The National Petroleum Council is due to report today on a study requested by US Energy Secretary Bodman (the webcast of the presentation this morning can be found here, though it’s badly edited. E.g., one has to wait 15 minutes to hear Mr Raymond begin speaking). Here are some of my concerns about it.

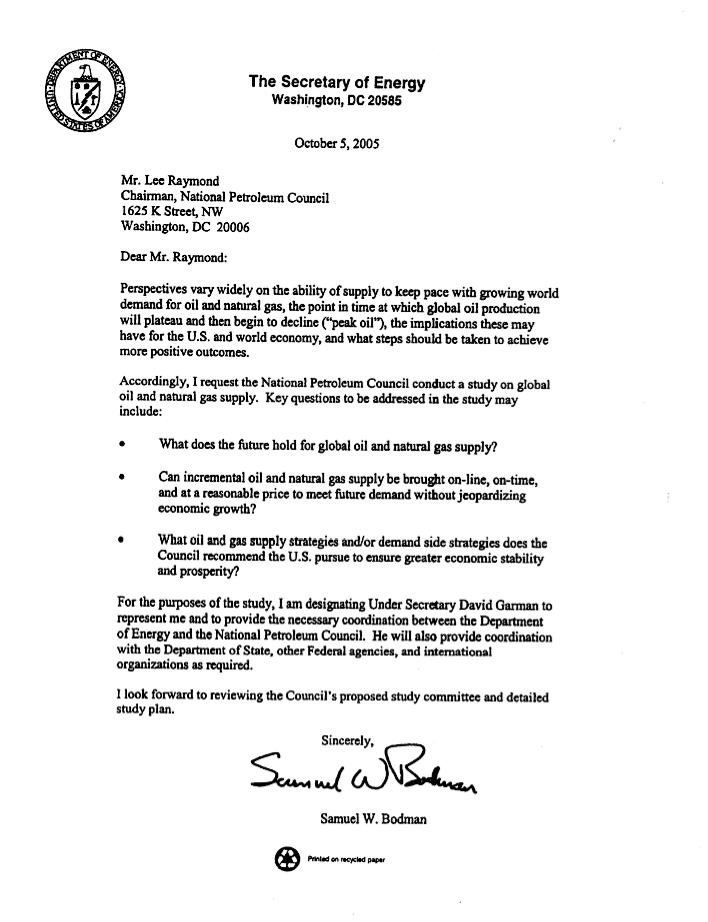

Firstly, let’s look at what Secretary Bodman asked the NPC to do. I obtained a copy of his letter here, and it looks like this:

A pretty sensible straightforward sort of letter, and I’m glad my elected officials are asking these kinds of question. However, the folks they asked it of have this mission:

The National Petroleum Council (NPC), a federally chartered and privately funded advisory committee, was established by the Secretary of the Interior in 1946 at the request of President Harry S. Truman. In 1977, the U.S. Department of Energy was established and the NPC’s functions were transferred to the new Department. The purpose of the NPC is solely to represent the views of the oil and natural gas industries in advising, informing, and making recommendations to the Secretary of Energy with respect to any matter relating to oil and natural gas, or to the oil and gas industries submitted to it or approved by the Secretary.

Ok, so we’re asking the oil and gas industry, who make their living by selling us oil and gas, whether there might any problem with the supply of oil and gas. I don’t know what Secretary Bodman was expecting, but in his place I would have expected to get a sales pitch for buying more oil and gas. Given that very low expectation, the report is better than one might have feared. However, it’s still pretty biassed, and fails to address the Secretary’s questions.

An aside to Secretary Bodman: next time try the National Academies.

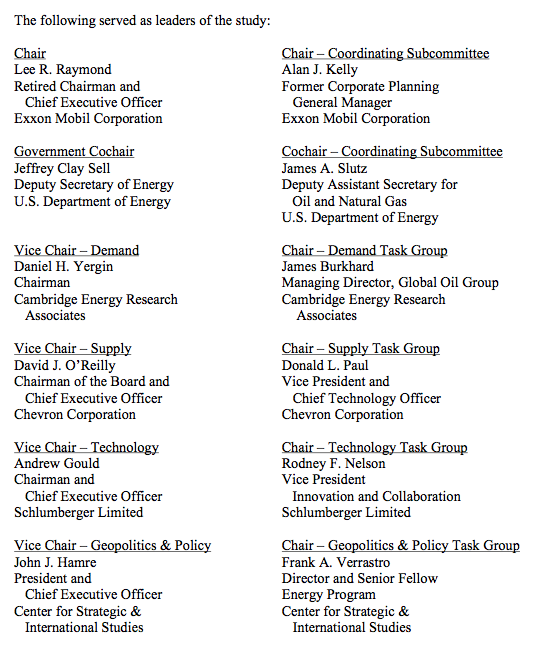

Anyway, continuing, the NPC put together a crack team of industry executives and consultants to answer the question of whether they could continue to deliver us enough oil and gas or not. (I should note here that my comments are based on a June 29th draft of the Executive Summary. I was one of the hundreds of persons consulted by the NPC, though not one of the ones who they paid much attention too, it seems. I’m assuming the final version will be on their website by the time you read this).

