus around 250 in Chris Skrebowski’s, because he did not include smaller fields, hence the term megaprojects. A post on this is in the works with publication due in November here at The Oil Drum.

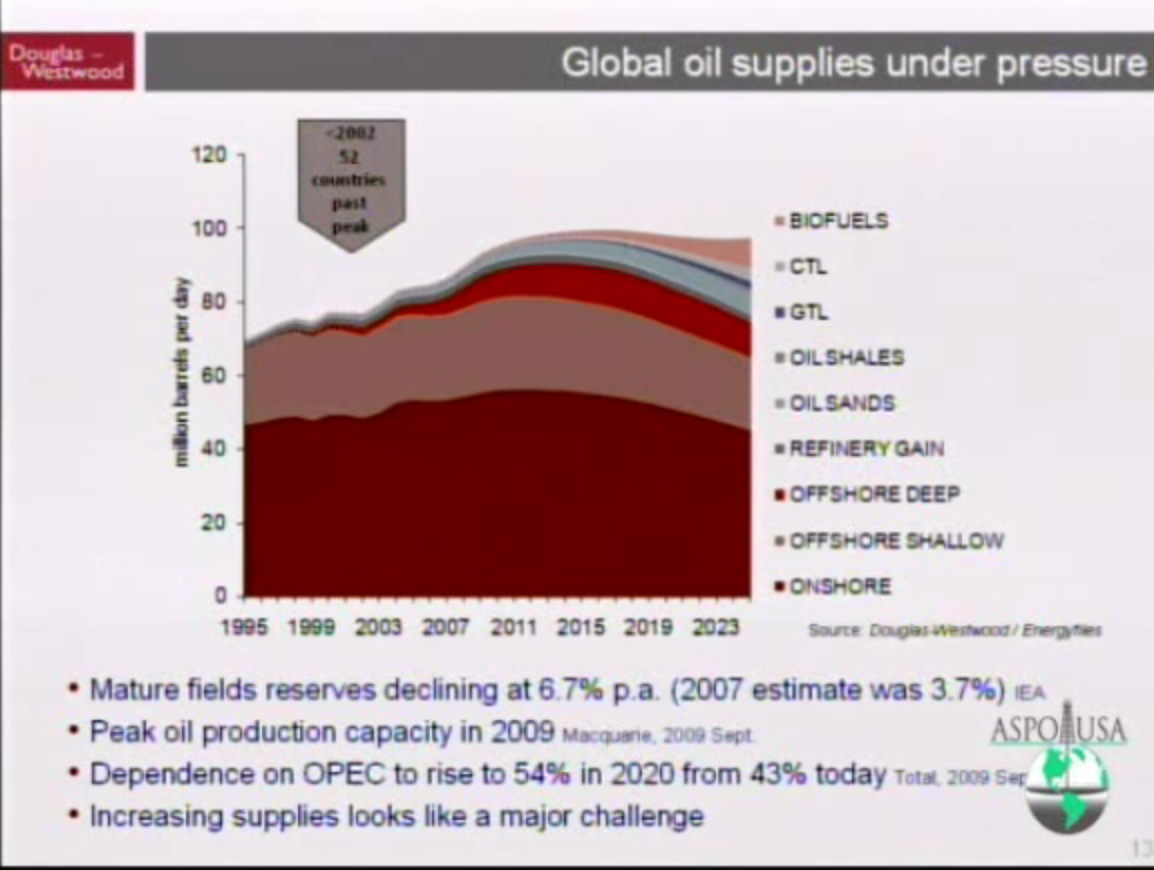

Interestingly another speaker at the conference, Douglas Westwood, presented a similar scenario with a plateau continuing until around 2014, after which the decline sets in:

Such analyses however do not include demand side effects and are therefore limited in portraying an accurate picture of the future. A major factor that was discussed extensively at the conference was fortunately the interplay between supply, demand and prices.

From oil supply analysis to demand analysis – three future trajectories

Steven Kopits from Douglas-Westwood (PDF presentation not available) kicked off the discussion on the role of demand and prices in oil supply by showing that growth in the world economy did not stop despite a lack of growth in oil supply since the fourth quarter of 2004. “Oil supply stopped responding, GDP growth still went up, oil prices rose, and that put us [the United States economy] in a recession, and that’s why I argue that this is the first Peak Oil recession,” according to Kopits. Based on this reasoning, future oil prices will be determined by how quickly demand will again hit oil capacity limits. Kopits thinks that this could happen quite soon, as he foresees huge growth levels in China. The country is expected to overtake the US in oil consumption by 2018, at 21 million barrels of production per day. The general pattern that he presented is that emerging economies will overtake supply from the developed economies of the world. Oil consumption in the latter will be driven down by high prices resulting in increased fuel efficiency and the development of large scale alternatives. “Belt tightening is expected to happen” says Kopits. So in one future possibility a ‘bullish path’ emerges where the pattern we just saw happening repeats itself, emerging economies grow, prices rise and developed economies have to give way and are forced to use less oil. The big question in this future is the amount of growth in emerging economies, most notably China. Allen Stevens, of Stifel-Nicolaus (PDF) showed an interesting graph in his presentation comparing per capita consumption in various countries, showing the huge gap between oil consumption in emerging and developed economies.

