Recently, we have had two new articles aiming to put to rest people’s fears about peak oil. One is from the New York Times:

Oil Industry Sets a Brisk Pace of New Discoveries

It talks about the many discoveries this year, and how, if they continue at the pace they have in the first half, they will be the best since 2000.

The other is from the October Scientific American, called

Squeezing More Oil from the Ground.

It is behind a pay wall (you can get it for $5.95). There is also a draft version available on line. Its premise seems to be that there are a lot of promising areas that we have not yet explored. When you put this together with advances in drilling and the promises of secondary and tertiary recovery, there is a good chance that oil production will not peak for many years.

In this post, we will look a little more at these articles, and see why peak oil, and perhaps the financial issues associated with peak oil, are still an issue, regardless of what these articles may suggest.

New York Times Article

A few excerpts from Oil Industry Sets a Brisk Pace of New Discoveries

NY Times:

It is normal for companies to discover billions of barrels of new oil every year, but this year’s pace is unusually brisk. New oil discoveries have totaled about 10 billion barrels in the first half of the year, according to IHS Cambridge Energy Research Associates. If discoveries continue at that pace through year-end, they are likely to reach the highest level since 2000.

Two times 10 billion barrels of oil is 20 billion barrels of oil. Twenty billion barrels of oil divided by 365 is only 54.8 million barrels a day–not nearly enough, if we are currently using 72 million barrels of crude oil a day. If 10 billion barrels is an unusually large amount in the first half, the likelihood of having equal success in the second half by luck is not very good.

NY Times:

While recent years have featured speculation about a coming peak and subsequent decline in oil production, people in the industry say there is still plenty of oil in the ground, especially beneath the ocean floor, even if finding and extracting it is becoming harder. They say that prices and the pace of technological improvement remain the principal factors governing oil production capacity.

There are a lot of issues with difficult to extract oil beneath the ocean floor. While it is theoretically possible for the oil price to be high enough to extract this oil, there is a real issue with too high an oil price (resulting in wholesale oil costs of over 4% of GDP) causing a major recession. Currently, such an oil price is about $80 per barrel. So it is not clear that prices can go enough higher, and stay enough higher, for extraction.

The more difficult to extract oil also has severe challenges in terms of the amount of up front investment needed, and the long time delay before it will actually come to market. For the new very deep ocean “finds’, it could be 10 years or more before we will actually get the oil extracted. By then, our oil needs, if economies continue to grow, will be much higher than today.

NY Times:

Since the early 1980s, discoveries have failed to keep up with the global rate of oil consumption, which last year reached 31 billion barrels of oil. Instead, companies have managed to expand production by finding new ways of getting more oil out of existing fields, or producing oil through unconventional sources, like Canada’s tar sands or heavy oil in Venezuela.

Companies haven’t managed to expand production. Crude oil production has been on a plateau since 2005. That is the problem.

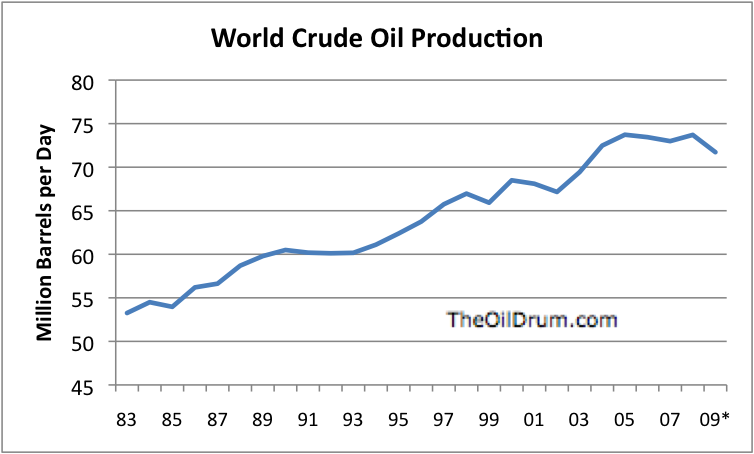

In Figure 1, note that oil production has not risen significantly since 2005. This happened, despite rising prices.