Here’s the folks who ran the study:

It is not very long since Mr Raymond was heading up an ExxonMobil that was taking out large editorial page ads in the New York Times arguing that peak oil would not occur for decades to come. And nor is it long since Mr Yergin was telling us that

There will be a large, unprecedented buildup of oil supply in the next few years. Between 2004 and 2010, capacity to produce oil (not actual production) could grow by 16 million barrels a day — from 85 million barrels per day to 101 million barrels a day — a 20 percent increase. Such growth over the next few years would relieve the current pressure on supply and demand…

While questions can be raised about specific countries, this forecast is not speculative. It is based on what is already unfolding. The oil industry is governed by a “law of long lead times.” Much of the new capacity that will become available between now and 2010 is under development. Many of the projects that embody this new capacity were approved in the 2001-03 period, based on price expectations much lower than current prices….

But at least for the next several years, the growing production capacity will take the air out of the fear of imminent shortage. And that in turn will provide us the breathing space to address the investment needs and the full panoply of technologies and approaches — from development to conservation — that will be required to fuel a growing world economy, ensure energy security and meet the needs of what is becoming the global middle class.

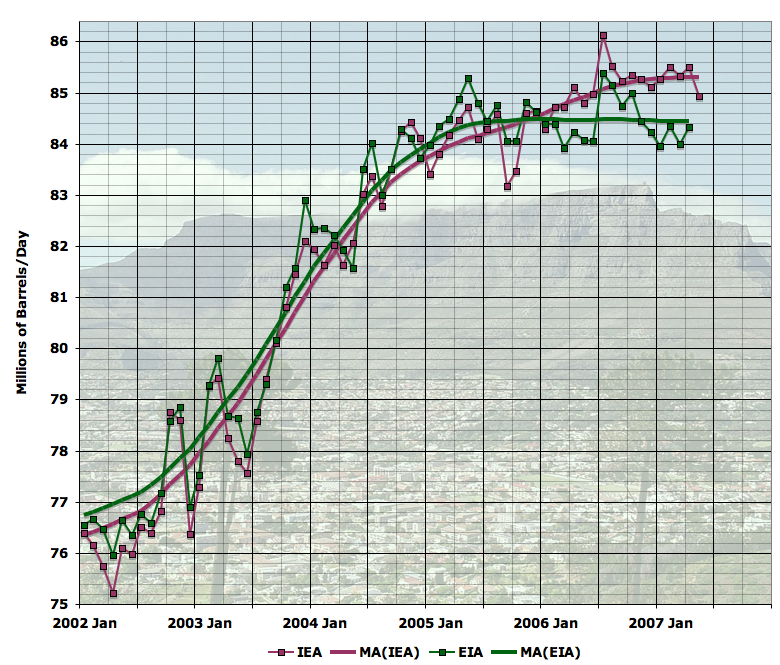

Well, the “not speculative” forecast, made in July 2005, is not looking too good so far:

Of the 16mbd of new capacity over five years, after two years we have seen somewhere between zero (EIA), or 1mbd (IEA) of new production. Not a good start, and it certainly hasn’t been enough to “take the air out of the fear of imminent shortage” as Mr Yergin promised us.

So you get the idea: the NPC put together a team who have a track record of being relentlessly overoptimistic, and the absolute trailing edge of concern about oil supply issues. What did they have to say?

During the last quarter-century, world energy demand has increased about 60 percent, supported by a global infrastructure that has expanded to a massive scale. Now, most forecasts for the next quarter-century project a similar percentage increase in energy demand from a much larger base. Oil and natural gas have played a significant role in supporting economic activity in the past, and will likely continue to do so in combination with other energy types. Over the coming decades, the world will need better energy efficiency and all economic, environmentally responsible energy sources available to support and sustain future growth.

Fortunately, the world is not running out of energy resources. But many complex challenges could keep these diverse energy resources from becoming the sufficient, reliable, and economic energy supplies upon which people depend. These challenges are compounded by emerging uncertainties: geopolitical influences on energy development, trade, and security; and increasing constraints on carbon dioxide emissions that could impose changes in future energy use. While risks have always typified the energy business, they are now accumulating and converging in new ways.

