Where is our gasoline and diesel supply headed? Even before Ike hit, quite a few areas of the US were starting to see gasoline shortages. The impact of Ike can only make shortages worse. Most likely, it will take refineries at least a week or two to get production back to normal levels after a storm of this type, considering the impacts of electrical outages and flooding. In this article, I will examine some of the issues that seem to be involved. Based on my analysis, fuel supply shortages are likely to last well into October, and are likely to get considerably worse before they get better.

Insight 1. Even before Hurricane Ike hit, inventories were very low.

According to EIA data, gasoline inventories the week that Hurricane Gustav hit were the lowest that they had been since 2000, amounting to 187.9 million barrels, or about 21 days supply. Quite a bit of this inventory is needed just to keep the pipelines filled. EIA does not publish information as to how far inventories need to drop before we start seeing outages, but it is clear that we have now reached the point where shortages are developing.

Insight 2. Friday, September 12, before Hurricane Ike hit, there were already gasoline shortages in some parts of the country. These occurred primarily because of the earlier impact of Hurricane Gustav.

Even though Hurricane Gustav hit on September 1, its impact on petroleum product supplies were not felt immediately, because some inventories were still available, and because it takes a while for shortages to work their way through the pipeline. Gasoline traveling by pipeline from Texas to New Jersey takes an average of 18.5 days to make the trip, so it shouldn’t be surprising that it took 11 days (from September 1 to September 12) for the Hurricane Gustav shortage to start to be felt.

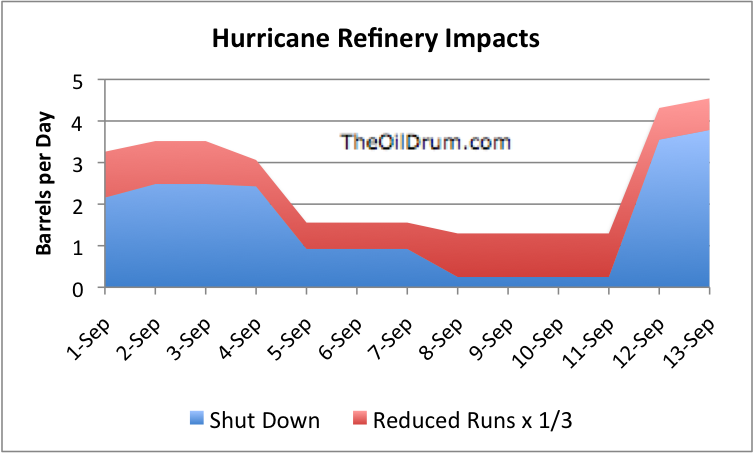

Insight 3. Since Hurricane Gustav hit, there has been a drop in refinery output of 1 to 3 million barrels a day.

The Department of Energy releases daily reports showing the amount of refinery capacity in the hurricane area that is shut in and the amount subject to reduced runs.

We cannot know to what extent runs are reduced. For the purpose of Figure 2, I have estimated that reduced runs have the impact of reducing production by one-third. The amount shown is the graph is a rough estimate of the amount by which refinery production will decrease. It is not exact because:

(1) We don’t know the extent to which production was reduced under reduced runs.

(2) I haven’t adjusted for expected refinery utilization rates, without the hurricane.

(3) The data is only for the hurricane area. It is likely that the hurricanes have changed refinery production elsewhere – some increases (greater use to offset shutdowns) and some decreases (because of unavailable crude).

Insight 4. It is likely that we will have product shortages for at least the next three to four weeks, because of shut in refinery capacity and reduced refinery runs.

We have said that it is likely to take a week or two to get refinery production up to pre-Ike levels. Suppose it takes 10 days. Adding 10 days to the date of the hurricane (September 12) brings us to September 22. If it takes an average of 18.5 days to get product from Texas to New Jersey by pipeline, it will take until approximately October 10 before supplies are back to normal. It could be a little shorter than this, or quite a bit longer.

Insight 5. One of the biggest refined product pipelines, Colonial Pipeline, is now reported to be shut down, because of lack of refined product input.

Colonial pipeline is one of the largest pipelines, with a capacity of 2.4 million barrels a day. It serves the Southeast and the East Coast.

Until Colonial pipeline is back to carrying full capacity of gasoline, diesel, and other refined products, there are likely to be shortages along the gulf coast and the Southeast. The Northeast may also begin to see shortages.

Other major outages have also been reported. Explorer pipeline, carrying 700,000 barrels a day of petroleum products from Texas/LA to Indiana, is completely shut down. Plantation pipeline, carrying 600,000 barrels a day of petroleum products from Louisiana to Virginia, is operating at reduced rates.

Insight 6. The lack of refined product (gasoline, diesel, jet fuel) is what is driving pipeline outages.

Until there is enough refined product, some of the pipelines will be short of products to ship. In the immediate aftermath of Ike, lack of electricity may also interefere with the operation of some pipelines, but it is too soon to have information about these disruptions.

Insight 7. Areas with pipeline disruptions are likely to experience shortages of all refined products, not just gasoline.

While gasoline is the product that is in short supply most quickly because of lower inventories than some other products, eventually diesel and jet fuel can expect shortages as well.

Insight 8. Regardless of whether price or some other type of rationing is used, someone, somewhere will need to go without refined product, if it is not available.

If there is not enough diesel to go around, some trucks will not be able to make deliveries or some road making equipment will not be able to operate. If there is not enough jet fuel for all of the airplanes, some flights will have to be cancelled. Some auto trips will have to be eliminated.

Insight 9. If 5 million barrels of refinery production is taken off-line, this is equivalent to a little over 25% of US refined product usage.

We would hope that the amount of refinery production off-line would drop fairly quickly, but it could be several days before it drops from the current 5 million barrels off-line. It will be impossibile to make up this huge shortage with imports of refined products from overseas, or the use of winter grade gasoline in summer.

Because shortages are likely to vary by part of the country, depending on pipeline service to the area, it is quite likely some areas will experience shortages of 25% for several days, even if loss in refined product declines to “only” a shortfall of 2 million barrels a day, which equates to 10% of current usage. At 10% of current product usage, there would be a shortfall of gasoline of about 910,000 barrels a day.

Insight 10. Because some areas are likely to be very short of supply, it is likely that gasoline prices would need to rise to $10 a gallon or more in those areas, to cut back demand sufficiently.

In some areas, there may be temporary shortfalls of 25% of more of gasoline supply. To allocate such short supplies would take a very high price. Government officials are not likely to let this happen. Instead, we are likely to see many stations that are completely out of gasoline, and other stations with long lines, selling at most 10 gallons per customer.

Insight 11. The lack of diesel, gasoline, and jet fuel is likely to cause feedbacks to the rest of the economy.

If people are forced to cut back on gasoline use, they are likely to cut back considerably on trips to restaurants and other discretionary trips. Restaurants that were doing poorly before will find their business much worse. Restaurants on the brink of bankruptcy may be forced over the edge.

Some people will suddenly find their incomes lower (for example, gasoline station owners who have no fuel to sell; waitresses in restaurants; truck drivers whose trips are reduced). These people will find it difficult to pay their bills, than previously. Some may default on mortgages and credit card debt.

Insight 12. We will all get to see first-hand a little of what the impact of peak oil is likely to be.

When there are shortages of fuel, people can be expected to hoard supplies. This may cause shortages to be worse than they would otherwise be.

Co-operation could go quite a way to solving day-to-day problems. We will get to see to what extent this actually comes into play.

Allocation by price has long been advocated as the American way. We will get to see how long this lasts when there is clearly not enough supply at prices voters consider “acceptable”.