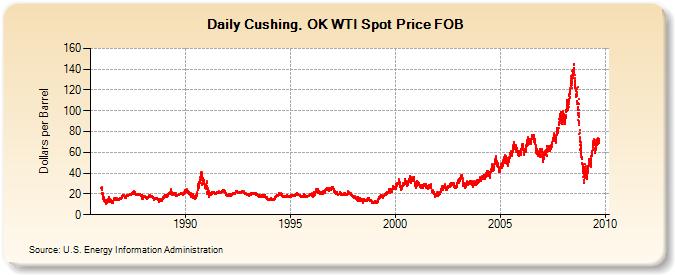

In Figure 2, note that even when oil prices rose far above their historical average price of $20 barrel in the 2003 to 2008 period, oil production in Figure 1 rose very little–virtually none after 2005. In fact, it was the lack of rise in production that was a major driver of higher prices.

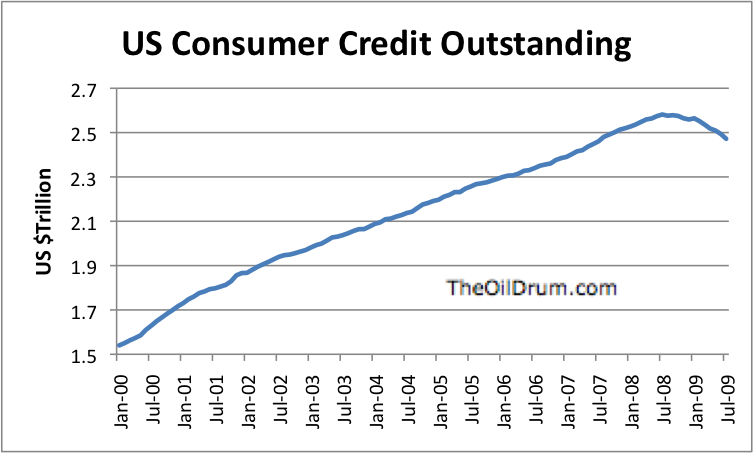

When prices finally dropped, there is significant evidence that it was related to high oil prices indirectly causing problems with credit markets.

In Figure 3, note that US consumer credit reached its peak in July 2008, precisely the same month oil prices reached their peak. Once credit started contracting, purchase of goods that required oil in their manufacture (such as cars) dropped. The drop in oil price reflected the inability of purchasers to continue buying products that used oil in their manufacture. If credit had continued to expand, it is possible oil prices would have continued to rise further, but still with virtually no increase in oil supply.

NY Times:

Reserve estimates typically rise over the life of a field, which can often be productive for decades, as companies find new ways of getting more oil out of the ground.

Maybe, maybe not. We don’t have very good knowledge of reserves around the world. In many places, particularly the Middle East, the reserves seem to be quite inflated. If reserve estimates are starting out from an inflated base, it is doubtful they will increase. They may still be overstated, even with huge improvements in technology.

One of the big issues is whether new technology can be implemented cheaply enough to keep the prices to a level that the consumer can afford. If new technology can only be implemented at $150 a barrel, and the economy starts crashing at $80 or $90 barrel, the new technology really may not be all that useful.

NY Times:

“The industry’s record has improved in recent years, thanks to high prices. According to Cambridge Energy Research Associates, oil companies have found more oil than they produced for the last two years through a combination of exploration and field expansions.

This comment is strange. Cambridge Energy Research Associates (CERA) is part of IHS, and IHS was quoted as saying:

In 2008, world oil reserves declined nearly 3%, primarily due to a 5.2 billion bbl decline in revisions that stemmed from reduced commodity prices.

World oil reserves (excluding oil sands) were 1,261 billion barrels at the end of 2007, according to British Petroleum. A 3% decline would amount to about 38 billion barrels–more than the 20 billion barrels hoped for this year in new discoveries.