The National Petroleum Council (NPC) examined a broad range of global energy supply, demand, and technology projections through 2030. The Council identified risks and challenges to a reliable and secure energy future, and developed strategies and recommendations aimed at balancing future economic, security, and environmental goals.

The United States and the world face hard truths about the global energy future over the next 25 years:

- Coal, oil, and natural gas will remain indispensable to meeting total projected energy demand growth.

- The world is not running out of energy resources, but there are accumulating risks to continuing expansion of oil and natural gas production from the conventional sources relied upon historically. These risks create significant challenges to meeting projected energy demand.

- To mitigate these risks, expansion of all economic energy sources will be required, including coal, nuclear, renewables, and unconventional oil and natural gas. Each of these sources faces significant challenges – including safety, environmental, political, or economic hurdles – and imposes infrastructure requirements for development and delivery.

- “Energy Independence” should not be confused with strengthening energy security. The concept of energy independence is not realistic in the foreseeable future, whereas U.S. energy security can be enhanced by moderating demand, expanding and diversifying domestic energy supplies, and strengthening global energy trade and investment. There can be no U.S. energy security without global energy security.

- A majority of the U.S. energy sector workforce, including skilled scientists and engineers, is eligible to retire within the next decade. The workforce must be replenished and trained.

- Policies aimed at curbing carbon dioxide emissions will alter the energy mix, increase energy-related costs, and require reductions in demand growth.

So, we could summarize this as “Peak oil is nowhere in sight; we think we can continue to grow oil supply in coming decades as we have in recent decades, but it’s getting trickier and you a) better be prepared to grant all our various requests for assistance in pulling it off, and b) should start trying to use less of our products in case we can’t quite manage it”.

So this is undoubtedly some kind of progress. The fact that the trailing edge of the debate is now officially calling for efficiency and conservation measures is a big deal and good progress. But I still think these guys are a long way from making contact with reality. CEO’s are supposed to set impossible goals and then exhort the troops to meet them, and that’s what we have here, I think, from this group of oil company CEO’s.

My bias is to look at the graphs and tables rather than the words. There aren’t too many in this report, but the ones they do have are very revealing.

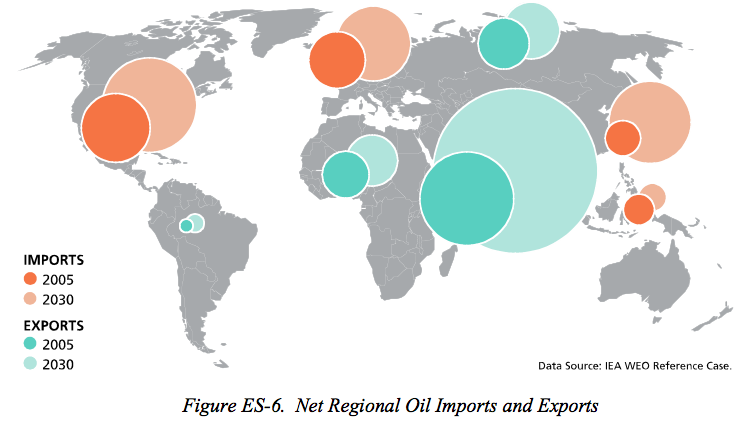

Middle East Reserves

A major concern with the NPC report is its failure to take seriously the potential concerns with Middle Eastern oil reserves. As figure ES-6 of the Executive Summary makes clear, almost all the growth in oil export capacity that the report assumes by 2030 is anticipated to come from the Middle East:

Note that Asia, North America, and Europe all grow their imports significantly, while Latin America, Africa, and Russia increase exports only slightly. The Middle East is required to increase exports massively to balance the books. This is no doubt predicated on the claims that two-thirds of the world’s oil reserves are in that region (eg see the BP Statistical Review of World Energy 2007. However, it needs to be realized that there are serious long-standing concerns about whether these reserves exist in the amounts claimed. For example, in the 2005 World Energy Outlook, the International Energy Agency writes on pages 125-128:

There are doubts about the reliability of official MENA reserves estimates, which have not been audited by independent auditors…

MENA proven oil reserves increased sharply in the 1980s and, after a period during which they hardly increased, rose further around the turn of the century. From around 400 billion barrels at the start of the 1980s, reserves ballooned to almost 700 billion barrels by 1989 and reached nearly 800 billion barrels at the end of 2004… Most of these increases occurred in the Middle East. In the second half of the 1980s, Saudi Arabia and Kuwait revised their reserves upwards by about one-half. The United Arab Emirates and Iraq also recorded large upward revisions at that time. Total Middle East reserves jumped from 398 billion barrels in 1985 to 663 billion barrels in 1990. As a result, world oil reserves increased by more than 40%.

