NOTE: Images in this archived article have been removed.

Recently, the IEA published a “Special Report” called World Energy Investment Outlook. Lets’s start with things I agree with:

Recently, the IEA published a “Special Report” called World Energy Investment Outlook. Lets’s start with things I agree with:1. World needs $48 trillion in investment to meet its energy needs to 2035. This is certainly true, if we assume, as the IEA assumes, that world economic growth will actually improve a bit, from 3.3% per year in the 1990 to 2011 period to 3.6% per year in the 2011 to 2035 period. It is likely that the growth in investment needs will be even higher than the IEA indicates.

In my view, this is a CYA report. The IEA sees trouble ahead. There is no way that investment of the needed amount (which is likely far more than $48 trillion) can be met. With the publication of this report, the IEA can say, “We told you so. You didn’t invest enough. That is why energy supply ran into huge problems.”

2. Without reform to power markets, the reliability of Europe’s electricity supply is under threat. The current pricing model, in which wind and solar PV get feed in tariffs and electricity prices for other fuels is set using merit order pricing, produces huge market distortions.

In my view, the problem is even worse than the writers of the report understand. The value of wind and solar PV are inherently difficult to determine, because they produce intermittent supply, and this is not comparable to other types of electricity. Furthermore, a big chunk of costs relate to transmission and distribution–42% of electricity investment costs in the New Policies Scenario. Many well-meaning researchers looked at wind and solar PV and thought they were a solution, but they tended to look at the situation too narrowly.

To look at the situation properly, one really needs to look at the total system cost of generating electricity with intermittent renewables (of a given amount) compared to the total system cost of generating electricity without intermittent renewables. Proper pricing needs to include all of the additional costs involved, including the additional cost for storage, the additional cost for long distance transmission, and the additional costs encountered by fossil fuel providers in ramping up and down their transmission to match changing output from intermittent renewables.

A study by Weissbach et al.(here or here) suggested that wind and solar PV were “an order of magnitude” less effective than fossil fuels, hydroelectric or nuclear, when full costs were considered. Broader analysis also raises questions as to whether there is any real carbon savings from wind and solar PV–did the belief they were helpful just come from underestimating true system costs?

I would raise the question as to whether competitive markets for electricity even make sense. Regulated markets allow the various players to make an adequate return, and allow utilities to collect adequate fees for infrastructure. The overseer can increase or reduce investment of a particular kind, based on the needs of the particular system. I notice a recent Bloomberg article says, Europe Faces Green Power Curbs to Stop Grids Overloading. The current system is clearly working badly.

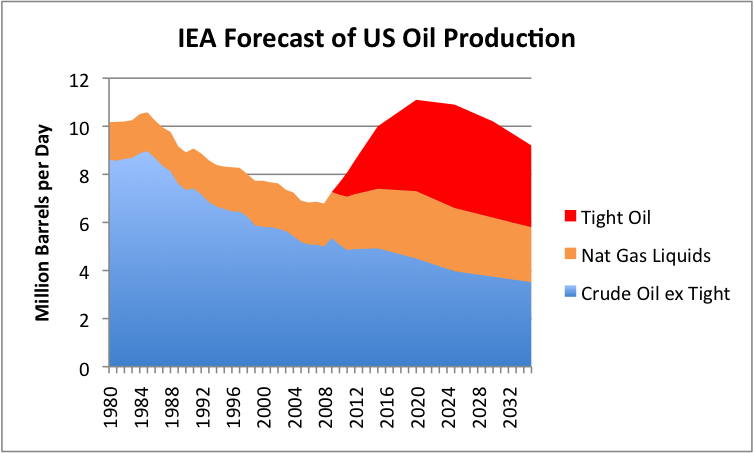

3. Tight oil from shale deposits will need significant supplementation from other sources, if it is to be sufficient to meet our needs to 2035. This is the chart I made from data provided by the IEA in its November 2012 World Energy Outlook, with respect to its New Policies Scenario.

Figure 1. My interpretation of IEA Forecast of Future US Oil Production under “New Policies” Scenario, based on information provided in IEA’s 2012 World Energy Outlook.

The current report is not intended to be a report regarding future oil production, but one highlight is, “Meeting long-term oil demand growth depends increasingly on the Middle East, once the current rise in non-OPEC supply starts to run out of steam in the 2020s.” This implies that not only is US tight oil not going to solve our problems, neither will tight oil elsewhere. Instead IEA is back to its old plan of “calling on OPEC”–hoping that the Middle East is there to help, if no one else is around. This is wishful thinking–something I will discuss later.

4. IEA’s investment report is one documenting diminishing returns, even though it never uses that term. Diminishing returns take place if society is becoming less and less efficient at producing energy products. For oil, the issue is that the easy to extract resources were pulled out first; we must now move on to more difficult to extract resources. For electricity, the issue is that the old resources produced too much carbon; we must now move on to higher-priced approaches that (hopefully) produce less carbon.

We can see diminishing returns many places in the report. The major point of the report is that investment costs are expected to rise faster than either the amount of oil or the amount of electricity produced. There are other more specific statements, too. In US tight oil, “High production rates mean that resources are rapidly depleted, with a corresponding rise in costs per barrel as operators move out of the sweetspots to areas where the recovery per well is lower”(page 65). EU will need prices higher than today’s prices for LNG transported from America (page 76). In refineries, the drive is toward more complex and expensive technologies (page 77). There is a steady upward trajectory of the oil prices in the New Policies Scenario (page 81). Offshore wind is expected to move farther offshore, with higher expected costs (page 104).