Another question is how a 5.2 billion barrel decline (from reduced commodity prices, as stated by IHS) could cause most of this decrease, if we are talking about a $30+ billion decrease. One wonders whether the IHS statement really was intended to apply to some subset of world oil reserves. Perhaps the CERA statement should also be interpreted to apply to some subset of world reserves. It is possible the CERA statement about reserve replacement may also apply to oil and gas reserves on a combined basis, since companies generally give their oil and gas reserves on a combined “barrel of oil equivalent” basis.

These quotes regarding reserves illustrate how difficult it is to interpret statements found in newspapers about reserves. The reporters often don’t understand quite what they are talking about, so the quote doesn’t quite get all of the specifics needed to understand what is being described. If someone wants reserve replacement to sound favorable, he or she can often find a way to word the statement so it sounds good, whether or not the details really add up to an increase.

Price is important in all of this. If the price of oil isn’t high enough, reserves may not be developed. But if the price of oil is too high, it may sink the economy, and the reserves still may not be developed.

Scientific American Article

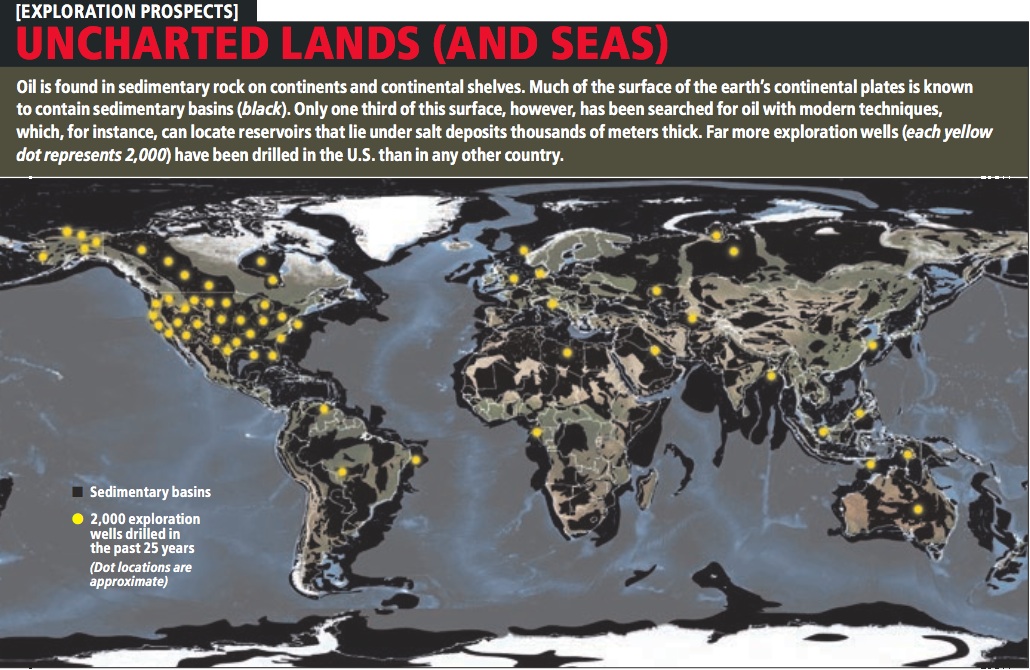

This graphic alleges that much of the world’s oil deposits have not adequately been explored with modern technology. It seems to me that one doesn’t really need modern technology to get at large reservoirs in easy to reach locations. It is only when one is looking for either very small deposits, or deposits in locations that are difficult to extract from that modern technology really is needed. We aren’t likely to find any more Saudi Arabias, whether or not we have fancy new equipment.

The issue that arises with deposits that are in difficult to reach locations, like thousands of feet under the sea, and then under a salt dome as well, is that the oil found in those locations is almost always very expensive to extract. It is hard to believe that even with new technologies that will change–it is the location that makes oil extraction so difficult. New technology may make extraction a little easier, but it is still likely to be expensive.