This dramatic and sudden revision in MENA reserves has been much debated. It reflected partly the shift in ownership of reserves away from international oil companies, some of which were obliged to report reserves under strict US Securities and Exchange Commission rules. The revision was also prompted by discussions among OPEC countries over setting production quotas based, at least partly, on reserves. What is clear is that the revisions in official data had little to do with the actual discovery of new reserves. Total reserves in many MENA countries hardly changed in the 1990s. Official reserves in Kuwait, for example, were unchanged at 96.5 billion barrels (including its share of the Neutral Zone) from 1991 to 2002, even though the country produced more than 8 billion barrels and did not make any important new discoveries during that period. The case of Saudi Arabia is even more striking, with proven reserves estimated at between 258 and 262 billion barrels in the past 15 years, a variation of less than 2%.

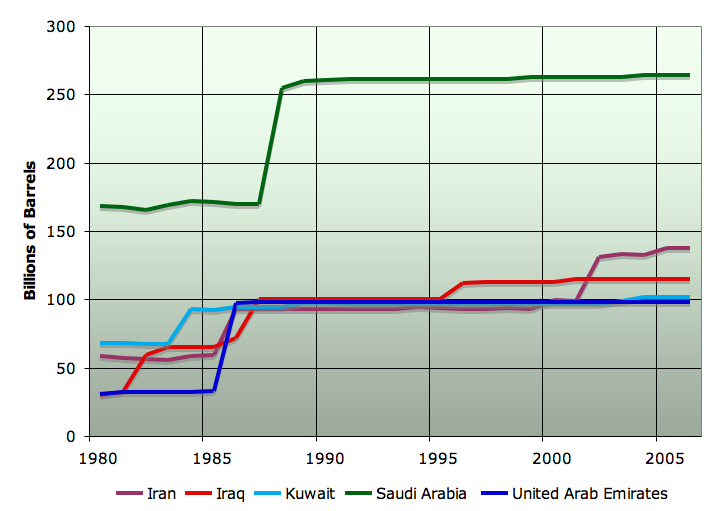

The reserves data for the five main Middle Eastern oil producing countries are shown in this next graph:

This clearly shows the very strange pattern of reserve updates, which is quite unlike reserve histories in western countries that wander up and down year-by-year as oil is consumed and new discoveries are made and additional recovery projects are implemented.

Recently, data is starting to come to light that suggests that not all these reserves additions were appropriate. For example, in 2006, Petroleum Intelligence Weekly obtained a 2001 document from the Kuwait Oil Company which suggested that remaining proven oil reserves there were only about half of the official number. This has now been confirmed by the Kuwaiti Oil Minister, with the Kuwait Times reporting earlier this year: “Sheikh Ali also confirmed to Al-Wasat newspaper that the state’s proven oil reserves have fallen to 48 billion barrels, as reported last year by Petroleum Intelligence Weekly, down from an announced 100 billion barrels.”

In the case of Saudi Arabia, concern that future production would be limited has existed since at least 1979, when a Senate Subcommittee Staff report on the subject stated, after extensive interviews with the American oil company executives managing the country’s fields at that time:

Saudi Arabia’s decision to cut back its producing target to 12 mmbd was significantly influenced by the conclusion that higher production rates would require costly investments and might not be maintained for a period of time acceptable to Saudi Arabia. The oil production level that can be maintained until it begins to decline to lower levels is known as the “production plateau.” The plateau that the Arabian American Oil Company (Aramco) now uses as a basis for its planning indicates that a rate of 12 mmbd may last 15-20 years before irreversibly declining, a period Saudi Arabia now finds uncomfortably short. Higher rates, such as 16 mmbd, could only be maintained for a shorter period of time before declining. Moreover, the prospect of future discoveries in Saudi Arabia is highly uncertain. In addition, technical problems have complicated the management of the oil fields since the early 1970’s. Taking into account all these factors, it would be imprudent for the United States to plan on a change in Saudi Arabian oil development plans to increase long-term production above 12mmbd. The current plan of a target capacity of 12 mmbd achieved no earlier than 1987 is a considerable change from an earlier one which envisioned a capacity of 16mmbd in 1983.