The view that Chinese demand will move up so quickly was contested by Michael Rodgers of PFC Energy (PDF) who gave an outlook on future oil & gas production and consumption in China (PDF). Based on their model that included eight categories of oil demand, energy efficiency, solid but slowing GDP growth patterns, and a similar car trajectory as in developed countries, Chinese oil demand was foreseen to hit 11 million b/d by 2015 and slightly more than 12 million b/d by 2020, shown in the figure below.

This slower growth was also portrayed in Dave Cohen of ASPO-USA (presentation found here (PDF). Cohen showed a second type of future with a more protracted economic downturn–either a very long slow recovery with many up and down patterns or a more L shaped depression similar to the great depression of the 1930s. The underlying mechanism for this pattern would be the inter-linkage between the Chinese and United States economy. It is clear that Americans must repair their balance sheets and are in deep debt trouble, but also the Chinese economy is not faring so well according to Dave Cohen. He showed that China’s GDP numbers are inflated because of the way output is calculated, and that recent GDP growth in China is (almost) entirely due to a huge internal governmental stimulus which is not a sustainable economic investment pattern. “The Chinese, traditionally a nation of savers, needs to build up their domestic demand. This requires steady “organic” year-over-year growth over the next decade or longer. Otherwise, the economy overheats and you get mis-allocation of resources (capital) and bubbles (like now),” according to Cohen. He concludes that China will not provide the consumption engine the world economy needs for sustained growth as their economy and domestic demand is too small, and because of these factors, that Chinese oil demand will not grow in the future at the levels seen pre-2008. The implication of these factors is that there will be a much slower return to high oil prices and several cycles of contraction before the world’s balance sheets are again at a reasonable level.

A third possible future which looks at the financial system as the driver of our current situation was shown by Nate Hagens of The Oil Drum (PDF1), (PDF2). Hagens disagrees with Kopits in calling this the first peakoil recession: “I do not think peak oil caused this financial crisis; peak oil is one of many symptoms of an exponential growth based system running into finite limits.” Due to continued exponential growth in our financial system that was not based on accumulating sufficient resources, we have accumulated so much debt that this can no longer be paid off under any scenario. “We have an amazing overshoot of debt, by my calculations the total amount of debt, not derivatives but total debt, is between 230 and 290 trillion dollars…That’s beyond the ability to pay back…Basically we have overextended the relationship between debt and real assets.” according to Hagens. He showed the amount of debt accumulation in the United States shown in figure 8 below, but it isn’t just the United States. “The whole world is around 300% to 400% in debt relative to GDP.”

As money is a claim on future resources, and these resources cannot be forthcoming due to limits of growth, a debt deflationary spiral will ensue, resulting in a downward trajectory of GDP, causing a decline in resource prices that results in further underinvestment in resource production. As the world comes out of this deflationary cycle, the physical resource basis for renewed growth will have degraded significantly, higher prices will kick-in again and GDP will be affected. There was no comment on how long this reinforcing cycle would continue or where it would end. Under this scenario we would have already reached peak prices according to Nate Hagens because the future economy can sustain only much lower prices due to the erosion of resource capital. Conceptually this trajectory is shown in figure 9.

Synopsis – uncertainty over our future path

Although supply side analyses show that oil supply can remain on a plateau until around 2014 and would decline relatively slowly afterwards, the picture may change significantly because of the current disconnect between levels of debt in most economies of the world and the physical resource base. Several future scenarios could emerge as a result of this situation. In one future scenario we will witness continued high oil prices as emerging economies are able to sustain renewed strong growth and thereby outbid developed countries with respect to future oil consumption. The resulting decline in consumption in OECD countries will be relatively smooth as high prices induce massive investment in energy efficiency and alternative fuels. This assumes that such fast growth is possible on the existing physical resource basis and that the current debt situation can be managed in some way. In a second future scenario, we see a much slower growth scenario in emerging economies as they too suffer from overhanging debt and are too interlinked with developed countries to be able to sustain high growth levels. The future will in that case be more like a U shaped or even great depression like L shaped situation; oil (and resource) price cycles will occur with high price volatility and a lack of sustained investment. We can muddle through, but at significant reduction in GDP as huge shocks ripple through the system, and also huge risk of political and geopolitical cascades. In a third scenario, the debt situation has become too big to solve globally, and we enter a deflationary self-reinforcing spiral. GDP will spiral downward, resulting in much less investment in the physical base of our economies. In this scenario, even when the economy recovers, resource scarcity kicks in due to a serious lack of investment, and GDP again declines under the pressure of very high prices.

As to which of these futures (or variants) will occur, I have not made sufficient analysis to offer an opinion, but I am sure that collectively there is sufficient knowledge to point to which direction is most probable.

Thanks to ASPO-USA

I want to expressly thank ASPO-USA for organizing this great conference in Denver which has brought me many useful insights in the relationship between oil and our economy.