Scientific American also has a graphic on tertiary recovery techniques. It says:

After primary and secondary recovery have run their course, more aggressive methods, some of them still experimental, can soften the remaining oil so it can flow toward the wells. Because these advanced methods are expensive, the battle to get more out only gets this fierce when resale prices are sufficiently high.

incendiary

Burning part of a reservoir (which requires injecting air underground) enhances the recovery rate in three ways. First, heat from the fire makes oil less viscous. Second, the combustion produces carbon dioxide, which pushes oil out. Third, the fire breaks the larger and heavier molecules of oil, making it more mobile.Chemical

Substances called surfactants, injected into a reservoir, help oil detach from the rock and flow better. Layers of surfactant engulf oil into droplets, similar to the way ordinary soap washes oily materials off a surface. A variation consists of injecting chemicals that generate the soaplike materials from components present within the oil itself.Biological

Experiments are testing the injection of bacteria (together with nutrients and, in some cases, oxygen) that grow in the interface between the oil and the rock, helping to release the oil. The bacteria are allowed to grow for several days before recovery resumes. In the future, genetically engineered microorganisms could partially digest the most viscous oil and thin it out.

Here again, the issue is price. Can these techniques be implemented cheaply enough that they can be used without raising the price of oil so high that the price is beyond what consumers can afford?

More on the Financial Issues Involved

Dave Murphy showed a graphic earlier this year that illustrated the relationship between oil prices and recession. In this graphic, Dave uses retail prices to determine his percentage of GDP. The threshold for retail oil prices seems to be about 5.5% of GDP (equivalent to 4% wholesale). The dollar per barrel cut off for causing a recession seems to be in the $80 to $90 barrel range.

It will be hard to maintain an oil price at a level that sends the US (and the world) into recession. While we usually think of oil production as being limited by geology, it seems to me that the weak link is really finances. What tends to happen is that when the price of oil gets very high, people change their purchasing patterns. People continue to buy oil products, because they need transportation to work. People also continue to buy food, and it also is a heavy user of oil. What people cut back on is expenses that can be deferred–buying a new larger house, buying a new car, going to a restaurant, contributions to charities.

This cutback in expenditures causes recessionary impacts. As things get worse, some debt holders start defaulting on their debt. This might be restaurant owners who have less business, and because of this can’t pay their debt. It might be homeowners with long commutes, who cannot pay both their mortgage payments and the cost of gasoline for their long commutes. It might be governments who cannot collect enough taxes, because of dropping demand (and lower prices) for houses in their suburb. It might be a charity with lower contributions.

Eventually, the debt defaults result in a cut-back in credit like we saw in Figure 3, because of the adverse impact of the debt defaults on lenders. Once there is a cutback in credit, consumers are no longer able to purchase as many cars and other durable goods. These durable goods require oil in their manufacture. With fewer purchases of goods using oil in their manufacture, the demand for oil drops. Because of the drop in demand for oil, oil prices drop again, allowing the economy to recover a bit, as it is doing now.

But as the economy recovers, demand begins to grow again. With the rise in demand, oil prices are likely to rise again to a level where they have an adverse impact on the economy. The world economic system was damaged pretty badly with the last price spike. Another spike could have much more adverse results. Eventually, the world economy may become so damaged by oil price spikes that recovery of the world economy in the form we now know it may not be possible.

I don’t know how this will work out. There could be huge international defaults. The result might be each country more on its own, with much less international trade, because countries would no longer trust each other for credit. Globalization could start unwinding.

How soon such a scenario would might occur is not certain, but it seems to me that a scenario like this, rather than the amount of reserves in the ground, is likely to determine how much oil is ultimately produced. Some countries may be able to keep up production for a while, even with a world financial crisis, but eventually oil producing companies are likely to run into barriers–parts they need for equipment that they cannot obtain, or lack of trained people to perform needed services (because such services were formerly done by an international trade partner).

It would be nice if there were a guarantee that came with oil reserves as currently reported that we really will be able to extract the oil that they represent. It seems to me this will be the case:

(1) If the world economy stays together,

(2) If the price of oil stays in a zone that is neither too high to crush the economy, nor too low to discourage the expensive investment needed for getting the oil out, and

(3) If there are enough investment dollars available, for the sizable front end investment required to produce the oil.

Those are three pretty big “if”s. Without them, it seems like oil production will be very difficult.