In fact, due to a combination of lower production (via the demand collapse of the 1980s), and technology that allows oil operators to both increase recovery and maintain plateau until a field is more deeply depleted, Saudi Arabia has still been able to produce over 9mbpd in recent years, more than 25 years after the words above were written. However, is it at all prudent to assume that now, at this late stage, production can be increased significantly more than was thought feasible in 1979, and continue for decades more? That is what the NPC report would have you believe.

More recently, Matt Simmons, in his book Twilight in the Desert has documented in great detail that extensive exploration efforts have only found modest amounts of new oil discoveries, just as Aramco executives predicted in the late 1970s. Thus Saudi production still comes from the same handful of giant fields it was coming from in 1979, most of which are now quite mature. In particular, recent research here at The Oil Drum has shown that the northern half of Ghawar, which historically accounted for 4mbd of Saudi production, is significantly more depleted than Saudi Aramco has revealed, and production from this part of the field cannot be maintained much longer at recent levels. This raises the question of whether the development of other fields that Saudi Arabia is now undertaking will be sufficient to increase overall capacity, or only offset declines in north Ghawar. This may be in part why Saudi Arabia has not been able to increase production since 2004, which has had a great deal to do with the fact that global oil production has not increased appreciably in the last two years.

It seems to me that this issue is of central importance to global oil reserves and production capacity. Given the fact that most of the relevant data are closely held state secrets of the countries in question, I can see that reasonable people might hold a different view than me about the amount of oil remaining in the Middle East, and the potential for production increases. However, the fact that the issue is not even flagged to the reader of the executive summary of the NPC report suggests the degree of bias that pervades that document.

Reliance on Undiscovered Oil

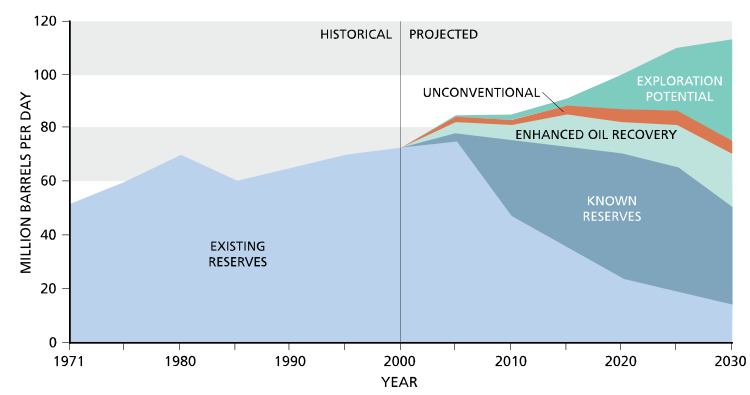

Not only is much of the growth in oil anticipated to come from the Middle East, where it is unclear whether the oil exists, and whether the region will be stable enough to produce it, but it is also mainly not yet discovered:

As you can see, the growth in total liquids supply comes by and large from about 40mbd of “Exploration Potential”. Now, to put this in context OPEC liquids production at the moment, according to Table 16 of the OPEC Monthly Oil Market Report (PDF)) is just around 30mbd. So the NPC wants us to believe that there is a whole other OPEC plus a third waiting to be discovered.

If that doesn’t sound too likely to you, you’re not alone. The ASPO curve for the trend in oil discoveries shows a peak back in the 1960s, with gradual downtrend ever since:

So in summary, the NPC report is saying that production will increase by around 25% over the next twenty five years, but this increase is entirely reliant on finding large amounts of new oil, mainly in the Middle East. Unfortunately, it is rather unlikely that the existing claims of oil reserves in the Middle East are true, and even less likely that massive amounts more oil can be found there. Even if it could, the Middle East is the least politically stable region of the world, and relying ever more heavily on it for critical inputs to our economy is likely to be fairly painful at regular intervals.

However, their number one recommendation on the demand side is:

Based on a detailed review of technological potential, a doubling of fuel economy of new cars and light-trucks by 2030 is possible through the use of existing and anticipated technologies, assuming vehicle performance and other attributes remain the same as today. The 4 percent annual gain in CAFE standards starting in 2010 that President George W. Bush suggested in his 2007 State of the Union speech is not inconsistent with a potential doubling of fuel economy for new light duty vehicles by 2030. Depending upon how quickly new vehicle improvements become incorporated in the full fleet average, it should be possible to lower U.S. oil demand by about 3-5 million barrels per day by 203014. Additional fuel economy improvements would be possible by reducing vehicle weight, horsepower, and amenities, or by developing more expensive, step-out technologies.

That’s something I can heartily agree with, and it’s great to hear the oil industry calling for a doubling of fuel economy.