The point that the IEA does not seem to understand is that diminishing returns affects buyers’ ability to pay higher prices for products. The IEA assumes that buyers will be able to pay higher prices (than the general rise in inflation) for energy products, without it adversely affecting the economy. This clearly isn’t true because salaries do not rise to match the higher cost of energy products. Buyers will cut back on discretionary goods, when energy prices rise. This leads to layoffs in discretionary sectors and quite possibly recession. It also leads to higher default risk.

In fact, wages tend to drop from diminishing returns, because workers are becoming, in some sense, less efficient and thus producing less goods per hour of work. Joseph Tainter inThe Collapse of Complex Societies says that diminishing returns were what led to the collapse of ancient civilizations.

Points of Disagreement

1. Many OPEC countries which hold the largest, lowest-cost reserves are deliberately limiting their production rates so as to keep reserves for the longer term. This is common misbelief, repeated by the IEA, but it not true.

The true cost of production in the Middle East is not just the cost of pulling the oil out of the ground. Instead, one has to look at the full cost of the entire system needed for the extraction, including whatever costs are needed to pacify the people in the area, plus whatever costs are needed for additional infrastructure. Even if Iraq can in theory ramp up oil production, this does not automatically happen. Even if Libya can in theory ramp up production, we shouldn’t expect fighting to stop tomorrow. With these costs, the cost per barrel is up close to, or above, today’s oil cost.

Saudi Arabia publishes high reserve numbers, but there is no indication that Saudi could, if they wanted to, greatly ramp up production. Saudi’s big recent addition was 500,000 barrels a day of refinery capacity in 2013, so that it could make use of heavy, polluted oil from Manifa field, that was supposedly part of its “spare capacity.” An additional 400,000 barrels a day at the same facility is supposed to come on line in 2014. There are declines going on elsewhere, so it is not clear that even these additions will actually add to its total oil production. Saudi Arabia’s total output was slightly lower in 2013 than in 2012, according to the EIA.

The Saudi “proven oil reserves” are unaudited numbers. Its big oil field is Ghawar, producing something like 5 million barrels a day. We don’t know how long it can continue producing. We know that horizontal wells can keep production from declining for a while, but that if a drop-off comes, it is likely to be more severe than with vertical wells. If Ghawar production starts declining significantly, world oil production is likely to drop.

We know that Saudi Arabia has some heavy oil it can in theory develop, not that different from Canadian oil sands or Venezuelan Oronoco belt heavy oil. Such oil would require large front-end investment and flow very slowly. According to the Wall Street Journal, “That the Saudis are even considering such a project shows how difficult and costly it is becoming to slake the world’s thirst for oil. It also suggests that even the Saudis may not be able to boost production quickly in the future if demand rises unexpectedly.”

2. It makes sense to find new sources of investment that will provide funds at lower rates for energy project finance. The report talks trying to find new sources of investment for energy projects other than the traditional source. In particular, it mentions the possibility of tapping funds held by institutional investors (pension funds, insurers, sovereign wealth funds and so on). Pensions and insurance companies are of course currently involved by holding stocks and bonds of oil and other energy companies.

The reason why new sources of lending are needed (besides the problem with high costs) is that the fact that prior sources are getting burned out at the same time huge amounts of new lending are needed. Governments used to be sources of funds, but can no longer be taken for granted (page 38). Changes in Basel III rules make it harder for banks to make long-term energy loans, without charging higher rates (page 39). Quite a bit of the lending in the future will be need to be to developing countries (see Figure 2 below). Many who have lent to developing countries in the past have suffered losses (page 39). With respect to oil projects, there are many examples where oil companies have made big investments, with virtually no return, such as Kazakhstan oil (page 81).

Figure 2. Energy investment required by part of the world–IEA exhibit.

Perhaps sovereign wealth funds, if they feel that the risk is appropriate, can lend in situations where past experience suggests prudence is needed. But with a background in the insurance industry, I am not sure that makes sense for insurance companies and pension funds to get into financing ports in Iraq, refineries in India, or long distance transmission lines to offshore wind turbines. If they do, it needs to be as part of program where adequate risk premiums are included in the interest rates, and the risk is distributed over a large number of participants using bonds or securitization of some form. It seems like an intermediary such as a bank would need to be involved.

The big interest in those writing the report is getting costs down for the borrowers. If risk is going up, it is not at all clear that interest rates should be going down. Furthermore, developing an undeveloped country using $100 barrel oil is far more difficult than developing an undeveloped country using $20 barrel oil. This is a big reason that financing debt in undeveloped countries doesn’t work well.

Comment

What the IEA has inadvertently stumbled upon is the reason why oil limits are a problem, and in fact, the reason why energy limits in general are a problem. It looks like there are plenty of resources available and plenty of ways to reduce energy use through mitigation. In fact, it becomes to impossible to finance everything that needs to be done.

An energy-providing device, or an energy-saving mitigation, requires up front payment. This payment reflects the fact that oil and other scarce resources (high priced metals, for example) need to be used in creating these devices. Oil and other scarce resources need to be used in developing new oil, gas and coal fields and power plants as well. This puts pressure on both debt markets and on scarce resources. At some point, the use of scarce resources becomes too great, and debt needs become too high. The projects with high up-front costs are among the worst contributors.

The plan to keep adding more and more debt doesn’t work. The economy is growing too slowly. People’s salaries are not rising to match the higher costs involved. The locations where the debt is needed are not in the part of the world with adequate banking services. It is the inability to finance all of the investment that is needed that will bring the system down. Resource scarcity will be behind the scenes, playing a role as well, but its problems will be hidden behind the problems of financing the needed energy investments.